Summary:

- Cisco is losing market share to Arista in the networking end-market, with Arista achieving double-digit growth compared to Cisco’s low-single-digit growth.

- Cisco’s end-to-end security business is outdated and lagging behind competitors like Palo Alto, who offer more comprehensive and cloud-focused security solutions.

- Cisco’s acquisition of Splunk may not have significant synergies, as Splunk’s business model differs from Cisco’s hardware-centric model.

Sundry Photography

Cisco (CSCO) has exhibited a modest 3.1% average revenue growth and 4.8% average adjusted operating profit growth over the past five years. The company is experiencing a decline in market share within both the networking and security end markets. Consequently, I recommend initiating coverage with a ‘Sell’ rating and assigning a fair value of $45.

Networking is Losing to Arista

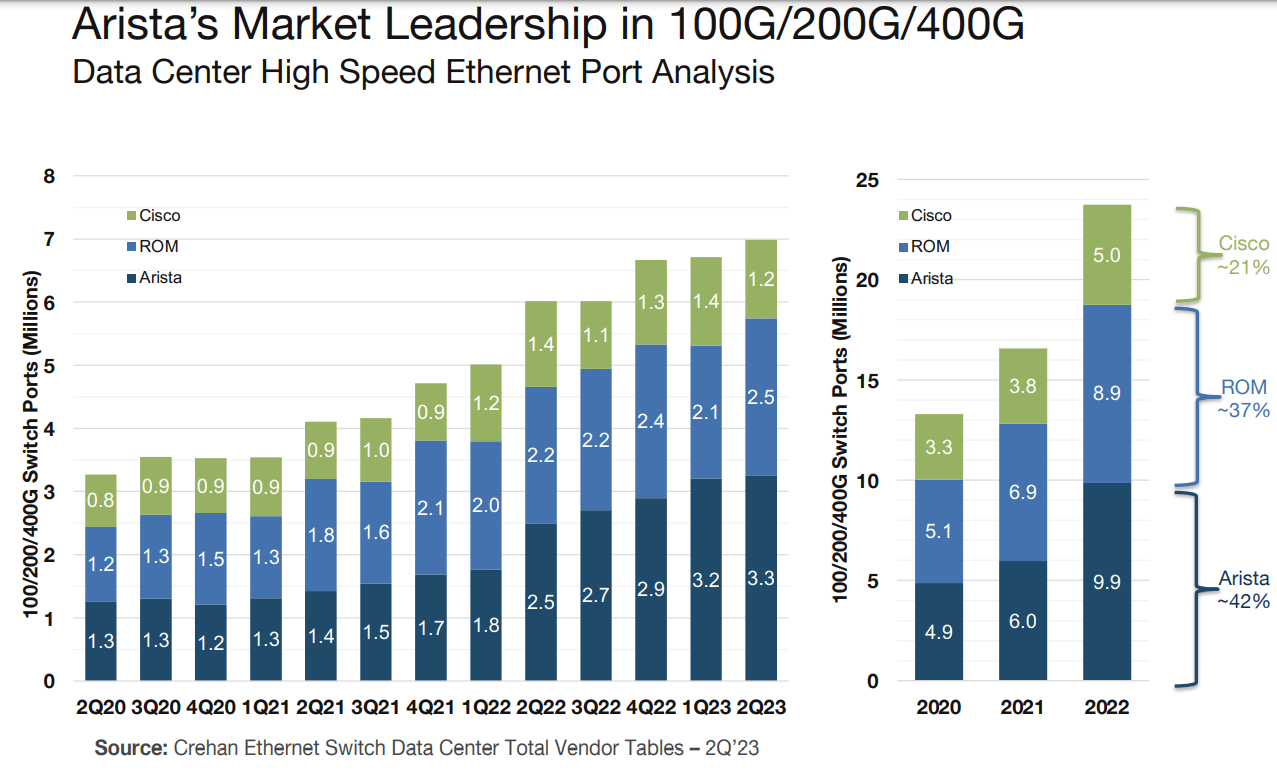

It is evident that Cisco is ceding market share to Arista, with Cisco experiencing low-single-digit growth, whereas Arista (ANET) has achieved double-digit growth over the past few years. The accompanying chart underscores this trend, revealing that Cisco added only 1 million 100/200/400G switch ports compared to Arista’s notable 2 million during the same period.

Arista Investor Deck

The decline in Cisco’s market share can be attributed to several factors. Firstly, a decade ago, as enterprises began migrating their workflows to the cloud, Cisco did not promptly adjust its product strategy to align with the demands of the cloud transition era. Instead, the company maintained its focus on traditional on-premise routers and switching technology, neglecting significant investments in software-defined networking (SDN). SDN-powered switches offer greater suitability for cloud deployment, providing enhanced flexibility and scalability capabilities.

Secondly, a decade ago, Cisco held a dominant position, with traditional networking products generating substantial cash flow and profits. The challenge arose when it became difficult for the company to disrupt its own success and reallocate resources to embrace newly developed technologies.

Lastly, in 2013, Cisco introduced ACI, its premier software-defined networking (SDN) solution for data centers, utilizing the Nexus 9000 series products as spine and leaf switches. While Cisco endeavors to catch up with rivals in providing data center solutions, the company finds itself arriving late to the game. Moreover, Cisco’s historical premium pricing is losing favor among enterprises as more budget-friendly options emerge.

Outdated Network Security

Cisco’s End-to-End Security business encompasses Cloud and Application Security, Industrial Security, Network Security, and User and Device Security. A decade ago, Cisco’s security business thrived as a bundled offering with their networking devices, providing a comprehensive solution for network integration. However, in the current era of cloud computing, their End-to-End Security has become outdated, lagging behind competitors such as Palo Alto (PANW).

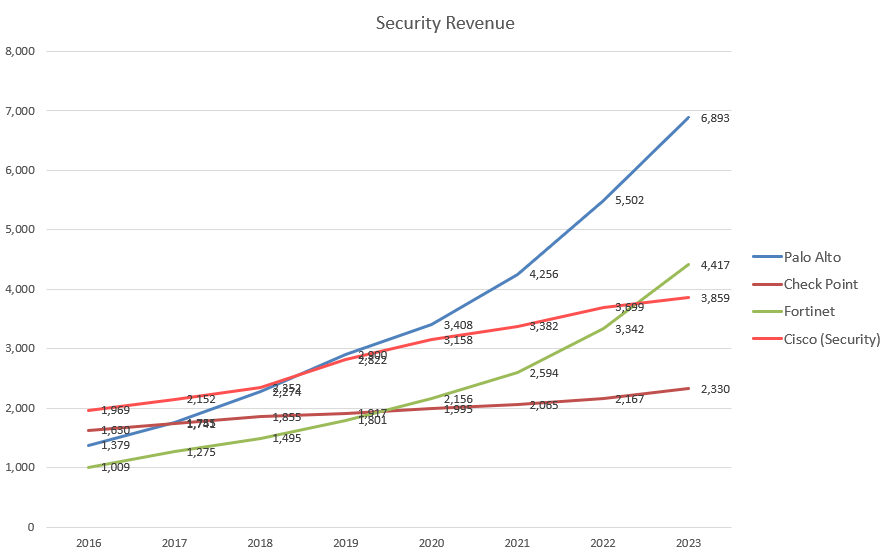

In FY23, Cisco’s End-to-End Security revenue only experienced a modest growth of 4.3%. It appears that their security products remain hardware-centric, a characteristic ill-suited to the evolving demands of cloud security and comprehensive protection. In contrast, rivals like Palo Alto employ a modular approach, offering multiple modules or subscriptions to counter various internet threats. The accompanying chart illustrates the revenue trends among major cybersecurity companies, highlighting Palo Alto and Fortinet’s (FTNT) significant market share gains in recent years. Their success can be attributed to software and module-centric products that align more effectively with the requirements of cloud infrastructure.

Palo Alto, Check Point, Fortinet, Cisco 10Ks

For readers seeking a deeper understanding, I recommend referring to my introductory article on Palo Alto Networks.

Splunk Acquisition

Cisco is strategically leveraging M&A to transition a significant portion of their business towards software and services. Noteworthy acquisitions include Splunk, acquired for $28 billion in 2023, IMImobile for $730 million in 2021, ThousandEyes for $1 billion in 2020, and Duo Security for $2.3 billion in 2018.

While the Splunk deal has the potential to enhance Cisco’s capabilities in security and observability, it appears that there are limited synergies between Splunk and Cisco. The primary driver behind Cisco’s decision to acquire at such a high cost is their struggle with topline growth. Cisco is paying a premium of approximately 30% over Splunk’s market price before the deal was announced, with the acquisition price implying over 7x forward revenue.

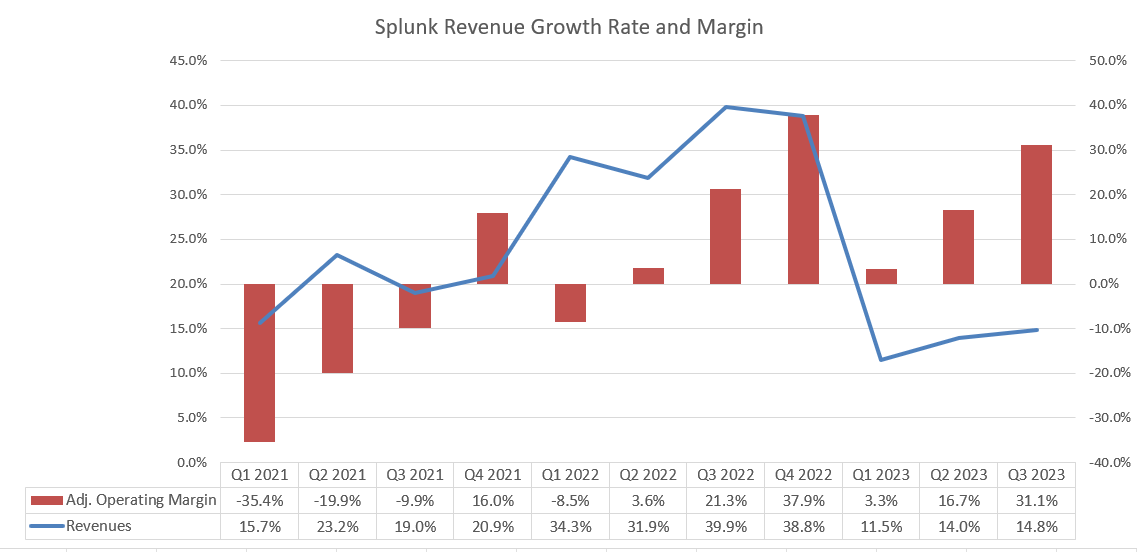

The accompanying chart illustrates Splunk’s revenue growth and adjusted operating margin trend, which is currently standing at around the low-to-mid teens.

Splunk Quarterly Results

Splunk specializes in security data analytics, operating a platform that collects extensive datasets from various sources. However, according to Palo Alto’s management, Splunk’s solutions may present challenges in promptly investigating cybersecurity incidents. Palo Alto’s Security Operations Center (SOC), on the other hand, can seamlessly integrate AI into SOC transformation and automation processes, allowing for faster and more efficient investigation of cyber threats.

It’s worth noting that Splunk is actively investing in AI and automation technologies, and its vast datasets remain a key advantage in the cybersecurity space.

In addition, Splunk is endeavoring to expand its presence in the infrastructure observability market. However, as a relatively smaller player in this space, it faces competition from established companies such as Datadog (DDOG) and Dynatrace (DT). It appears that Splunk, entering the field later, may struggle to compete effectively against these specialized players.

According to Datadog’s management, Splunk’s platform is centralized in security management, presenting a notable difference from Datadog’s infrastructure, which operates in real-time. For a more in-depth exploration of observability, I recommend referring to my introductory article on Datadog.

In summary, the potential for synergies between Cisco and Splunk is questionable. This uncertainty arises from the fundamental differences in Splunk’s business model, centered around subscription-based solutions, and Cisco’s traditional hardware-centric business model.

Isovalent Deal

Cisco announced its acquisition of Isovalent in December. Cisco had previously participated in the startup’s Series A funding at the end of 2020. Isovalent, a cloud-native security and networking startup, is expected to enhance Cisco’s security capabilities for cloud infrastructure.

Isovalent leverages eBPF and Cilium to gather data sets from both Linux and Windows, integrating with various platforms and applications such as Splunk, Datadog, and Isovalent itself. I believe the acquisition of Isovalent will benefit Splunk’s ecosystem. It’s important to note that Isovalent, while a small company, faces competition from several alternatives in the market.

Financial Results and Outlook

During Q1 FY24, Cisco achieved a robust 7.6% revenue growth and an impressive 27.6% growth in adjusted net income, reaching the upper end of their guidance range.

Cisco Quarterly Results

Their balance sheet remains strong with $23.5 billion in cash and cash equivalents. Operating activities generated $2.4 billion in cash, and they returned $2.8 billion to shareholders through dividends and share repurchases.

For FY24, revenue guidance is set to be between $53.8 billion and $55 billion, with Non-GAAP earnings per share ranging from $3.87 to $3.93. The guidance suggests one or two quarters of low revenue growth followed by a return to normal growth. The subdued growth in the upcoming quarters is attributed to implementation constraints, with large customers working through elevated product shipments from previous quarters. Essentially, Cisco over-earned in the prior fiscal year. The current full-year guidance implies an approximately -5% revenue growth rate, a reasonable expectation given the over-earning in the preceding fiscal year.

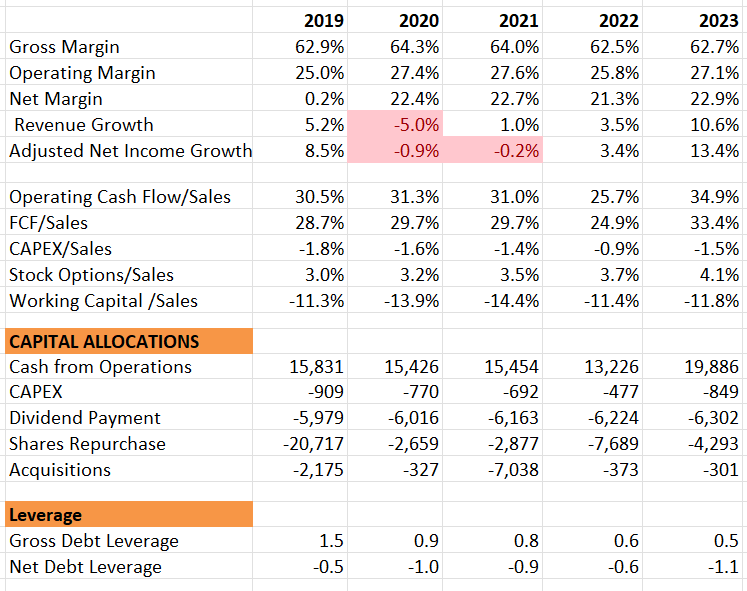

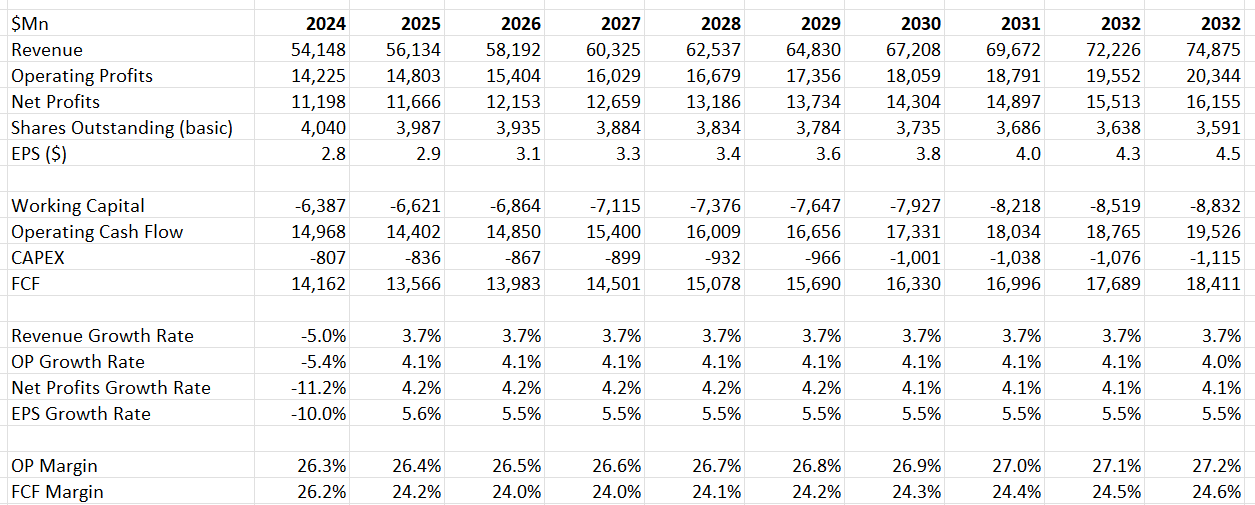

The table below provides an overview of Cisco’s historical financials. In summary, they have demonstrated a low growth rate in both topline and bottom-line figures, with an average of 3.1% revenue growth and 4.8% net income growth. Their balance sheet remains robust with a net positive cash position, and their dividend payout and share buyback activities are deemed decent.

Cisco 10Ks

Valuation

The revenue growth assumption for FY24 takes into account the near-term headwinds stemming from elevated inventory shipped to their large customers, aligning with their provided guidance. When projecting normalized revenue growth, the model assumes 3% for organic revenue growth and 0.7% for acquisition growth, consistent with their historical average.

Given the sluggish top-line growth, the likelihood of generating significant operating leverage is low. The estimate suggests only a 10 basis points leverage annually.

Cisco DCF – Author’s Calculations

The model employs a 10% discount rate, assumes a 3% terminal growth rate, and considers a 19% tax rate. Based on these parameters, the calculated fair value is $45 per share.

Key Risks

Weak Growth in Q2 and Q3 FY24: As discussed in their Q1 FY24 earnings call, the management anticipates a challenging Q2 and Q3, attributing it to the elevated inventory shipped to their large customers. I believe the subdued growth in the upcoming quarters is temporary, and their growth rate should resume once these customers have successfully digested their inventories.

Collaboration Business Decline: The collaboration business, contributing over 7% to Cisco’s total revenue, faced a decline of 9.4% in FY23 and 5.4% in FY22. Cisco encompasses Meetings, Collaboration Devices, and Contact Center businesses within this segment. The significant rise of Zoom (ZM) has introduced considerable downside risk for Cisco’s collaboration business, and I anticipate ongoing pressure on this business segment in the future.

Conclusion

In light of the challenges Cisco is facing in the cloud transition era and the perceived erosion of their competitive advantages, particularly in the realm of on-premise networking, I am initiating a ‘Sell’ rating. I assign a fair value of $45.

Analyst’s Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.