Summary:

- Today’s news that Pfizer Inc.’s twice-daily oral weight loss drug will be discontinued due to safety concerns has dropped the share price to a new low.

- The company has struggled all year as its COVID franchise has disintegrated after contributing ~$100bn in revenues across 2 years.

- As Pfizer’s share price sinks in a bad year for Pharma, Eli Lilly stock has been soaring – demonstrating the value of having a horse in the GLP-1 weight loss race.

- Pfizer and its CEO believed it could grab a $10bn share of the $90bn GLP-1 market, but that looks to be in serious doubt after today’s Phase 2 data readout.

- Nevertheless, Pfizer is rebuilding, and investors prepared to ride out the lows may ultimately be rewarded. A Dividend yielding >5% is another positive.

choi dongsu

Investment Overview – Pfizer’s Reward For COVID Heroics – A ~50% Share Price Haircut

2023 has been a difficult year for the “Big Pharma” industry, and no company has felt the heat worse than Pfizer Inc. (NYSE:PFE), the New York-based company that became a household name (if it was not already) after developing, in partnership with Germany-based BioNTech (BNTX), the most widely used vaccine of the COVID era – Comirnaty.

In early 2022, Pfizer stock traded at its all-time high share price of ~$55, in large part thanks to a $37bn revenue contribution from Comirnaty in 2021, and a forecast for $32bn of revenues from the same source in 2022, plus $22bn of revenues from Paxlovid, the COVID antiviral, investors may have been forgiven for believing more upside was the natural outcome. After all, the Pharma doubled its earnings in 2021, posting $81.2bn, and forecast for ~$100bn of revenues in 2022.

Pfizer did not disappoint – achieving $100.3bn of revenues in 2022, making it the world’s largest pharmaceutical company by revenue. By the time the company came to report 2000 earnings, however, at the end of January this year, its stock price had slipped to ~$44 per share. How could a sector leading $100bn of revenues, up nearly 25% year-on-year, and up ~140% compared to 2021, possibly result in a 20% share price haircut?

The answer is that the market quickly concluded Pfizer’s COVID revenues were not sustainable and began to sell off the stock – which has now reached a new low of $29 per share – down nearly 50% from its Jan ’22 high. How can a revenue injection of ~$100bn from COVID vaccine and antiviral drugs – a high-margin business, it should also be pointed out – possibly cause the share price to decline?

In December 2020, Pfizer reported a cash position of $12.24bn, and total current assets of $35bn. In December 2022, that had risen to $44bn, with $74bn of current assets. Again, it is worth asking the question – how can this possibly be bad for business?

Short-Term Pain Versus Long-Term Gain – How Eli Lilly Showed Pfizer The Way Forward

While Pfizer’s share price has fallen steadily throughout 2022 and 2023, the share price of Eli Lilly and Company (LLY), a company that posted $28bn of revenues in 2022, and $6.3bn of net income, versus Pfizer’s $100bn revenues, and $31.4bn of net income, kept growing.

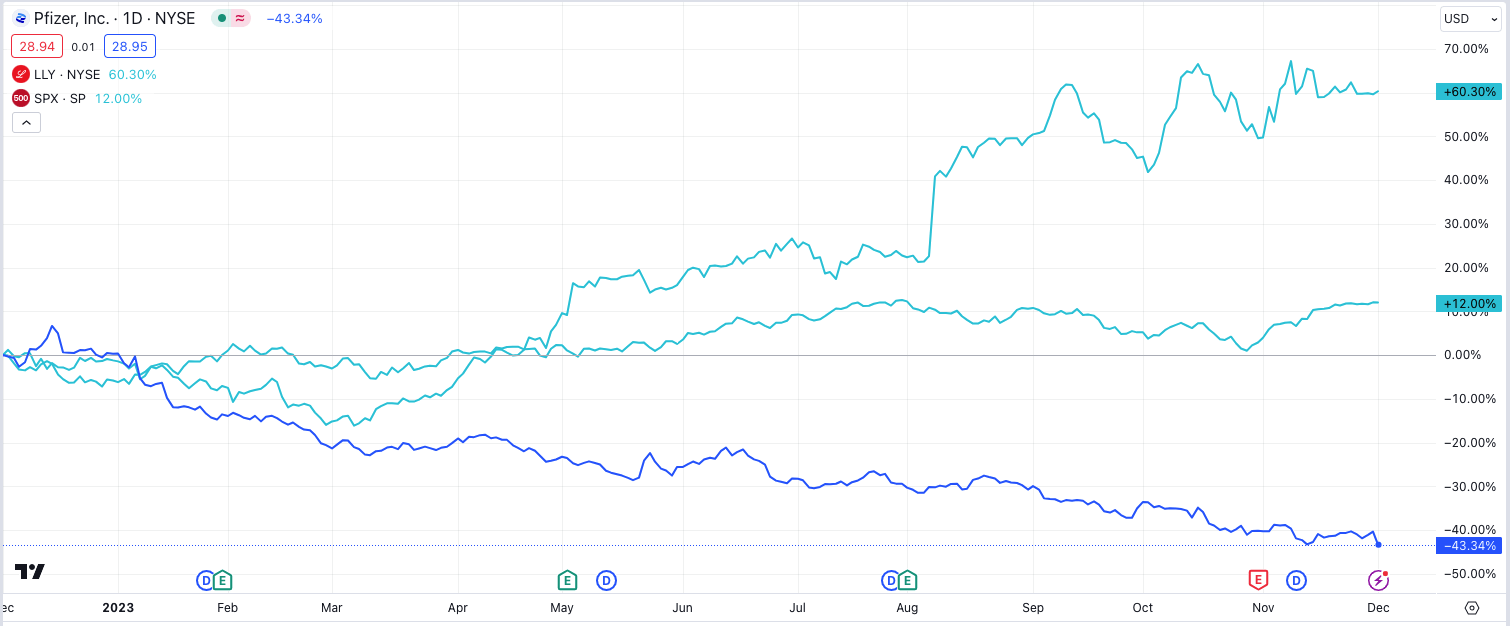

Pfizer vs Eli Lilly – 1 year share price performance (TradingView)

As we can see above, Lilly’s share price is up >60% across the past 12 months, whilst Pfizer’s is down >43%. The S&P 500 index (SP500) is +12%. Lilly’s market cap of $564bn (at the time of writing) is 3.5x higher than Pfizer’s.

This incredible truth may all come down to a single drug – Lilly’s tirzepatide. According to drugbank.com:

Tirzepatide is a novel dual glucose-dependent insulinotropic polypeptide (GIP) and glucagon-like peptide-1 (GLP-1) receptor agonist. Dual GIP/GLP-1 agonists gained increasing attention as new therapeutic agents for glycemic and weight control as they demonstrated better glucose control and weight loss compared to selective GLP-1 receptor agonists in preclinical and clinical trials

Tirzepatide has secured approvals to treat patients with Type 2 Diabetes (“T2D”), under the brand name Mounjaro, and to treat patients with obesity, under the brand name Zepbound. The best-known GLP-1 receptor agonist that tirzpetaide compares favorably against is Novo Nordisk’s (NVO) semaglutide, which is also approved in T2D and obesity, under the brand names Ozempic, and Wegovy.

In 2020, 2021, and 2022, Ozempic earned revenues of ~$3bn, $4.8bn, and $8.5bn, and across the first nine months of 2023, $9.5bn. Wegovy earned $3.1bn across the equivalent period in 2023. Mounjaro, which was only approved in May last year, earned $569m of revenues in Q1 this year, $980m in Q2, and $1.4bn in Q3.

Analysts have speculated that the global market for GLP-1 products will reach >$70bn by 2032, and that may even be a conservative estimate given that there are ~35m people with Type 2 diabetes in the U.S. alone, while ~42% of the U.S. is classified as obese, and ~9% as severely obese. The list price of Zepbound is ~$1060 for a 1-month supply, ~20% lower than Wegovy. Do the math, and $1060 x 12 months, x 9% of 330m U.S. population equates to a market opportunity – in severely obese people in the U.S. alone – of >$350bn.

Unlike COVID, T2D and obesity are not short-term markets. Therefore, while Pfizer has announced substantial downgrades to its Paxlovid and Comirnaty revenues in 2023, taking a non-cash charge of $5.5bn in Q3 to write off unused inventory, Eli Lilly is looking forward to generating revenues potentially comparable to Comirnaty plus Paxlovid for years, if not decades to come.

Framed in this way, it is not quite so hard to understand why Eli Lilly’s share price is rampant, while Pfizer’s is in retreat.

If You Can’t Beat Them Join Them? Pfizer’s Plan For Twice-Daily GLP-1 Scuppered – Faint Hopes For Once-Daily Progression

Under its CEO Albert Bourla, Pfizer cannot be accused of lacking the ability to innovate, and Pfizer has been developing its own GLP-1 agonist, which is known as Danuglipron. A major advantage of Danuglipron is that it can be taken orally, whereas semaglutide and tirzepatide are self-injectable therapies.

In fact, back in January, at the JP Morgan Healthcare conference, CEO Bourla confidently predicted that Danuglipron “could be $10 billion product for us in a market that could be $90 billion,” adding:

we think there will be very few players that will play in the oral GLP-1, us and Lilly, clearly, we are going to be one of them. We think the data should show which one has a better profile. We believe and we hope that we will have. But no matter what, it’s going to be so big a market that it’s going to be a very big product for both of us, I think.

Clearly, the market does not share Bourla’s enthusiasm, and the fact that Pfizer ditched an experimental, once-daily obesity pill, lotiglipron, in late June, over concerns around liver damage, arguably justified the lack of enthusiasm. Shortly after its announcement, Lilly released data showing its own oral weight loss pill, orforglipron, had achieved 14.7% weight loss in patients at 36 weeks, with an acceptable safety profile.

Nevertheless, Pfizer had been persevering with twice daily administered danuglipron, and released its latest data set from a Phase 2 clinical study in ~600 obese adults without T2D earlier today. First, the good news – the study met its primary endpoint, demonstrating a statistically significant change in body weight from baseline. According to the press release:

Twice-daily dosing of danuglipron showed statistically significant reductions from baseline in body weight for all doses, with mean reductions ranging from -6.9% to -11.7%, compared to +1.4% for placebo at 32 weeks, and -4.8% to -9.4%, compared to +0.17% for placebo at 26 weeks. Placebo-adjusted reductions in mean body weight ranged from -8% to -13% at 32 weeks and -5% to -9.5% at 26 weeks.

Now for the bad news: the safety profile of the drug was poor – quoting from the press release again:

While the most common adverse events were mild and gastrointestinal in nature consistent with the mechanism, high rates were observed (up to 73% nausea; up to 47% vomiting; up to 25% diarrhea). High discontinuation rates, greater than 50%, were seen across all doses compared to approximately 40% with placebo.

In summary, it looks very much like the end of the road for twice-daily danuglipron, and investors are once again dumping Pfizer stock, which has now slipped into the $20s, down >4% so far in trading today. All may not be quite lost, however, as Mikael Dolsten, MD., PhD., Chief Scientific Officer & President, Pfizer Research and Development commented:

We believe an improved once-daily formulation of danuglipron could play an important role in the obesity treatment paradigm, and we will focus our efforts on gathering the data to understand its potential profile. Results from ongoing and future studies of the once-daily danuglipron modified release formulation will inform a potential path forward with an aim to improve the tolerability profile and optimize both study design and execution.

Pfizer’s Dismal 2023 Ending On Yet Another Bum Note – Is There Hope For 2024?

It has undoubtedly been a horrid year for Pfizer and its shareholders, as the company has lost more value than any other Pharma. And yet, in September, in a note for Seeking Alpha, I suggested this could be the best time to buy Pfizer stock in a decade (which was the last time the share price sank this low). Is this the case after the Pharma’s latest setback?

Clearly, the market has not reacted well to the downgraded FY23 guidance, the write-downs, and plans to shed $3.5bn worth of jobs and expenses as a result of the rapidly shrinking COVID franchise. Q4 earnings and guidance for FY24 are unlikely to set investors’ pulse racing, as it will likely confirm that a once-hotly anticipated market for private COVID vaccinations has fallen flat, and it should not be forgotten that Pfizer is carrying some $31bn of current liabilities, and $62bn of long term debt, for total liabilities of ~$118bn.

With all that said, however, as I wrote in September, ever since spinning out its legacy brands division – the likes of Viagra, Lipitor, and Lyrica – into a new company, Viatris, in 2020, the company has been in a rebuilding phase. As I wrote in September:

Using its COVID vaccine and antiviral cash windfall, since 2021 Pfizer has been on a major M&A spending spree.

Since mid-2021 Pfizer has completed: a $2.3bn deal for Trillium Therapeutics and its 2 CD-47 targeting blood cancer drug candidates; a $7bn deal for Arena Pharmaceuticals and its late stage autoimmune candidate Etrasimod; an $11.6bn deal for Biohaven and its lead candidate Nurtec, indicated for migraine treatment; a $5.4bn deal for Global Blood Therapeutics and its ~$200m per annum commercial stage drug Oxbryta, indicated for Sickle Cell Disease (“SCD”), and lead candidate GBT601, which may offer a functional (permanent) cure for SCD; a $525m deal for Reviral and its antiviral therapeutics targeting respiratory syncytial virus (“RSV”), and a a $43bn deal for Seagen – the antibody drug conjugate (“ADC”) specialist with 4 approved drugs which drove ~$2bn of revenues last year.

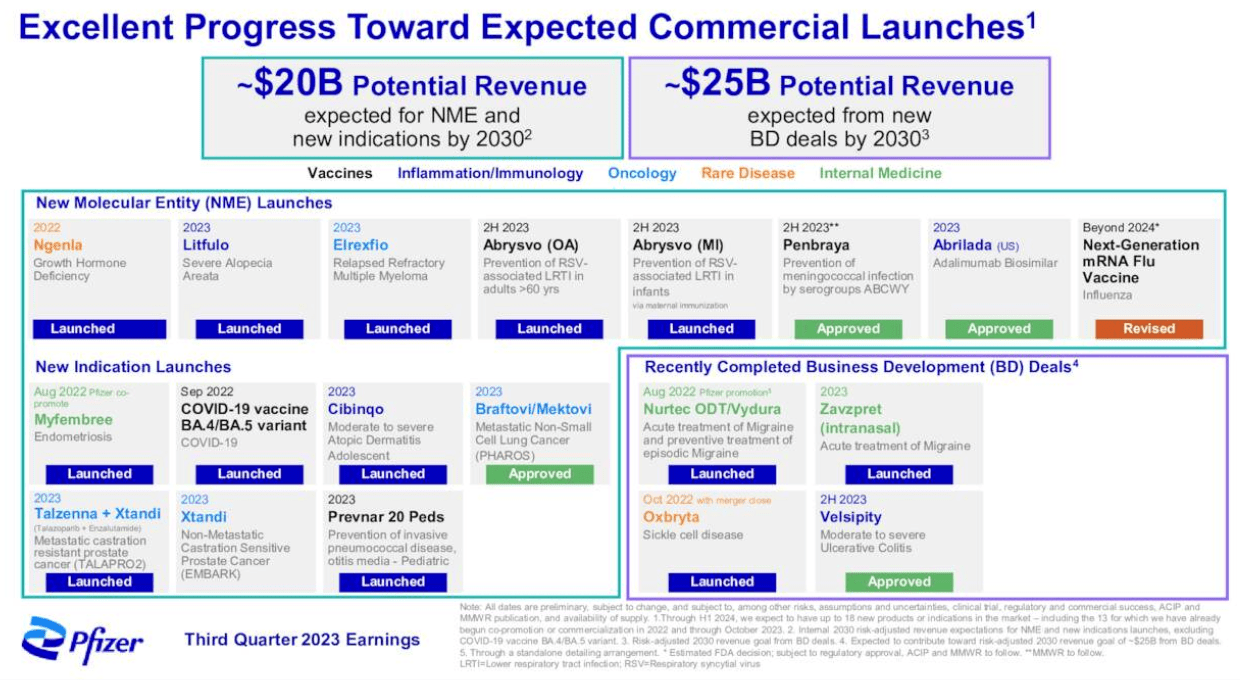

Pfizer ex-COVID expansion plans (Pfizer Q3 earnings presentation)

As we can see above in a slide from Pfizer’s Q3 earnings, the company believes its M&A spree, plus its internal pipeline, can generate some $45bn of new product revenues by the end of the decade. Revenue guidance for FY23 may have been downgraded to $58bn – $61bn, with adjusted EPS $1.45 – $1.65, but management is looking upwards, even while it deals with the COVID revenue crash, and it has some genuine firepower in that arsenal of newly acquired, and newly launched drugs.

While Eli Lilly grabs the plaudits for its mold-breaking weight loss drugs and appears to have the Midas touch when it comes to drug development, it’s important to remember that Pfizer brought us Comirnaty within 9 months of the pandemic being declared, and Paxlovid when COVID antiviral therapeutics were dangerously scarce.

It may, therefore, be wrong to believe that Pfizer has lost its knack for innovation overnight. With amongst the lowest forward price-to-sales and price-to-earnings ratios in the Big Pharma sector, and with a dividend yielding 5.4%, compared to Eli Lilly’s 0.8%, there may be no harm in holding Pfizer Inc. stock long-term, even if the company has made itself a laughingstock in 2023 so far.

Analyst’s Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.

Gain access to all of the market research and financial analytics used in the preparation of this article plus exclusive content and pharma, healthcare and biotech investment recommendations and research / analytics by subscribing to my channel, Haggerston BioHealth.