Summary:

- Coca-Cola is one of the leading beverage companies and has been a paragon of innovation in the soft drink industry for many decades.

- Currently, Coca-Cola’s dividend yield is 3.1%, outperforming its major competitors in the consumer packaged goods (CPG) sector.

- Coca-Cola has a broad geographic presence and a portfolio of recognizable brands, which provides risk diversification and strengthens its position in global markets.

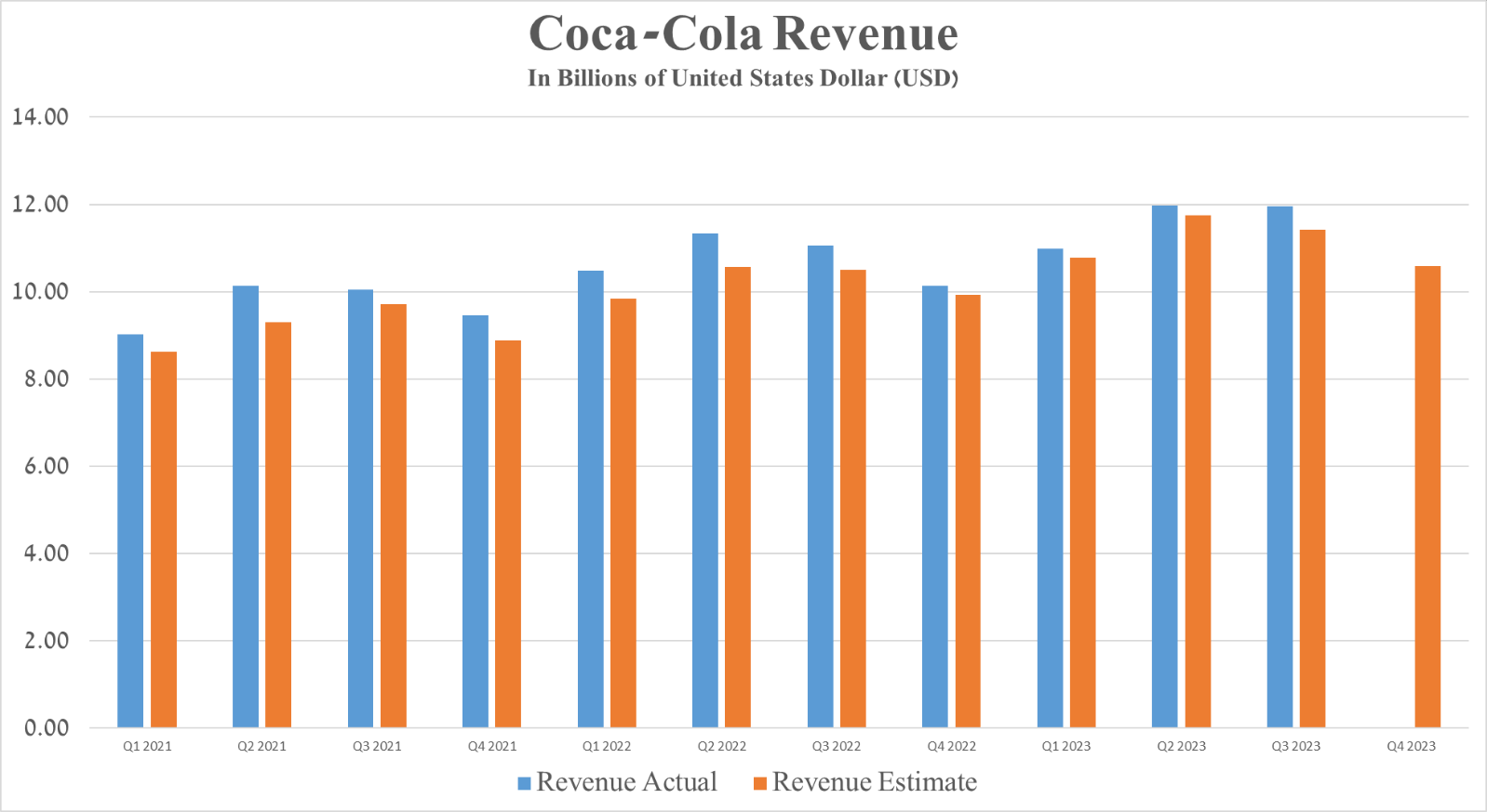

- Coca-Cola’s revenue was about $11.95 billion for the third quarter of 2023, up 8% from the third quarter of 2022 and also beating analysts’ expectations by $580 million.

- Due to the risks that were described in the article and the expected continuation of the technical correction in the price of its shares, I believe that the price level at which the risk/reward profile will be attractive to conservative investors is $55.9-$56.1 per share.

Editor’s note: Seeking Alpha is proud to welcome ALLKA Research as a new contributor. It’s easy to become a Seeking Alpha contributor and earn money for your best investment ideas. Active contributors also get free access to SA Premium. Click here to find out more »

smirart

Coca-Cola (NYSE:KO) is one of the leading beverage companies and has been a paragon of innovation in the soft drink industry for many decades.

Thesis

This article will present an analysis of the company’s financial results in recent quarters, an outlook on its business growth in 2024, and the key factors that make Coca-Cola one of the most attractive assets among other companies in the consumer staples sector.

These factors include, among others, the growth of dividend payments over the past 61 years, extremely high return on equity, Coca-Cola’s year-on-year decline in debt, an extensive portfolio of well-known brands, and declining consumer inflation in the US and Europe.

However, in light of the growing trend of healthy eating, the increasing popularity of anti-obesity drugs worldwide, and considering the expected technical correction, I am starting Coca-Cola coverage with a “hold” rating.

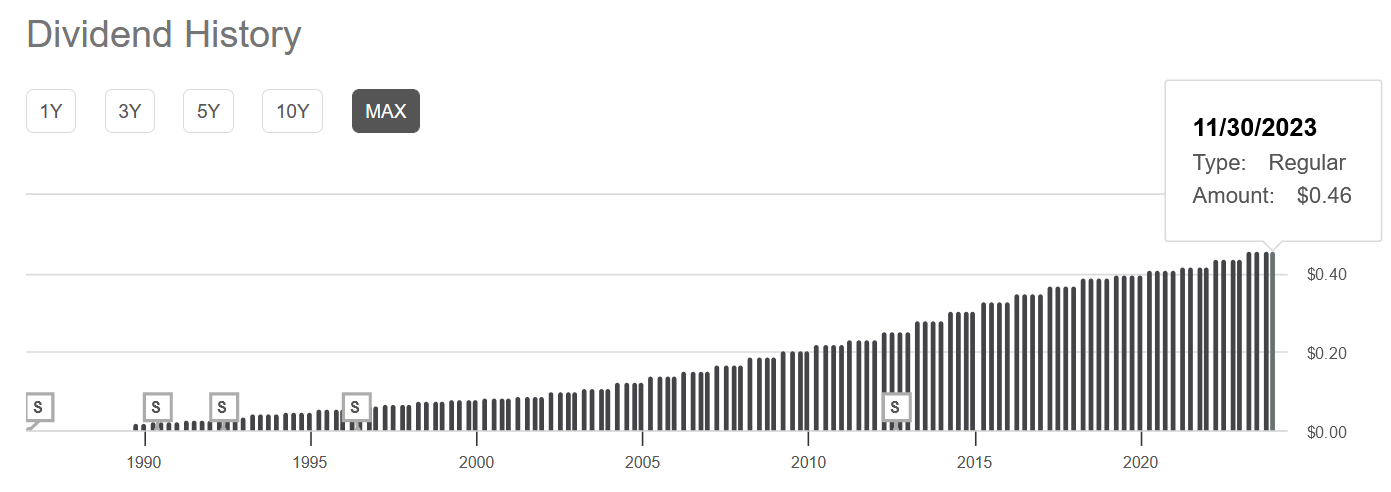

Coca-Cola is the longest-tenured Dividend King

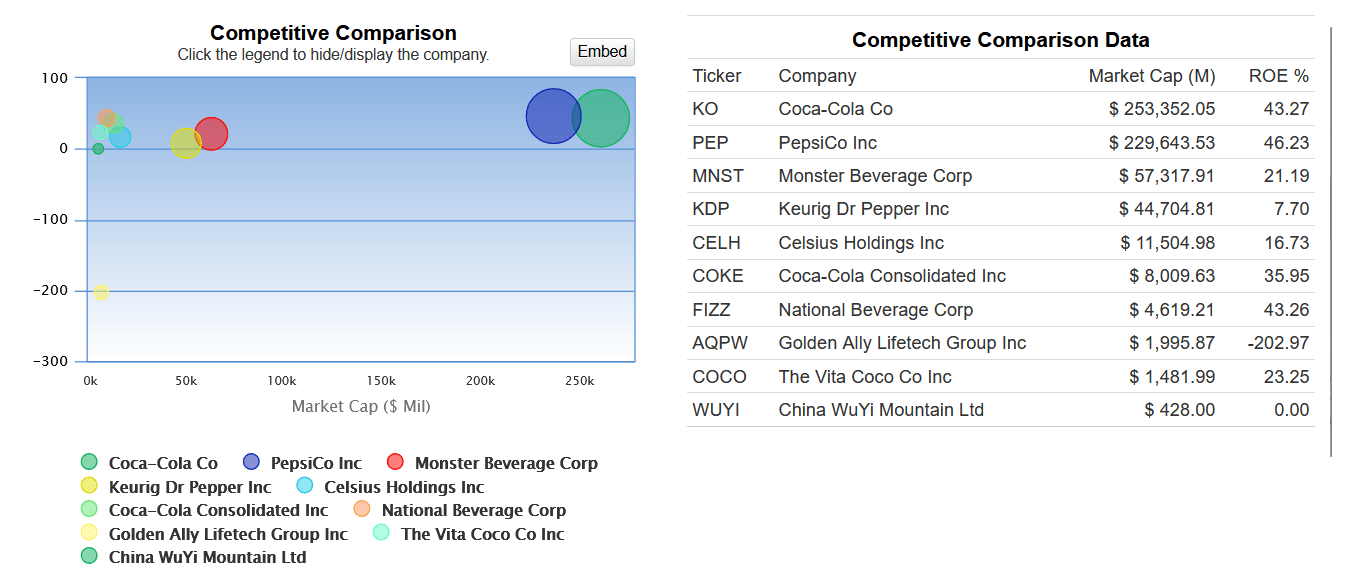

Coca-Cola, a prominent blue-chip stock, holds a coveted spot in the exclusive S&P 500 Dividend Aristocrats index thanks to its management consistently raising dividend payouts for the past 61 years. Currently, Coca-Cola’s dividend yield is 3.1%, outperforming its major competitors in the consumer packaged goods (CPG) sector, including PepsiCo, Monster Beverage, and Keurig Dr Pepper.

Source: Seeking Alpha

Considering the quarterly dividend is equal to $0.46 per share, by the end of 2023, Coca-Cola will spend more than $7.9 billion for these purposes, which is 4 times more than it plans to invest in capital expenditures (CapEx). According to GuruFocus, the company has a return on equity (ROE) of around 43%, which not only indicates its strong balance sheet but also exceeds that of many of its competitors in the soft drinks market.

Source: GuruFocus

As a result, this underlines Coca-Cola’s financial strength and attractiveness to long-term investors, who are focused on stable dividend income and reliable investments.

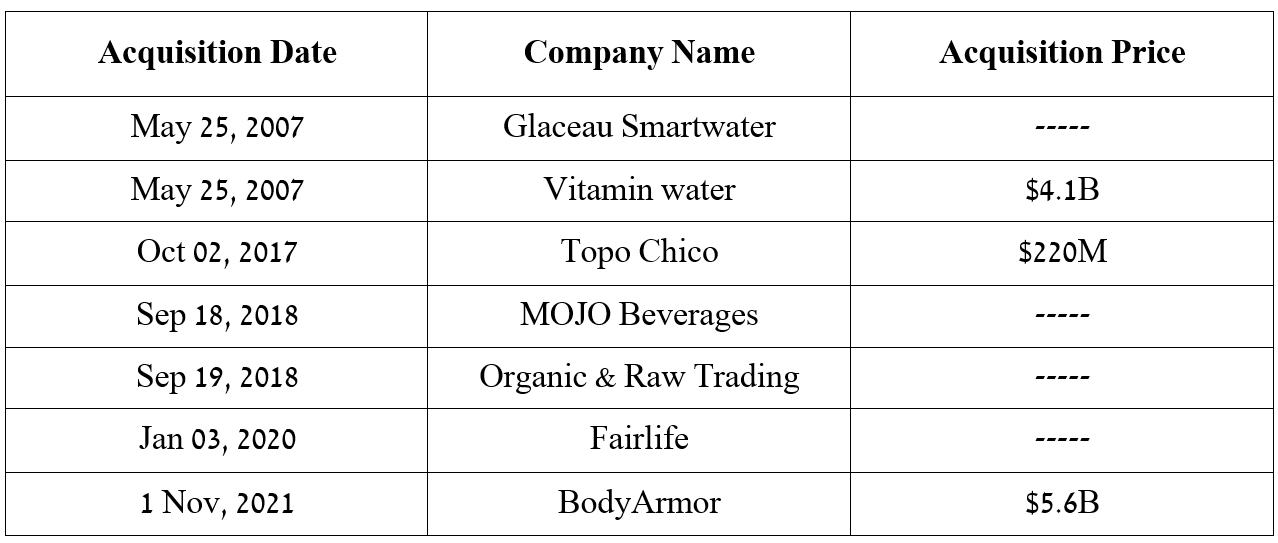

M&A transactions of Coca-Cola

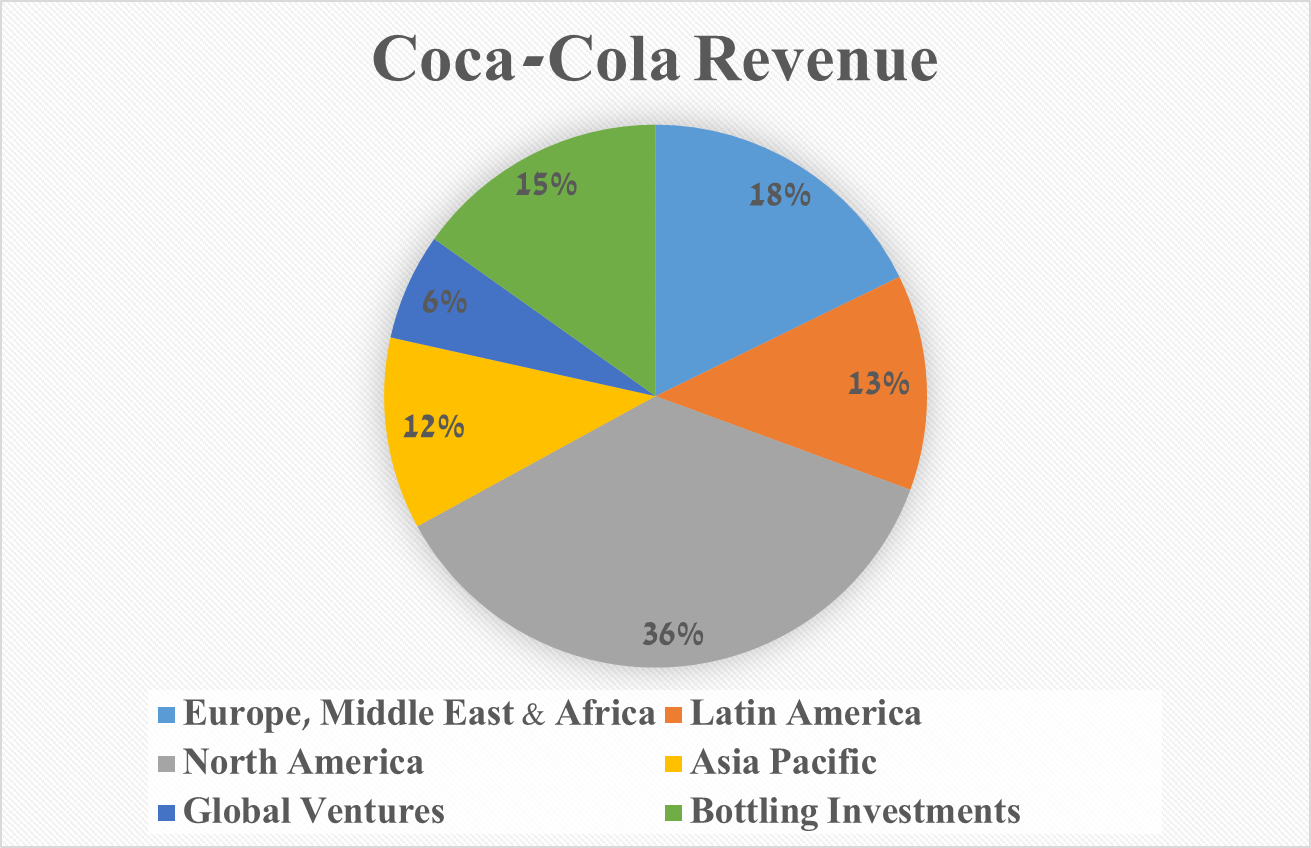

Coca-Cola has a broad geographic presence and a portfolio of recognizable brands, which provides risk diversification and strengthens its position in global markets. Partnerships with leading alcoholic and non-alcoholic brands and the commercialization of new products contribute to the growth of Coca-Cola’s brand value, which is $106.1 billion in 2023.

Due to stable cash flow and the need to diversify and expand its business and strengthen its position in the global carbonated beverage market, Coca-Cola is conducting M&A transactions and also entering into partnership agreements. The table below highlights some of the company’s largest and most recent acquisitions.

Source: Coca-Cola press releases

One of the latest deals was the news that one of the leading beverage alcohol companies, Constellation Brands, entered into a brand authorization agreement with Coca-Cola on January 6, 2022. According to the terms, the company will distribute ready-to-drink alcohol-based cocktails called FRESCA Mixed in the United States. I believe that this deal will allow Coca-Cola to enter the low-alcohol beverages market, estimated at $8 billion, with projected growth of 15-17% per annum.

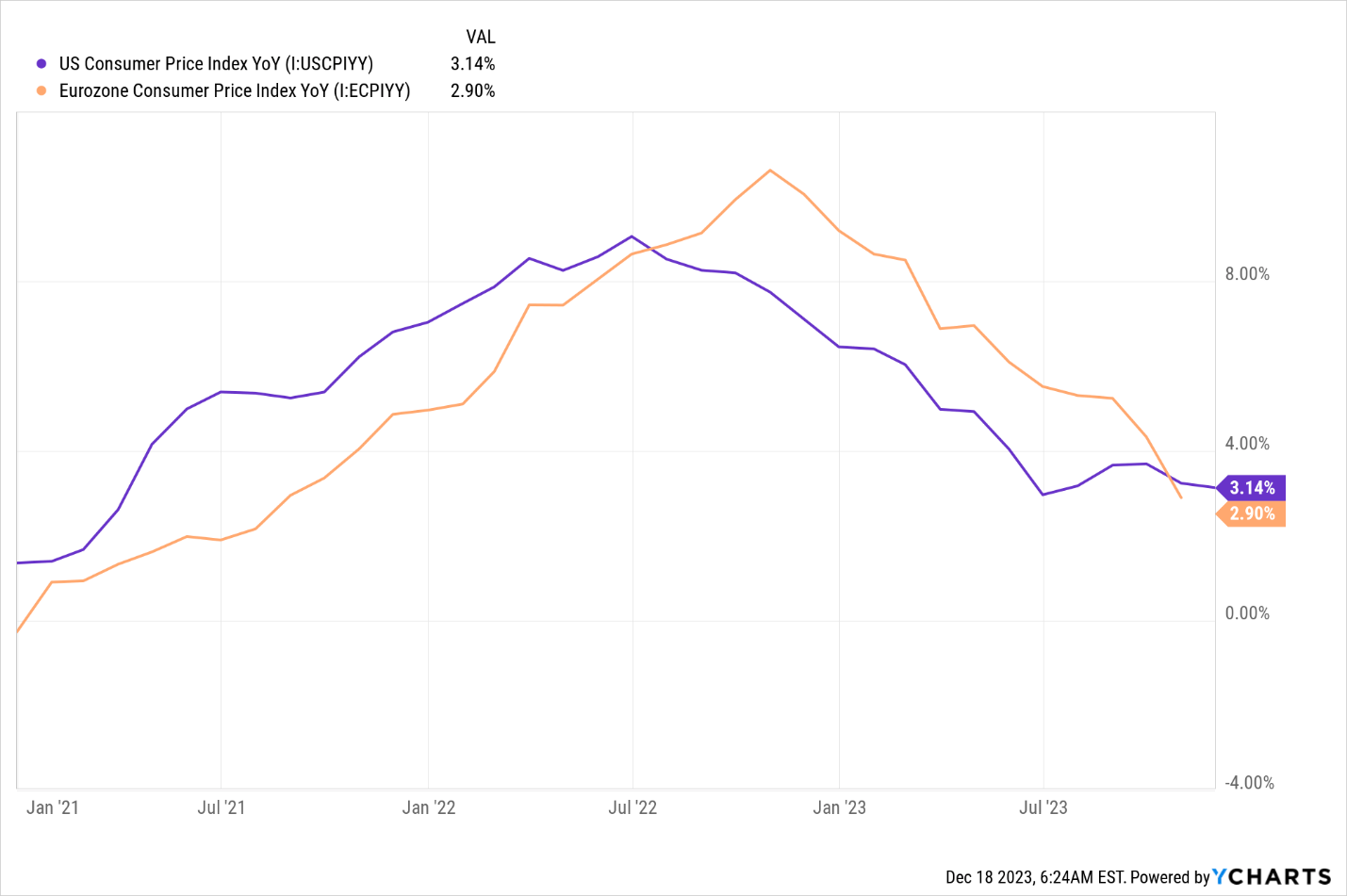

Positive signals for the economies of the USA and the European Union

Thanks to the effective policies of central banks, there has been a decline in inflation in the United States and the European Union in recent months.

Source: YCharts

As a result, this will help reduce pressure on consumers’ wallets, which will positively impact Coca-Cola’s financial results in 2024. In addition, published forecasts in the Summary of Economic Projections indicate that there will be at least three interest rate cuts in 2024, potentially leading to higher consumer spending and higher sales of the company’s products.

Source: Federal Reserve Board

A brief description of the reasons why I am initiating to cover Coca-Cola with a “hold” rating

On the other hand, the growing trend in healthy eating and an increasing number of people buying anti-obesity medications Ozempic and Zepbound may slow down the growth rate of demand for soft drinks. What’s more, currency fluctuations and the strengthening of the dollar could also have a negative impact on Coca-Cola’s margins, given that its product sales outside the US account for more than 60%. Also, given the technical analysis that will be presented later in the article, I believe that the price level at which the risk/reward profile will be attractive to conservative investors is $55.9-$56.2 per share.

Coca-Cola’s financial results and outlook

Coca-Cola’s revenue was about $11.95 billion for the third quarter of 2023, up 8% from the third quarter of 2022 and also beating analysts’ expectations by $580 million.

Source: Seeking Alpha

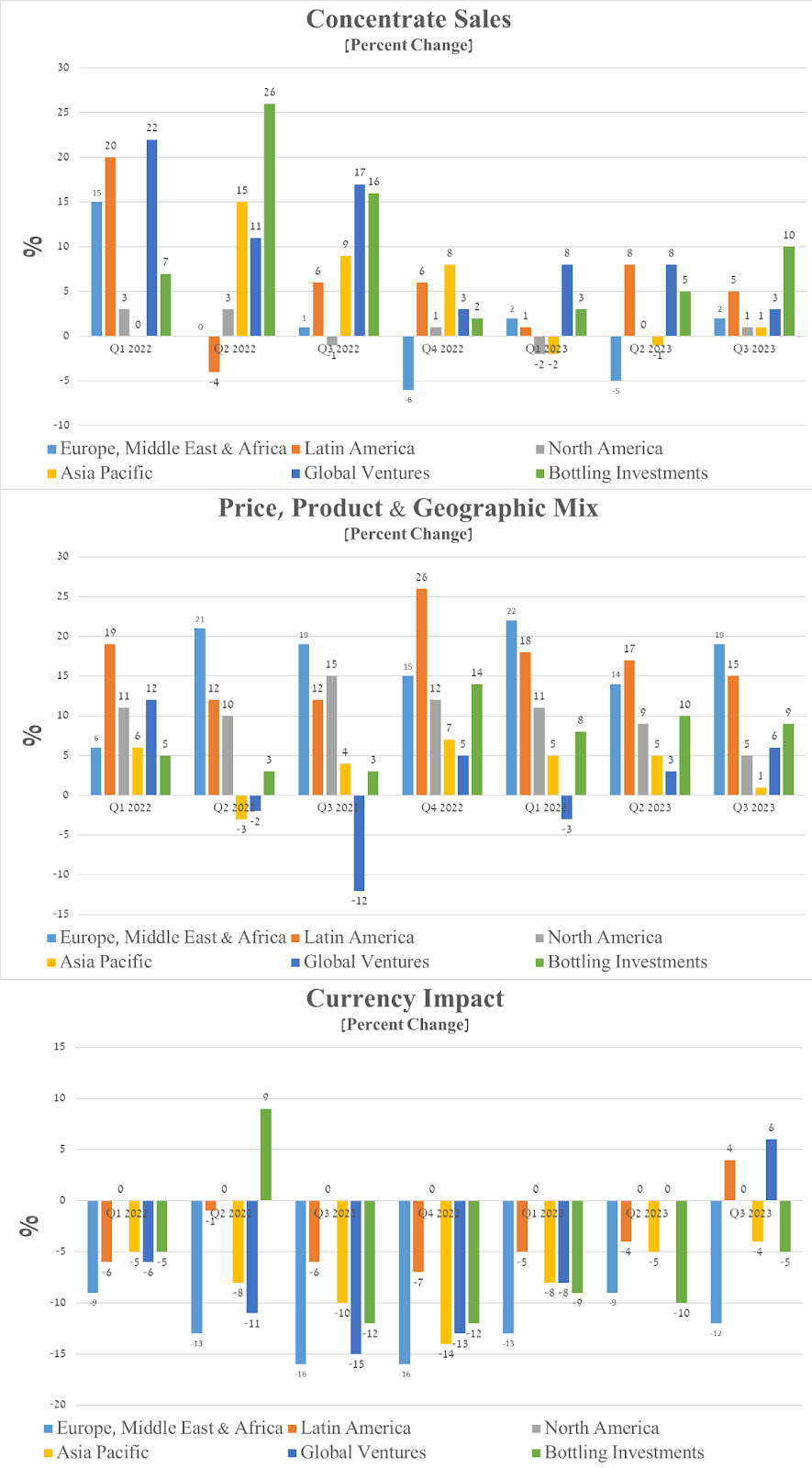

The growth of this financial metric was caused by an increase in packaging volumes, an increase in price/mix by 9% and also an increase in concentrate sales by 2%, even despite the closure of business in Russia. These factors partially mitigated the negative impact of the stronger US dollar compared to certain foreign currencies.

Source: 10-Qs

More importantly, the company’s effective strategies and leadership position in the global carbonated beverage market have enabled it to show growth in each of its operating segments. So, sales in the Latin America segment amounted to about $1.57 billion for the 3rd quarter of 2023, an increase of 24.2% compared to the third quarter of 2022, thanks to increased demand for soft drinks, coffee, tea, and juice in Brazil and Mexico.

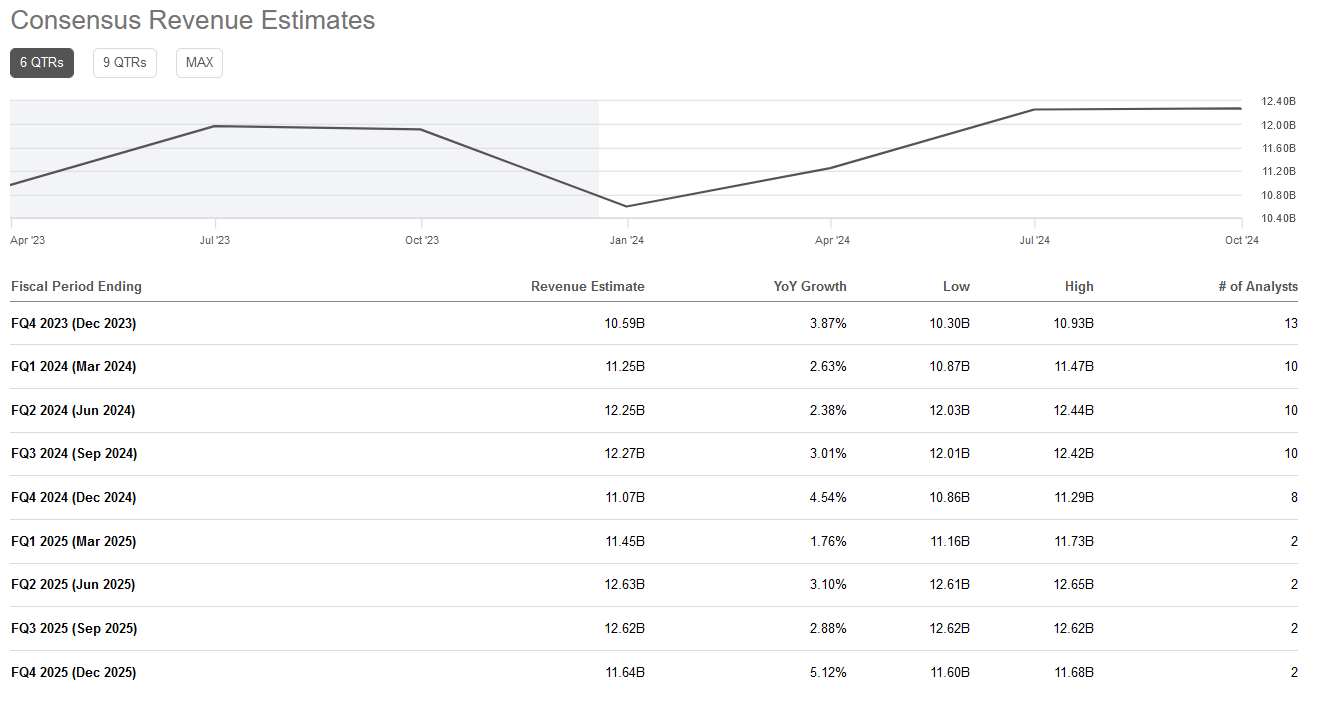

The Seeking Alpha platform offers data on Wall Street analysts’ expectations for the coming quarters. So, Coca-Cola’s revenue for the fourth quarter of 2023 is expected to be $10.3-$10.93 billion, which is 3.9% more than in the previous year. Moreover, it will continue to grow in subsequent years, including due to the expansion of its product portfolio and also rising prices for soft drinks.

Source: Seeking Alpha

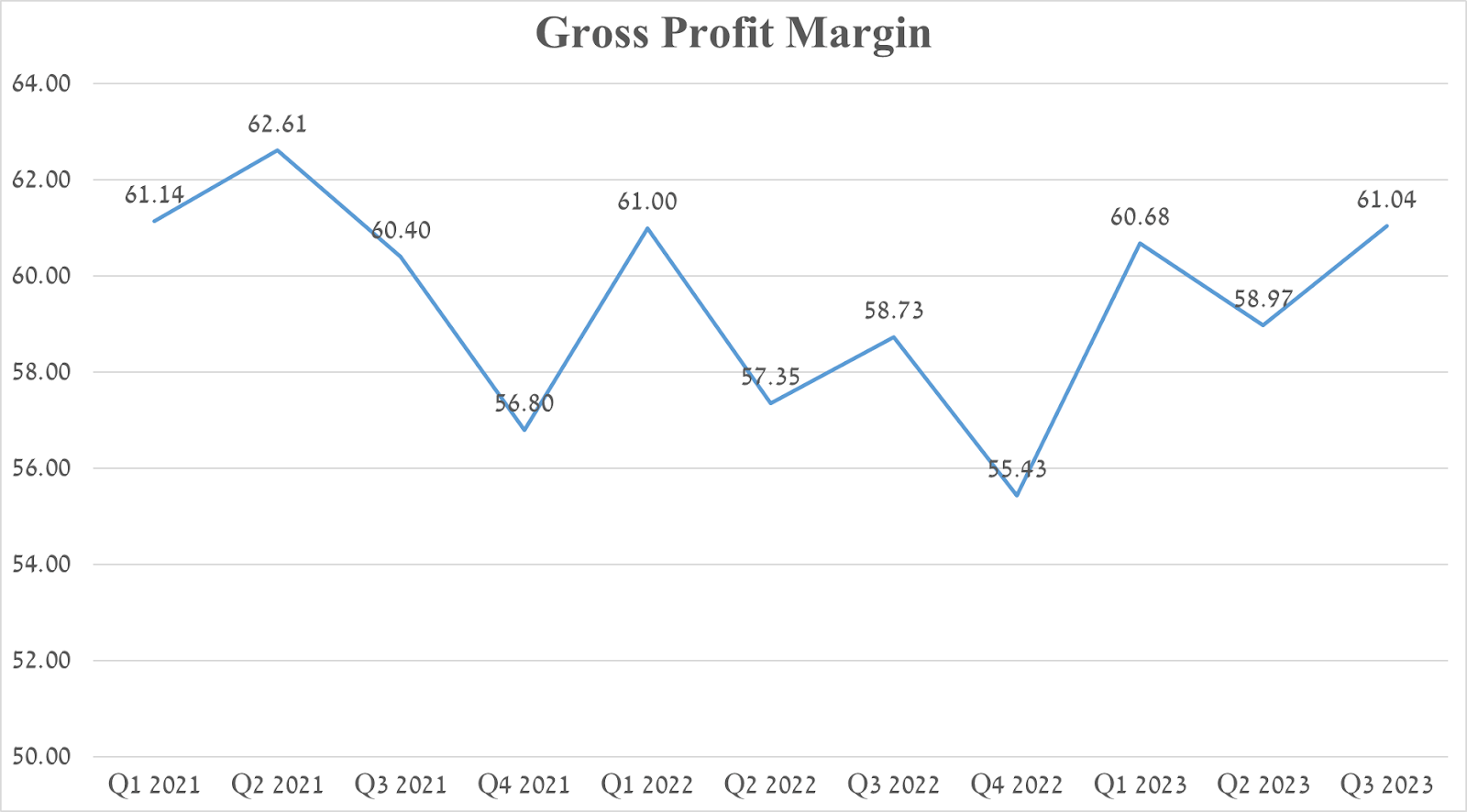

Coca-Cola’s gross margin was about 61% for the three months ended September 29, 2023, which is higher than in previous quarters, even despite elevated sugar prices and weakening exchange rates of emerging market economies against the US dollar.

Source: Seeking Alpha

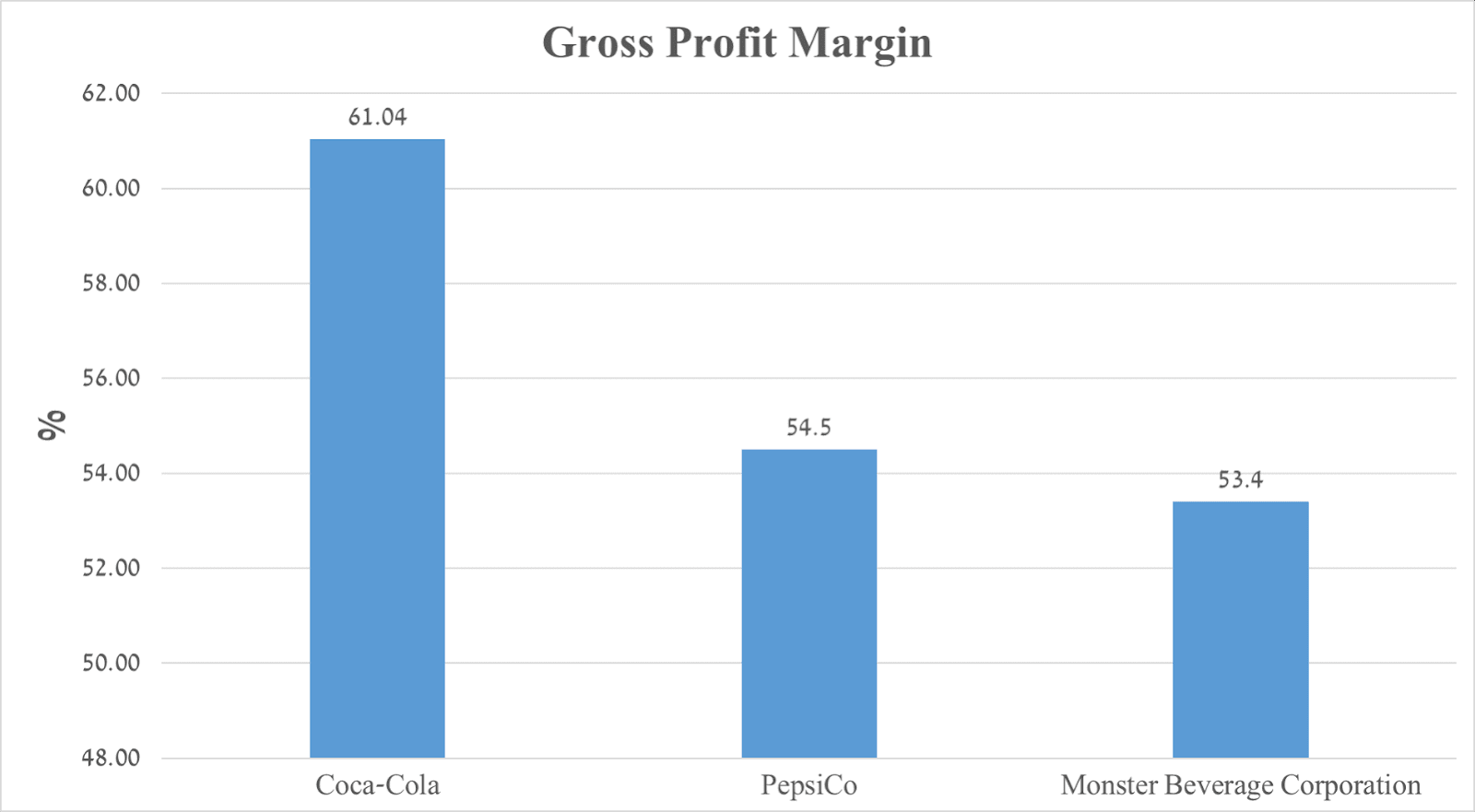

I expect this financial figure to be 61.2% for the fourth quarter due to the company’s revenue growth during the winter holiday season, lower inflation, and improved supply chain network efficiency. In addition, the company’s gross margin is higher than those of PepsiCo and Monster Beverage, which is another factor that makes Coca-Cola an attractive asset for investors.

Source: Seeking Alpha

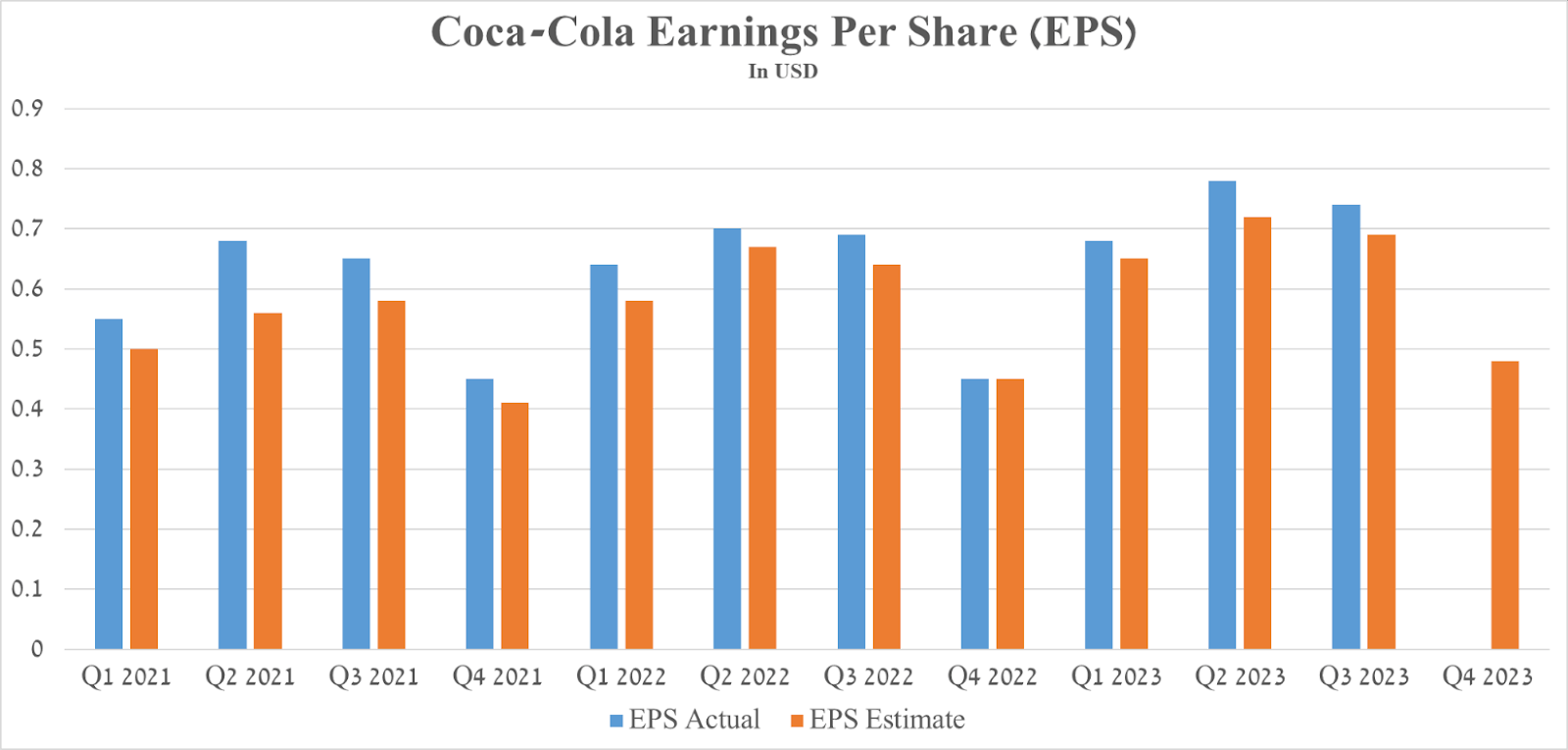

Coca-Cola’s Q3 Non-GAAP EPS was $0.74, up $0.05 from the prior year and also beating analysts’ consensus estimates. This figure is expected to be in the range of $0.47-$0.5 in the fourth quarter of 2023, and, as a result, the company’s Non-GAAP P/E [FWD] will be 21.8x.

Source: Seeking Alpha

In my estimation, this indicates continued investor optimism about Coca-Cola’s business prospects in the run-up to the 2024 interest-rate cuts by central banks, which are likely to increase consumer purchasing power.

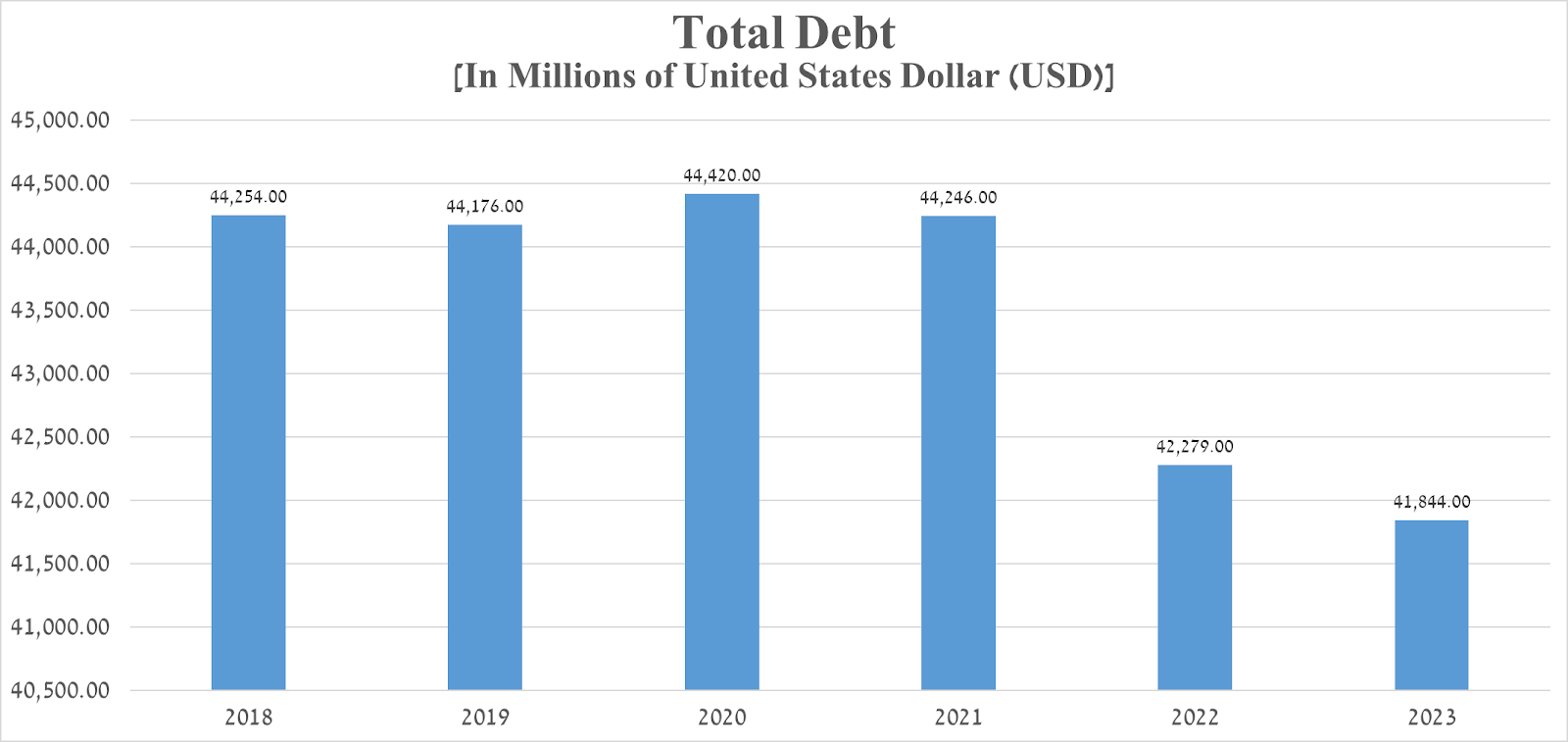

It is equally important to discuss the company’s debt. Coca-Cola’s total debt continues to decline year over year, mainly due to the repayment of notes and loans, and stood at $41.84 billion at the end of September 2023. Moreover, its total debt/EBITDA ratio has fallen below 3x, which indicates the strengthening of the company’s financial stability and, among other things, may contribute to increasing investor confidence and improving its credit rating.

Source: Seeking Alpha

Key risks to consider

I highlight several risks that need to be considered.

Healthy eating trend

While Coca-Cola has an extensive portfolio of sports drinks, juices, teas, and more, the growing popularity of healthy lifestyles may lead to a decrease in demand for its sugar-sweetened beverages, which are often seen as incompatible with a healthy diet.

Strengthening the US dollar

Exchange rate fluctuations significantly impact Coca-Cola’s financial performance since about 64% of its revenue is generated outside the United States.

Source: 10-Q

Strengthening the dollar against other currencies could negatively impact a company’s financial position and results of operations, creating challenges in managing currency risks.

The growing popularity of anti-obesity medications

The past few months have seen an increase in the number of people turning to anti-obesity medications. This trend is explained by the fact that drugs such as Novo Nordisk’s Wegovy and Eli Lilly’s Zepbound can achieve a reduction in body weight of more than 14% in less than a year. One of their key mechanisms of action is aimed at suppressing appetite. As a result, I expect that the popularity of anti-obesity medications may partially slow down the growth of Coca-Cola’s revenue.

Technical Analysis of Coca-Cola

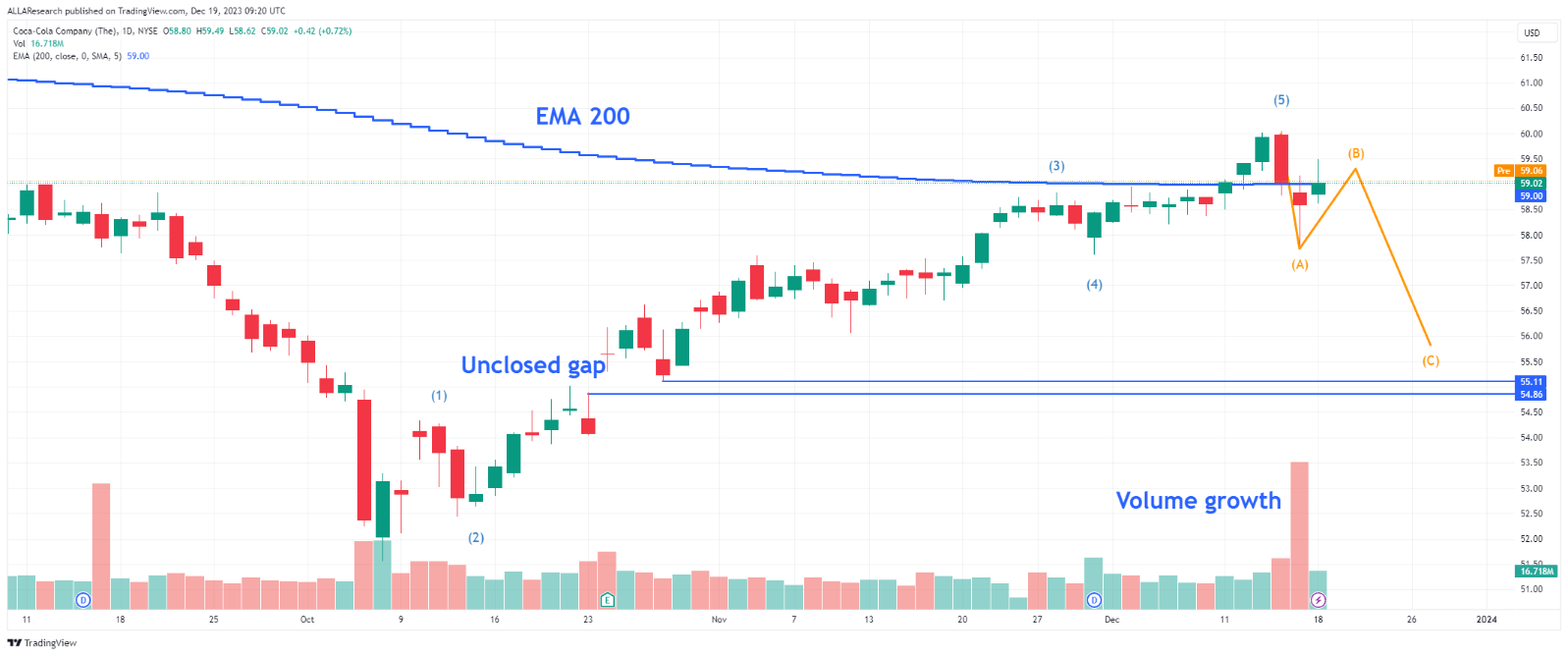

On the daily timeframe, the price of Coca-Cola shares is just below the EMA 200, which is the first signal that the bears are starting to take power into their own hands. In addition, according to my assessment, on December 14, the impulse wave (1)-(2)-(3)-(4)-(5) was completed and, after which a zigzag began to form, marked as (A)-(B)-(C). I expect the company’s share price to continue declining to $55.9-$56.1.

Source: TradingView

Takeaway

Coca-Cola is one of the leading beverage companies and has been a paragon of innovation in the soft drink industry for many decades.

The company’s revenue growth and margins, its high return on equity, the increase in its dividend payments year after year, and the predictability of its business model, these factors make Coca-Cola economically attractive to investors seeking stable and high returns on their investments.

That being said, due to the risks that were described in the article and the expected continuation of the technical correction in the price of its shares, I believe that the price level at which the risk/reward profile will be attractive to conservative investors is $55.9-$56.1 per share.

I’m initiating coverage of Coca-Cola with a “hold” rating.

Analyst’s Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.