Summary:

- Shares of Amazon have appreciated by 36.05% since the last article was published.

- AMZN’s operating metrics have improved, with the North American segment returning to profitability and the International segment reducing losses.

- Analysts have raised price targets for AMZN, and EPS projections show positive growth potential for the company.

HJBC

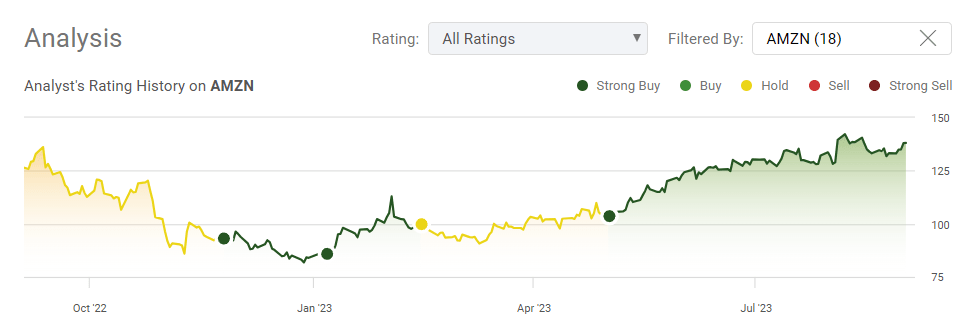

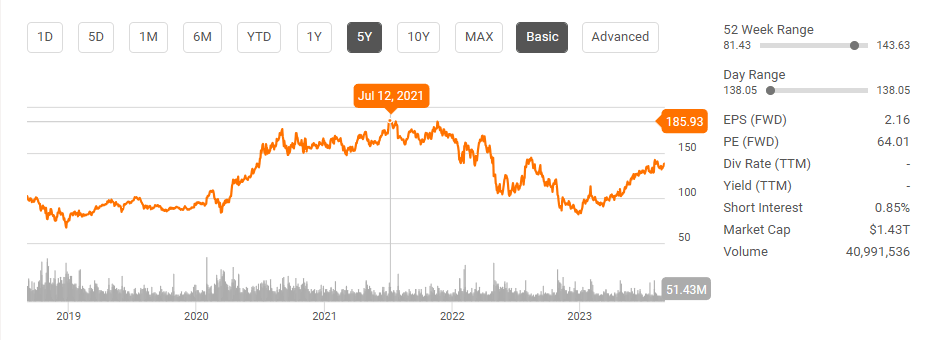

In my previous Amazon (NASDAQ:AMZN) article published on 5/2/23 (Amazon Could Be A Could Spring If Certain Trends Continue), I discussed how I felt shares of AMZN would keep appreciating due to the change in certain economic conditions. I had been a long-term AMZN bull, having been a shareholder for a significant period, but at the beginning of 2023, I began to question how much upside there was left in the tank compared to other companies I am invested in. My concerns were that Amazon Web Services (AWS) was the sole driver of profitability, and if the economic conditions didn’t ease, AMZN’s core business would continue to operate in the red. After AMZN reported its Q1 2023 report, I became very bullish again as the underlying business grew stronger, and the economic conditions I was concerned about continued to ease. Since my article on 5/2/23 was published, shares of AMZN have appreciated by 36.05%, outpacing the 8.46% returns from the S&P 500. After reassessing my investment thesis, I feel that there is a path for AMZN shares to reach and surpass their all-time highs in 2024.

Seeking Alpha

Why I was concerned about Amazon as an investment focused on capital appreciation

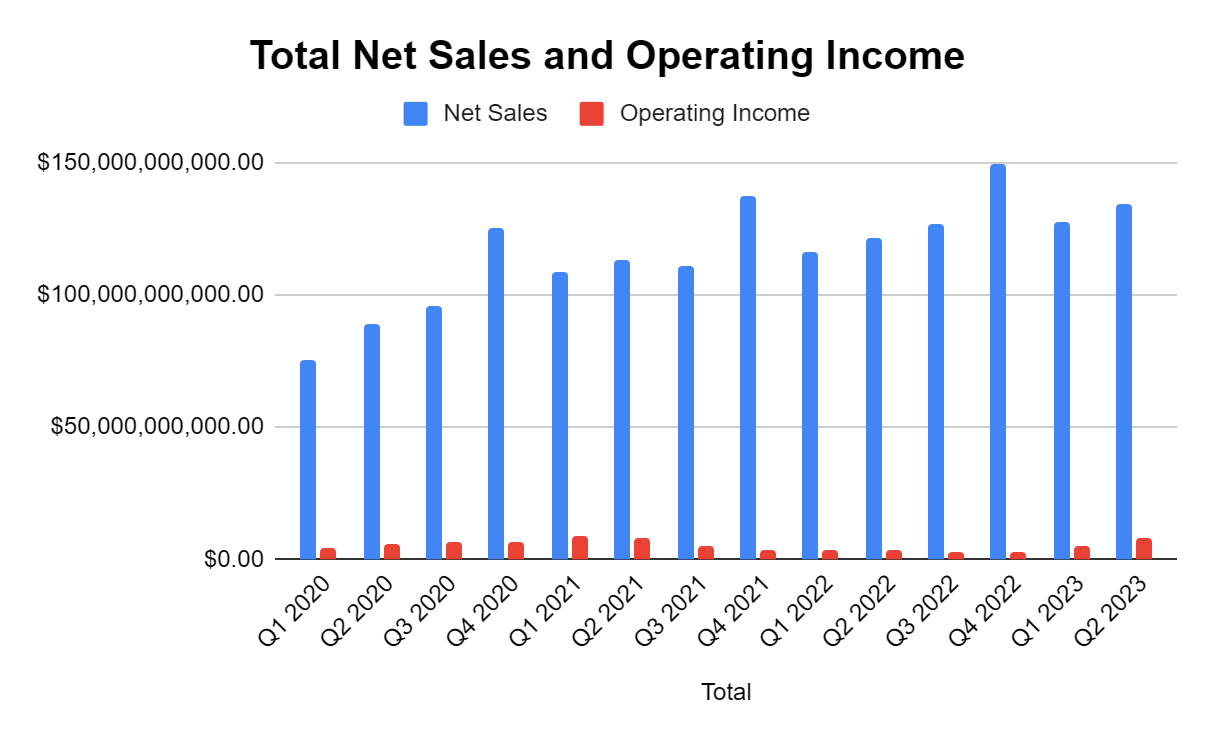

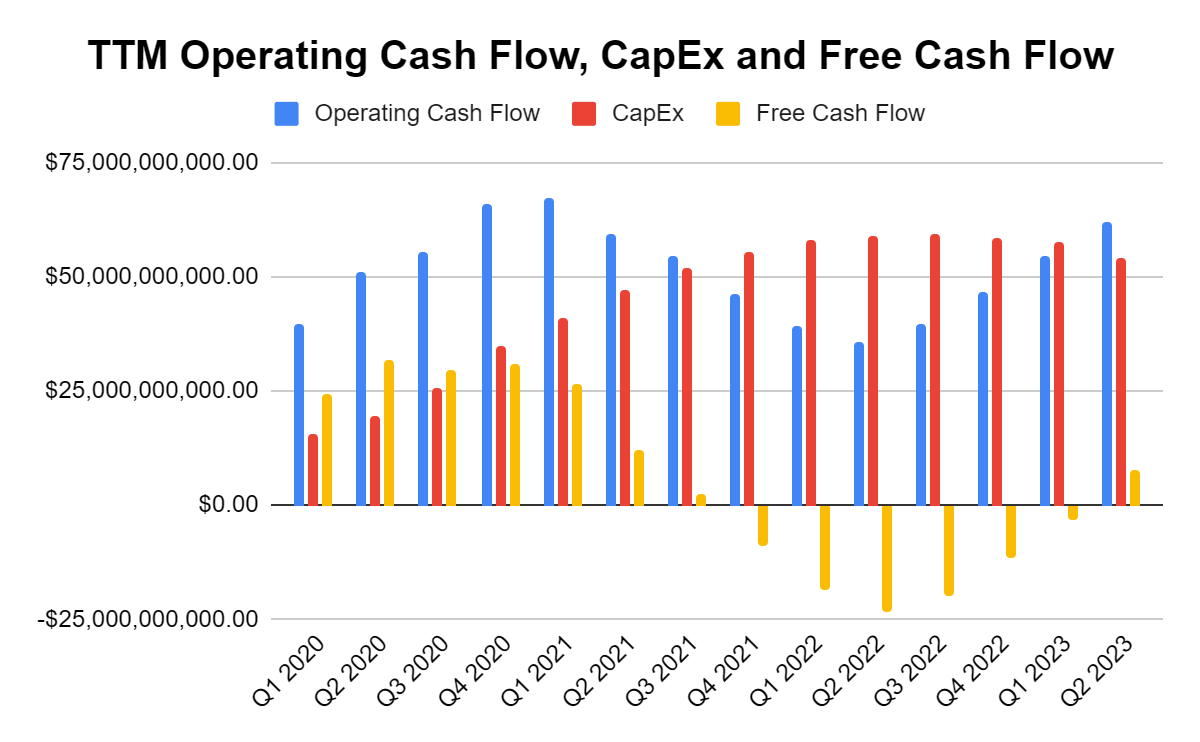

For me, AMZN has been a long-term investment focused on capital appreciation. AMZN doesn’t pay dividends, and I am unwilling to run a covered-call overlay strategy. Shares of AMZN could easily surpass the strike price that I would consider writing options at to generate income, and I am not interested in having my shares called away. While AMZN’s revenue continued to trend higher, the actual business landscape became more difficult due to economic factors, including inflation and rising rates. My concerns were that AMZN’s business wasn’t generating the level of operating cash flow from its operations that it had grown accustomed to, its large capital expenditures had created a long stretch of being free cash flow (FCF) negative, its operating margins had declined, and AWS was the sole reason for AMZN’s continued profitability. I went through all of the earnings releases (can be found by clicking here) from AMZN to put the following charts together.

Steven Fiorillo, Amazon

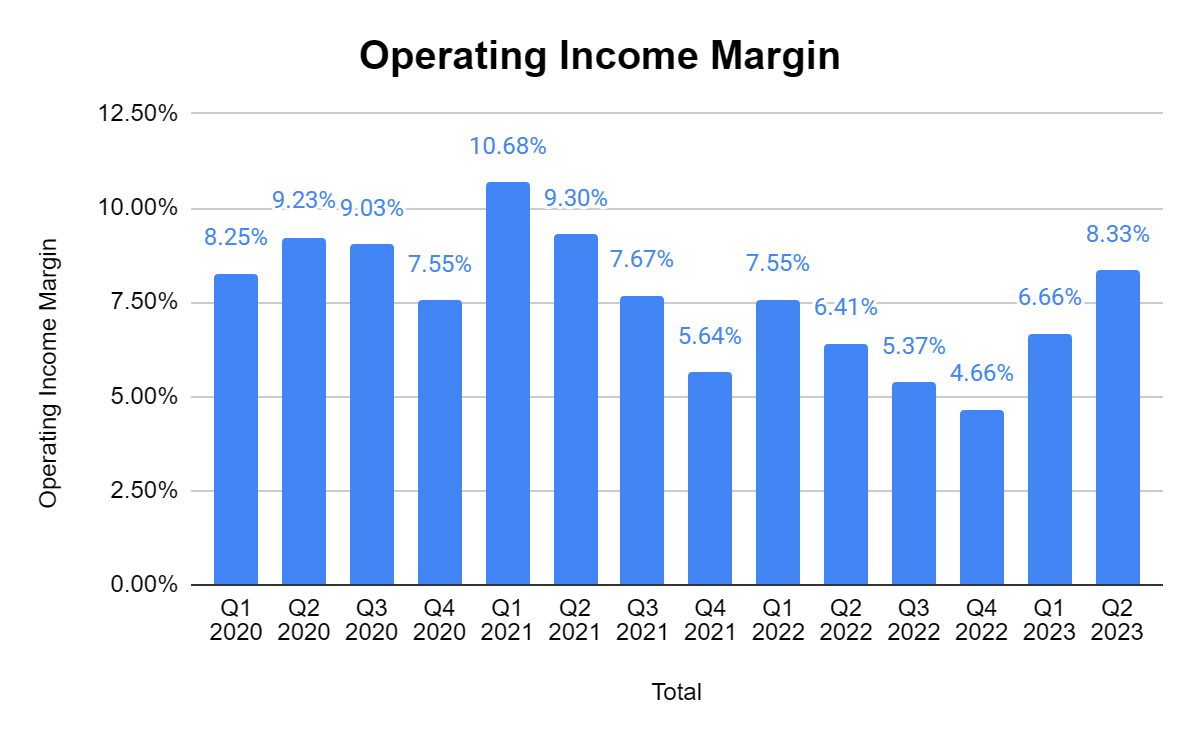

AMZN runs a low-margin business, and over the previous 14 quarters, AMZN has only generated an operating income margin that exceeded 10% once. The trend in 2021 and 2022 was identical. AMZN would generate a larger operating income margin in Q1 and then see its margins decline sequentially in Q2, Q3, and Q4. AMZN has never been a high-margin business as its traditional operations are capital intensive, but AMZN has been given a much larger multiple and premium than Walmart (WMT) because of its AWS segment. The issue I was having was that an ongoing trend of AWS representing 100% of AMZN’s operating income was forming, and the traditional businesses continued to operate in the red.

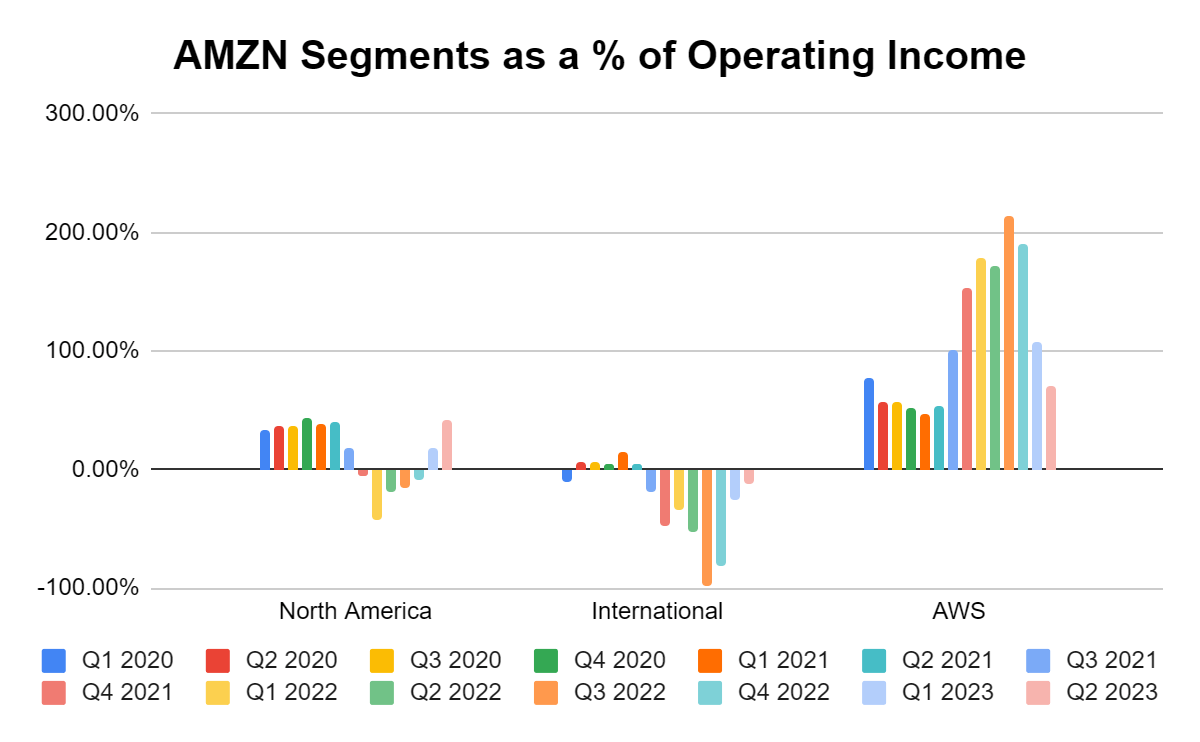

Steven Fiorillo, Amazon

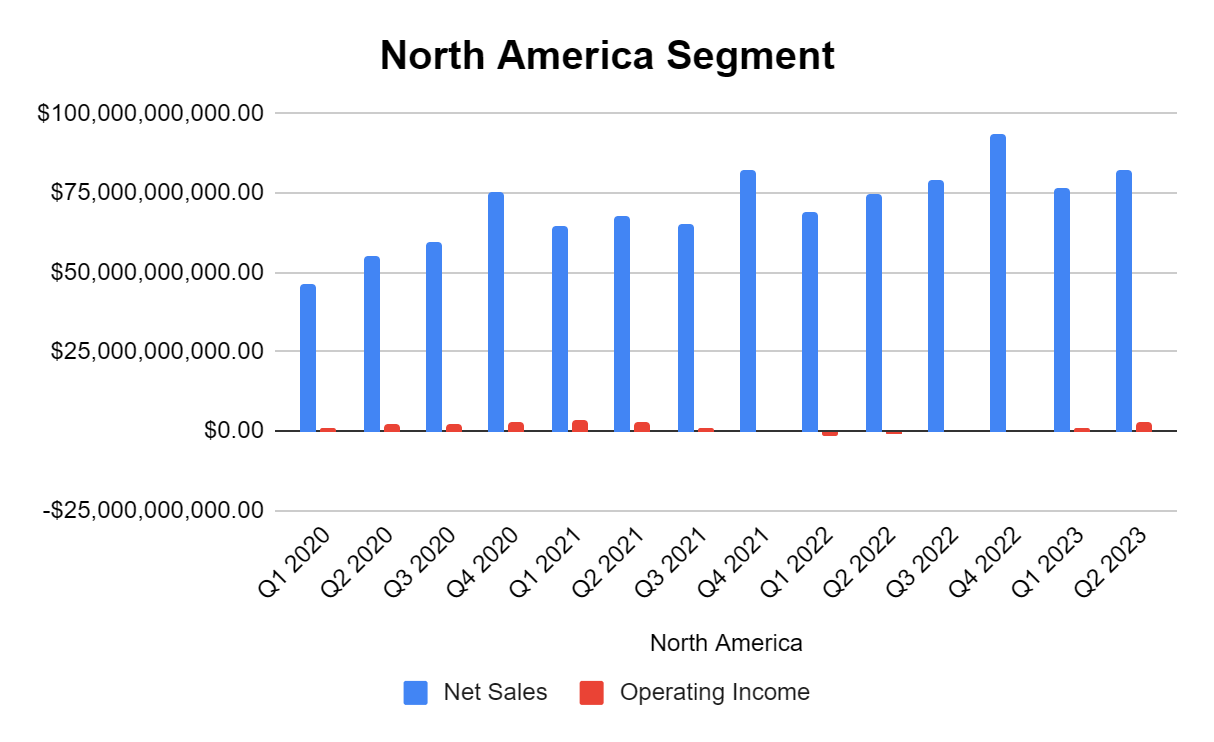

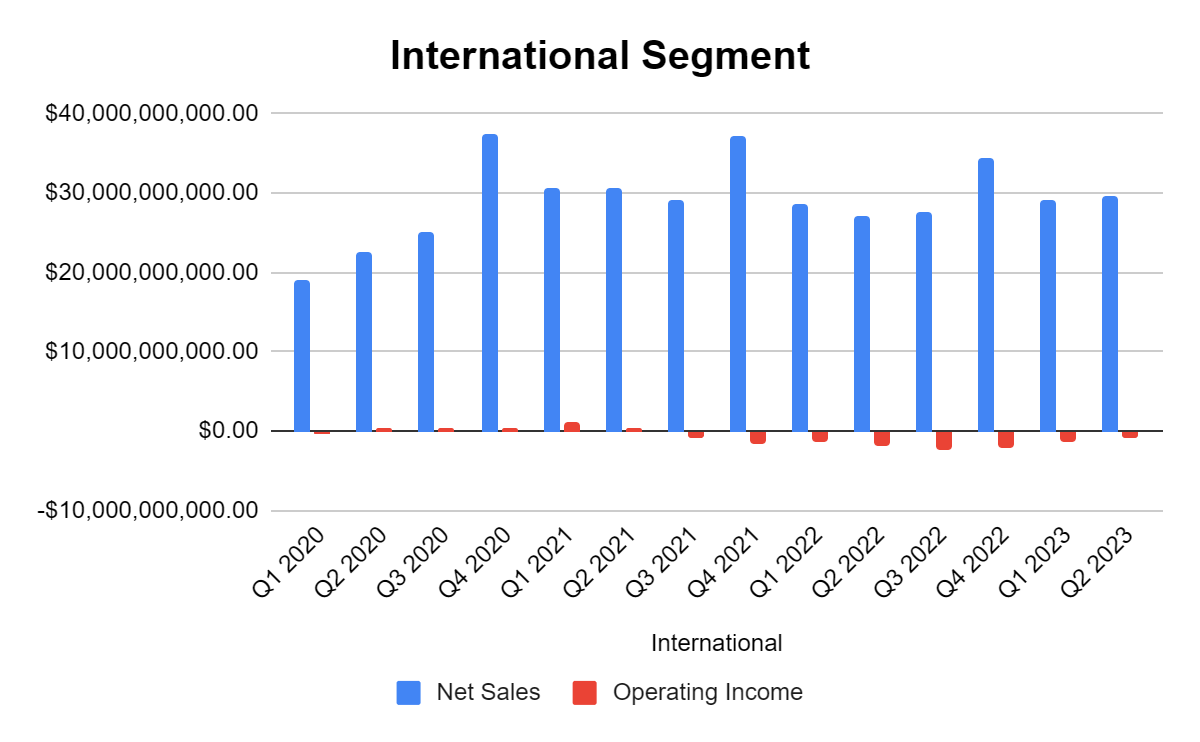

Starting in Q3 of 2021, the International segment started operating at a loss, and in Q4 of 2021, the North American segment also started operating at a loss. Over the next 5 quarters, both the North American and International segments operated in the red, and AWS accounted for 100% of AMZN’s profitability. In Q3 of 2022, AWS accounted for 213.98% of AMZN’s $2.53 billion in operating income as AWS generated $5.4 billion, while North America lost -$412 million, and the International segment lost -$2.47 billion. From Q4 2021 through Q4 2022, the North American segment ran in the red, losing -$3.05 billion cumulatively, while the international is still producing negative operating income and has lost -$12.43 billion since Q3 of 2021. This had taken a toll on AMZN’s underlying fundamentals, as its largest lines of revenue weren’t contributing to AMZN’s profitability.

Steven Fiorillo, Amazon

AMZN is one of the largest companies in the world, and while it’s still growing its top-line revenue, it’s not necessarily in its growth phase. When a company is generating hundreds of billions in revenue annually, and the only company in the S&P 500 that has generated more revenue on a TTM basis than AMZN’s $538.05 billion is WMT with $630.79 billion, I would expect there to be an abundance of FCF that is at least producing a buyback program. During the period when AMZN’s main business segments operated in the red, shares crashed by roughly -56.2%, losing over $100 per share and falling to the low $80s. While many factors, including a changing economic landscape, contributed to thinner margins and less profitability, the bottom line is that AMZN wasn’t as attractive as other tech companies from a valuation perspective. I had questioned if the amount AMZN was spending in CapEx would pay off and if my capital would better serve me allocated elsewhere.

Seeking Alpha

Why I am bullish on Amazon going forward and I feel that it can surpass its all-time highs in 2024

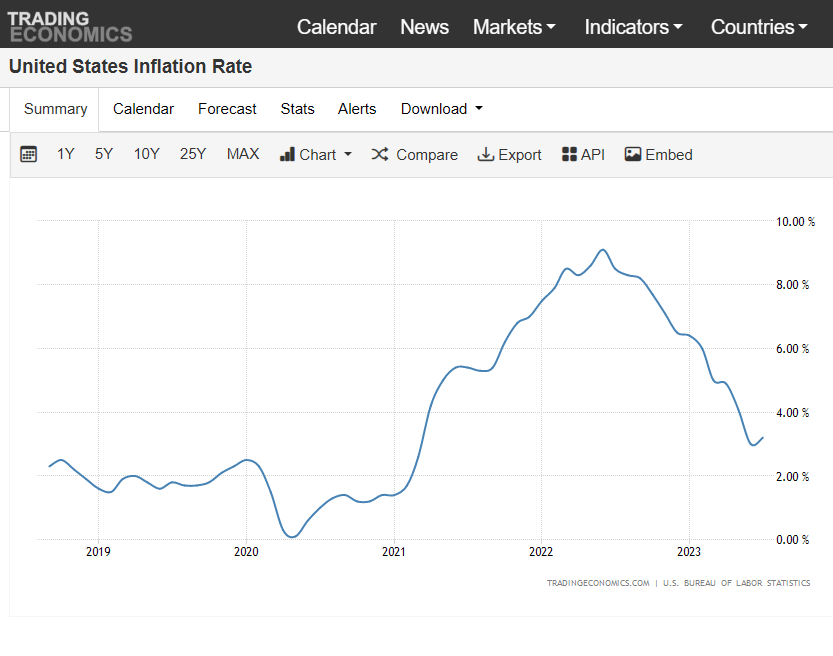

I never exited my position in AMZN, and as I predicted in my previous article, the easing economic landscape caused AMZN to experience an easier operating environment that led to better operating metrics. In Q2 of 2023, AMZN generated $134.3 billion in revenue, a topline beat of $2.96 billion compared to the consensus estimates and a 10.8% YoY increase. AMZN also produced almost double the consensus estimate of $0.34 in EPS, generating $0.65. As inflation fell over the past year, it has helped create a less intrusive operating environment for AMZN to conduct business in. The lowered inflation rate has helped curtail the rate at which the cost of revenue and total operating expenses grew and positively impacted margins.

Trading Economics

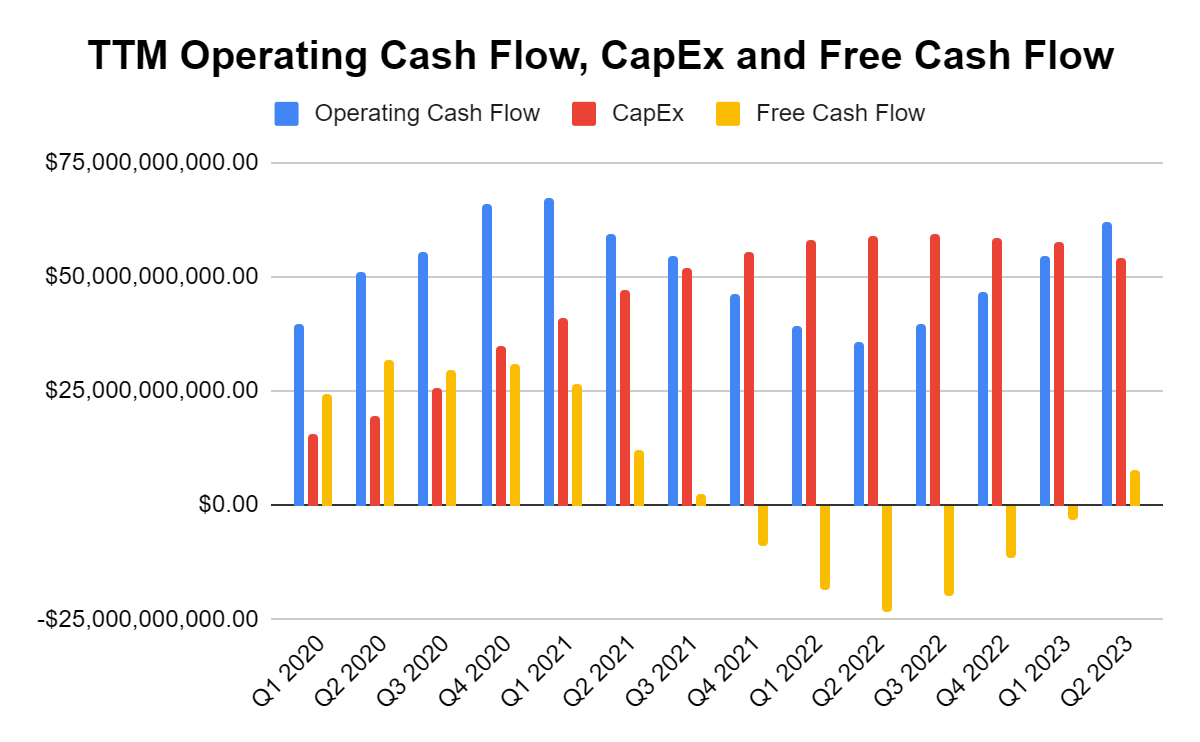

AMZN had allocated more capital toward CapEx than it was generating in operating cash flow on a TTM basis from Q4 2021 to Q1 2023. Going into the height of our inflationary environment AMZN continued to produce less cash from operations on a forward TTM basis while maintaining its CapEx spend of over $50 billion. On a TTM basis, AMZN generated negative FCF from Q4 2021 through Q1 of 2023, and now it looks as if the combination of its CapEx spend and falling inflation have paid off. AMZN has seen 5 consecutive quarters on a TTM basis of growing cash from operations being generated, and this is the first quarter since Q42021 where AMZN was FCF positive.

Steven Fiorillo, Amazon

On an individual segment basis, AWS is no longer the sole means of operating profitability. The North American segment has produced its 2nd consecutive quarter of generating positive operating income, growing from $898 million in Q1 to $3.21 billion in Q2. The International segment has also seen its 3rd consecutive tightening of losses, going from -$2.47 billion in Q4 2022 to -$895 million in Q2 2023. For AMZN to regain the rest of the ground it has lost from a share value perspective; these segments need to generate sustained profitability and contribute to AMZN’s overall operating income and FCF.

Steven Fiorillo, Amazon Steven Fiorillo, Amazon

The big Wall Street firms are on the AMZN upgrade cycle as operating margins are increasing, and AMZN is back to being FCF profitable. The Following firms have raised price targets for AMZN shares:

- Needham buy rating, price target to $160 from $150

- Morgan Stanley Overweight, price target to $175 from $150

- Bank of America Buy rating, price target $174 from $154

- Rosenblatt buy rating, price target $184 from $73

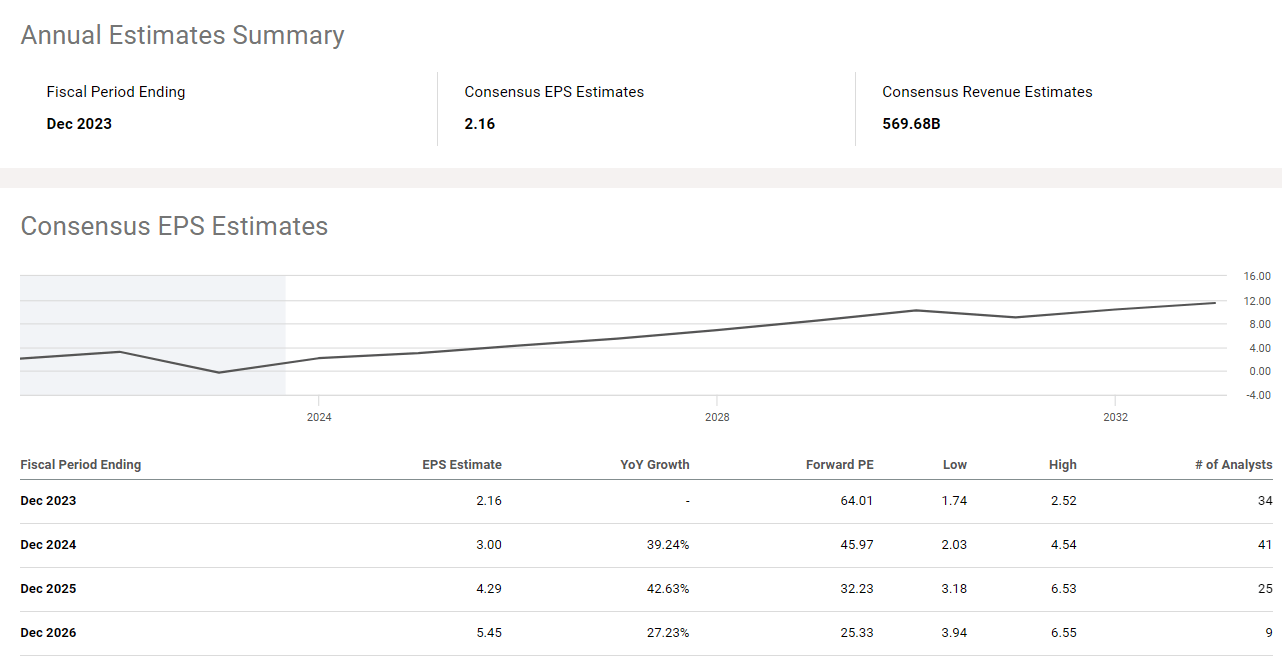

When I look at the analyst community, I see significant growth in their consensus EPS projections. In 2022, AMZN finished the year having generated -$.27 in EPS. Over the TTM, AMZN’s EPS has increased to $1.28. After looking at the consensus EPS estimates on Seeking Alpha (click here to view) I am encouraged by what I see. The EPS estimate for 2023 from 34 analysts is $2.16. In 2024, 41 analysts have AMZN’s EPS increasing 38.89% to $3. In 2025, 25 analysts are projecting that the consensus EPS for AMZN will be $4.29, a 43% YoY increase. Going out to 2026, 9 analysts see AMZN’s EPS coming in at $5.45.

Seeking Alpha

While these are just projections, the combination of price target upgrades from Wall Street firms and the EPS outlook from the analyst community is positive for shares of AMZN. In the Q2 results, AMZN provided strong guidance indicating that revenue from Q3 would come in between $138.0 billion and $143.0 billion, while the street is looking for $138.29 billion. AMZN has also guided that their operating income will come in between $5.5 billion and $8.5 billion, significantly larger than the $2.5 billion generated in Q3 of 2022.

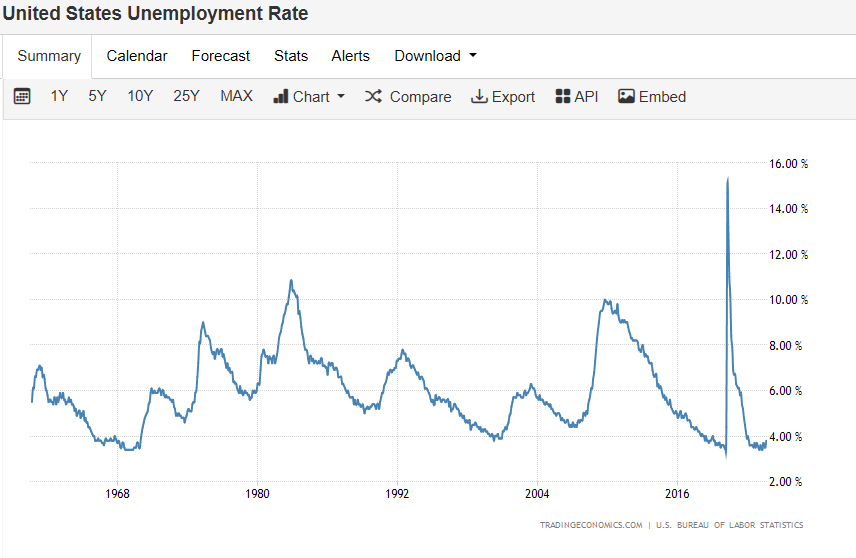

There are 3 main reasons why I feel AMZN can continue to surpass estimates QoQ going forward. We have a low unemployment rate, inflation is cooling, and the Fed is expected to start cutting rates in 2024. We are not in a situation where unemployment is rising, which means that more people have capital coming in, which is either increasing or sustaining their spending power. When unemployment is low, it helps GDP expand as more goods and services are purchased. As the impacts of inflation cooling are reflected through the economy, AMZN should continue to see an easier operating environment as its costs of operations ease.

Trading Economics

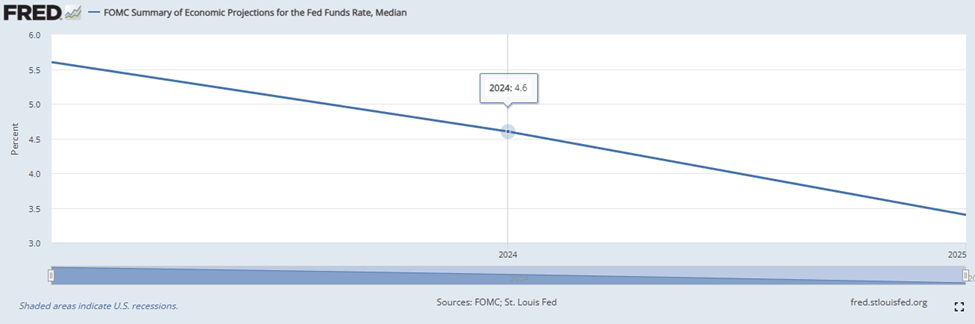

The St. Louis Fed is projecting that the Fed Funds Rate will decline to 4.6% in 2023 and 3.4% in 2025. As the Fed Funds Rate declines, the cost of capital for individuals and businesses will become cheaper. As rates on credit cards and loans decline, more businesses and individuals are more likely to spend. This is critical for the economy because businesses are more likely to expand operations and fuel growth when the cost of capital is a lower percentage of revenue generated.

St. Louis Fed

As employment continues to be strong and with rates declining, I expect that spending will increase from businesses and individuals. AMZN should be a beneficiary of these economic trends as a majority of the additional capital spent on goods and services flows toward AWS and their traditional e-commerce business. AMZN was able to spend over $50 billion in CapEx on a TTM basis since Q3 2021, which should pay off in dividends for them. They were able to expand during a difficult operating period, and now that inflation is declining, I believe AMZN is going to see better margins and their FCF increase surpassing their 2020 levels. If this occurs, then AMZN should be in a position to start a buyback program while maintaining a healthy level of CapEx allocation. In an environment where AMZN is growing its EPS, buybacks will help amplify this metric and correlate to a more attractive P/E level.

Steven Fiorillo, Amazon

Conclusion

Shares of AMZN have appreciated by36.05% since my last article on 5/2/23, and I feel this is only the beginning. The North American segment is back to profitability, and the International segment is closing the gap on its losses. AMZN has put itself in a position where its spending on CapEx has set it apart from its competitors. I think we’ll see FCF expand on a TTM basis QoQ as inflation continues to cool and rates start to decline. I wouldn’t be surprised to see a buyback program announced in 2024 and shares get back to all-time highs. AMZN is a stock that can absolutely catch fire as the analyst community is likely to continue its upgrade cycle as margins and profitability improve. AMZN has done a fantastic job at rectifying many of its operating issues, and the path forward to all-time highs in 2024 is intact. We will see what occurs over the next several quarters.

Analyst’s Disclosure: I/we have a beneficial long position in the shares of AMZN either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Disclaimer: I am not an investment advisor or professional. This article is my own personal opinion and is not meant to be a recommendation of the purchase or sale of stock. The investments and strategies discussed within this article are solely my personal opinions and commentary on the subject. This article has been written for research and educational purposes only. Anything written in this article does not take into account the reader’s particular investment objectives, financial situation, needs, or personal circumstances and is not intended to be specific to you. Investors should conduct their own research before investing to see if the companies discussed in this article fit into their portfolio parameters. Just because something may be an enticing investment for myself or someone else, it may not be the correct investment for you.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.