Summary:

- Intel aims to become the global leader in chip manufacturing, focusing on at-scale production and infrastructure capabilities.

- The company has government support and is achieving timelines to meet demand, with subsidies and partnerships aiding their transformation.

- Intel faces risks such as potential debt burden, lack of consumer demand, and competition from other foundry competitors.

JHVEPhoto

Thesis

Intel (NASDAQ:INTC) creates tech components and platforms for computing and communications industries. They are undergoing a shift from a stable dividend stock, causing large volatility in the stock price downward. With hardware cooling off from the pandemic and people preparing for a recession, Intel’s revenue showed big declines and reduced guidance. However the main focus under the new leadership of Pat Gelsinger (CEO) is to make Intel the global foundry leader in chip manufacturing (majority of chips being made by Intel’s operations). This has led to a higher risk environment for the stock and investors are diligently following Intel’s actions as the chip industry has proven to be essential for our future development including A.I. With a high projected CAGR for chips and the geopolitical tension surrounding Taiwan Semiconductors (their main competitor), Intel could be an interesting value proposition that has the infrastructure and assets to create a large moat in the chip industry.

Company overview

Intel Corporation designs and manufactures computer products and technology platforms within 6 different segments. Client Computing Group (CCG), Data Center and AI (DCAI), Network and Edge (NEX), Mobileye, Accelerated Computing Systems and Graphics (AXG), and Intel Foundry Services (IFS). CCG focuses on operating systems, hardware and applications for PC’s. DCAI offers solutions for cloud service providers and enterprise customers. NEX adapts hardware to general purpose with cloud software programming across networks. Mobileye represents self-driving and driving assistance technologies. AXG creates products and technologies to solve customers’ computational problems. IFS is Intel’s operations manufacturing other companies’ chips. By revenue in 2022, Intel’s largest segments include CCG (32%), DCAI (19%), NEX (9%), Mobileye (2%).

Industry overview

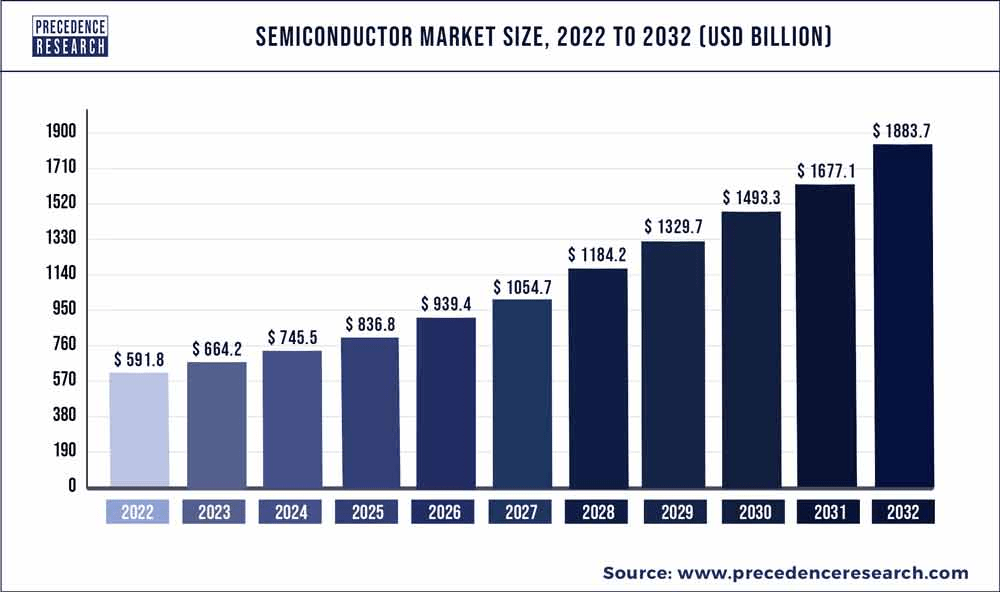

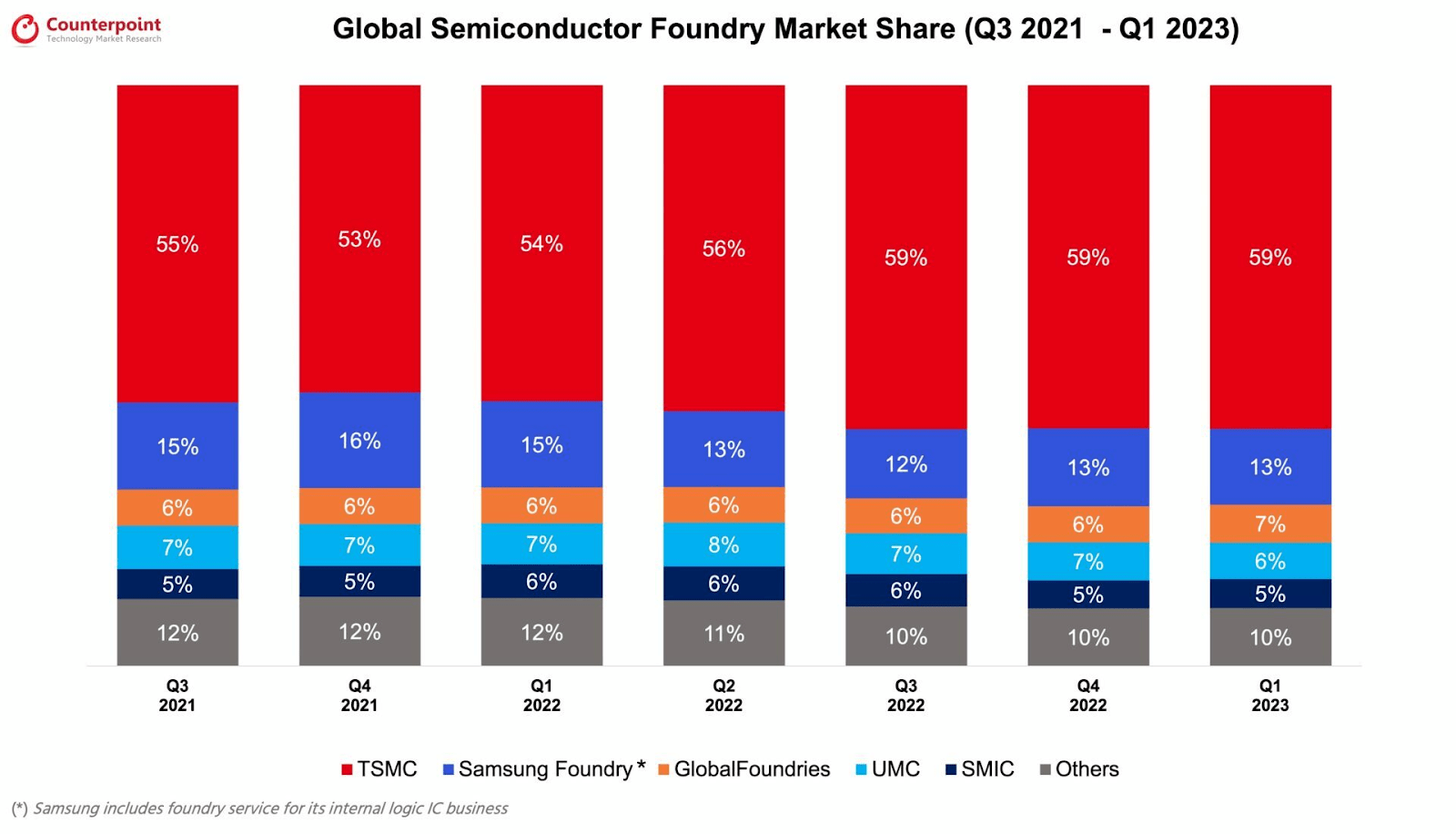

The global semiconductor market is worth $573 billion and is expected to grow to $1.4 trillion by 2029, which is a 12% CAGR. Intel is the 2nd largest in market share at 9.7% which is behind Samsung’s 10.9% market share. With the growth of A.I. technology and its necessity for increased processing power, coupled with the growing EV sector with smart cars, semiconductor companies like Intel will be seeing large work orders coming their way for the foreseeable future.

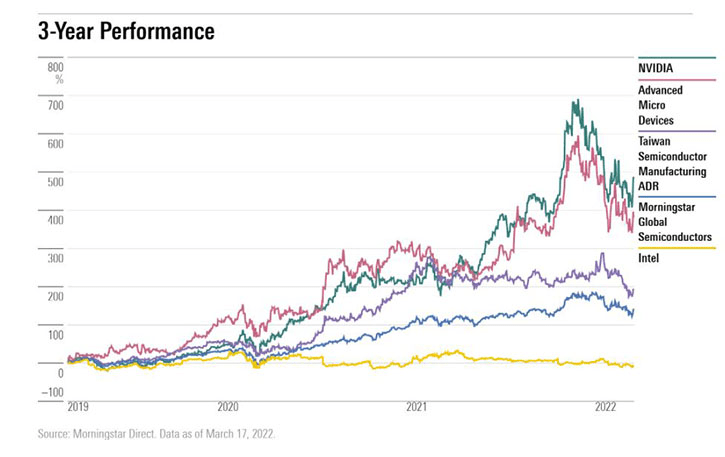

Semiconductor Market Size Forecasts (Precedence Research) Global Semiconductor Market Share (Counterpoint Research) Intel Price Performance (Morningstar )

ESG

Intel’s commitment to achieve net-zero greenhouse gas emissions across global operations by 2040 and to increase the energy efficiency and lower the carbon footprint of their products and platforms is one of their additions to their RISE strategy. Some of the RISE goals include: 10% reduction in our greenhouse gas emissions on an absolute basis by 2030, 2030 goal to achieve 100% renewable electricity across global operations, and inaugural green bond of $1.3 billion for projects that support investments in sustainable operations, energy efficiency, greenhouse gas emissions reductions, water stewardship, and renewable energy.

As part of the Alliance for Global Inclusion, Intel works with technology companies to create a Global Inclusion Index Survey, which serves as a benchmark to track diversity and inclusion improvements, provide information on current best practices, and highlight opportunities to improve outcomes across industries. From the second annual survey in 2022, they were able to see significant improvements and trends towards diversity and inclusion of employees across multiple industries. In addition to their industry contribution, Intel has shown gender pay equity globally and continues to maintain race/ethnicity pay equity in the US according to their public EEO-1 survey data since 2019.

Competitive advantage

Intel has the infrastructure to dominate large-scale production.

Intel is one of the longest standing competitors in the space, controls virtually the whole US market for chips, and the new CEO understands that they need to refocus on an area that they can dominate which is at-scale manufacturing for the future. While Intel has been on a steady decline, Nvidia (NVDA) and Advanced Micro Devices (AMD) have taken the spotlight and have outperformed Intel when it comes to hardware capabilities. Nvidia and AMD have proven that as the smaller company, they have Intel beat when it comes to technology at this moment. Pat Gelsinger recognizes that Intel has gone away from its roots and he is reenergizing the behemoth towards its advantage of built out infrastructure capabilities. Since entering in 2021, Gelsinger has created additional sites in Ohio (2 factories), Arizona, and Germany, with plans for EU expansion in France, Ireland, Italy, Poland, Spain to meet their ambitious goal of 5 new technology nodes in 4 years. He also worked to pass the US Chips and Science act which subsidizes $52 billion towards chip manufacturing in the US, where Intel holds the majority market share. The last unique aspect of Intel is the diversification of its segments. Not only do you get a hardware business but also a growing cloud solutions provider, chip producer for A.I. developments, and the self-driving potential of the Mobileye division. With cloud-solutions and self-driving cars becoming more advanced, it is a natural assumption that A.I. will be used to better and potentially perfect an ever-learning products for consumers. This would leave Intel in a spot to double or even triple dip on artificial intelligence development as they become more of a reality for consumers.

Catalysts

Government Support and Achieving Timelines to Meet Demand

The big questions that lie ahead for Intel is will consumer demand fill their large at-scale manufacturing vision, how much support will they receive from governments for building their factories, and will they be able to achieve these objectives by their timeline. Intel’s new CEO was influential in lobbying for the approval of the CHIPS and Science act passed in 2022. This law will fund over $280 billion for domestic research and manufacturing of semiconductors. Intel has a successful track record of collaborating with local, state, and federal governments (Whitehouse.gov, 2022). Their most recent success brought all levels together for a megadeal of around $2.4 billion in 2022 for their Ohio manufacturing sites. With over $40 billion from the CHIPS act devoted to manufacturing incentives and Intel’s frequent collaborations with the federal government (10+ federal grants from 2012-2022), it would be no surprise to see Intel take a big slice of these incentives.

Currently Wall Street analysts expected Intel to have a worse Q1/Q2 then their results, which speaks to the quality of leadership helming Intel. While this is not an easy pivot, shifting focus to become the world leader in semiconductor chip production, the success of Intel will come down to how well the leadership can navigate this period of negative cash flow and mitigate the risk of laying down massive amounts of capital. With subsidies from the government, more investor partnerships, and upfront investment from clients, that part of the equation will become much easier. Seeing these factors coalesce would serve as a major catalyst that brings validity to IDM 2.0’s mission, making Intel the leading producer of chips globally.

Other major catalysts in the water would be new partnerships with clients such as automobile companies or other chip players like AMD and Nvidia. With AMD/Nvidia further along technologically, they may need partners to help them produce and distribute their chips with the growing demand for A.I. development, which is where Intel would be a valuable ally. The same can be said about automotive companies. If you’ve noticed, most modern cars are becoming more and more like a computer than a simple machine. With a tight supply chain, car companies may look to lock in relationships with players like Intel to make sure their next fleet of vehicles will have top of the line tech and won’t be delayed. This brings attention to Intel as a potential sleeping giant in the A.I. race who could stand to gain from the tailwinds of manufacturing technology at scale. While Intel, AMD, Nvidia have historically been competitors, the shift in Intel’s business with IDM 2.0 may be an opportunity for them to bury the hatchet and utilize each other’s competitive advantage in this A.I. race.

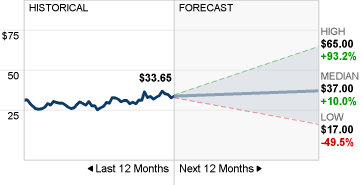

Intel Stock Price Forecasts (CNN)

Financials

2022 revenue was $63.1 billion, down $16 billion or 20% from 2021. Major segment moves were lower revenue in CCG and DCAI, higher revenue in NEX. 2022 results were influenced by slow consumer demand, inflation anxiety, and higher interest rates. Given the supply chain issues that still exist from the pandemic leading to higher per unit costs, it is not surprising that this was a downward move with consumers and clients starting to pinch pennies. With the high uncertainty in the market and the commitment of Intel leadership towards IDM 2.0 (the foundry manufacturing focus) they did not provide guidance beyond Q1 of 2023 which was $10.5 to $11.5 billion. They came in at $11.7 billion which is 36% down YoY and beat expectations on EPS and Sales.

Most recent earnings in June showed that their cost savings initiatives of $3 billion allowed them to have $0.13 EPS compared to the negative outlook of ($0.04) EPS projected in April. Total revenue for the quarter was $12.9 billion, down 15% YoY but their foundry segment is up over 300%. While this is the smallest segment so far, it shows the progress the IDM 2.0 movement is making and the potential for growth as they aim to become the leading manufacturer of semiconductor chips.

With $43 billion in current assets and $27 billion in current liabilities, Intel has continued to improve their position with $8 billion in cash/cash equivalents and $16 billion in short-term investments. While this is slightly lower than their numbers from the end of 2022, they have brought down their current debt to asset ratio by about 1.5% (Intel, 2023). Total debt has seen a rise of about $9 billion or 24% but this should be expected with all the capital expenditures to continue development of new sites.

Valuation

As Intel is currently cash flow negative (due to their large capital expenditures going into development), a DCF model would be challenging to give an accurate depiction of the fair value of the company. Given that major milestones like technology and site completions are most likely to come around 2025, that may be a better time frame to reevaluate Intel’s numbers. Given analyst estimates, Intel sits with a median expectation of $37, ranging from $17 to $65 (CNN Money, 2023). The current uncertainty and multiple years out from fruition leave this as a big question mark for who will be right in their predictions. Keep your wits about you, understand your investment thesis, and if Intel aligns be sure to understand the complete business and that this will be a long transformation. East Asia accounts for 75% of global production. Qualcomm and GlobalFoundries

Risks

If Intel’s large manufacturing investments in Arizona, Ohio, EU Expansion in Germany, France, Ireland, don’t pan out, the large levels of debt on the balance sheet will weigh on their cash flow and ultimately the shareholders. Currently being cash flow negative due to capital expenditures to build factories in Arizona, Ohio, and Germany, shows that these are major shifts and investments in the business which carry inherent risk for investors. They have offset some of this risk by having advance partnerships from foundry clients to share some costs to guarantee manufacturing space and with investment firms splitting startup costs to leverage Intel’s market positioning in semiconductors.

If consumer/client demand is not there for all of the capacity they invested in, it will leave them with commercial spaces that will not be in use. If they miss on their technology node milestones, they could stand to lose ground to other foundry competitors as they would not be able to supply quality hardware manufacturing at-scale. Lastly, there is the risk that they run out of money before completing their transformation. This scenario seems unlikely with the large scale of Intel’s business, current debt levels (~66% of their debt can be paid with their cash, cash equivalents, and short term investments), and the large subsidized support from the US government but something to consider as they will be cutting costs for the next few years to support the business.

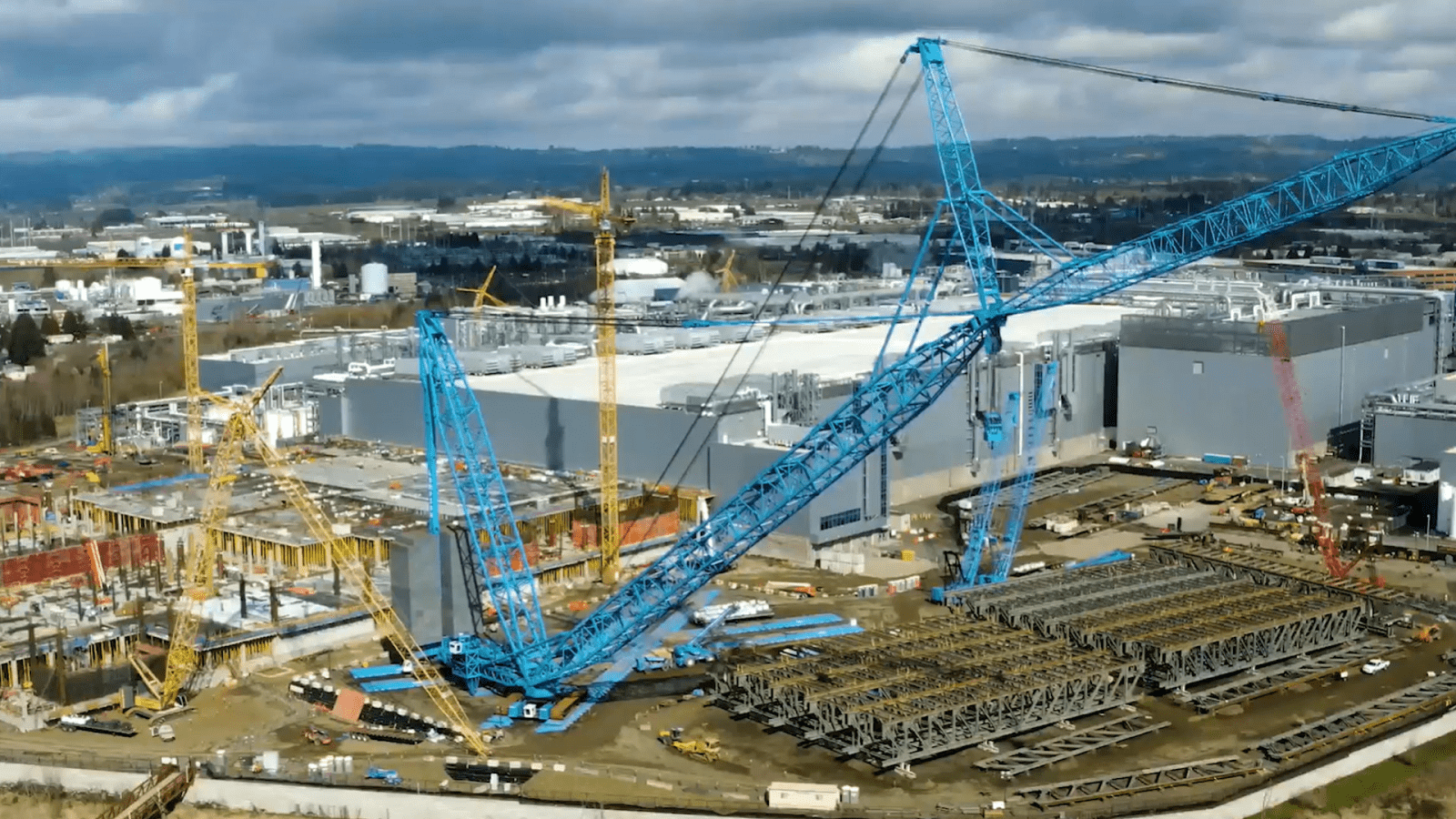

Intel Factory Production Progress (Intel Newsroom)

Conclusion

Intel is in a transition period and their numbers and profitability are down. This will probably continue to be the case until 2025 when major milestones are hit in their technology development and infrastructure. With the goal of becoming the premier manufacturer at-scale for semiconductors, Intel is in a great market that it should be able to capitalize on, with the big if being if their leadership will be able to navigate the transition smoothly. The road ahead is rocky for Intel but with the necessity of chip manufacturing only growing, IDM 2.0 could put Intel in position to overtake Samsung as the #1 manufacturer in the world. Be on the lookout for major government support, partnerships, and when Intel becomes cash flow positive. These catalysts will allow us to get a better picture of what role Intel will play in our future and allow us to better understand its fair value.

Analyst’s Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.