Summary:

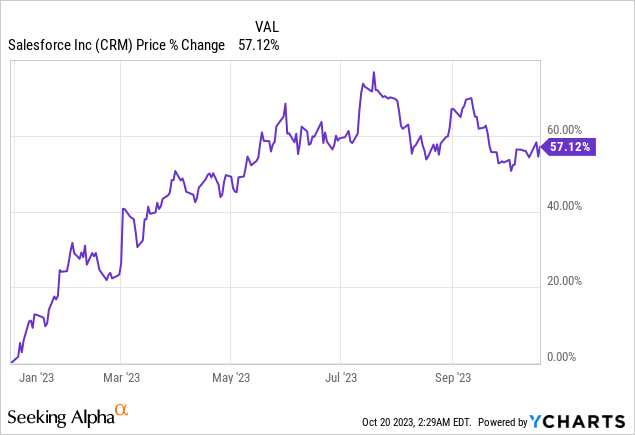

- Salesforce’s shares surged by approximately 57% over the year, driven by a strong focus on AI integration in its customer relationship management software.

- Despite its growth potential, Salesforce faces potential challenges related to macroeconomic factors affecting its sales cycle, which could impact its valuation.

- The company has made notable improvements in operating margins, with plans for further expansion, but a prolonged sales cycle remains a challenge in some industries.

- Salesforce invests in generative AI to boost its market position, but its valuation appears overpriced, as indicated by peer comparisons and a DCF model.

JasonDoiy

Salesforce (NYSE:CRM) has been among the tech giants that integrated AI into its business model, specifically within its customer relationship management software.

Throughout the year, Salesforce shares have surged by approximately 57%, driven by the AI revolution emphasized by CEO and founder Marc Benioff in the company’s recent earnings call. This surge reflects the growing expectations surrounding its revamped growth strategy, which aims further to enhance the company’s already impressive operating margins.

Nonetheless, despite the significant growth potential, the pace of Salesforce’s expansion will be influenced by macroeconomic factors impacting its sales cycle. If the company can sustain an 11% revenue growth rate in the next five years while preserving comparable levels of profitability, I do not find the company’s present valuation compelling. In my opinion, this represents the primary concern of the investment thesis.

Improved Operating Margin and Future Investments

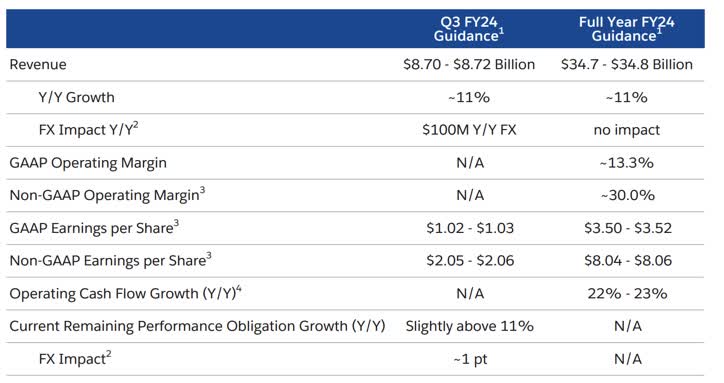

In the second quarter of fiscal year 2024, Salesforce delivered impressive results. The company forecasted an upper-end estimate of $34.8 billion from a revenue perspective, signifying approximately 11% year-over-year growth for the fiscal year 2024.

Salesforce’s IR

The standout feature of the latest results was the company’s operating margin, which reached 6%. This marked a significant increase of 5 percentage points, and there are plans to sustain this positive trend.

To achieve this, a short-term restructuring plan has been initiated to right-size the workforce and allocate resources to growth areas, such as Research and Development (R&D) in generative AI, MuleSoft, and Data Cloud. Currently, R&D accounts for 16% of the company’s total revenues.

While the company announced hiring 3,300 individuals, this was part of the strategic plan and aligned with the focus on growth. It’s worth noting that the majority of these hires are from India. Additionally, the company has raised its operating margin guidance to 30% for the entire fiscal year, with an expected year-over-year growth in cash flow of 22-23%. This reflects the significant shifts made by the company to prioritize profitability, as evidenced by the robust margin progression projected for the year, estimated at around 750 basis points year-over-year.

The company views the achieved 30% operating margin as a new baseline, with further expansion anticipated. Structural changes in business strategies, localization strategies, and automation efforts will drive this expansion.

Sales Cycle in the Current Macroeconomic Environment

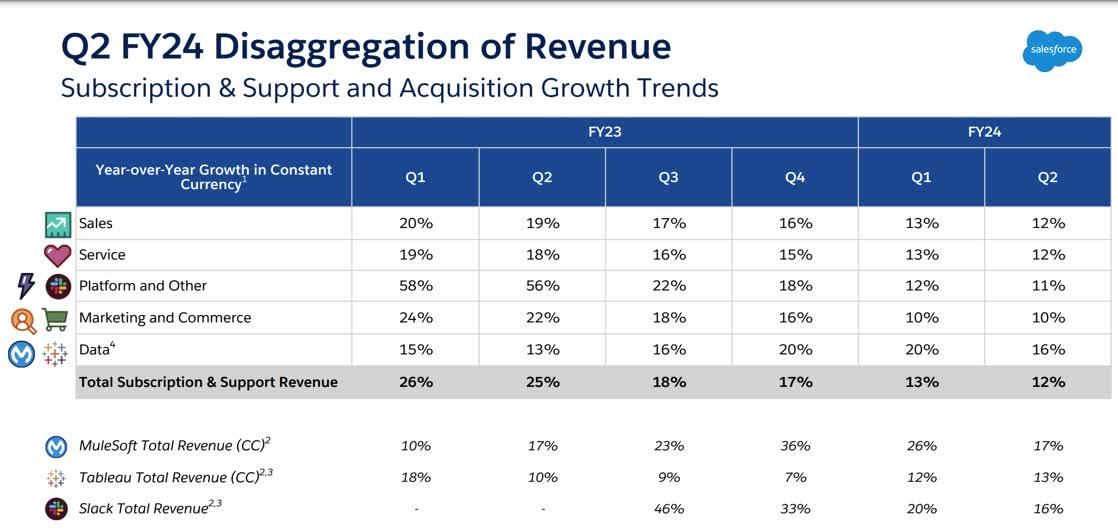

In recent years, Salesforce’s sales cycle has extended due to heightened scrutiny and increased approval levels within customer organizations. This has been primarily driven by uncertainties related to the macroeconomic situation.

To address this challenge, the company has adapted by offering sales enablement and training to assist account executives in navigating these complexities. The impact of this prolonged sales cycle has remained consistent over the past four quarters, with the most significant pressure experienced in the United States. Industries such as technology and retail have been particularly affected. Regarding specific product lines, Commerce Cloud, Marketing Cloud, and Slack have been impacted most.

Salesforce’s IR

Conversely, MuleSoft has shown strong performance. This can be attributed to changes within its sales organization, macroeconomic trends favorable to integration solutions, and preparations for embracing artificial intelligence (AI).

However, Tableau, which caters to a customer base focused on small and medium-sized enterprises (SMEs) and provides data visualization tools, has encountered some challenges in the current macroeconomic environment. The company is actively working on integrating its offerings with the Salesforce suite of products and expects ongoing growth from Tableau. It acknowledges that more work is still needed in this regard.

Driving Innovation with Generative AI

Salesforce has outlined several growth strategies, including international expansion, diversification across sectors, multi-cloud expansion, and ongoing innovation in data and AI. These areas will receive significant investment focus in the current fiscal year.

During Dreamforce, an AI event organized by Salesforce, the company introduced innovative and strategic changes to its marketing efforts. The Einstein 1 platform now encompasses various components of the generative AI platform, including Einstein 1 Sales, Einstein 1 Service, and Einstein 1 Marketing. This replaces Sales GPT and Service GPT. The company has introduced four domain features: sales email generation, service responses, case summarization, and product descriptions in commerce.

Salesforce’s approach is customer-centric, emphasizing trust and transparency. The company prioritizes enterprise security and data privacy, exemplified by the Einstein 1 Trust Layer. This layer allows public language models to access and read customer data but does not permit them to store or train on it.

Salesforce also promotes an open ecosystem approach, enabling customers to choose the model that best suits their needs, whether it’s Salesforce’s proprietary LLM (Large Language Models) or another solution.

Integrating generative capabilities into the workflow is a significant advantage, making it more efficient for sales representatives and service agents. This is a vast advantage point for the company, in my view.

Regarding the pricing model for Einstein 1, the pricing structure remains consistent with the previously announced $50 per user per month for Einstein-GPT. Customers must purchase specific SKUs for various services, but the primary monetization method is usage-based. Customers must be on the Unlimited Edition to access generic features, with additional SKUs required for sales.

It’s essential to monitor how Salesforce will evolve the pricing model over time, with a focus on a flat-rate, consumption-based approach. The company has also introduced a library to optimize prompts for the best possible results and cost efficiency.

Valuation: Not a Bargain

Companies with solid growth potential, particularly those emerging in AI, are often priced at a premium, and Salesforce is no exception. It is far from being a bargain.

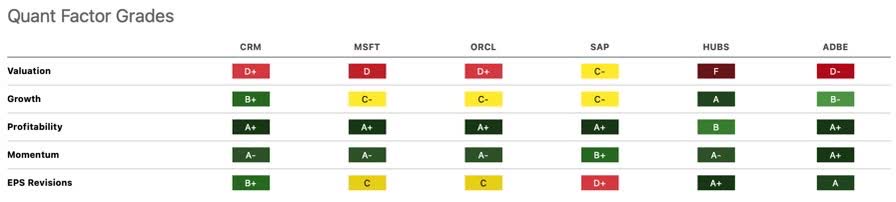

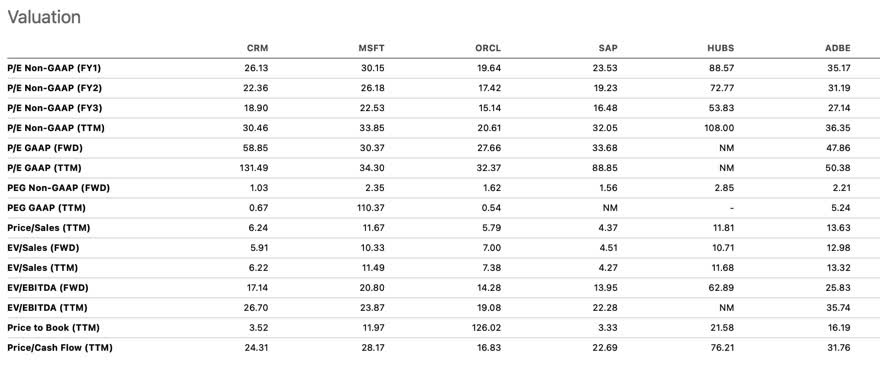

However, when comparing Salesforce’s current valuation multiples to those of its peers, there isn’t a significant difference in multiples, with only a few exceptions.

Seeking Alpha

As you can see in the table below, Salesforce competes with Microsoft’s (MSFT) Dynamics 365 CRM suite and trades at similar forward Price-to-Earnings (P/E) multiples. Compared to Oracle (ORCL), a direct competitor in CRM solutions, Salesforce trades at a noticeable premium. However, this premium diminishes significantly when looking at the 3-year P/E ratios. A similar trend is observed with SAP (SAP).

The most significant difference, where Salesforce appears undervalued, is when compared to HubSpot (HUBS) and Adobe (ADBE). While these companies may not be the primary competitors, they are notable contenders in marketing automation. In the case of Adobe Experience Cloud, which competes with Salesforce in some areas, Salesforce also appears undervalued by comparison.

Seeking Alpha

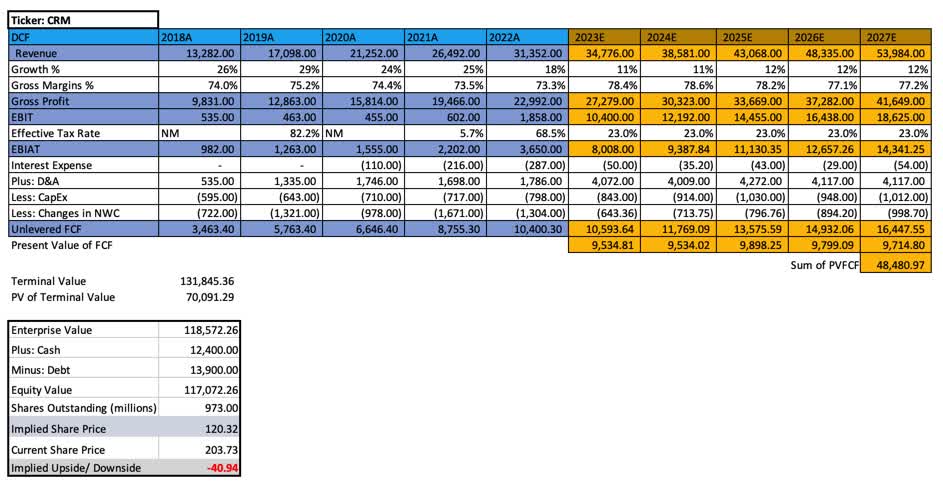

However, according to my Discounted Cash Flow (DCF) model, Salesforce trading at $203 levels until October 20 suggests it may be overvalued.

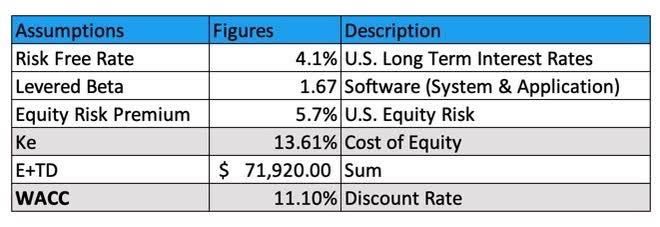

In constructing the DCF model, I employed a Weighted Average Cost of Capital (WACC) of 11.1%. This percentage was determined based on the following assumptions:

Company’s data, NYU stern, table compiled by the author

Considering the established discount rate, I utilized assumptions provided by S&P Global until 2027 across various domains. These assumptions were notably conservative. I assumed an average revenue growth rate of 11% for the next five years, during which gross margins are expected to maintain an average of 78%. Additionally, I factored from the same source the assumptions for Earnings Before Interest and Taxes (EBIT), an effective tax rate of 23% for the next five years, as well as Depreciation and Amortization (D&A) and Capital Expenditures (CapEx).

Subsequently, I made a conservative assumption of a -1.5% change in Net Working Capital (NWC), considering the average percentage of revenues over the last five years, to estimate Unlevered Free Cash Flow (FCF) figures for the next five years.

Company’s data, S&P Capital, table compiled by the author.

I calculated the Terminal Value of the Free Cash Flows (FCF) over the next five years, assuming stable growth into perpetuity at 2%, reflecting the U.S. GDP growth rate and the corresponding discount rate. This resulted in a PV of Terminal Value of $70.1 billion.

By adding the FCF’s Present Value (PV) for the next five years to the PV of the Terminal Value, we arrive at an Enterprise Value for Salesforce of $118.5 billion. Taking into account its cash position of $12.4 billion and reducing its debt position of $13.9 billion, I calculated a Total Equity Value of $117 billion. Dividing this by the 973 million outstanding shares, I arrived at an implied value of $120 per share for Salesforce. This suggests a 40% downside, which closely aligns with the gains of Salesforce’s stock year-to-date.

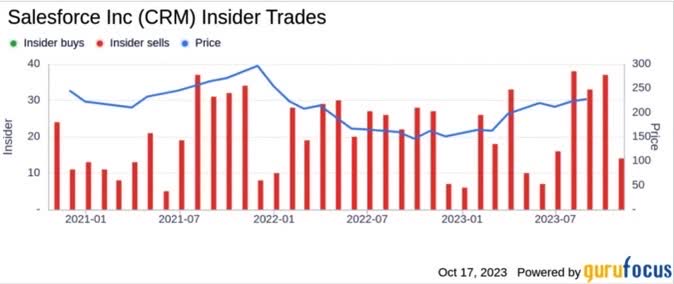

Interestingly, another indication that the company may be trading at stretched multiples is the signal from the company’s management, indicating that insiders have been selling shares in the company over the past few years, including recent transactions.

GuruFocus

The Bottom Line

Salesforce’s focus seems to be aligned with the five-point plan outlined by Marc Benioff, the CEO, a few quarters ago. The company continues to invest in Research and Development (R&D), optimize its workforce, prioritize product development, enhance relationships with shareholders, and expand its generative AI capabilities in the Data Cloud. The commitment to growth and margin expansion remains steadfast.

In my assessment, the expansion into AI is likely well reflected in the company’s valuation. According to my DCF model, approximately 40% of its value is attributed to the expected increase in future revenues driven by generative AI with Einstein 1.

For these reasons, I am currently maintaining a neutral position in Salesforce. Considering the company’s valuation for the remainder of this year, I believe there is limited room for upside considering the current momentum.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Analyst’s Disclosure: I/we have a beneficial long position in the shares of MSFT either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.