Summary:

- Microsoft posted a strong fiscal Q1 double beat, with sequential reacceleration at Azure being a key highlight.

- The results continue to support robust adoption of AI-related services at Microsoft, with prospects of further monetization over the nascent technology in FY’2H24 from 365 Copilot general availability coming up.

- Taken together with better-than-expected earnings resulting from persistent discipline in spend management, Microsoft maintains its ability to sustain margin expansion at scale, which is also value accretive.

jewhyte

In our previous coverage on Microsoft Corporation (NASDAQ:MSFT), we had discussed the prospects of Copilot as a key driver of total addressable market (“TAM”) expansion for the company’s core productivity software business, bolstering durability to its sustained path of double-digit growth at scale. Yet, the stock has declined more than 5% in value since, underperforming key market benchmarks S&P 500 (SP500) and the tech-heavy Nasdaq 100 (NDX) over the same period. This is broadly in line with the mega-cap peer group, as valuations continue to be impacted by a mixed macroeconomic outlook that has taken precedent over AI momentum in recent months.

But in the latest fiscal Q1 earnings release, Microsoft management has provided further details on the company’s pathway to monetizing Copilot with its upcoming general availability in about two weeks. This essentially improves visibility into Microsoft’s AI monetization roadmap, besting some of its enterprise AI software peers that have benefitted from a steep valuation upsurge on the nascent technology’s momentum in recent months. This is also supported by outperformance in Microsoft’s Azure unit during the fiscal first quarter, with reaccelerating growth driven by robust adoption of its AI-related services defying recent market concerns of slow than expected AI adoption risks. And this continues to reinforce our view that there is substantial pent-up value in the Microsoft stock attributable to its AI opportunities that have yet been realized.

AI has remained in focus once again for the latest earnings season, especially at Microsoft. Despite the stock’s tepid post-earnings late-trading in response to Microsoft’s fiscal Q1 outperformance, management’s optimism on a stronger second half of FY 2024 underscores continued strength in the company’s software and cloud computing moat despite intensifying competition. Incremental monetization on AI tailwinds is already evident from Azure in its provision of relevant infrastructure, while the upcoming general availability of Microsoft 365 Copilot is likely to further buoy opportunities stemming from the nascent technology’s demand. There are also emerging recovery tailwinds in the broader PC market, as well as the gradual normalization of cloud spend optimization trends, which will be beneficial to performance in Azure and Windows, especially ahead of the Windows 11 2023 update slated in Q4.

With the stock still trading below some of its AI software and mega-cap peers – especially given the recent pullback driven primarily by broader macroeconomic conditions – despite sustained double-digit growth at scale and proven capabilities in monetizing the emerging generative AI opportunities, Microsoft reinforces its prospects as a long-term winner from current levels.

AI Spotlight

Microsoft’s AI monetization efforts are becoming more pervasively felt across its broader business, kicking off fiscal 2024 to a strong start. Related growth momentum is observed across all realms of the AI value chain, spanning development, deployment and application across all of Microsoft’s core Azure cloud, productivity software, and even gaming businesses.

Azure: Specifically, Azure’s growth in FQ1 2024 underscores benefits from incremental AI infrastructure demand. The revenue stream grew 29% y/y in the fiscal first quarter, reaccelerating sequentially following several consecutive quarters of deceleration observed in the broader cloud-computing industry. Management has attributed much of the business’ outperformance during the quarter to robust adoption momentum for AI-related opportunities such as demand for Azure OpenAI Services. This continues to highlight the company’s competitive advantage in capturing the surging volume of dollars flowing into the development and deployment of AI applications amidst broader enterprise digital transformation trends since the sensational debut of OpenAI’s ChatGPT last year.

Azure OpenAI Services already support “AI-powered workloads” from more than 11,000 customers, with relevant revenue gradually representing a greater mix of total Azure and other cloud services sales generated during the fiscal first quarter. This is consistent with management’s previous expectations for at least a two-point contribution in Azure growth from the provision of AI-related services, up from the one-point contribution observed during the June quarter. Progress is also evident in the substantial outperformance of Intelligent Cloud segment revenue in the fiscal first quarter, which outperformed the upper range of the previous growth guidance by three percentage points at 19% y/y.

Based on our back of the napkin calculations, one point of growth at Azure represents about $500 million in annual recurring revenue. A recent court filing by Microsoft in relation to its proposed Activision Blizzard acquisition revealed $34 billion in fiscal 2022 Azure revenue, which translates to about $45 billion in fiscal 2023 based on the cloud unit’s blended annual growth of about 34% y/y during the period. Considering estimated growth in the minimum 20% range for Azure in fiscal 2024, one percentage point would represent about $500+ million. Thus kicking off the fiscal first quarter with a two-point contribution from Azure AI services effectively catapults the opportunity to the billion-dollar ARR club at just the early innings of AI adoption, underscoring the massive scale of Microsoft’s monetization opportunity on top of AI-related revenue from non-compute verticals.

Software: Meanwhile, continued resilience in Microsoft’s software sales amid a mixed macroeconomic outlook reinforces confidence in the upcoming general availability of Microsoft 365 Copilot. The AI-enabled software suite – which includes Microsoft Copilot UX, Bing Chat, Commercial Data Protection, Enterprise Security, Microsoft 365 Chat, and Microsoft 365 Apps – is scheduled for launch on November 1, supporting management’s optimism for a second half-weighted fiscal 2024.

Specifically, Microsoft 365 Copilot will launch at a subscription rate starting at $30 per month per user. The feature’s pricing power and adoption prospects can be validated by positive feedback from “600 paid customers through [the] early access program,” highlighting meaningful productivity gains as a key value proposition to end users.

Meanwhile, the standalone Microsoft Copilot add-on feature, which only includes Microsoft Copilot UX and Bing Chat, is offered at a monthly rate of $12.50, which is in addition to the $57 per month for existing base Microsoft 365 offerings. And with over 400 million active consumer and enterprise subscribers today in just Microsoft 365, the accompanying Copilot add-on’s robust pricing highlights the scale of Microsoft’s AI monetization opportunity ahead in just the software aspect alone, bolstering the company’s fiscal 2H growth story. As Microsoft continues to integrate AI across its portfolio of offerings – or as JPMorgan analyst Mark Murphy fittingly calls it as “remodelling every room of the house with AI” – the company is well-positioned to further scale related opportunities. This is already observed through accelerating take-rates in the high double-digit percentage range across Copilot features deployed via GitHub, Power Apps, Dynamics, sales, and security verticals.

Gaming: The biggest update on Microsoft’s gaming business is none other than the completion of its Activision Blizzard acquisition. Following almost two years of regulatory hurdles, the transaction finally got its final greenlight from the UK’s Competition and Markets Authority last week.

In addition to anticipated growth synergies stemming from the amalgamation of Microsoft’s existing Xbox device and cloud-based gaming businesses, and Activision Blizzard’s market leading games portfolio, the merger also precipitates the potential emergence of AI-driven improvements in the segment. This is consistent with Activision Blizzard CEO Bobby Kotick’s recent expectations for the company to further benefit from Microsoft’s “specialized talent in AI and machine learning,” which will bolster its competitiveness against competing rivals in the gaming industry, and unlock further growth opportunities ahead by improving gamers’ experience.

Taken together, Microsoft continues to track favorably as a key winner across the AI value chain, ranging from the provision of relevant infrastructure to facilitate the development and deployment of generative AI technologies, to the integration of relevant capabilities into applications for end-market use through its market leading productivity software suite and gaming foray.

Broader Industry Recovery Trends

In addition to AI momentum, Microsoft’s fiscal first quarter performance also underscores gradual recovery from cloud-spend optimization headwinds and the broader PC market slump on Azure and Windows demand, respectively, over the past year.

Specifically, in Azure, the segment’s reaccelerating growth during the fiscal first quarter likely reflects normalizing cloud spend optimization trends, in addition to incremental demand for AI services. This is consistent with recent industry checks that suggest an emerging slowdown in cloud spend optimization, which could be an incremental tailwind to Azure’s forward growth outlook second to the rise in AI-related opportunities. The anticipated improvements are likely to become more consistently evident heading into the second half of fiscal 2024, given the incremental benefit of an easier PY compare when the cloud-computing industry was most impacted by optimization challenges. This builds on the continued normalization of optimization trends over the past two quarters as reiterated by management and evident in Azure’s sequential reacceleration in the fiscal first quarter. With Azure being another high margin business complementary to Microsoft’s software sales, the company is likely to benefit from incremental margin expansion tailwinds ahead of moderating optimization challenges, which will be favorable to its longer-term valuation prospects.

Meanwhile, emerging PC recovery trends is also supportive of management’s optimism for a second half weighted fiscal 2024. Global PC shipments declined at a slower rate for the second consecutive quarter during calendar Q3, suggesting that the peak of the industry’s two-year slump is now behind us. Looking ahead, we see Microsoft being well positioned to take advantage of this cyclical recovery, as the timing coincides with the upcoming launch of the Windows 11 update. Specifically, the “version 23H2” – which will entail more than 150 new features, spanning AI integration in staple Microsoft apps such as Paint and Photos, Copilot voice chat, and DALL-E for Bing – is expected to become available in calendar Q4. This is likely to complement the anticipated upgrade cycle – especially in the enterprise spending segment – on PCs bought during the pandemic heading into calendar 2024.

Fundamental Considerations

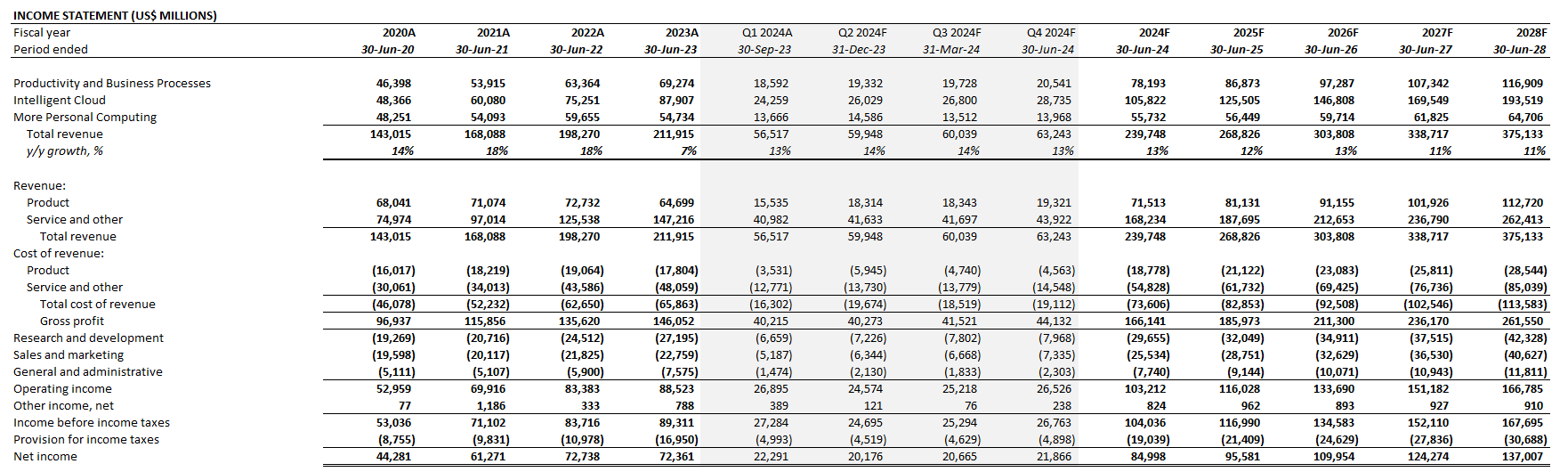

Adjusting our fundamental forecast for Microsoft’s actual fiscal Q1 performance, and also management’s optimism on the company’s forward outlook ahead of several key industry tailwinds spanning AI momentum and broader demand recovery trends in cloud and PC, we expect total revenue to maintain its restored double-digit percentage pace of growth in the teens through fiscal 2024.

Author

The Intelligent Cloud segment is expected to be the core mix contributor and growth driver alongside the Productivity and Business Processes segment, considering the continued ramp-up of AI-related sales. Meanwhile, More Personal Computing sales are expected to benefit from the emerging recovery in PC demand heading into the holiday season, supported by the anticipated start of an upgrade cycle that coincides with the upcoming deployment of the Windows 11 update in calendar Q4.

On the profitability front, management remains committed to keeping operating margin flat y/y through fiscal 2024. In addition to management’s continued caution over “increasing capital intensity,” which will be felt primarily in cost of revenue to facilitate incremental AI demand capture, Microsoft’s FY 2024 margins also faces an ongoing headwind from the change in its equipment useful life estimate. However, we remain confident in the company’s company ability to drive operating leverage and keep a cap on opex spend to compensate for the anticipated contraction in gross profit. And this is already off to a solid start, given operating expenses for the fiscal first quarter came in lower than the lower range than the previous guidance, while the company also outperformed management’s expectations, indicating increased operating leverage. This is also in line with our expectations discussed in the foregoing analysis for continued scale in high margin software and Azure revenues, helped by the ongoing ramp-up of newly introduced AI services – particularly heading into the second half of fiscal 2024. We model 9% growth in FY 2024 opex spend, relative to 10% in FY 2023, with an expectation for greater operating leverage in sales and marketing, and general and administrative expenses.

Author

Microsoft_-_Forecasted_Financial_Information.pdf.

Valuation Considerations

Currently trading at about 8x fiscal 2026 sales, and 22x fiscal 2026 earnings, Microsoft stock’s pace of multiple expansion this year continues to lag behind its mega-cap and software peers despite being the key beneficiary of impending AI tailwinds. We believe the stock’s performance at current levels continue to reflect market’s mispricing of Microsoft’s upside potential given its favorable fundamental prospects, backed by unmatched market leadership in monetizing consumer and enterprise software opportunities, durable double-digit growth sustained by its TAM-expanding AI foray, and sustained margin expansion through scale.

We are maintaining our base case price target of $347, which equally weighs the application of average mega-cap and software peer group forward sales (~9x) and (~32x) earnings multiples on Microsoft’s fundamental projections. We believe Microsoft’s sustained double-digit growth trajectory at scale, alongside consistent margin expansion warrants a higher valuation multiple from the stock’s currently traded levels on a relative basis to peers.

Author

From a sales perspective, Microsoft currently trades at about 8x fiscal 2026 revenue, which is largely in line with the broader software and mega-cap peer group averages. However, Microsoft’s impressive track record of double-digit growth and margin expansion, which has been reinforced by its proven AI monetization roadmap, warrants an incremental premium.

Meanwhile, from a profitability perspective, Microsoft currently trades at a multiple that trails the mega-cap peer group average of 32 CY/2024 and 25x CY/2025 earnings. Considering the company’s ability to keep pushing its margins higher amid a shift in revenue mix to Intelligent Cloud, boosted by incremental scale of AI-related sales, the durability to Microsoft’s profit expansion warrants an earnings multiple that is at least closer in line with the mega-cap peer group average in our opinion.

The Bottom Line

Microsoft’s solid fiscal first quarter performance continues to reinforce confidence in its software and cloud-computing moats, which have been further strengthened by the advent of generative AI adoption. While markets remain optimistic about Microsoft’s AI opportunities, we are more impressed by the improved durability to the company’s sustained trajectory to double-digit growth prospects despite its sprawling market share. Time and again, Microsoft has proven its ability to renew its forward growth trajectory and defy the law of large numbers despite risks of industry maturation, which is a rare find amongst its peers and key to bolstering the stock’s bullish thesis.

Considering Microsoft’s current market valuation continues to trail its mega-cap and AI software peers, which diverges from its proven ability to deliver on capturing emerging secular tailwinds, we believe there is further upside potential with catalysts for realization shaping up favorably heading into fiscal 2H24.

Analyst’s Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.

Thank you for reading my analysis. If you are interested in interacting with me directly in chat, more research content and tools designed for growth investing, and joining a community of like-minded investors, please take a moment to review my Marketplace service Livy Investment Research. Our service’s key offerings include:

- A subscription to our weekly tech and market news recap

- Full access to our portfolio of research coverage and complementary editing-enabled financial models

- A compilation of growth-focused industry primers and peer comps

Feel free to check it out risk-free through the two-week free trial. I hope to see you there!