While Meta’s big tech peers have hit new all-time highs in recent weeks, META stock is still sitting roughly ~8% off its nominal all-time highs of ~$384.33 per share.

In this note, I shall provide an update on my 5-year CAGR return expectations for Meta.

Furthermore, we will look into the potential pathway for Meta stock to hit new all-time highs in 2024.

Despite recent strong financial performance, Meta stock is overvalued by around 15-20% and may face significant selling pressure in the event of a broad market pullback.

Under the caveat of pursuing slow, staggered accumulation, I rate Meta stock a modest “Buy” at current levels.

Justin Sullivan

Introduction

In my latest report on Meta Platforms Inc. (NASDAQ:META), I downgraded the social media giant’s stock to a “Hold” rating with a prediction for higher volatility in META stock due to surging long-duration treasury yields:

Meta’s ongoing top-line growth re-acceleration and recent margin expansion have driven a strong recovery in free cash flow generation. Furthermore, META stock has been on a strong upward trend, but the recent rise in treasury yields may lead to a corrective pullback in the stock despite Meta’s improving financial performance.

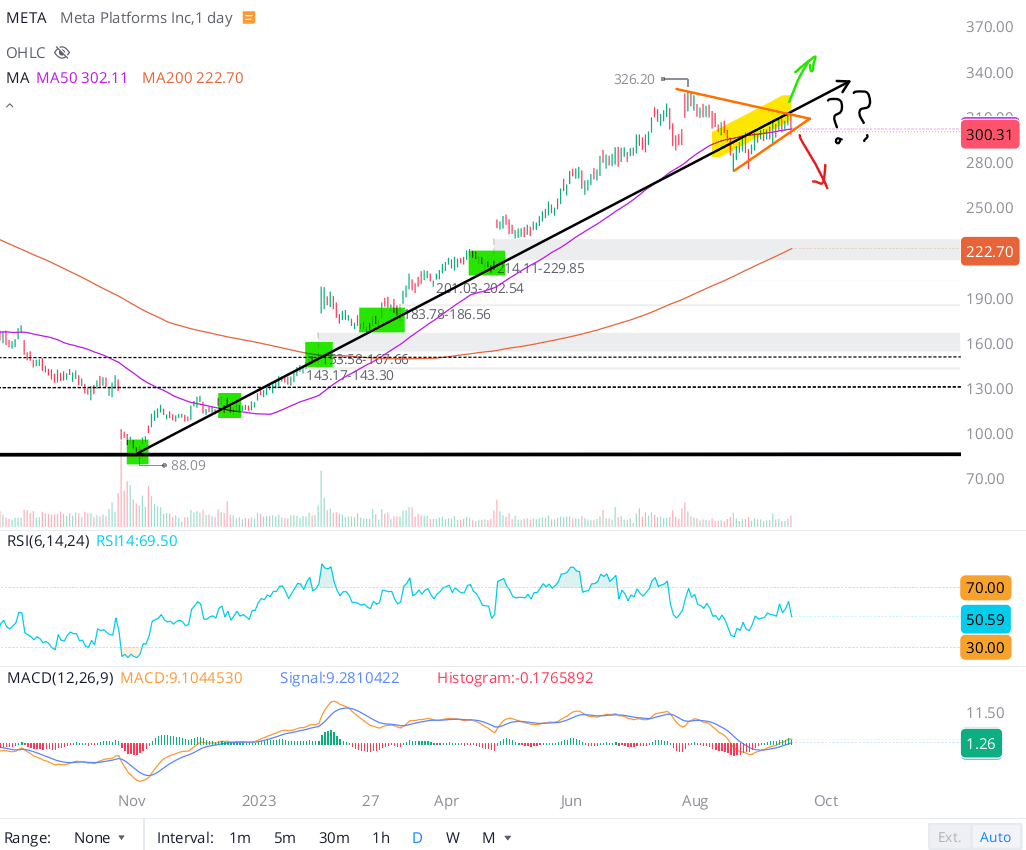

From a technical perspective, Meta’s stock looks primed for a big near-to-medium-term move as the price action tightens in a triangle formation right underneath META’s uptrend line from its 2022 bottom. However, triangles can break out in either direction and so, META investors must brace for volatility.

Meta stock chart 09/18/2023 (WeBull Desktop)

Considering Meta’s strong fundamental performance and relatively reasonable valuation, I think any pullback is likely to be corrective in nature. As you can see in the chart, Meta’s stock has formed a triangle pattern, which can break in either direction. The price action has gotten tighter in recent weeks, and a breakout or breakdown is looking imminent.

If Meta can break back above the uptrend line and re-claim recent highs of $325, I can see the stock marching higher to all-time highs in the next 6-12 months. On the flip side, a breakdown of this triangle can lead META down to low-to-mid $200s for a gap fill. Also, Meta’s chart has another massive gap at ~$155 and that’s where we could be headed in the near-to-medium term if a deep recession (and advertising slump) were to materialize in 2024.

Based on technicals, Meta’s risk/reward is finely balanced right now, with an imminent breakout or breakdown on the horizon. With long-duration treasury yields climbing back above pre-SVB levels [and a flurry of treasury issuance yet to come], a downward resolution looks like the more likely outcome for Meta (and the tech-heavy (QQQ) ETF) in this environment.

After the publication of that report in mid-September, Meta stock bounced around the $300 level quite a bit [heading into Q3 earnings], going as high as $330 and as low as $280 in October 2023. Now, while the corrective pullback was far shallower than our expectations, the heightened volatility view for META stock was accurate!

WeBull Desktop

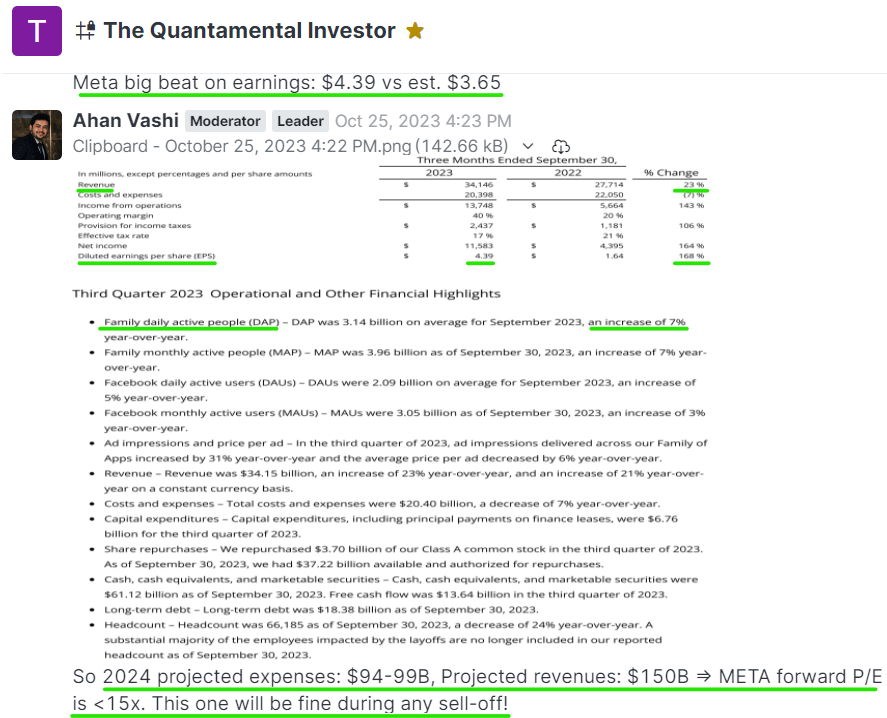

Then, on 25th October 2023, Meta reported much stronger-than-expected earnings for Q3, with revenues coming in at $34.15B (up 23% y/y, +$0.7B greater than street estimates) and EPS rising to $4.39 (vs. est. $3.65).

TQI Chats

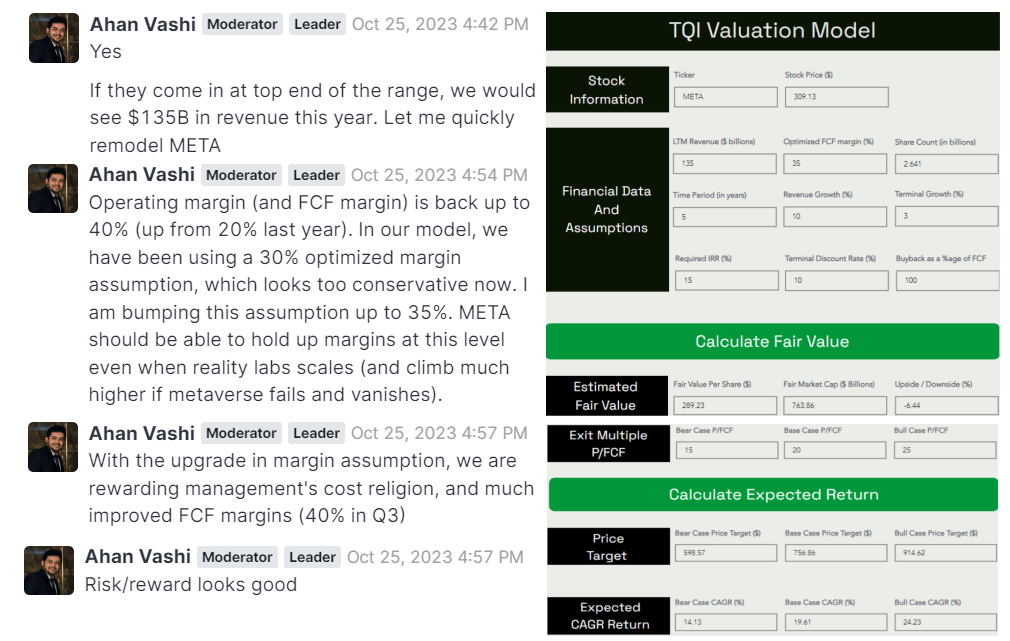

Given improved margin performance and a positive outlook from Meta’s leadership, I raised the optimized margin assumption in our valuation model for META from 30% to 35%. And, with this alteration, our intrinsic value estimate for Meta rose from $245 to $289 per share.

TQI Chats

Now, despite reporting solid financial performance and a broadly positive earnings call from its management, Meta’s stock turned negative in the after-hours session (reversing an initial post-ER pop of +3.5%). While the negative earnings reaction was perplexing, I figured Mr. Market could be pricing in future macro weakness and held off on buying slightly above fair value.

TQI Chats

TQI Chats

Fortunately, Meta sold off further [-5%] in the next trading session, affording us a suitable entry point. At my investing group, we flipped from “Hold” to “Buy” on 26th October, and we have since maintained a bullish view on Meta:

TQI Chats

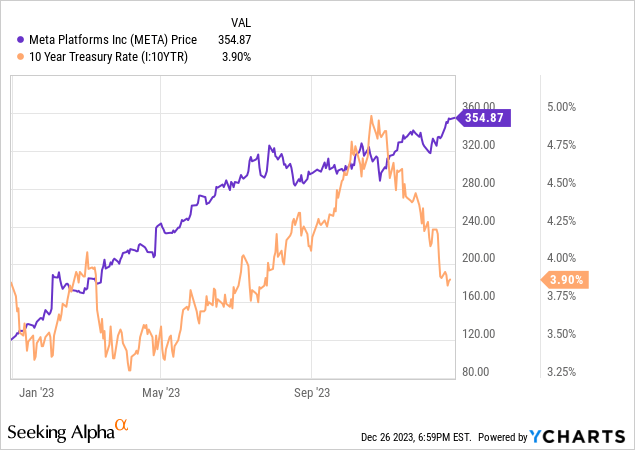

Now, in addition to its strong fundamentals, Meta’s stock is currently benefitting from a sharp decline in long-duration treasury yields [like most of the tech sector (QQQ)]. In fact, the entire post-ER rally in Meta stock (from $290 to $355) is attributable to the movement in yields.

In today’s note, we shall re-evaluate our expected return for Meta in light of this significant jump in the stock. Furthermore, we will try to reason out a potential path to new all-time highs for Meta’s stock in 2024.

META’s Fair Value And Expected Return

Since we are simply looking to assess the impact of the jump in META’s stock price on its expected returns, I will not repeat the finer details of the model in this note. However, if you’re interested, a detailed explanation of our valuation model for Meta is available in this report on SA.

The one key update is the change in the optimized FCF margin assumption, which has been raised from 30% to 35% [explained in the previous section]. All of the other assumptions are straightforward but feel free to share any questions and/or thoughts in the comments section below.

Here’s our latest valuation model for Meta:

TQI Valuation Model (TQIG.org)

As you can see above, Meta’s fair value is still ~$289 per share (or $764B market cap). With the stock currently trading around $355, Meta now looks overvalued by ~20%. Now, Meta has a positive net cash balance of ~$43B (or roughly ~$16 per share). Even if we were to add this net cash back to its fair value (derived by DCF), Meta is still overvalued by ~15%.

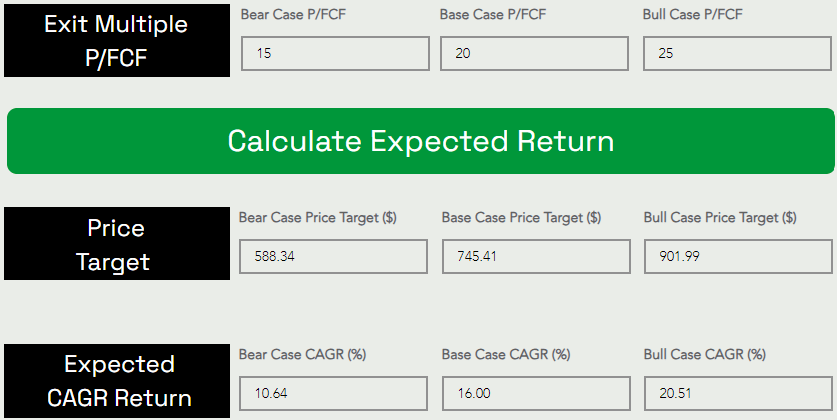

While our fair value estimate is unchanged, the recent gains in META stock have altered its expected returns significantly. Here’s where 5-yr CAGR expected returns stand now:

TQI Valuation Model (TQIG.org)

Assuming a base case P/FCF (exit) multiple of ~20x, I see Meta’s stock rising from $355 to $745 at a CAGR rate of ~16% over the next five years. While Meta’s 5-year expected CAGR has declined from ~20% in late October to ~16%, it still beats my investment hurdle rate of 15%. Hence, META stock is still a decent “Buy” at its current levels under our valuation process.

While Meta’s risk/reward is certainly not as good as it was a couple of months ago (or a year ago [in the $90s] when I was buying hand over fist), technical momentum in META can easily carry the stock higher in the near term amid rising investor interest in artificial intelligence [AI].

Is Meta Platforms Stock Projected To Go Up?

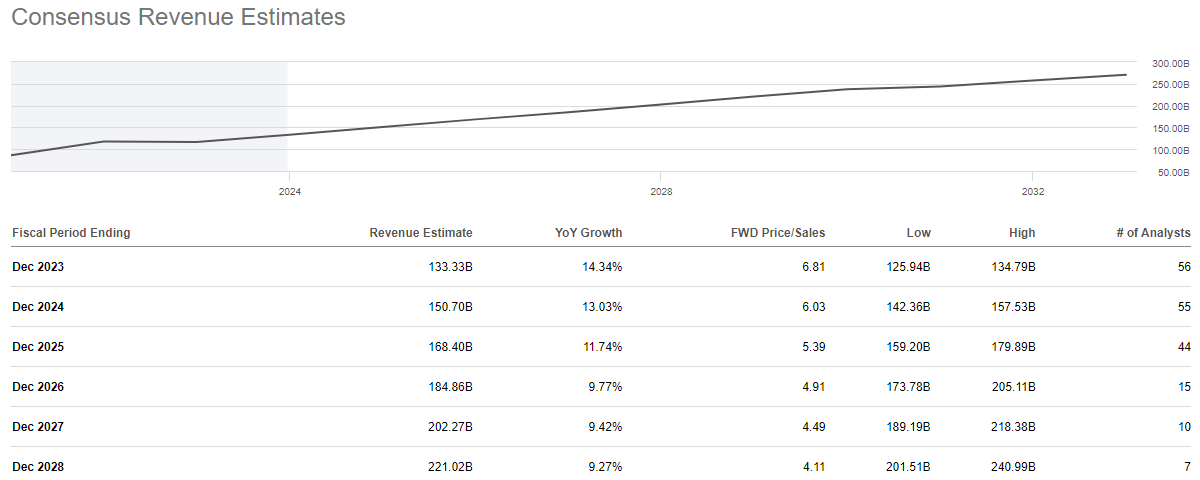

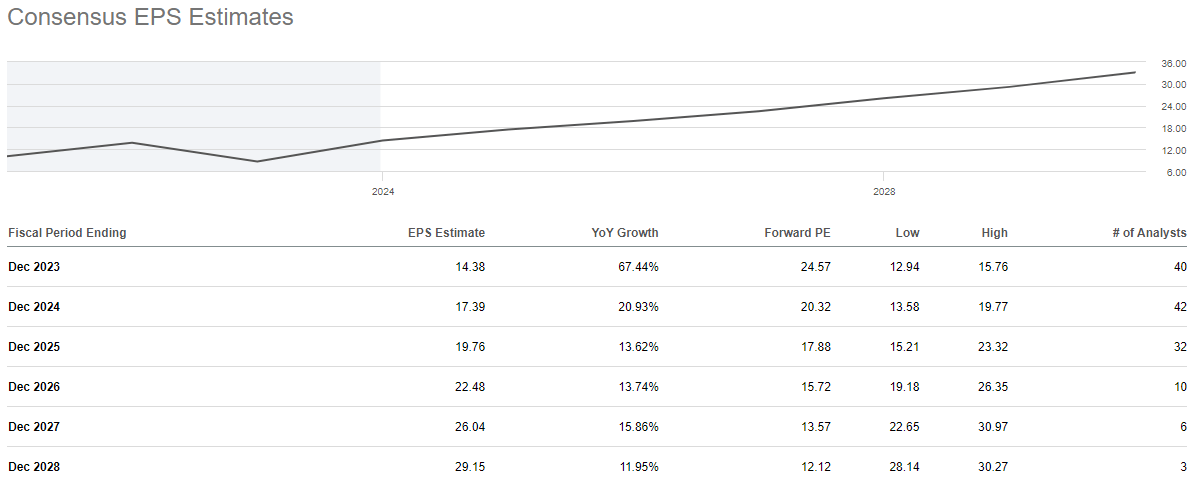

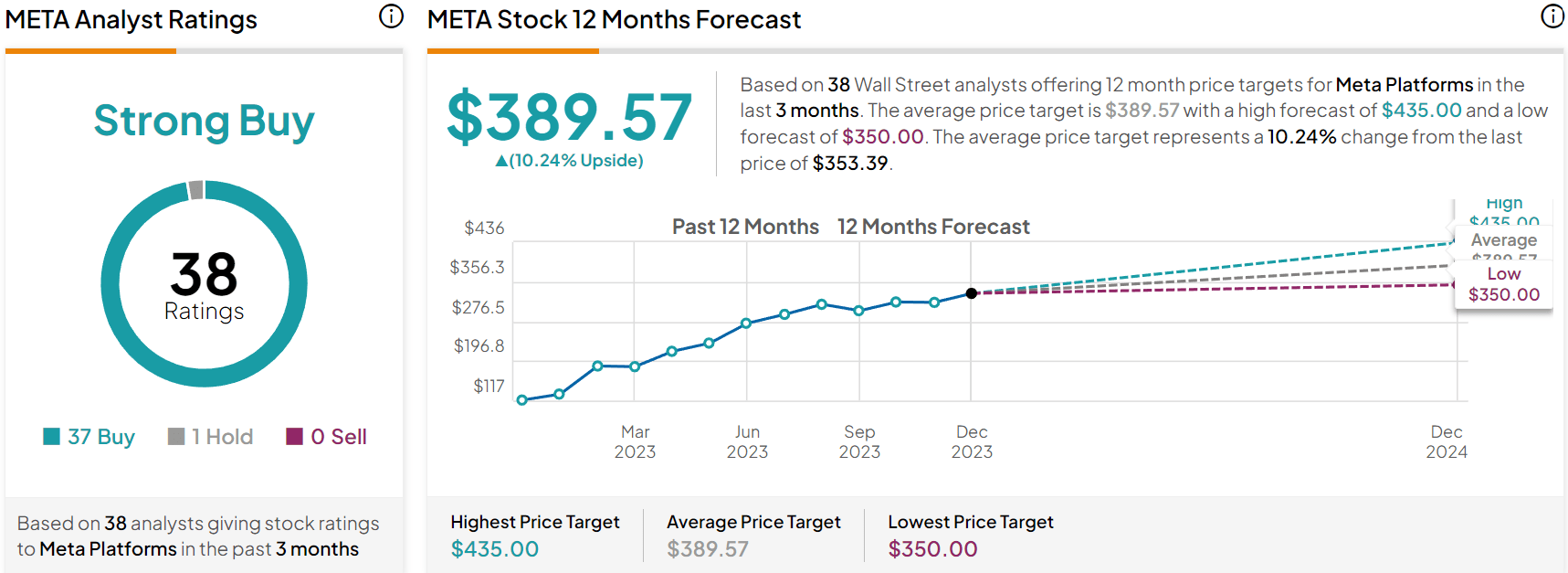

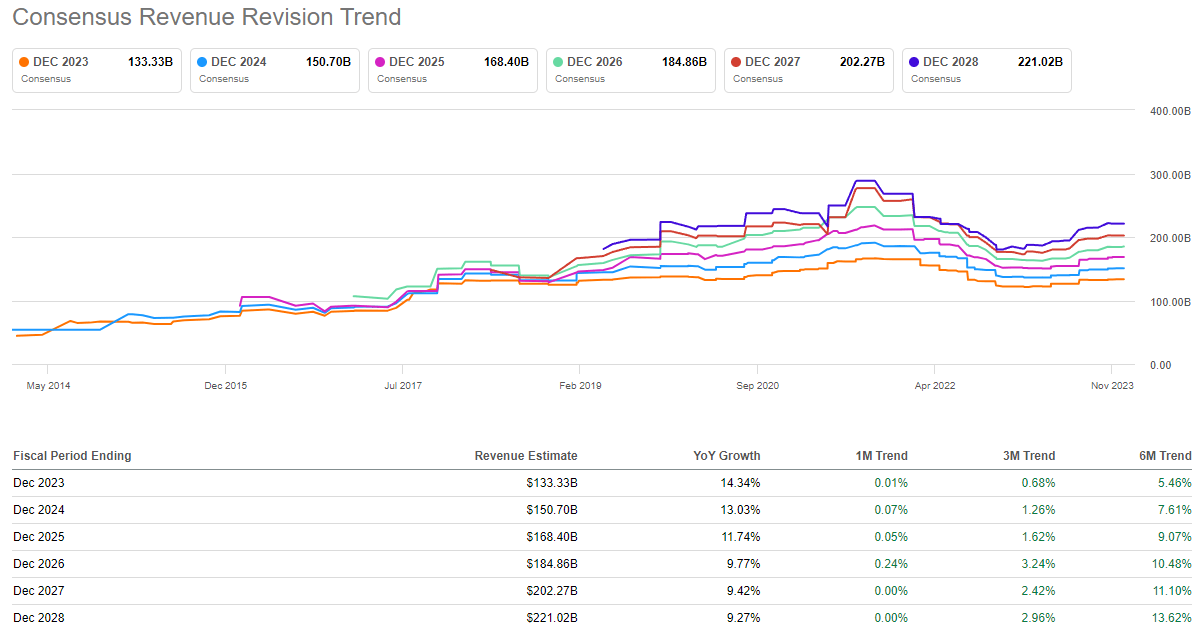

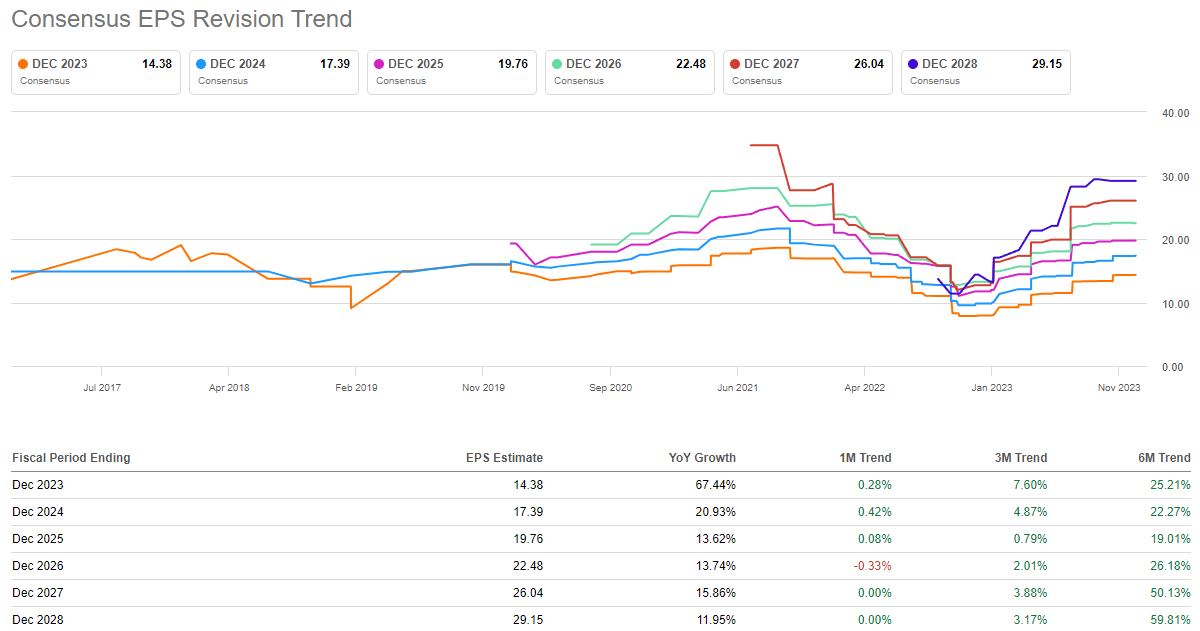

As we have discussed in the past, Meta is set to benefit tremendously from the advancements in the artificial intelligence arena, and consensus analyst estimates from Wall Street firms suggest healthy top and bottom-line growth at Meta over the next five years.

SeekingAlpha

SeekingAlpha

Consequently, Meta’s stock is projected to rise to $389.57 per share in the next twelve months based on 38 Wall Street analyst ratings, with 37 “Buy”, 1 “Hold”, and 0 “Sell” ratings!

TipRanks

Clearly, Wall Street [sell-side] analysts are bullish on Meta’s stock. However, with the tech-heavy Nasdaq-100 index (NDX) (QQQ) breaking out to new all-time highs last week, many investors are pondering whether META stock can reach new all-time highs in 2024. Let’s solve this quandary!

Can META Stock Reach New Highs In 2024?

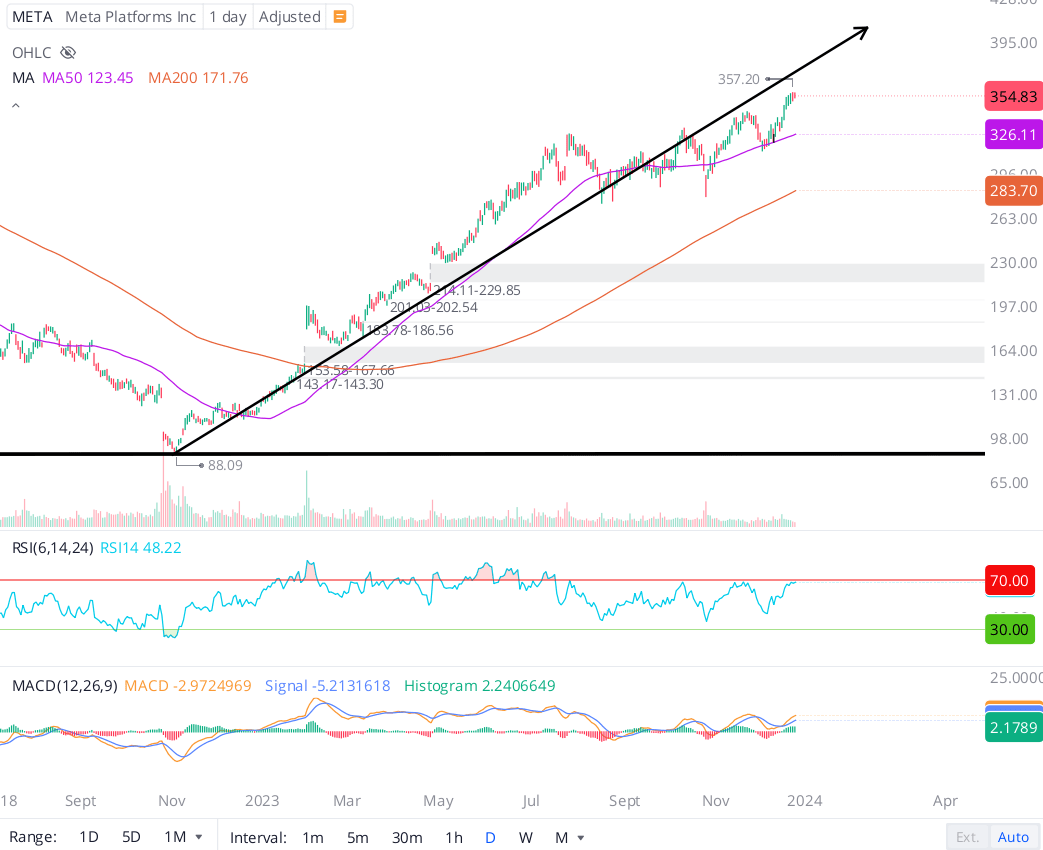

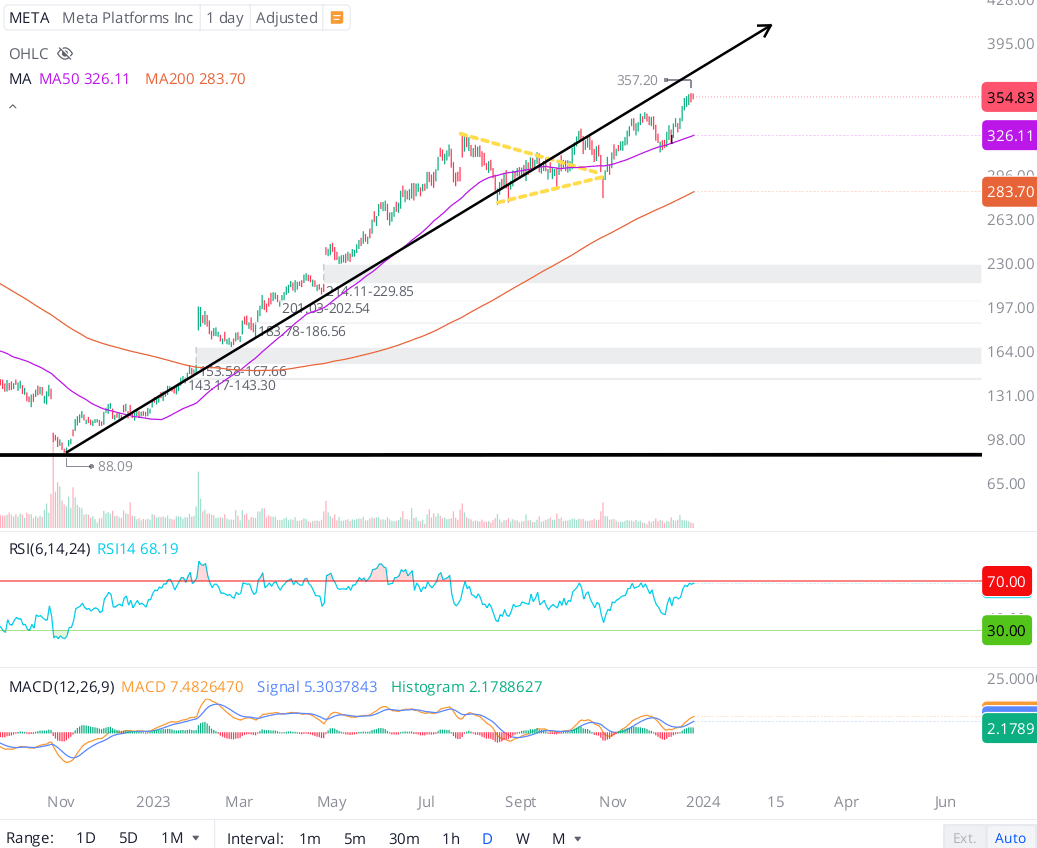

On the back of a stunning 20%+ jump off of its October 2023 lows, Meta’s stock has moved up into the $350s. While tech-heavy QQQ ETF hit new all-time highs last week, Meta is still sitting ~8% off of its all-time highs. Despite being close to “overbought” territory, Meta’s chart setup remains bullish, and while I think META’s price is once again running ahead of its fair value, the stock could continue to climb towards new all-time highs in the next 6-12 months on the back of strong business performance.

WeBull Desktop

Technically, Meta’s stock is still trading under the uptrend line from October 2022 lows, and yet another rejection from the trendline is possible given RSI on the daily, weekly, and monthly charts are in the overbought territory or getting very close to it. The rally in QQQ is also showing signs of exhaustion, with market participants rotating out of the leaders [Magnificent 7 stocks] and into trailing sectors in recent weeks. In the event of a broad market pullback, META stock could come under significant selling pressure, with the stock having gone up in a straight line since hitting a bottom in October 2022.

However, if Meta’s stock manages to re-claim its uptrend line, I can see META breaking above its previous nominal highs of $384.33 per share in the near future. From a psychological standpoint, the $400 level could prove to be a big hurdle; however, Meta can surely take a swing at it in 2024 given growing optimism on Wall Street, strong momentum in the business & the stock, and relatively better valuation than peers.

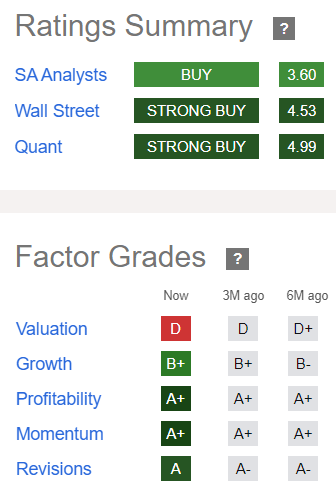

Meta Quant Factor Grades (SeekingAlpha)

According to Seeking Alpha’s Quant Rating system, Meta has a “Strong Buy” rating with a score of 4.99/5. While Meta continues to boast an “A+” rating on “Profitability”, the earnings “Revisions” grade has improved from “A-” to “A” over the last three months in a clear indication of an imminent recovery in earnings growth. With sales growth of ~23% y/y in Q3 2023, Meta’s strong quant factor grade of “B+” for “Growth” makes complete sense.

SeekingAlpha

SeekingAlpha

SeekingAlpha

While Meta’s “Valuation” grade has deteriorated to “D” on the back of a sharp move up in its stock, the “Momentum” grade is now a firm “A+”. In my view, both Meta’s business and stock are showing improved momentum. And in the near term, technical momentum alone can be enough to drive a stock higher.

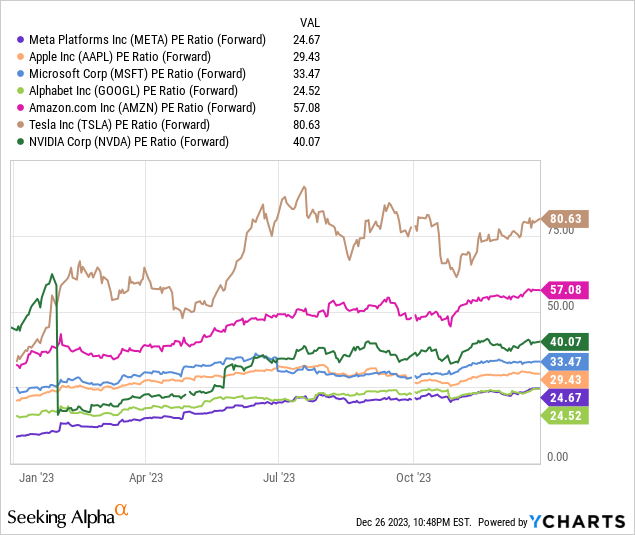

Now, Meta isn’t just a technical momentum play here, as its future earnings projections are showing a “V-shaped recovery”. Furthermore, Meta is still one of the cheapest names in the big tech arena:

As per data from YCharts, Meta’s forward P/E currently stands at 24.67x, which represents a 20-30% discount compared to the likes of Apple (AAPL) and Microsoft (MSFT). Now, in my view, Meta is likely to generate $150B in revenue in 2024. Given management’s total expense guide of $94-99B, I believe Meta can produce ~$55B [$20+ per share in profit] next year. Assuming 2024 EPS of $20, Meta is trading at just ~18x 2024E earnings, which is lower than S&P 500’s (SPY) forward P/E multiple of ~20x.

With Meta’s business growing faster than both AAPL and MSFT, I think META stock getting re-rated higher to multiples commanded by big tech peers such as Apple and Microsoft is more than plausible. That said, I like to be conservative in my assumptions, and so, I am assuming that Meta will only re-rate up to the market (S&P 500) multiple of ~20x forward P/E.

Now, assuming a ~20x forward P/E multiple and 2025E EPS of $22, I can see META stock rising to ~$440 per share by the end of 2024! That’s another 24% upside from current levels.

Bottom Line

The answer to our question is – “Yes, Meta can get to $400 in 2024”. And we now know what needs to happen for Meta to get there – continued business momentum and a reasonable amount of trading multiple expansion. Given the current macroeconomic environment and the elevated likelihood of a hard landing (economic recession) in 2024, it is hard to foresee further trading multiple expansion. However, that’s exactly what has driven the year-to-date stock market rally in 2023. And despite Meta rallying by more than 200% in the past year, it is undervalued on a relative basis.

After a significant jump in its stock price, the long-term risk/reward for Meta is not as attractive as it was back in October. However, I think a 5-year CAGR return of ~16% from a secular growth compounder like Meta is worthy of fresh capital in this environment. In my view, Meta remains a much better hideout than many of its big tech peers due to its relatively reasonable valuation. Under the caveat of pursuing slow, staggered accumulation, I rate Meta stock a modest “Buy” at current levels.

Key Takeaway: I rate Meta a modest “Buy” in the $350s, with a strong preference for staggered accumulation.

Thanks for reading, and happy investing. Please share your thoughts, concerns, and/or questions in the comments section below.

Analyst’s Disclosure:I/we have a beneficial long position in the shares of META either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.

How To Invest In This Environment?

In order to navigate this tricky economic period, we are pursuing “Bold, Active Investing with Proactive Risk Management” at our investing group – “The Quantamental Investor“. With a laser focus on valuations, profitability, and balance sheet strength, we are buying the winners of tomorrow! Furthermore, we are utilizing index-based options to guard against significant broad-market declines. Join us today to prepare for whatever the market may throw at you in 2024!