Nvidia Corporation and other big tech stocks have been experiencing measured selling since mid-July, potentially due to a rapid run-up in long-duration treasury yields.

However, the selling pressure has picked up this week, with big tech earnings apparently failing to justify the Generative AI hype and a “flight-to-safety” trade into treasury bonds underway.

While leading AI stocks like Microsoft, Alphabet/Google, and Meta Platforms have struggled with monetizing Generative AI technology, Nvidia is expected to continue performing well as a picks & shovels provider.

On the back of a -20% decline, Nvidia’s long-term risk/reward looks significantly improved under our valuation model, with the stock closing in on fair value and the 5-year expected CAGR return rising to ~20%.

That said, Nvidia’s technical setup looks precarious. I continue to rate Nvidia “Hold/Neutral” in the low $400s due to multiple reasons outlined in this article. Read on to learn more.

mphillips007

Introduction: “Magnificent 7” Are Coming Back To Earth, And So Is Their Leader, Nvidia

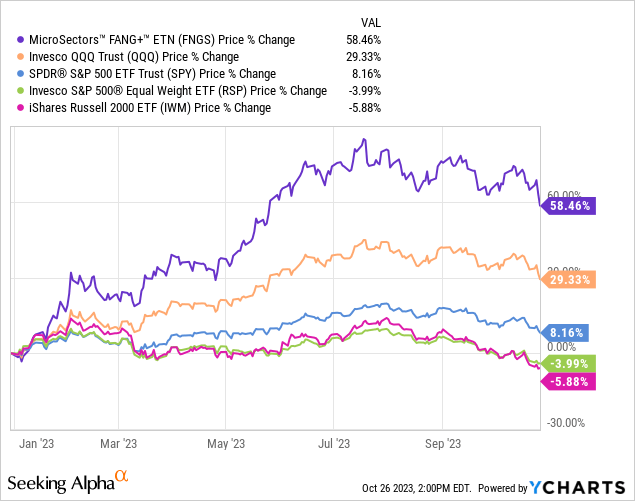

Amid a rising interest rate environment, Nvidia Corporation (NASDAQ:NVDA) and its big tech peers have served as a very profitable hiding spot for investors, in an apparent “flight-to-quality” trade. While the “Magnificent 7” stocks are still up significantly in 2023, these previously high-flying big tech stocks have been taking a hit ever since the market formed a local top in mid-July, with the selling pressure picking up over the last few sessions.

Major U.S. equity indices (SPY, QQQ) have reconnected with key technical levels such as the 200-DMA [or are close to doing so], with the rapid run-up in long-duration treasury yields finally taking some wind out of big tech sails. However, I think the stock-bond dynamic has shifted or is shifting right now, with investors finally selling stocks to buy bonds in a real “flight-to-safety” trade. The economy is potentially headed into a recessionary or stagflationary environment, and heightened geopolitical risks pose the threat of a black swan event for the markets.

In recent months, I have issued multiple warnings about unwarranted valuation premiums in the big tech arena (especially in leaders – Apple (AAPL) and Microsoft (MSFT) – negative equity risk premiums) and outlined the top-heavy nature of this market as a significant risk to major equity indices:

A big chunk of this year’s rally in tech has been attributed to breakthroughs in Generative AI (argued by bulls) or the hype around it (by bears). While we have seen tons of product announcements and releases from a variety of companies, monetization of Generative AI technology remains an unsolved mystery [outside of Nvidia, which is the “picks & shovels” provider of this AI race].

After releasing their Q3 reports earlier this week, leading AI stocks such as Microsoft, Alphabet/Google (GOOGL), and Meta Platforms (META) haven’t fared all that well, with investors seemingly dejected by a clear lack of progress on the monetization of Gen AI products and services that are eating up billions of dollars in CAPEX investment.

Now, as a “picks & shovels” provider riding the red-hot generative AI theme, Nvidia is likely to deliver another blowout quarter next month and Nvidia’s AI GPU (and now CPU) chips are projected to sell like hotcakes for the next few years [despite the U.S. banning exports of advanced AI chips to China].

If there’s any real, proven beneficiary of the generative AI trend, it is Nvidia. And yet, Nvidia’s stock has lost considerable ground in recent sessions, along with its big tech peers. From a fundamental perspective, I think Nvidia will continue to perform well in upcoming quarters since its major customers (cloud hyperscalers) remain committed to their aggressive CAPEX spending plans in the hunt for AI dominance.

In my recent article “Nvidia: The Magnificent One Delivers On Its AI Promise,” I shared the following stance on NVDA stock:

With Nvidia Corporation stock once again breaking out to new all-time highs in the after-hours session, I see no resistance for the stock, i.e., the sky is the limit for this AI leader. Investors and analysts have been chasing NVDA higher and higher in order to stake their claim in the “AI rush”, and as of now, Nvidia remains the most obvious “picks and shovels” play in the market.

WeBull Desktop

Technically, Nvidia’s stock is significantly overbought; however, we know that it can stay in overbought territory for long periods of time, and momentum can carry NVDA stock to unimaginable levels. Given Nvidia’s robust financial performance and management’s optimistic outlook, I don’t think investors (institutional or retail) are going to be in any hurry to race toward the exit doors here.

I may sound like a broken record but I will say this again –

Nvidia Corporation is a great company with market-leading products and arguably the best CEO in the semiconductor industry. However, the price we’re being asked to pay for Nvidia (~$1.2T) is too steep, in my opinion. In a zero-interest rate world, investors can afford to be valuation agnostic; however, we are no longer operating in such an environment, with the FED still pulling liquidity out of financial markets and a bank credit tightening cycle in effect after multiple bank failures.

A valuation compression still looks inevitable for Nvidia, and while the long-term risk/reward on offer is looking decent after Q2 2023, the stock offers little to no margin of safety to long-term investors.

In the case of Nvidia, the AI hype is real, and I have been wrong on the stock in the past. That said, despite running the risk of missing out on further gains in NVDA stock, I choose to remain on the sidelines in this counter. While Nvidia is delivering exceptional financial performance right now, I continue to believe that the current price tag leaves little to no margin of safety for a long-term investor. Given the lack of revenue visibility going into a potential economic recession (hard landing), I am “Neutral” on Nvidia Corporation stock at these elevated levels.

Key Takeaway: I continue to rate Nvidia Corporation stock “Avoid/Neutral/Hold” at $500.

Since then, Nvidia has dropped by nearly 20% or $100 per share, and it is now trading very close to our fair value estimate of $390 (shared in the note linked above). In light of NVDA’s price decline, Nvidia’s 5-year expected CAGR has moved up to ~20%, rendering the stock a “Buy.” However, as I shared in my previous note –

I think our updated model for Nvidia is very generous, and lofty assumptions leave little margin of safety.

Source: Nvidia: The Magnificent One Delivers On Its AI Promise.

As of today, I stand by our model assumptions, fair value estimate, and projected returns. However, given the rapid run-up in long-duration bonds and heightened geopolitical risks, I see a greater possibility of a hard landing in the economy. And in that scenario, our generous FCF margin and sales growth assumptions can prove to be too aggressive. Before updating our model again, I would like to review the Q3 earnings report (expected November 21st) and learn about the business’ trajectory from Nvidia’s management during the conference call.

So, is Nvidia a buy, sell, or hold at current levels?

From a fundamental perspective, I see no material weakness in Nvidia for the foreseeable future given the positive read-through from cloud hyperscalers (Microsoft and Alphabet), Meta Platforms, and Tesla (TSLA). The valuation is subject to debate, and I am not entirely confident in our long-term growth and margin projections due to the elevated likelihood of the economy slipping into a recession at some point within the next 12 months. Hence, I would like to rely upon technical analysis in this particular case to help us make an informed investment decision.

Nvidia’s Tryst With Troublesome Technicals

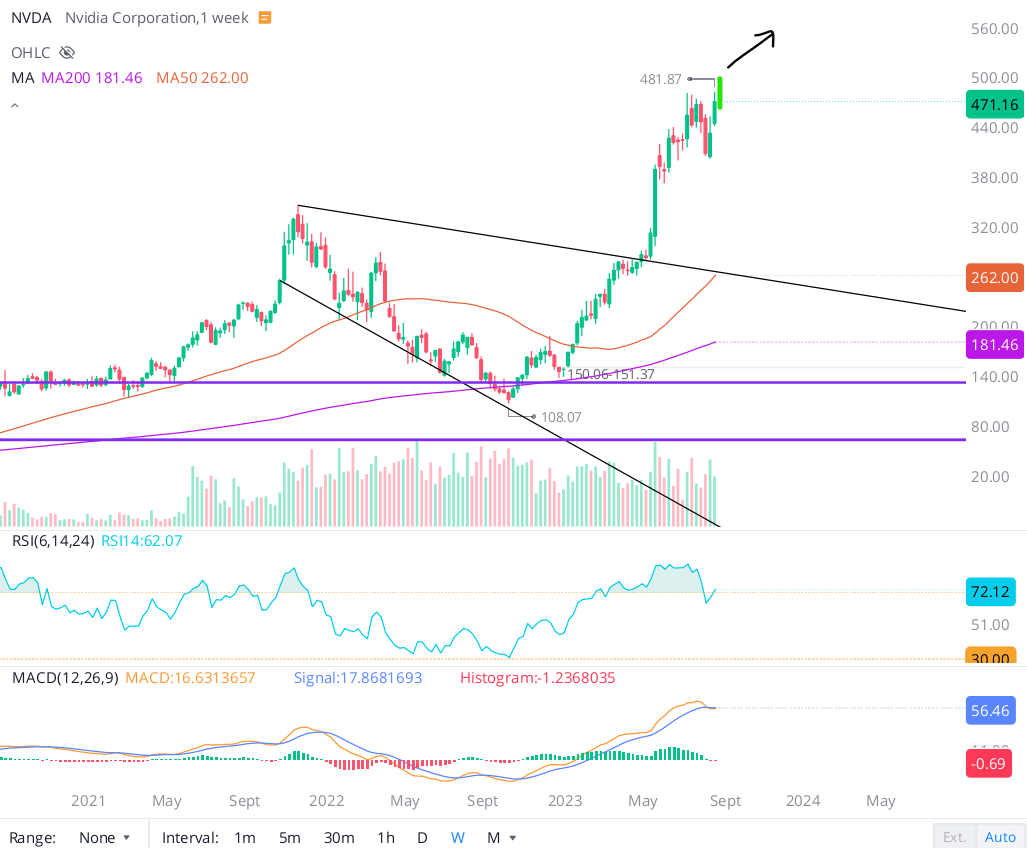

Back at $500 per share, I refused to chase NVDA stock despite mentioning that technically, the sky is the limit for Nvidia with no resistance at an all-time high. However, on the back of a ~20% decline, Nvidia Corporation stock is now in a technical correction and currently sits at a make-or-break level at ~$400 per share, with lots of air underneath this psychological level.

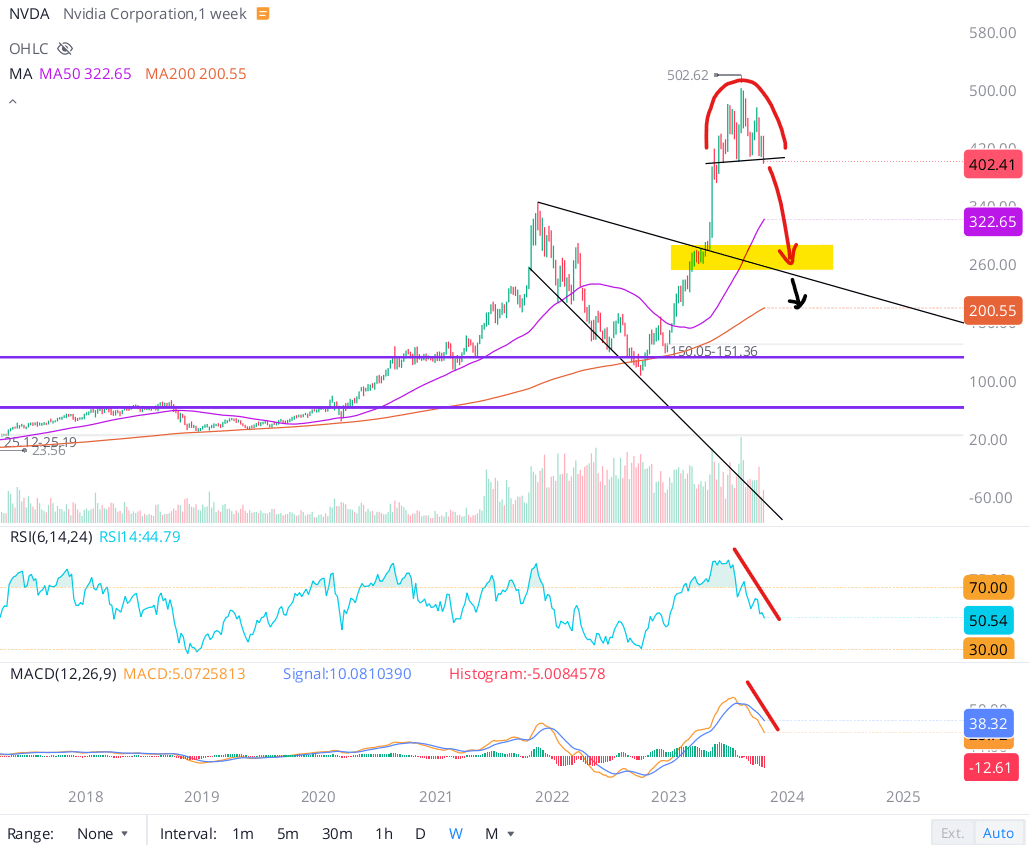

On the weekly chart, Nvidia looks to be forming a rounding top. With RSI and MACD indicators rolling over, Nvidia breaking the $400 level could trigger a sharp selloff because there’s little to no support on the chart. As you can see below, Nvidia went up from ~$250-300 to ~$400-500 in a straight line, and in technical analysis, we tend to see such vertical moves get re-traced.

WeBull Desktop

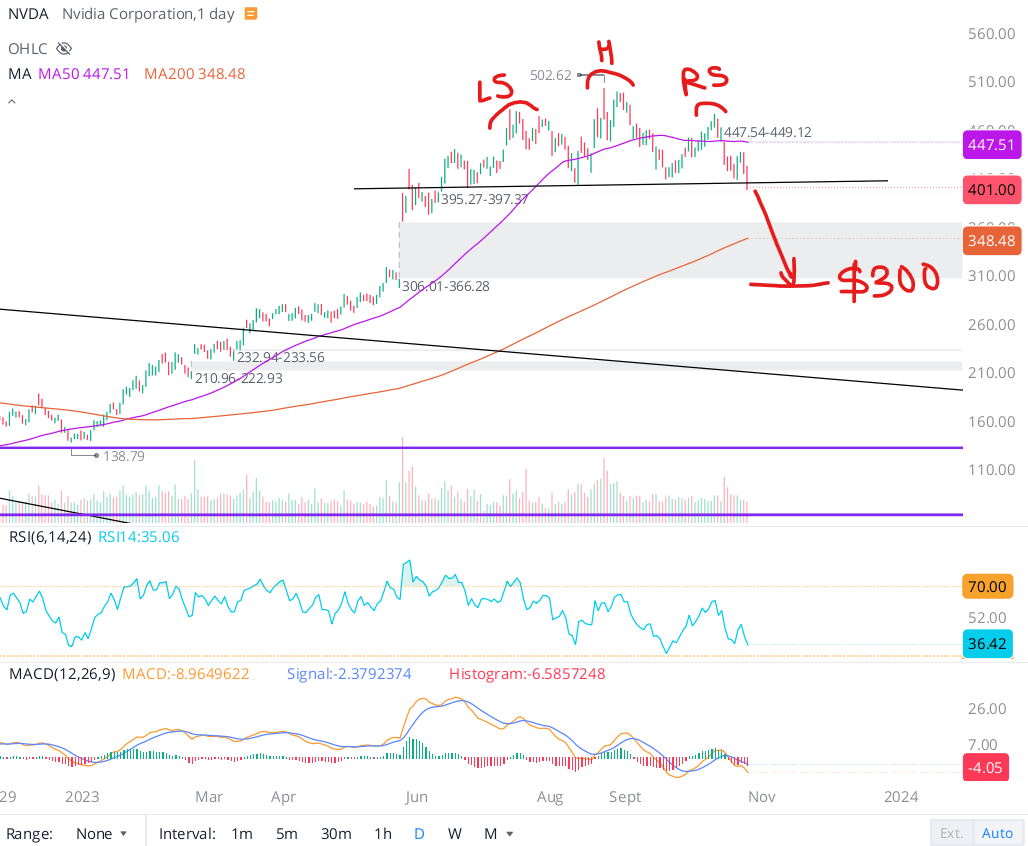

Zooming in using the daily chart, we can observe the formation of a bearish “Head And Shoulders” pattern in NVDA stock with the neckline at ~$400-410. While we haven’t broken the neckline yet, NVDA is poking under this key trendline, and a breakdown here seems inevitable given the technical breakdowns we are seeing in other big tech stocks and major equity indices.

WeBull Desktop

If NVDA stock breaks the $400 level and we see follow-through selling in the next few sessions, I would view it as a confirmation of the “H&S” pattern. A bearish “H&S” pattern that I highlighted for QQQ is already playing out, and I wouldn’t be surprised if Nvidia joined the bear parade here. While Nvidia could find some support at the 200-DMA level [$350], the measured target of the “H&S” pattern is $300, which also happens to be the technical gap fill level for Nvidia stock.

Concluding Thoughts

In light of a -20% decline since my last update on Nvidia, the long-term risk/reward for NVDA stock has improved significantly, with the stock moving closer to my fair value estimate of $390 and the 5-year expected return rising to nearly 20%. As a picks & shovels play, Nvidia should continue to benefit from the ongoing AI CAPEX spending bonanza from other big tech companies. Hence, I think Nvidia’s financial performance will continue to remain strong, at least in the near term.

That said, the wild run-up in long-duration treasury yields has increased the likelihood of a hard landing, which could negatively impact the demand for Nvidia’s AI chips. Also, the U.S. ban on the export of AI chips to China poses a fresh challenge for our long-term growth projections for Nvidia. Given our valuation model for Nvidia is quite generous, I still don’t think we have a margin of safety to deploy fresh capital into Nvidia.

Technically, Nvidia’s stock is trading at a make-or-break level. A breakdown here could send the stock into a tailspin down by ~25% to $300 per share. Despite strong beats from its big tech peers for Q3, Nvidia and the “Magnificent 7” names are experiencing increased selling pressure in recent sessions, with major market indices breaching key technical levels.

Looking at recent market action, I believe a “flight-to-safety” trade into long-duration treasury bonds [real safe haven] is seemingly underway, and a lot more money could come out of (previously high-flying) big tech stocks [perceived safe havens] in the next few weeks and months.

Given the heightened macroeconomic, geopolitical, and technical headwinds, I cannot justify buying Nvidia at current levels. If we do see a breakdown of the $400 level (confirmation of the “H&S” pattern), then I think NVDA stock will slide down to $250-350 range in a jiffy.

For bold investors willing to weather volatility, Nvidia Corporation stock could be a decent bet right here. However, considering the near-to-medium term risk/reward, I will be staying on the sidelines for now, but if NVDA gets down to $250-300, then count on me to be a buyer.

Key Takeaway: I rate Nvidia “Neutral/Hold” in the low ~$400s.

Thank you for reading, and happy investing! If you have any questions, thoughts, and/or concerns, please feel free to share them in the comments section below.

Analyst’s Disclosure:I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.

How To Invest In This Environment?

In order to navigate this tricky economic period, we are pursuing “Bold, Active Investing with Proactive Risk Management” at our investing group – “The Quantamental Investor“.

Join our community today and take control of your financial future.