Summary:

- The article discusses the performance of Disney in 2018, focusing on revenue, profit margins, and the potential for matching Netflix’s margins.

- Let us never forget, that Disney is and will probably continue to be the an effective ambassador abroad. That alone makes the brand invaluable as many foreign nationals’ first “American”experience.

- The company is undervalued on both my modified Graham number bear case and owner earnings model bull case.

Wirestock

Blast back to 2018

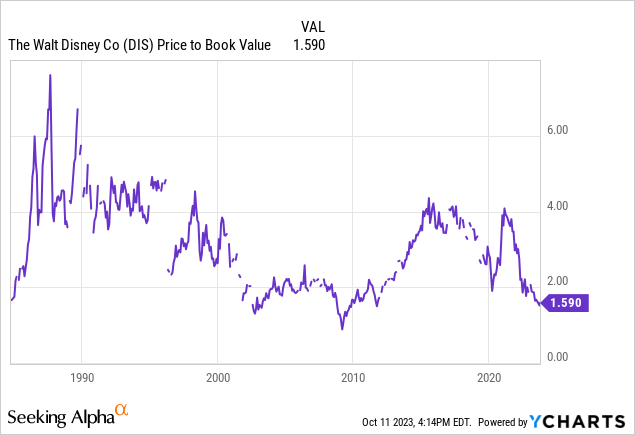

Of the few concentrated bets that I’m still adding to, The Walt Disney Company (NYSE: DIS) is amongst my top 10 single holdings currently by size that I hold and add to, having bought the majority of my shares under $95. I previously wrote an article on Disney and consider it one of the better deals in the market for a variety of reasons. The asset value of the company is my greatest attraction to the stock. In short, the stock hasn’t seen price-to-book values this low since the early 2000s.

The ultimate turnaround will be when Disney+ margins begin to approach those of other successful streaming companies. If we look at Disney 2018, the company was firing on all cylinders largely through the DPEP [Disney Parks, Experiences and Products] side of the business. As the linear starts to get phased out and newly returned CEO Bob Iger transitions the television content more towards the direct-to-consumer streaming business, we should hope to see more normalized margins that ideally would be a mix of Netflix (NFLX) and 2018 Disney margins.

If this is achieved with the current large increase in revenue since adding Disney+, then we have a very undervalued stock on our hands.

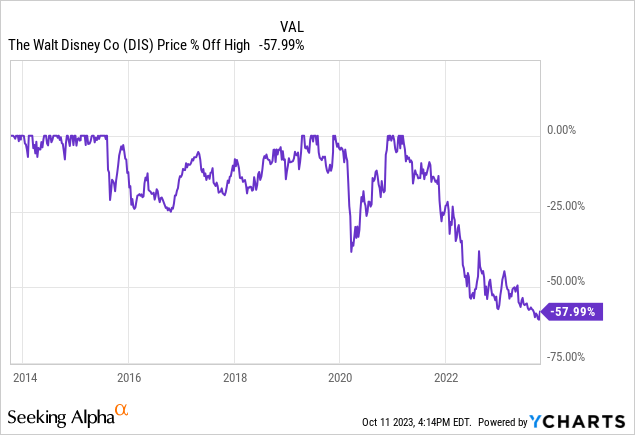

Percent off high

Disney continues lower and continues to whet my appetite even further. This next leg down below what I considered fair value in my previous article has enticed me to once again add.

Division of revenues and income

According to Fact Set, the division of Disney revenues follows the below categories:

| Revenue Category | Percentage |

| Entertainment and Programming | 41.66% |

| Web Based Data and Services | 23.64% |

| Parks and Recreation [DPEP] | 20.63% |

| Accommodation providers | 7.75% |

| Retail sales | 6.32% |

Although Fact Set breaks down the revenues into a few different subcategories, Disney generally classifies them as DMED for the media side and DPEP for the parks and hotel side. The DMED business represented about 35% of total operating income for FY22 and DPEP 65%. So in this case we have huge revenues with slim margins on the media business and lower revenues with higher margins on the parks/entertainment and retail side.

The equation here for a turnaround looks quite clear, enhance the parks business with greater CAPEX and cut the fat on the media side now that a customer base has been established. The linear media business also needs to be slowly merged into the “Web Based Data and Services” portion, or streaming. No small feat. However, Netflix has shown us that fairly high operating and profit margins can be achieved in direct-to-consumer streaming. Replicating it is the ultimate goal.

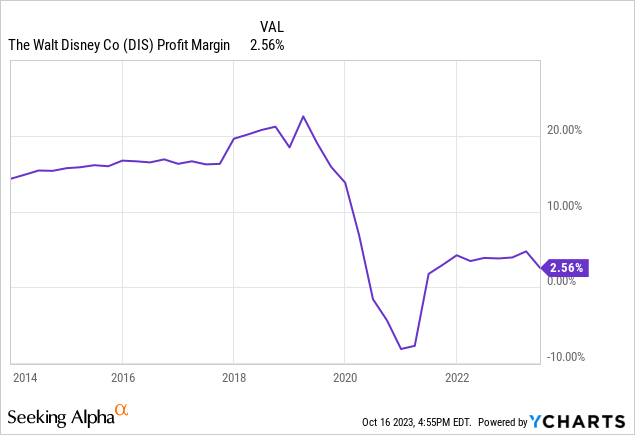

Margin trends

Disney Profit Margins (Seeking Alpha)

This used to be a very healthy margin business. I cut off the chart in 2018 because this was the apex of Disney’s profit margins under Iger and right before COVID-19 hit. If I average out the profit margin numbers from 2013 to 2019, we still come up with 17.17% profit margins across this period. While I don’t expect the business to be achieving similar margins any time soon with the additional layer of complexity related to Disney+, if we mix the margins with one of the best examples in Netflix, this should generate a GAAP net income that would be enviable.

Disney

Disney+ was launched on November 12, 2019. This combined with park closures during Covid and the departure of Iger resulted in negative profit margins for a short stint. The recovery has been slow and not entirely pretty.

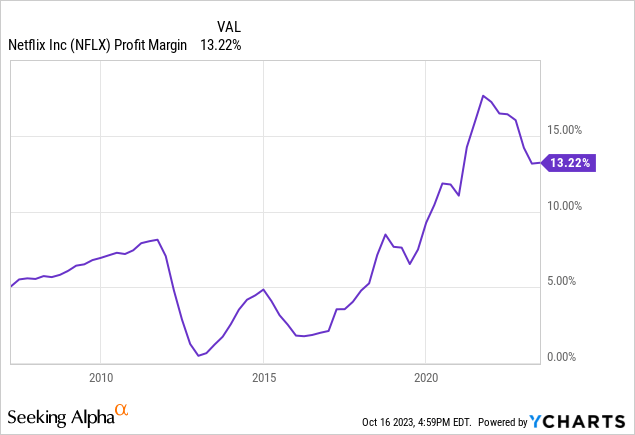

Netflix (NFLX)

Back to Netflix as a comp for what all streaming services aim to achieve. While Netflix has been around longer than 2009, streaming was introduced during this period. It took the good part of 7 years to achieve a steady upward trajectory for positive margin trends while the company also began to phase out the physical disk business. I wasn’t even aware, but Netflix still mailed DVDs up to September of this year. Any dying business will have a long tail and take time to phase out.

That being said, part of the difficult trek to profitability for Netflix had to do with the adoption of streaming. Luckily streaming has now become the norm, so Disney does not have to fight that battle. Streaming competition is also more fierce than ever, but Netflix has built a blueprint that should speed up the process to ascending margins in about half the time as it took Netflix. If it took Netflix 7 years, I’d like to think Disney could start that trajectory in 3.5-4 years. We should be near the sweet spot for margin improvement.

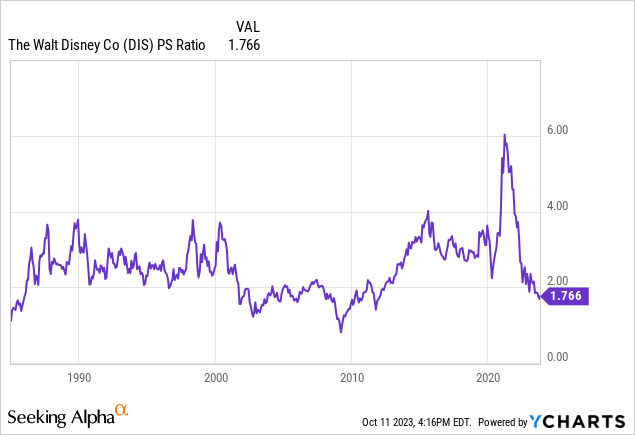

Revenue, the lifeblood of profit

From a price-to-sales perspective, Disney is trading cheaply. It is trading at one of its cheapest valuations in a decade.

For all the flack that Disney has received for the difficult rollout of their streaming product and the downward trajectory of their linear products, they have created more revenue. Revenue, I would argue, is as hard or harder to produce than income. Yes, you can subsidize a product, make it almost free, and book some revenue through the company or investors being willing to eat negative margins. However, money isn’t free. The company providing the subsidies must have a brand and excellent pro forma to garner the backers.

With revenue being the lifeblood of profit, creating more of it is the key to future growth. Margin expansion is the next step in Disney’s growth story. They could have sat around on the linear media business, let it slowly die, and remained pretty profitable just based on the parks, hotel, and merchandise businesses. However, they have chosen to modernize and grow. I appreciate that as an investor but also realize that the profits will take time to materialize.

What if Disney can match Netflix’s margins?

This is not a now or a next-year supposition, but even a few years off still seems like a good value to me. If Disney can successfully merge into full DTC streaming on the media side, achieve Netflix’s current margins and grow revenue at 8-9% during the meantime, that would be my bull case. Even disregarding any revenue growth, let’s see what that margin mix would look like:

Data courtesy of Seeking Alpha

- Total TTM revenue: $87.8 Billion

- DPEP: 34% of revenue at: $29.85 Billion at 17.7% average pre-Covid margins= $5.28 Billion net income.

- DMED: 66% of revenue at: $57.9 Billion at Netflix margins of 13%= $7.64 Billion net income.

- Total net income based on margin assumption mix of $12.92 Billion.

The above scenario is static and based on today’s revenue numbers. This would get us back to the best Disney operating year on record, 2018, which saw a net income of $12.598 Billion. Using CFRA analyst Kenneth Leon‘s next year 9.4% growth estimates for Disney’s top line would get us to $13.85 Billion net income. Again, these are modeled estimates for everything pumping on all cylinders, the bull case. That would mean that Disney is trading at 11 X future potential earnings.

Still cheap on based on assets

In my previous article, I looked at Disney primarily on an asset basis. Since then, the price-to-book value has hit even further lows. Being that Disney is in a turnaround phase, with lots of write-offs and expenses, I used a modified Graham number using the book value and EBITDA per share as a proxy to income. Here is an update on that model for where we stand today:

- Disney TTM book value per share: $53.34

- Disney TTM EBITDA/Share: $7.1/share

- Graham Number= SQRT 22.5 X BV X EBITDA/share = 22.5 X $53.34 X $7.1= $92.3 a share.

Building a model, value if a turnaround succeeds

In my bull case price model I will be making the following 2025 future assumptions using a Buffett Owner Earnings Model with TTM numbers bumped up by 10%:

- $13.85 Billion net income based on $94 Billion in revenue (a 10% revenue increase)

- Depreciation and Amortization of $5.75 Billion (a 10% D&A increase)

- CAPEX of $5.217 Billion (a 10% CAPEX increase)

- A risk free discount rate of 5% assuming flat rate trends.

Owner earnings model:

All numbers in millions:

- NI 13,850 + 5,750 D&A = 19,600

- 19,600 – 5,217 CAPEX = 14,383

- 14,383 / 5% RFR = $287,660 market cap

- 287,660 / 1840 assumed shares outstanding at an average .03% increase in float per annum = $156.33/share

What if the margins never materialize

On the flip side, if those margins never materialize, this would still be a value, but only based on the asset value of the company, which I believe is more than the recorded book value based on the real estate holdings alone. What if Disney were only able to achieve just above their current margin trends on the DMED side? Let’s run the same Owner Earnings model under these assumptions:

- DMED, 66% of $94 Billion in revenue equivalent to $62.04 Billion. At 3% margins would be equivalent to $1.83 Billion.

- DPEP at 34% of $94 Billion in revenue equivalent to $31.96 Billion at 17.7% margins would be equivalent to $5.65 Billion

- Net income $7.48 Billion

- + $5.75 Billion D&A= $13.23 Billion

- Minus $5.217 CAPEX = $8.017 Billion “Owner Earnings”

- Discounted at a 5% RFR= $160.34 Billion fair market cap

- Divided by shares outstanding = $87.14 a share

The key to unlocking value will be the DMED margin improvement. I was being conservative in the above scenario and would expect the parks and resorts to contribute more income than the model with the proposed CAPEX bump in the next decade. Again, in even the worst of scenarios, I’m seeing Disney trading at or slightly below its fair value.

Political issues, how does the rest of the world feel?

This is not the first time I have written about Disney. I am very interested in keeping myself abreast of the company since it has become one of my larger holdings. Having traveled extensively, I would have to say that Disney has maintained its brand appeal internationally even though it has deteriorated domestically. It is still one of the first places on the list to visit should a foreign national set foot in one of the various locations that have a Disney Park.

As someone who leans to the right side of the political spectrum, I also acknowledge what some of my readers have pointed out, some liberal, US-based issues have seeped into the Disney media content. This is not prescient throughout the rest of the world where Disney is known solely for its Parks, Hotels, and retail products.

I have seen recent feature-length films put out by Disney, and while they were not all that impressive, none of them struck me as agenda-based either. I must also admit that I do not stream Disney+ or subscribe to the linear segments, but supply and demand should eventually reconfigure the offerings to a nice happy middle. Simply put, we are all customers, and business survival will eventually come down to pleasing all of your customers. Our demand will eventually modify the supply. The beauty of a capitalist economy is that the customer eventually wins in the end. The only way we don’t is if there is someone willing to subsidize an agenda.

DMED trends

Commentary courtesy of Disney MRQ 10Q:

“In November 2022, the Company purchased Major League Baseball’s (MLB) 15% redeemable non-controlling interest in BAMTech LLC (BAMTech), which holds the Company’s domestic DTC sports business, for $900 million (MLB buy-out). MLB’s interest was recorded in the Company’s financial statements at $828 million prior to the MLB buy-out.”

The biggest new news in Disney’s DMED segment with the return of Iger is the complete buyout of the engine behind Disney+ in BAMTech LLC. With complete ownership, the signal is now that DMED will start the transition to a direct to customer content approach as Disney has free rein to engineer the business. The recent spat with Charter (CHTR) emphasized Disney’s new, stronger positioning to negotiate with linear content providers.

Both sides reworked their linear and DTC streaming deals to enhance the ad revenue for Disney while making sure that Disney would remain a streaming option for Charter clients as they make their own transitions.

Subscriber deceleration

Statista.com

The YOY reduction in subscribers has not gone over well as evidenced by Disney share price trends. However, Disney and other streaming services are going the route of higher monetization per user at this point versus service price cuts to attract a greater number of eyeballs. This is bound to happen as price increases take hold and ads are placed across all the platforms.

Disney also has the advantage as evidenced by the Charter deal, to migrate their content to other streaming services outside of Disney+ where companies like Netflix do not enjoy that advantage. While they may not increase their subscriber revenue through this, the ad revenue will still be theirs. Ads on streaming will be the new norm and the key to higher margins.

10 Year $60 Billion DPEP CAPEX trends

Disney is looking to Double Down on the park CAPEX trends:

“Parks have become a reliable profit engine for Disney and has helped cushion losses in the Disney+ streaming business, which is expected to become profitable only next year. Iger has described the parks as “a tremendous business” for the California-based global entertainment company.

Disney said its parks, experiences and products segment has expanded at a combined annual growth rate of 6% since fiscal 2017, and generated $32.3 billion in operating income over the last 12 months, according to a presentation included in a regulatory filing.“

Iger has now seen his CEO contract extended through 2026 and intends to capitalize on the Theme Park’s profitability as much as possible during this duration. Not only are the parks doing very well, but the CAPEX is also needed to thwart competition like Universal Comcast (CMCSA), which recently opened its Super Mario-themed land at the California park and has larger expansion ambitions on the horizon in Florida as well.

I recently detailed my visit to Universal’s property in California, and it is certainly becoming a formidable foe. I am also a buyer of Comcast. This doesn’t have to be a zero-sum game. However, when I was younger, Universal struck me as more of a historical filmmaking experience rather than a ride experience. With the addition of Jurassic Park, Minions, Nintendo, and Harry Potter themes, my impressions have completely changed and Universal Parks now gives me the impression of a direct competitor to Disney domestically.

On the flip side, I don’t believe Comcast’s Universal Studio themes resonate even half as deeply with the rest of the world when they examine which international park to partake in. But if Disney gets lazy, that could soon change. I love that Iger recognizes its new opponent and is doubling down on their workhorse.

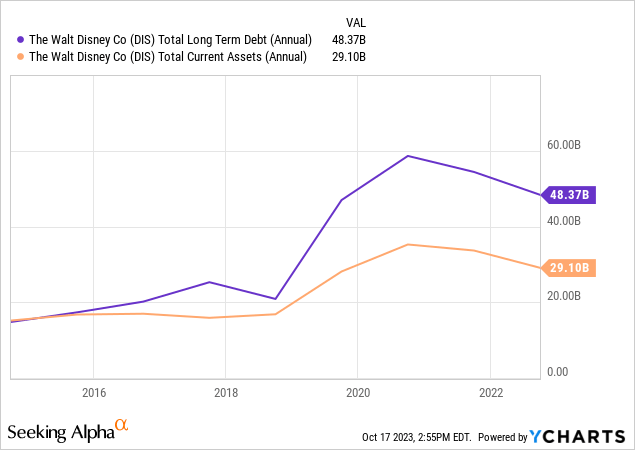

Balance sheet

Long term debt has seen a decline from its peak at near $60 Billion, now down to $48 Billion. Current assets are solid at near $30 Billion. The EBIT/net interest expense ratio is a healthy 5x. Not amazing, but ample coverage.

SeekingAlpha

We can see a clear deceleration in interest expense growth coming into TTM. As many analysts have noted, established companies with ample cash equivalents offset a lot of interest expense by collecting interest themselves on their cash positions.

Parting thoughts, the parks are as conservative as Apple Pie

What I do know about Disney is what the parks look like. Having recently been to the California park and considering going back again this October, the parks have stayed the same since I was a child. They decorate them beautifully for each season starting in October during the Halloween month and I am looking forward to seeing what California Adventure Park has in store for their unique Halloween theme. Disney, throughout the world, is a proxy for American culture. People in China, Japan, and Paris visit to get a taste of what traditional Americana feels like.

Let us never forget, that Disney is and will probably continue to be an important American cultural ambassador abroad. That alone makes the brand invaluable. Buy and undervalued on both my Bull and Bear cases.

Analyst’s Disclosure: I/we have a beneficial long position in the shares of DIS, CMCSA either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

The information provided in this article is for general informational purposes only and should not be considered as financial advice. The author is not a licensed financial advisor, Certified Public Accountant (CPA), or any other financial professional. The content presented in this article is based on the author's personal opinions, research, and experiences, and it may not be suitable for your specific financial situation or needs.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.