Summary:

- UnitedHealth Group is one of the world’s largest health insurance companies, headquartered in Minnetonka.

- On October 13, UnitedHealth Group will publish its financial report for the third quarter of 2023.

- The company’s stable operating profit growth has been extremely favorable to its 10-year dividend growth rate [CAGR], which is 21.77%.

- We believe that one of the key reasons behind UnitedHealth Group’s beating the consensus EPS in recent quarters is its aggressive use of its share repurchase program.

- We initiate our coverage of UnitedHealth Group with an “outperform” rating for the next 12 months.

Cecilie_Arcurs

UnitedHealth Group (NYSE:UNH) is one of the world’s largest health insurance companies, headquartered in Minnetonka. For decades, the company has played a key role in the healthcare sector, providing its services and products through two business platforms, Optum and UnitedHealthcare, helping to improve the quality of life of hundreds of millions of people.

Optum provides a wide range of services in the healthcare market through Optum Health, Optum Insight, and Optum Rx. The crucial division is Optum Health, which is focused on providing surgical, primary, and urgent care to approximately 103 million customers.

This division partners with various care delivery systems, companies, and government organizations to improve the services’ quality and reduce costs for its clients. As a result, Optum Health continues to introduce advanced digital health technologies such as remote patient monitoring and real-time patient consultations with doctors. We believe that as the 5G network expands in the United States, demand for Optum Health’s services will only increase as it allows more people living in remote places to access high-quality health care.

UnitedHealthcare provides health insurance products and ensures Americans have access to health care through a network of approximately 1.7 million physicians and 6,400 hospitals and other facilities. In the three months ending June 30, 2023, UnitedHealthcare businesses served about 52.84 million individuals worldwide, an increase of 1.59 million compared to the previous year. As a result, this shows that the business strategies implemented by the company’s management continue to be extremely effective. Moreover, we believe that this trend will continue as UnitedHealthcare continues to expand the range of services it offers faster than competitors and also has numerous partnerships with medical laboratories and clinics that help reduce the cost of care for customers.

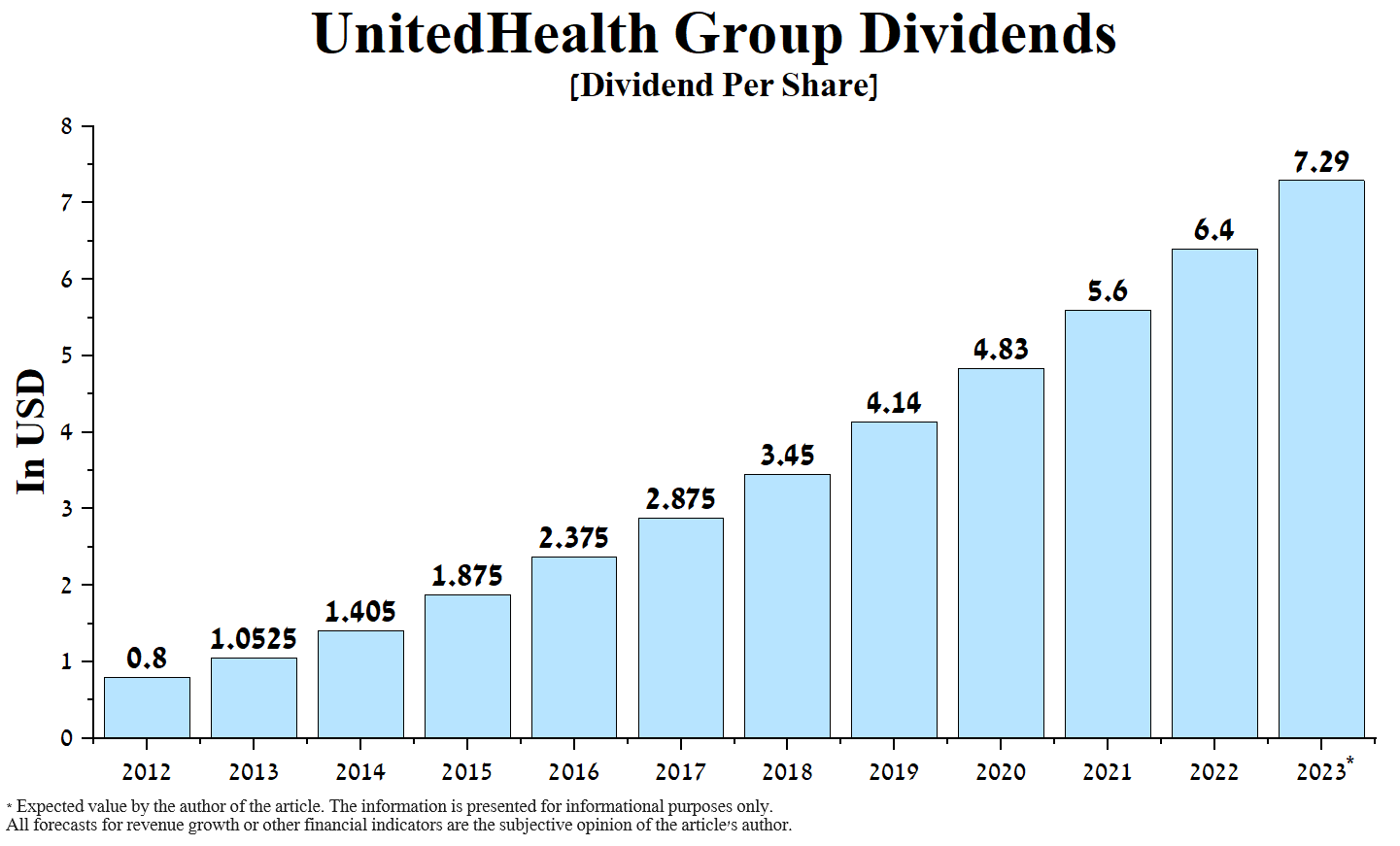

Over the last fourteen years, UnitedHealth Group has consistently raised its dividend payments annually. The company’s stable operating profit growth has been extremely favorable to its 10-year dividend growth rate [CAGR], which is 21.77%. This figure is significantly higher compared to the healthcare sector and is thus one of the factors attracting financial market participants to invest in UnitedHealth Group.

Author’s elaboration, based on Seeking Alpha

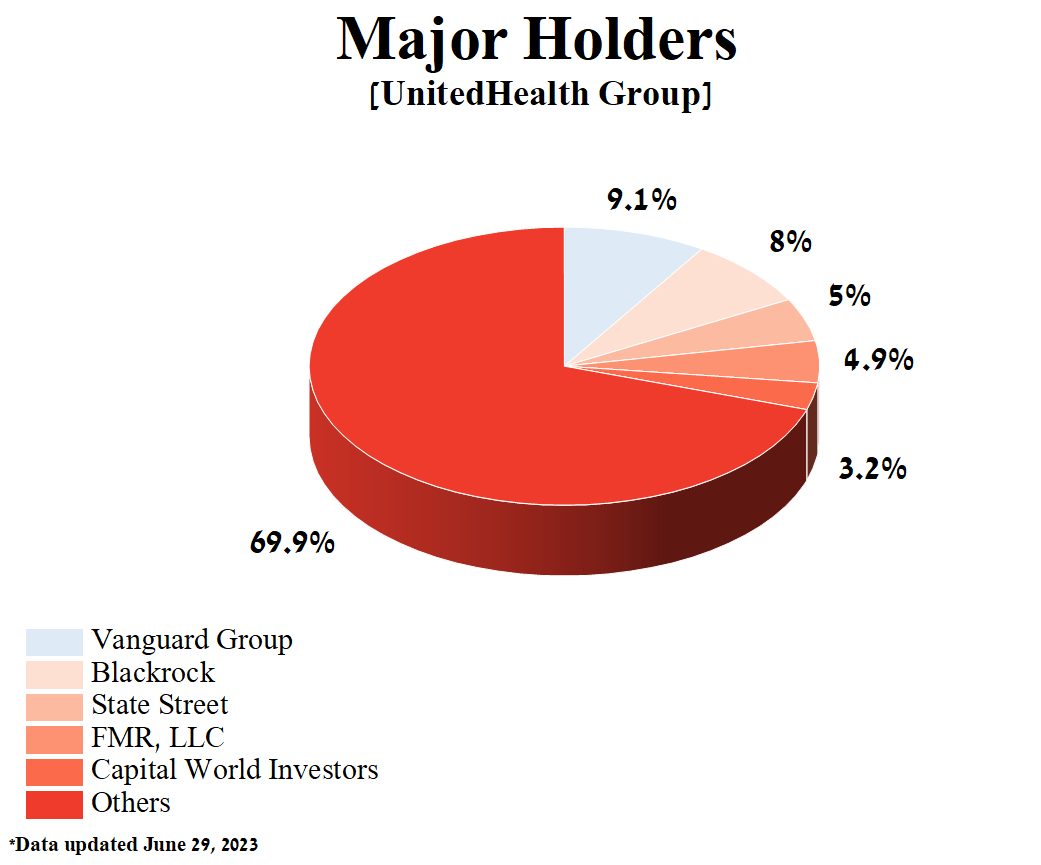

UnitedHealth Group has historically attracted significant investment from key Wall Street giants. So, the company’s five largest shareholders, owning 30.07% of its shares, are Vanguard Group, State Street, Capital World Investors, FMR, and Blackrock.

Author’s elaboration, based on Yahoo Finance

The second quarter of 2023 showed outstanding results as UnitedHealth Group’s revenue and EPS exceeded analysts’ expectations. In addition, its Optum Rx division’s revenue continues to grow at double-digit percentages year over year despite increased competition in the U.S. pharmacy benefit management market.

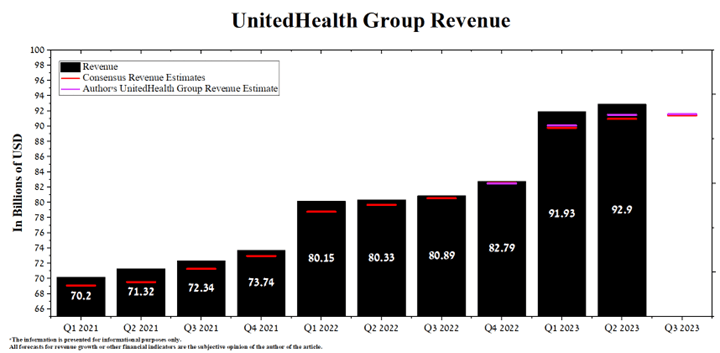

On October 13, UnitedHealth Group will publish its financial report for the third quarter of 2023. According to our assessment, it should once again please investors with the growth of its revenue and the preservation of high margins relative to competitors despite the persistence of inflationary pressure.

According to Seeking Alpha, UnitedHealth Group’s third-quarter 2023 revenue is expected to be $88.99-$92.74 billion, up 11.9% year-over-year and 0.5% higher than analysts’ expectations for the previous quarter. At the same time, following our model, the company’s total revenue will be within this range and will amount to $91.6 billion. UnitedHealth Group’s revenue growth, year-over-year and quarter-over-quarter, will be driven by a gain in the number of new clients served, increased script volumes, and expanded membership of existing customers.

Author’s elaboration, based on Seeking Alpha

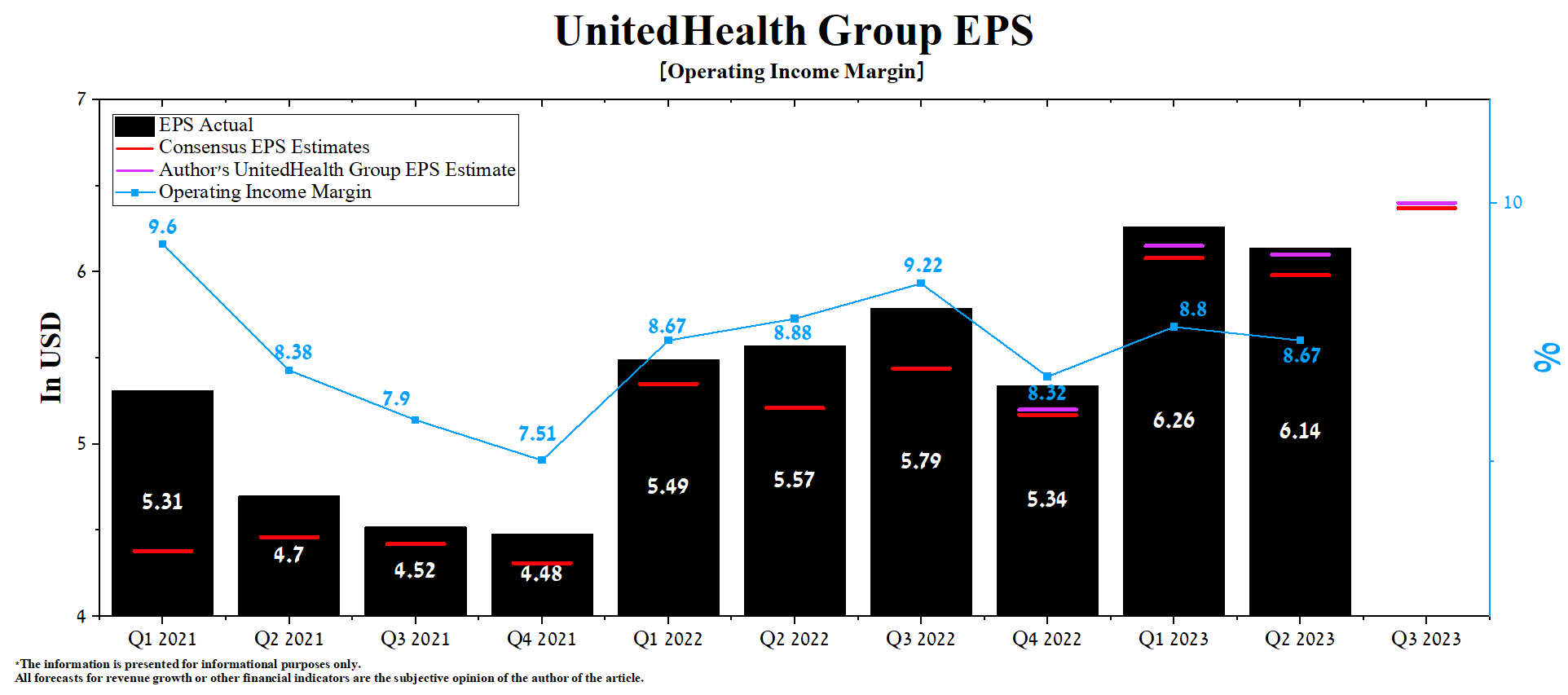

We forecast that UnitedHealth Group’s operating income margin will reach 8.5% by 2023. At the same time, in 2024, this financial metric will increase to 9.1% due to an increase in the number of services and products provided, optimization of labor costs, an increase in the number of people served under the Medicare Advantage and Medicaid programs and a decrease of the expenses associated with the consequences of COVID-19.

According to Seeking Alpha, the company’s third-quarter EPS is expected to be $6.18-$6.73, up 6.5% from the consensus estimate for the second quarter of 2023. At the same time, according to our model, UnitedHealth Group’s EPS will be slightly higher and amount to $6.4.

Moreover, the company’s Non-GAAP P/E [TTM] is 22.3x, 26.83% higher than the sector average and 3.16% higher over the average over the past five years. On the other hand, UnitedHealth Group’s Non-GAAP P/E [FWD] is 21.1x, which is one of the factors indicating its slight overvaluation by Wall Street ahead of the upcoming respiratory viral infections season.

Author’s elaboration, based on Seeking Alpha

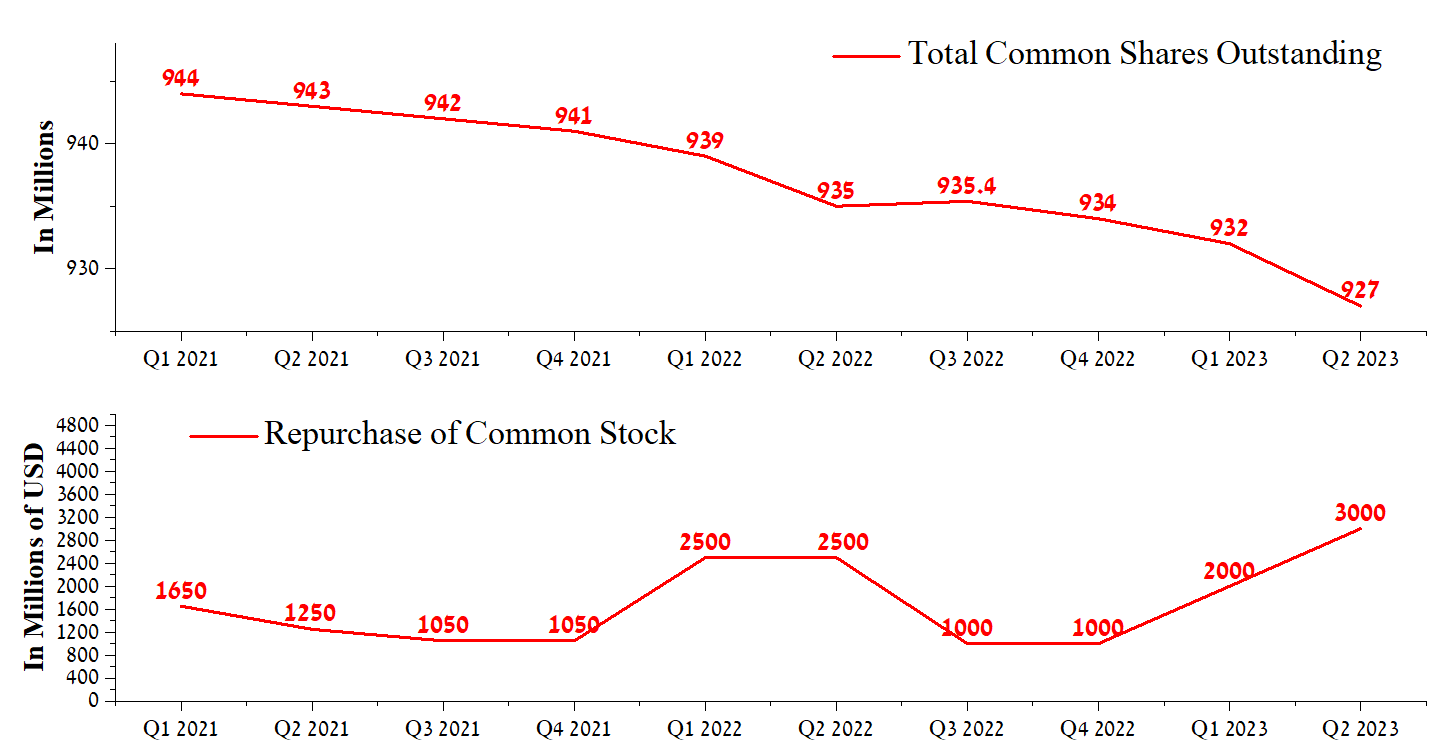

We believe that one of the key reasons behind UnitedHealth Group’s beating the consensus EPS in recent quarters is its aggressive use of its share repurchase program.

During the second quarter of 2023, UnitedHealth Group repurchased shares for about $3 billion, which is $1 billion more than the previous quarter and $500 million more than the second quarter of 2022. At the same time, at the end of June 2023, the company’s management has authorization to buy out up to 21 million of its shares, which will minimize the influence of short sellers during a period of increasing deterioration in the geopolitical and macroeconomic situation in the world.

Author’s elaboration, based on Seeking Alpha

Conclusion

UnitedHealth Group is one of the world’s largest health insurance companies, headquartered in Minnetonka. For decades, the company has played a key role in the healthcare sector, providing its services and products through two business platforms, Optum and UnitedHealthcare, helping to improve the quality of life of hundreds of millions of people.

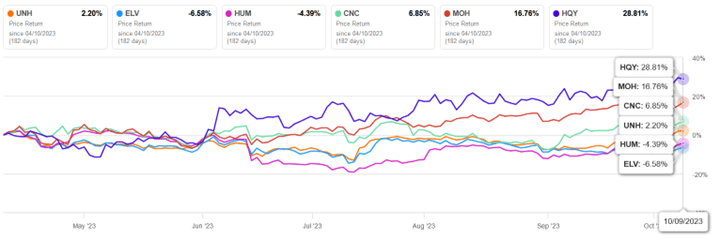

With UnitedHealth Group’s revenue growing quarter over quarter and maintaining a total debt/EBITDA ratio below 2x, which indicates there are no significant risks to the redemption of senior notes, the company’s share price has increased by more than 2% over the past six months, outperforming Humana (HUM), one of its key competitors.

Author’s elaboration, based on Seeking Alpha

We expect the company’s financial position to continue to improve, driven in part by increased demand for healthcare services due to the relatively rapid aging of the US population and the need to minimize the impact of the long-term effects of COVID-19.

We initiate our coverage of UnitedHealth Group with an “outperform” rating for the next 12 months.

Analyst’s Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

This article may not take into account all the risks and catalysts for the stocks described in it. Any part of this analytical article is provided for informational purposes only, and does not constitute an individual investment recommendation, investment idea, advice, offer to buy or sell securities, or other financial instruments. The completeness and accuracy of the information in the analytical article are not guaranteed. If any fundamental criteria or events change in the future, I do not assume any obligation to update this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.