Summary:

- After several years of increasing debt levels, Coca-Cola has reduced net debt as a percentage of net debt + equity to 2016 levels.

- Coca-Cola’s current P/E multiple is low compared to historical levels.

- The low current multiple and analysts’ estimates reflecting continuing EPS growth provide opportunity for share price growth.

- A dividend yield over 3%, together with potential share price gains, provides an opportunity for double digit returns through the end of 2025.

Justin Sullivan

Investment Thesis:

I last published an article on Coca-Cola Company (NYSE:KO) back on February 4, 2021, titled, “Coca-Cola: Earnings And FCF Are Not ‘The Real Thing’“. I included in my summary points,

- There is an issue with Coca-Cola’s reporting of GAAP and non-GAAP earnings – earnings and free cash flow are arguably not “the real thing” and are overstated.

- At current share prices and based on traditional financial metrics, strong returns are possible over the next four years, with a caveat to watch the “equity Bucket” and possible unsustainable increases in debt levels.

Despite the potential for strong returns, I rated Coca-Cola a Hold at the time due mainly to my concern at the possible unsustainable increases in debt levels. Time to take another look.

Debt levels greatly improved –

At the time of my 2021 article, Coca-Cola’s debt net of cash as a percentage of net debt + equity had increased from 50.5% at the end of 2016 to 63.0% at the end of September 2020 (last available reported results).

Pleasingly, Coca-Cola’s debt net of cash as a percentage of net debt + equity has since decreased to 51.4% at the end of Q2-2023, just a little above the 50.5% at the end of 2016.

Regular ‘Beats’ against analysts’ consensus EPS estimates –

Since my 2021 article, Coca-Cola has beat analysts’ consensus EPS estimates for 10 of the 11 quarters reported and matched on the remaining one.

Lower P/E Multiple makes current share price more attractive –

Despite regular beats against analysts’ EPS estimates, Coca-Cola’s P/E multiple has decreased from 25.77 in February 2021 to the current reading of 20.44.

Despite the lower current multiple, SA Premium analysis shows an increase of 8.54% in share price since the publication of my 2021 article and Total Return of 17.97% including dividends (note these percentages do not take into account duration held, so do not represent annualized returns, which would be lower).

Summary and conclusions –

But for the decline in multiple, Coca-Cola would have provided strong returns since my previous article was published. The lower current multiple and the ability of Coca-Cola to meet or exceed analysts’ EPS estimates, positions the stock to provide strong returns between now and holding through the end of 2025. The debt levels are no longer the concern they were previously. Taking all of the foregoing into account, I believe Coca-Cola stock presently deserves an upgrade from Hold to Buy. A more detailed financial analysis in support of this conclusion follows.

Financial Analysis and Comment

Looking for market mispricing of stocks –

What I’m primarily looking for here are instances of market mispricing of stocks due to distortions to many of the usual statistics used for screening stocks for buy/hold/sell decisions. I believe the answer is to compare projections, based on analysts’ estimates out to the end of 2024 or later, to past performance. Summarized in Tables 1 and 2 below are the results of compiling and analyzing the data on this basis.

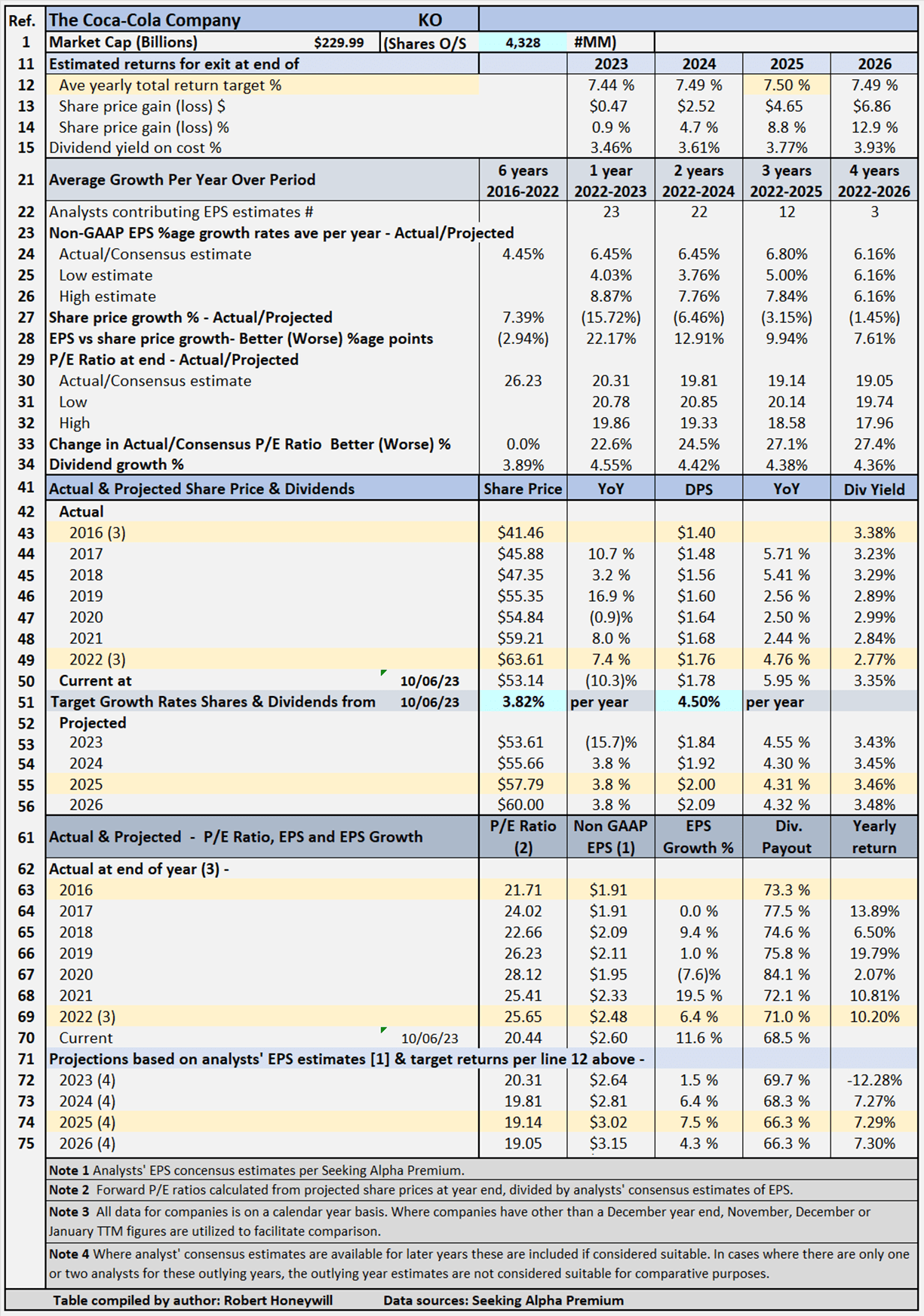

Table 1 – Detailed Financial History And Projections

Seeking Alpha Premium

Table 1 documents historical data from 2016 to 2022, including share prices, P/E ratios, EPS and DPS, and EPS and DPS growth rates. The table also includes estimates out to 2026 for share prices, P/E ratios, EPS and DPS, and EPS and DPS growth rates. (Note – while estimates are shown for analysts’ EPS estimates out to 2023 to 2026 where available, estimates do tend to become less reliable, the further out the estimates go. These estimates are only considered sufficiently reliable if there are at least three analysts’ contributing estimates for the year in question). Table 1 allows modeling for target total rates of return. In the case shown above, the target set for total rate of return is 7.5% per year through the end of 2025 (see line 12), based on buying at the October 6, 2023, closing share price level. As noted above, estimates become less reliable in the later years. I have decided to input a target return based on the 2025 year, which has EPS estimates from twelve analysts, because it allows for the impact of the projected EPS growth rates to be taken into account in the assessment of the value of Coca-Cola shares. The table shows to achieve the 7.5% return, the required average yearly share price growth rate from October 6, 2023 through December 31, 2025, is 3.82% (line 51). Dividends and dividend growth account for the balance of the target 7.5% total return.

Coca-Cola’s Projected Returns Based On Selected Historical P/E Ratios Through End Of 2025

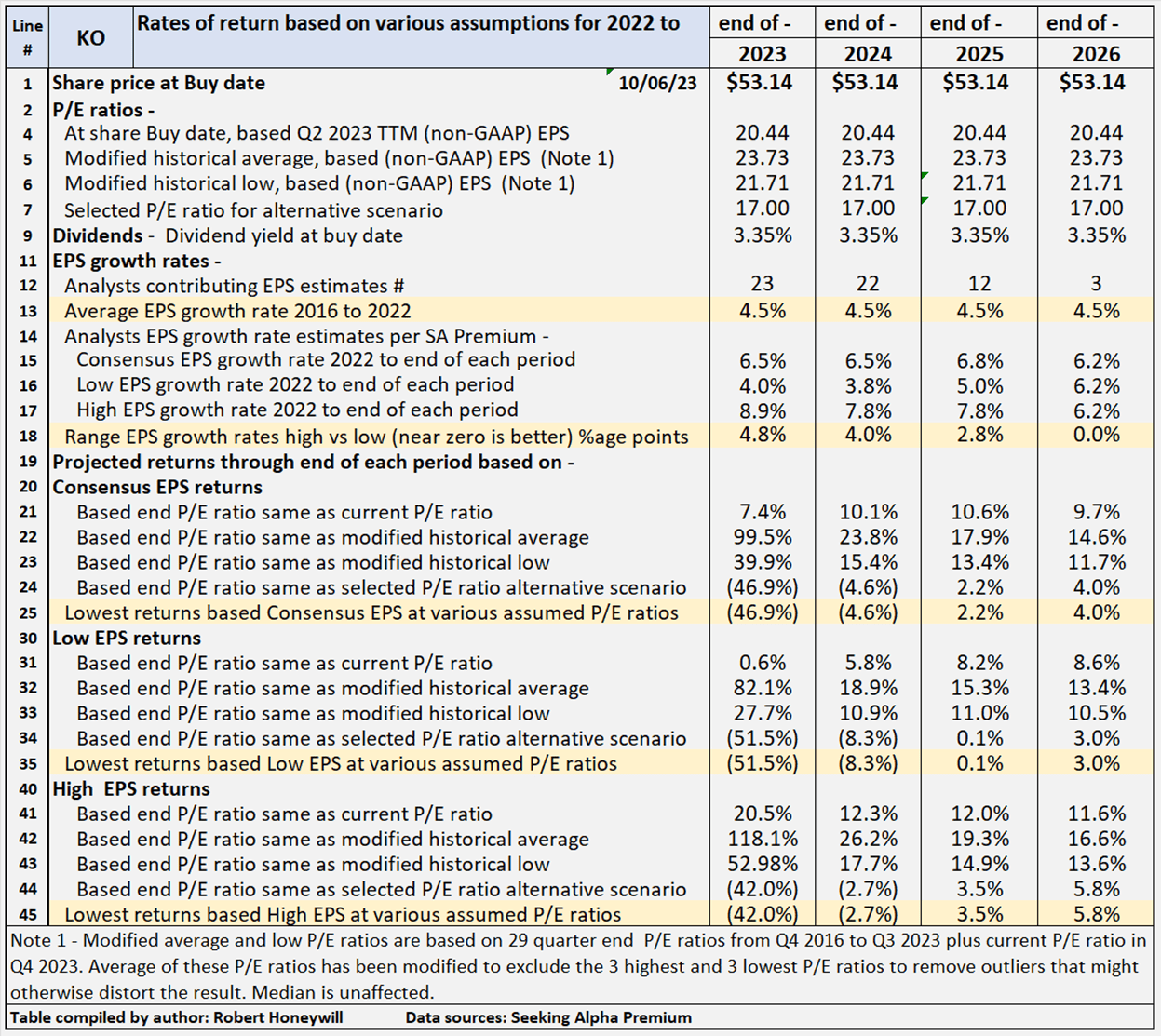

Table 2 below provides additional scenarios projecting potential returns based on select historical P/E ratios and analysts’ consensus, low, and high EPS estimates per Seeking Alpha Premium through end of 2025.

Table 2 – Summary of relevant projections Coca-Cola

Seeking Alpha Premium

Table 2 provides comparative data for buying at closing share price on October 6, 2023, and holding through the end of years 2023 through 2026. There’s a total of twelve valuation scenarios for each year, comprised of three EPS estimates (SA Premium analysts’ consensus, low and high) across three different P/E ratio estimates, based on historical data, plus a fourth P/E ratio selected to provide an alternative scenario. Coca-Cola’s P/E ratio is presently 20.44, which is below the historical average P/E ratio of 23.73. Table 2 shows potential returns from an investment in shares of the company across the range of P/E ratios This analysis, from hereon, assumes an investor buying Coca-Cola shares today would be prepared to hold through 2025, if necessary, to achieve their return objectives. Comments on contents of Table 2, for the period to 2025 column follow.

Consensus, low and high EPS estimates

All EPS estimates are based on analysts’ consensus, low and high estimates per SA Premium. This is designed to provide a range of valuation estimates ranging from low to most likely, to high based on analysts’ assessments. I could generate my own estimates, but these would likely fall within the same range and would not add to the value of the exercise. This is particularly so in respect of well-established businesses such as Coca-Cola. I believe the “low” estimates should be considered important. It’s prudent to manage risk by knowing the potential worst-case scenarios from whatever cause.

Alternative P/E ratios utilized in scenarios

- The actual P/E ratios at the share buy date are based on actual non-GAAP EPS for Q2-2023 TTM.

- A modified average P/E ratio based on 29 quarter-end P/E ratios from Q4 2016 to Q3 2023 and current P/E ratio in Q4 2023. The average of these P/E ratios has been modified to exclude the three highest and three lowest to remove outliers that might otherwise distort the result.

- A modified low P/E ratio calculated using the same data set used for calculating the modified average P/E ratio, and calculated on a similar basis, with the three highest and lowest P/E ratios excluded.

- A median P/E ratio is calculated using the same data set used for calculating the modified average P/E ratio. Of course, the median is the same whether or not the three highest and lowest P/E ratios are excluded. In the case of Coca-Cola, I have chosen to use an assumed P/E ratio of 17.0 in place of the historical median of 23.81 (similar to the average). I have done this to provide an idea of the impact on returns of the multiple declining significantly below the present level and the historical average. The selected P/E multiple of 17.0 compares to the sector median of 16.84 for PE Non-GAAP [FWD], per Seeking Alpha Premium metrics.

Reliability of EPS estimates (line 18)

Line 18 shows the range between high and low EPS estimates. The wider the range, the greater disagreement there is between the most optimistic and the most pessimistic analysts, which tends to suggest greater uncertainty in the estimates. There are twelve analysts covering Coca-Cola through end of 2025. In my experience, a range of 2.8 percentage points difference in EPS growth estimates among analysts is low, and suggests a fairly high degree of certainty, and thus increased reliability.

Projected Returns (lines 19 to 45)

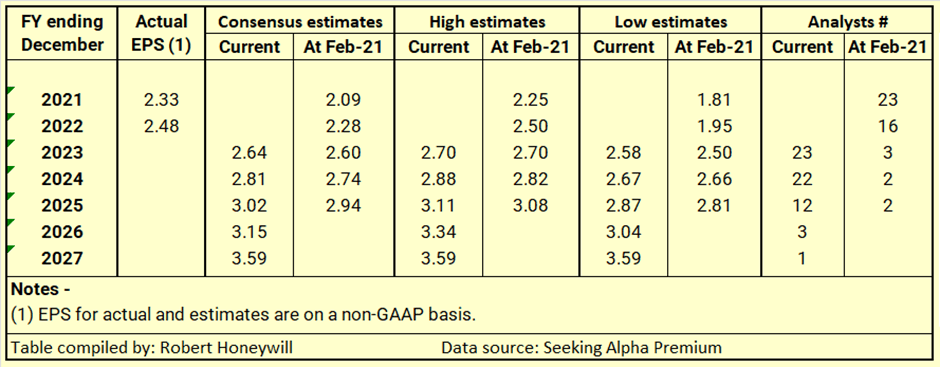

Lines 25, 35 and 45 show, at a range of historical P/E ratio levels, Coca-Cola is conservatively indicated to return between 0.1% and 3.5% average per year through the end of 2025. The 0.1% return is based on analysts’ low EPS estimates and the 3.5% on their high EPS estimates, with a 2.2% return based on consensus estimates. Those are the lowest of the returns under the consensus, low and high EPS scenarios and assume a P/E multiple at 17.0, roughly in line with the sector average. At Coca-Cola’s historical average P/E multiple of 23.73, the indicative returns range from 15.3% to 19.3%, with consensus 17.9%. If Coca-Cola’s present multiple of 20.44 continued through 2025, returns ranging from 8.2% to 12.0% are indicated, with consensus 10.6%. Coca-Cola has been regularly beating analysts’ estimates, causing analysts to increase their EPS estimates over time, as shown in Table 3 below.

Table 3

Seeking Alpha Premium

The increases in analysts’ EPS estimates over time encourages me to believe Coca-Cola’s multiple is likely to remain around or above the current level, at which levels double digit returns are indicated for holding through end of 2025.

Checking Coca-Cola’s “Equity Bucket”

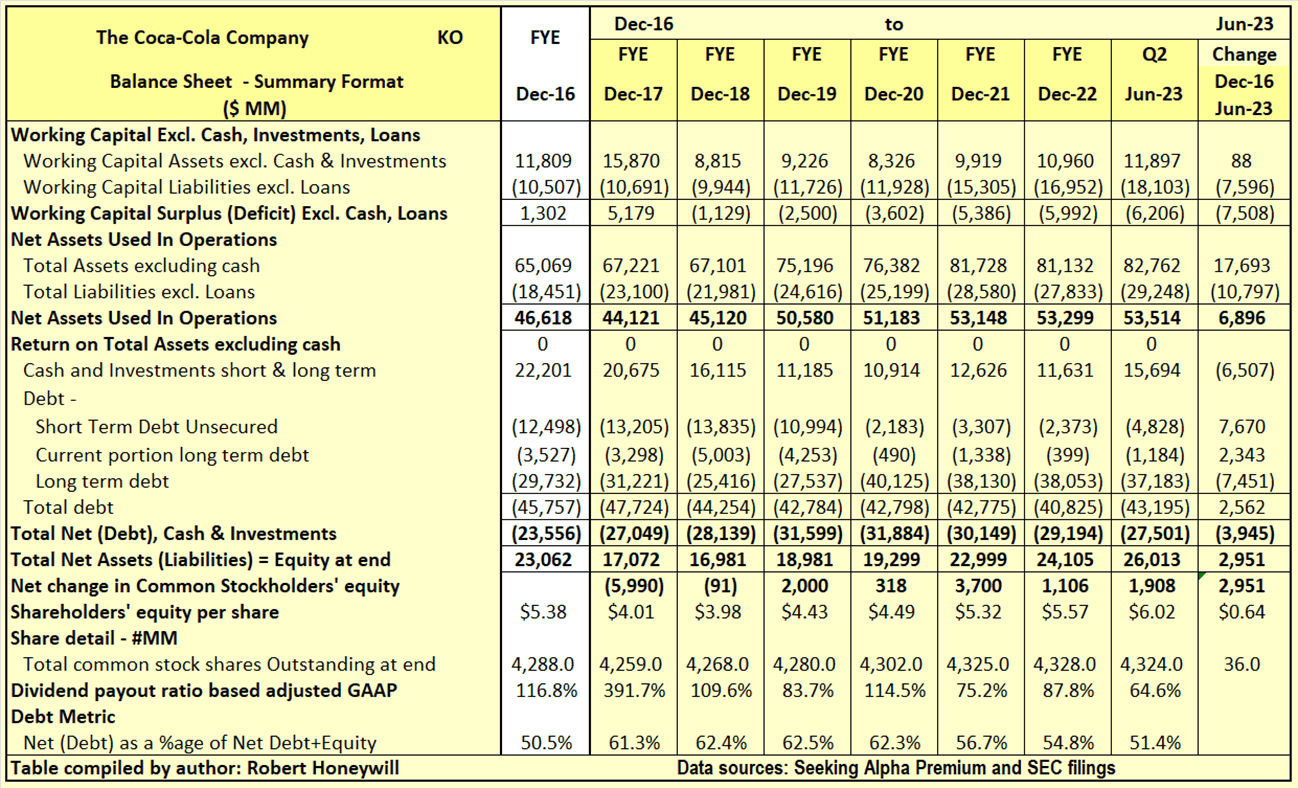

Table 4.1 Coca-Cola Balance Sheet – Summary Format

Seeking Alpha Premium and SEC filings

Over the 6.5 years end of 2016 to end of Q2-2023, Coca-Cola increased Net assets used in operations by $6,896 million. This $6,896 million increase was funded by a $3,945 million increase in debt net of cash, and a $2,951 million increase in shareholders’ equity. Net debt as a percentage of net debt plus equity has increased slightly from 50.5% at end of 2016 to 51.4% at end of Q2-2023. Outstanding shares increased by 36.0 million from 4,288 million to 4,324 million, over the period, due to shares issued for stock compensation, partly offset by share repurchases. The $2,951 million increase in shareholders’ equity over the last 6.5 years is analyzed in Table 4.2 below.

Table 4.2 Coca-Cola Balance Sheet – Equity Section

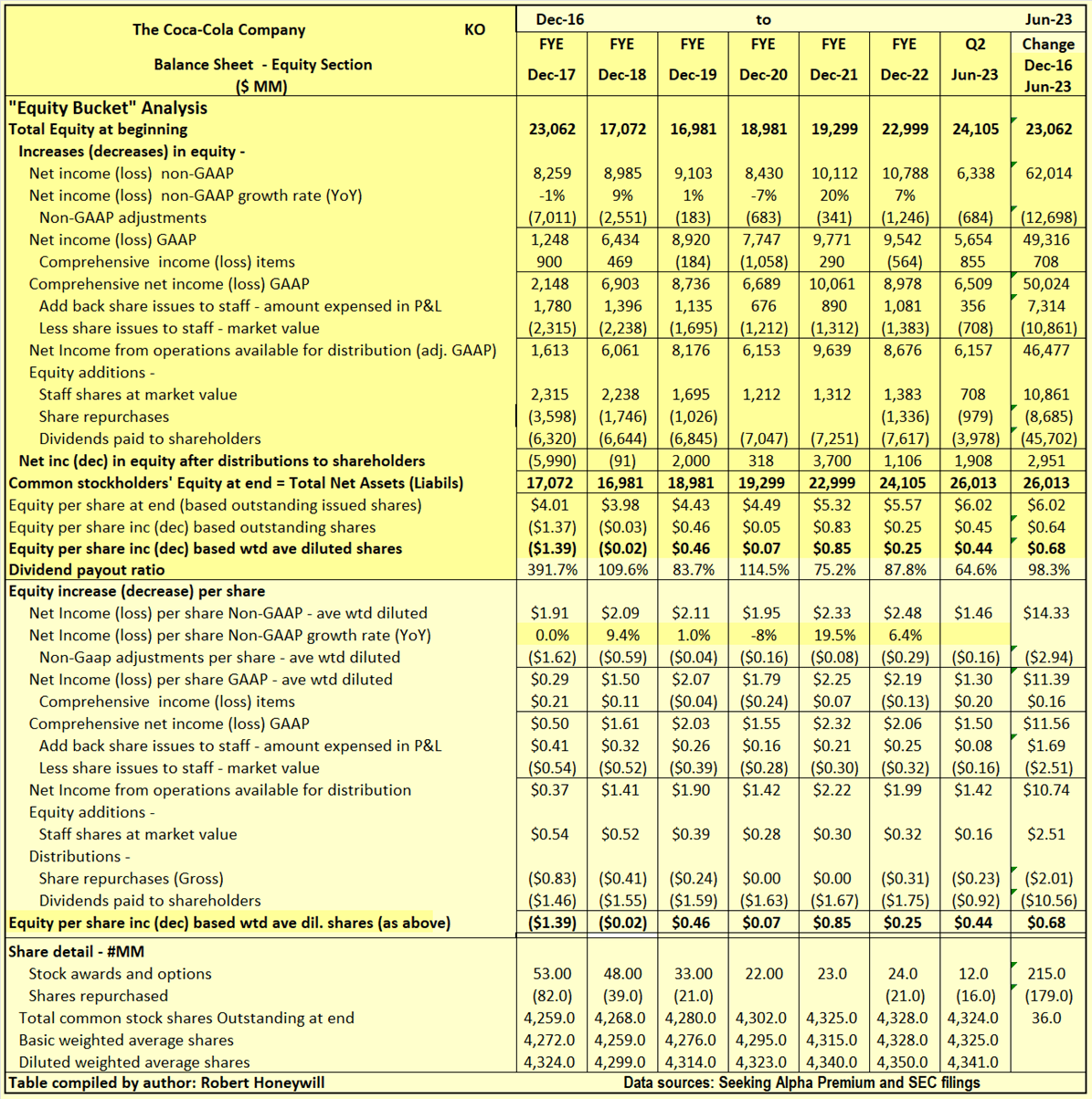

Seeking Alpha Premium and SEC filings

I often find companies report earnings that should flow into and increase shareholders’ equity. But often the increase in shareholders’ equity does not materialize. Also, there can be distributions out of equity that do not benefit shareholders. Hence, the term “leaky equity bucket.” I look for evidence of this in my analysis of changes in shareholders’ equity. Coca-Cola’s “leaky equity bucket” issues are towards the worst end of the spectrum.

Explanatory comments on Table 4.2 for the period end FY-2016 to end Q2-2023.

- Reported net income (non-GAAP) over the 6.5-year period totals to $62,014 million, equivalent to diluted net income per share of $14.33.

- Over the 6.5 year period, the non-GAAP net income excludes a significant $12,698 million (EPS effect $2.94) of items regarded as unusual or of a non-recurring nature in order to better show the underlying profitability of Coca-Cola. It always is of concern when companies exclude costs year after year on the basis they are temporary or unusual.

- Other comprehensive income includes such things as foreign exchange translation adjustments in respect to buildings, plant, and other facilities located overseas and changes in valuation of assets in the pension fund – these are not passed through net income as they fluctuate without affecting operations and can easily reverse in a following period. Nevertheless, they do impact on the value of shareholders’ equity at any point in time. For Coca-Cola, these items were income positive $708 million (EPS effect $0.16) over the 6.5-year period.

- Amount taken up in equity to account for shares issued to staff over the 6.5 years is $7,314 million. This compares to an estimated market value of $10,861 million at the time of issue for these shares. The real cost of these shares is greater by $3,547 million (EPS effect $0.82) than allowed for in arriving at non-GAAP EPS, a material difference.

- By the time we take the aforementioned items into account, we find, over the 6.5 year period, the reported non-GAAP EPS of $14.33 ($62,014 million) has decreased to $10.74 ($46,477 million), added to funds from operations available for distribution to shareholders.

- This $46,477 million is sufficient to cover dividends of $45,702 million, leaving an adjusted net operating surplus after dividends of $775 million. On this basis, dividend payout ratio is 98.3%.

- Issue of shares by way of stock compensation effectively raised $10,861 million through the issue of 215 million shares to staff at an average market price of $50.52 per share (without these issues this staff compensation would have required cash of $10,861 million to provide similar compensation benefit (ignoring differing tax treatment for cash versus stock compensation). These staff share issues were offset in part by repurchase of 179 million shares for $8,685 million at an average price of $48.52 per share. The net effect of shares issued to staff less shares repurchased was an increase in shareholders’ funds of $2,176 million ($10,861-$8,685).

- The foregoing analysis shows the $2,951 million net increase in shareholders’ funds per Table 4.1 above was comprised of the $2,176 million net capital raised through issue of shares to staff offset by share repurchases, plus the adjusted net operating surplus after dividends of $775 million.

Coca-Cola: Summary and Conclusions

The current dividend yield is 3.35% and dividend yield on cost is projected to grow to 3.76% by end of 2025, underpinning potential returns. There also appears to be an opportunity for share price gains from EPS growth, which could be further magnified by multiple expansion. With a potential for double digit returns from buying now and holding through end of 2025, Coca-Cola is upgraded from Hold to Buy.

Analyst’s Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Disclaimer: The opinions in this document are for informational and educational purposes only and should not be construed as a recommendation to buy or sell the stocks mentioned or to solicit transactions or clients. Past performance of the companies discussed may not continue and the companies may not achieve the earnings growth as predicted. The information in this document is believed to be accurate, but under no circumstances should a person act upon the information contained within. I do not recommend that anyone act upon any investment information without first consulting an investment advisor and/or a tax advisor as to the suitability of such investments for their specific situation. Neither information nor any opinion expressed in this article constitutes a solicitation, an offer, or a recommendation to buy, sell, or dispose of any investment, or to provide any investment advice or service. An opinion in this article can change at any time without notice.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.