Summary:

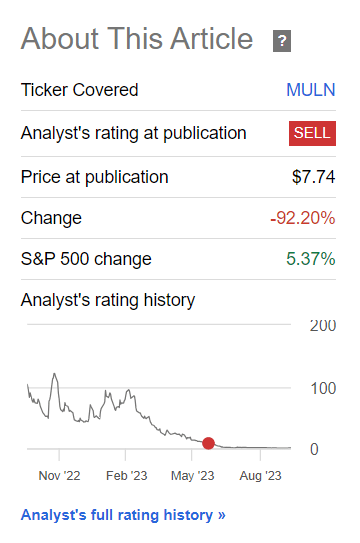

- Mullen’s stock price started to soar lately. However, the current price of $0.6/sh is still 92% below the price at the time I published my previous Sell call.

- In this article, I analyze the most recent news and corporate actions. Read on.

- Aside from the new revenue, I don’t think MULN has anything to boast about. And these revenues are not enough, given the high costs and bleak outlook for the future.

- I reiterate my Sell recommendation, but strongly advise you not to short this stock, as it could be artificially supported by short squeezing and FOMO for a while longer.

Mario Tama

Introduction

To be honest, I do not know why Mullen Automotive, Inc. (NASDAQ:MULN) stock is so popular among retail investors – the EV industry is full of companies that I think are much more transparent, with operations that are more predictable and understandable for forecasting. However, my first bearish article on the company in May attracted a lot of attention that I honestly did not expect. And now I am hearing even more talks about MULN – in the last 5 days, the stock price has surged over 15%. However, the current price of $0.6/sh is still 92% below the price at the time I published my previous Sell thesis:

Seeking Alpha, my Sell article on MULN

What happened to the company to make it feel investor demand again? Let’s figure it out together.

Recent Corporate News And Weird Actions

My last article came out on May 27, 2023, so I have a few things to report in terms of the new financial and corporate data.

On June 21, Mullen stated that it currently has enough capital to sustain its operations for at least the next 12 months, and its assets are unencumbered, except for $7.3 million in outstanding debt. Despite trading at a significant discount compared to its cash position of $135 million, Mullen Automotive’s management was confident that the company has achieved or is on track to achieve its previously stated objectives. The company also highlighted two recent acquisitions that have contributed valuable, unencumbered assets to its balance sheet. These acquisitions include majority ownership in Bollinger Motors and certain assets related to Electric Last Mile Solutions, with a total value of $253 million.

On June 29, the firm announced that it made its 1st recorded revenue by selling 22 electric cargo vans to the Randy Marion Automotive Group for $310,000. Additionally, Mullen Automotive is said to be currently engaged in six Campus EV Pilot Programs across various industry sectors, including aviation, pharmaceuticals, public utilities, and universities.

On July 6, MULN announced an authorized stock repurchase program worth up to $25 million. The program would allow the company to buy back shares of its outstanding common stock until December 31, 2023. David Michery, the CEO and chairman of Mullen Automotive, stated that the company was initiating this buyback program as an attractive opportunity to utilize its capital and provide value to its shareholders. The stock surged ~53% that trading day.

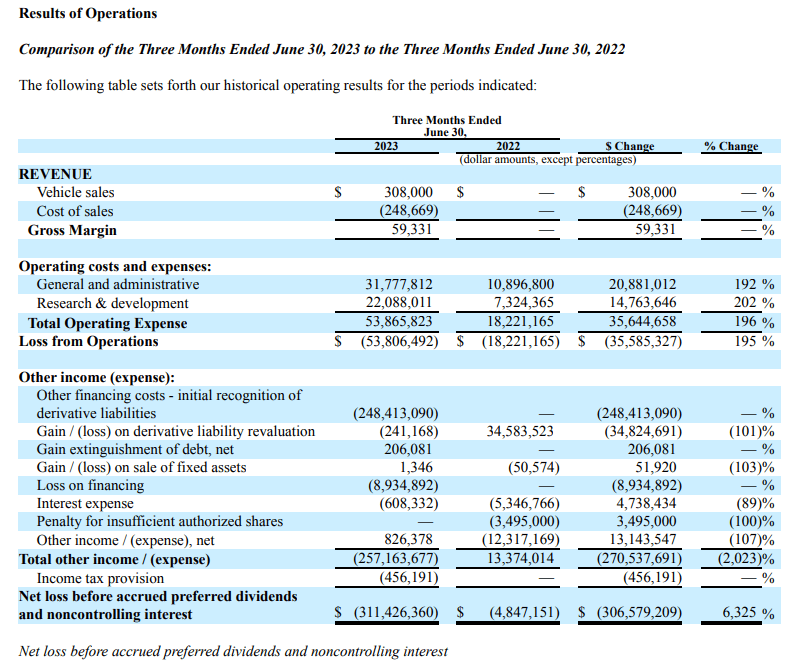

On August 14, the company released its first 10-Q report with revenue and reported GAAP EPS of -$11.14. Here’s what the profit and loss report looks like:

SEC, Seeking Alpha, MULN

What aspects do I find concerning or troubling?

Well, in fact, it would be easier for me to answer the question that I do not find troubling in MULN’s case.

What kind of buyback are they even talking about when they are a company that has just made the first $308,000 in revenue from shipping a few vehicles? In my view, that is an absolutely outlandish corporate action that I can’t wrap my head around. If you know even a little bit about corporate finance, you probably know in which cases buybacks are to be welcomed – and that is definitely not the case with MULN. Let me explain this with real examples.

You may know well about Merck (MRK). The firm announced a $10 billion buyback plan back on February 22, 2000, which was considered the largest at that time. However, instead of increasing, the company’s stock dropped by approximately 15% in the following month. This buyback was seen by investors as a reflection of the company’s weaknesses, as it was facing the expiration of important patents, had a limited drug pipeline, and its chief scientist acknowledged that it could no longer maintain its targeted 20% EPS growth rate. That huge cash pile of $10 billion could have been spent on future research and development, expanding the pipeline. But it wasn’t.

Buybacks can be seen as a negative signal in high-growth industries, suggesting that the company lacks new investment opportunities, Harvard Business Review notes [link above]. Investors in such industries may interpret buybacks as an admission of limited growth potential, leading to a sell-off of the company’s shares. This effect is more commonly observed in technology-driven sectors where rapid changes and innovation are critical for success.

This is directly related to MULN. The electric car market today is an absolutely crazy place in terms of competition. Larger pure players like Tesla (TSLA) are taking more and more market share in their hands, while more diversified players – formerly ICE-focused like Ford (F) and General Motors (GM) are trying to use their scale to catch up. And I have not even mentioned the Chinese, Japanese, and Korean giants whose electric cars I see more and more frequently on the roads. A distinctive feature of all the industry players mentioned above is mass production capabilities, which MULN never had and still does not have. And I doubt it will ever do.

Management says MULN is undervalued in the market – but what will they use to back up that statement? All I have heard so far is cash relative to the market cap. But why don’t biopharmaceutical companies buy their stock immediately after the FDA approves their drugs? In any case, companies that do announce this are immediately punished by the market, as such a decision is usually interpreted as a lack of confidence in management’s own assessments of the company’s value. The answer is quite simple: management is usually aware that the scaling process is still ahead of them. And if their drug is not unique (the consumer can easily switch to another company’s product at no additional cost of any kind ), then that once again speaks to the impossibility of buybacks.

The only criterion by which to judge MULN’s valuation today is its gross profit margin, which is 19.26%. It is lower than Tesla’s 21.49%, but well above the auto industry average. The problem for MULN, in my opinion, is the sustainability of this metric. The few cars it has delivered were pre-ordered a long time ago. And the industry is currently going through anything but the best of times where, as I mentioned earlier, competition matters and decides everything. In the future, MULN will inevitably face this problem when customers expect lower prices – or they will simply switch to another brand.

Aside from brand new revenue (a drop in the bucket compared to OPEX), I don’t think MULN has anything to boast about. That’s why the share price is falling like a stone – and the problem here is hardly the brokers, whom the firm is trying to sue for manipulation.

The Bottom Line

In my opinion, the current situation suggests that MULN investors are in for more pain as, over time, the short sellers will disappear and the company will face the reality that it lacks the money to develop and is unable to withstand larger EV players.

This is such an uncertain story that even professional analysts dare not give their forecasts for sales and earnings per share:

Seeking Alpha, MULN

So I reiterate my Sell recommendation despite the 92% drop since my last Sell call. But I also strongly advise you not to short this stock, as it could be artificially supported by short squeezing and FOMO for a while longer.

Thank you for reading!

Editor’s Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.

Analyst’s Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.

Hold On! Can’t find the equity research you’ve been looking for?

Now you can get access to the latest and highest-quality analysis of recent Wall Street buying and selling ideas with just one subscription to Beyond the Wall Investing! There is a free trial and a special discount of 10% for you. Join us today!