Summary:

- The completion of the third Vogtle nuclear plant expands zero-carbon generation in the Southwestern Power Pool.

- NextEra Energy benefits from Mountain Valley Pipeline completion both in ownership & gas availability for generation. Through NEER, it is also a major project developer for wind and solar power.

- NextEra has a solid, growing utility base serving its Florida customers via its FPL division.

ANPerryman/iStock via Getty Images

I am upgrading low-beta (0.46) NextEra Energy (NYSE:NEE) from hold in my previous report to buy for growth investors on the basis of several factors. NextEra has two primary parts: its Florida utility business (FPL) which serves 5.8 million customer accounts (about 12 million people) and its national renewables energy project business, NextEra Energy Resources (NEER).

Investors should note, however, that because of its relatively low dividend (2.8%) yield-seekers may prefer, for example, short-term Treasuries.

While $137.4 billion-market cap NextEra Energy pays a small dividend, is subject to higher financing costs as interest rates stay elevated and has seen its renewables projects pipeline slow in part due to solar panel origin sanctions,

a) it achieved a breakthrough on long-awaited Mountain Valley Pipeline, in which it has a 31% interest. This 2 BCF/D gas pipeline will liberate available, inexpensive Appalachian gas to serve the US East Coast and even Gulf Coast LNG projects.

b) NextEra’s underlying FPL business continues strong as Florida remains one of the country’s most attractive permanent destinations. Over the past year the state created new 412,000 private sector jobs and its unemployment rate dropped to 2.6%.

c) Solar-origin sanctions are now a known factor, incorporated into expectations.

d) US government energy budgets prioritize the clean energy projects in which NEER specializes.

e) Natural gas prices, from which FPL generates much of its electricity, have moderated from last year.

f) Baseload nuclear-generated (zero-carbon) electricity may also be more available through Southern (SO) and the Southwest Power Pool via the recent onstreaming of 1100-megawatt Vogtle unit 3 in late 2023 and eventual onstreaming in 2024 of similarly sized Vogtle unit 4.

Second Quarter 2023 Results and Guidance

Next Era reported second quarter 2023 net income of $2.8 billion, or $1.38/share compared to 2Q22 net income of $1.4 billion or $0.70/share.

Adjusted 2Q23 earnings were $1.77 billion or $0.88/share compared to $1.6 billion or $0.81/share for 2Q22. The bulk of the difference between GAAP and adjusted earnings was due to gains associated with non-qualifying hedges.

Dividing the adjusted earnings of $1.8 billion: FPL reported adjusted earnings of $1.15 billion and NEER reported adjusted earnings of $781 million.

Company management forecasts adjusted 2023 EPS to be between $2.98-$3.13 and adjusted 2024 EPS to be between $3.23 and $3.43. Beyond 2024 the company expects an annual growth rate of 6-8% off the 2024 level, rising to an estimated $3.63-$4.00 by 2026. NextEra also expects to grow dividends per share 10%/year through at least 2024 off a 2022 base.

In its investor call, the company noted that it plans to sell non-strategic (for it) Texas pipelines that deliver 25% of Mexico’s natural gas via Pemex.

On the development side, NextEra Energy Resources’ backlog is about 20 gigawatts (GW) after adding almost 1.7 GW (primarily solar but also some wind and storage) and putting over 1.8 GW in service.

Mountain Valley Pipeline

Mountain Valley Pipeline began in 2014 as a joint venture between EQT (EQT) and NextEra. EQT’s interest is now owned by Equitrans (ETRN), operator at 48%, with NextEra holding 31%, Consolidated Edison (ED) Transmission 10%, and WGL Midstream 10%, and RGC Midstream 1%. MVP will carry 2 BCF/D (2 million dekatherms/day). The joint venture finally recently received a US Supreme Court go-ahead and expects to finish the last 6% of construction by the end of 2023.

Because completion previously looked so uncertain, NextEra took substantial write-offs–including $800 million in 2022–on its MVP investment. It may be able to reverse at least some of these.

Macro

The Florida state economy is strong and growing. Growth in electricity demand is directly tied to economic growth, so FPL’s demand prospects are good.

Although supported as a large federal budget priority, renewables projects have slowed for several reasons: supply chain issues, tariffs on imported parts, difficulty and delay in connecting to the electricity grid, utility and consumer concerns about intermittency, cost, disposal, need for back-up at 1.1x capacity, cost of batteries, and land use concerns.

However, in addition to the new flexibility from MVP, gas prices generally are lower than in 2022. The Russian cutoff of gas to Europe and how Europe handles the 40% of its natural gas demand that was formerly supplied by Russia (right now with a surprising reliance on spot supplies rather than long-term LNG) will also affect the global-and US-gas market.

Natural Gas Prices and Increased Nuclear Availability

In 2021, natural gas was by far (74%) the primary electricity generation fuel in Florida. Nuclear power was a distant second at 11.5%.

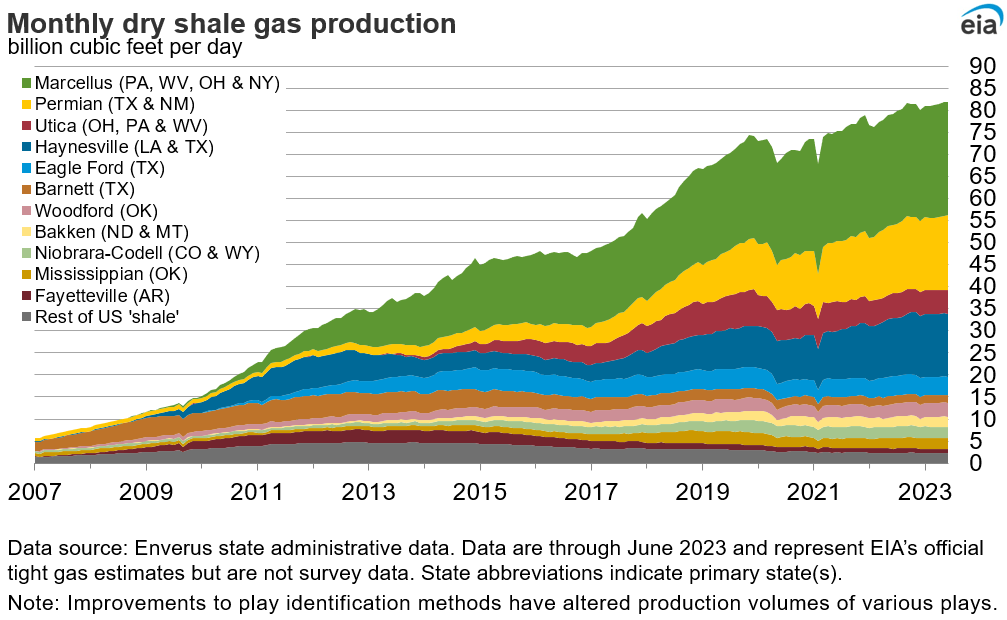

Completion of and NextEra Energy’s ownership interest in Mountain Valley Pipeline may make Appalachian and Utica gas (green and red-brown band) more readily available and cheaper for Florida.

EIA

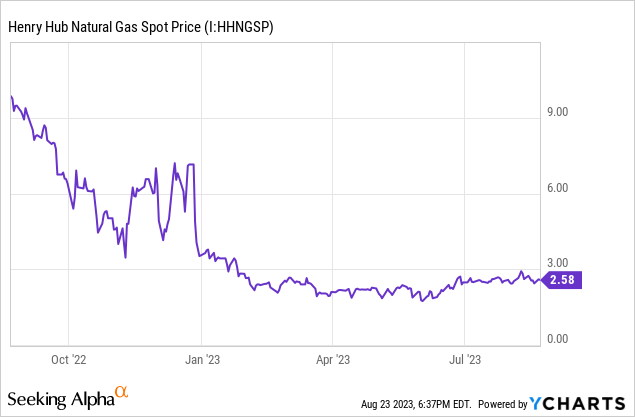

The Henry Hub (Louisiana) natural gas futures price for September 2023 is at $2.50/MMBTU on August 23, 2023, and the graph shows the marked decline from last year.

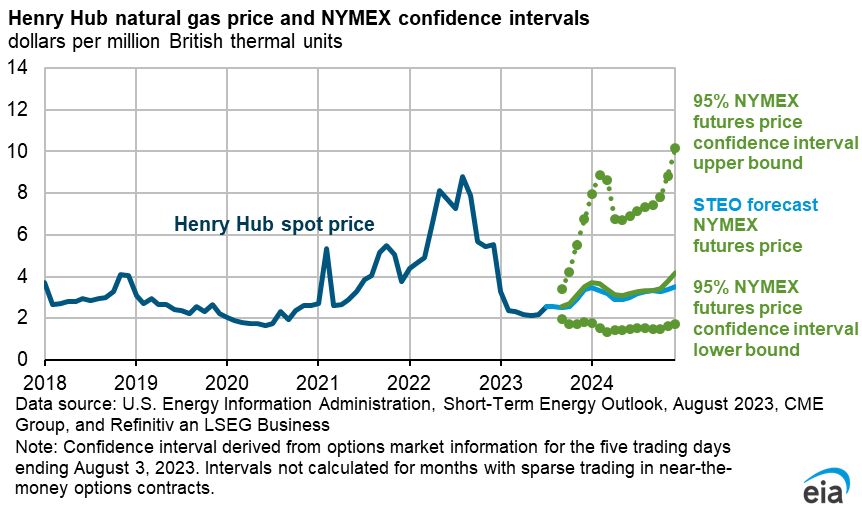

The futures prices trajectory is normal: higher in the winter and dipping again in the spring of 2024. The 5-95 confidence interval of price projections from the EIA’s August 8, 2023, Short Term Energy Outlook is shown below.

EIA

The completion of the third Vogtle nuclear plant shouldn’t be overlooked as an expansion of zero-carbon generation in the Southwest Power Pool to which NextEra belongs. Owned by fellow SPP member Georgia Power/Southern Company, the third Vogtle plant (1100 MW) was operational as of July 31, 2023. The fourth Vogtle nuclear plant (also 1100 MW) is slated for operation in March 2024.

Governance

NextEra Energy grew from a utility founded in 1925. The company is headquartered in Juno Beach, Florida and is among the largest global generators in the world of electricity from wind and solar power.

At August 1, 2023, Institutional Shareholder Services ranked NextEra’s overall governance as 6, with sub-scores of audit (7), board (7), shareholder rights (3), and compensation (8). On the ISS scale, 1 represents lower governance risk and 10 represents higher governance risk.

Note that the CEO of FPL stepped down in January 2023 for allegations of campaign finance violations and other issues.

At July 31, 2023, shorted shares were only 0.9% of floated shares.

Insiders own a negligible 0.2% of stock.

NextEra’s beta is an attractive 0.46: its stock moves directionally with the overall market but to a smaller extent (less volatility). This is characteristic of utility stocks.

On June 29, 2023, the four largest institutional stockholders, some of which represent index fund investments that match the overall market, were Vanguard (9.7%), BlackRock (7.5%), State Street (5.5%), and JP Morgan Chase (3.7%).

Blackrock, State Street, and JP Morgan are signatories to the Net Zero Asset Managers initiative, a group that as of June 30, 2023, manages $59 trillion in assets in assets worldwide and which (despite less energy supply due to reduced Russian exports to Europe) limits hydrocarbon investment via its commitment to achieve net zero alignment by 2050.

BlackRock made a point of saying it voted against 93% of ESG-related proposals in the 2023 proxy year.

Regulators

The company’s most significant regulator, for FPL, is the Florida Public Service Commission. In rate cases NextEra responds to input from a wide variety of customer-stakeholders.

Apparent from the several decisions and court cases, NextEra’s ownership interest in Mountain Valley Pipeline was affected by US appellate court decisions, US Congressional authorization, and finally a US Supreme Court decision that will allow construction to be completed.

Stock and Financial Highlights

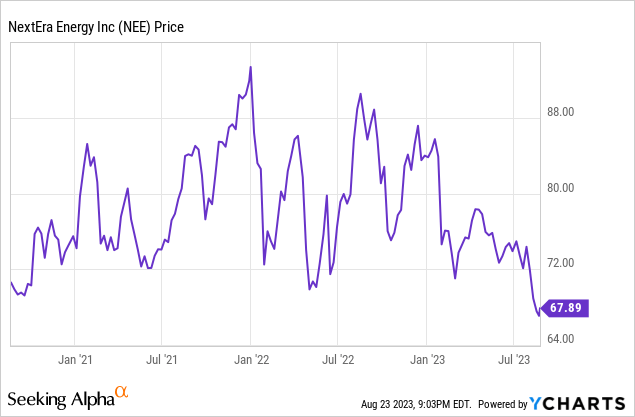

NextEra’s August 23, 2023, closing price was $67.89/share, 75% of its 52-week high of $90.10/share and its one-year target of $90.06/share. Market capitalization is $137.4 billion.

Trailing price-earnings ratio is 17 at the trailing twelve months’ earnings per share (EPS) of $4.05. EPS in 2023 is projected by analysts at $3.12 and in 2024 at $3.41 for a forward price-earnings ratio of 20-22.

Trailing twelve months’ return on assets is 3.6% and return on equity is 14.5%.

At June 30, 2023, NextEra had liabilities of $113.9 billion, including $61.0 billion of long-term debt, and assets of $168.3 billion, giving a liability-to-asset ratio of 68%, standard for a utility and lower than many.

The company’s market value per share is about three times book value per share of $22.13, indicating very positive market sentiment. The ratio of enterprise value to EBITDA is 14.3, above the level of 10.0 or less that would indicate a bargain.

A dividend of $1.87/share yields 2.8%.

NextEra has an average rating from fifteen analysts of 1.8, or “buy” leaning toward “strong buy.”

Positive and Negative Risks

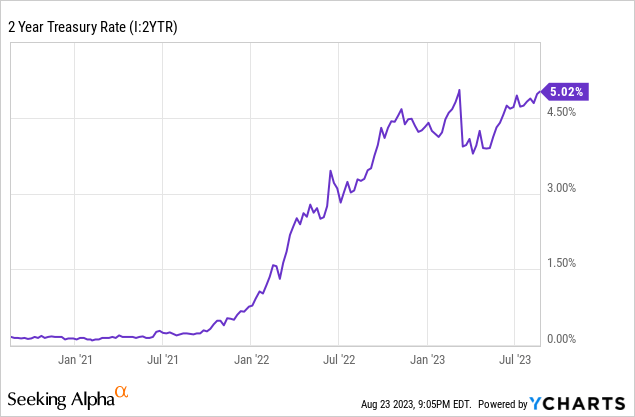

Higher interest rates and any increases will continue to impact NextEra and all utilities due to rising debt costs. Moreover, higher interest rates attract investors away from dividend-paying equities. For example, the current 2-year Treasury yield is 5%.

Weather, including hurricanes, always remain a risk for Florida utilities.

Despite the IRA, the market for utility-scale renewables may cool as utilities in the US and abroad prioritize grid resilience and back-ups to ensure 24/7 reliability.

Positive risks are the continued growth of Florida’s population and economy and the moderated natural gas prices.

Recommendations for NextEra Energy

While I do not recommend NextEra Energy to dividend-seekers, I am upgrading it from “hold” to “buy” for investors seeking capital appreciation.

The company’s steady low beta of 0.46 is indicative of its solid utility business in a growth market with lower-cost generation fuels that balances its entrepreneurial clean-energy projects division.

Although not bargain-priced, the company is at the low end of its 52-week range. NextEra has good growth plans and a sizeable energy project backlog. The challenges of executing these renewable projects-despite backing from the US government-is now better-known and so incorporated in the company’s stock price.

I own shares of NextEra Energy.

NextEra Energy

Analyst’s Disclosure: I/we have a beneficial long position in the shares of NEE, EQT either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.