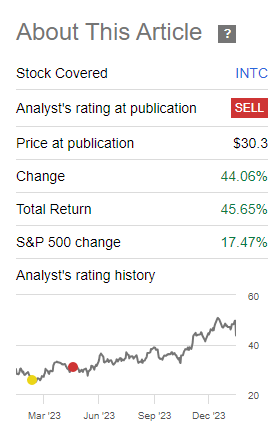

We got the Intel thesis wrong and the stock soared soon after our Sell call.

Q4-2023 was a great quarter if you kept your eyes firmly on client computing and did not glance at the data center segment.

Intel hit a wall at 4.0X revenues, despite some strong inflows into the semiconductor segment.

troyek

It is safe to say that we got the thesis wrong about Intel Corporation (NASDAQ:INTC). When you get such price action after your first (and only) “Sell” call, then you have to acknowledge that you got things wrong.

3 Things The Wall Street Cheerleaders Are Getting Wrong

Even more embarrassingly, this is total return after an epic down day post the Q4-2023 results. So what more is there to say? Well, looking at the thesis and how it played out highlighted one of the most important lessons in this bull market. We go over what we thought would happen, what actually did happen and how we are changing our stance.

Our Assumptions

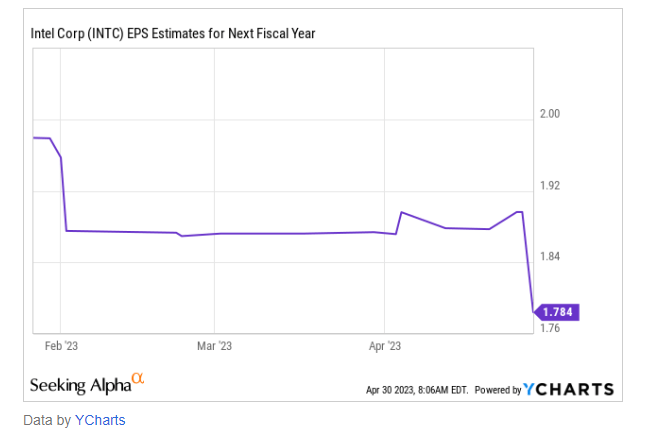

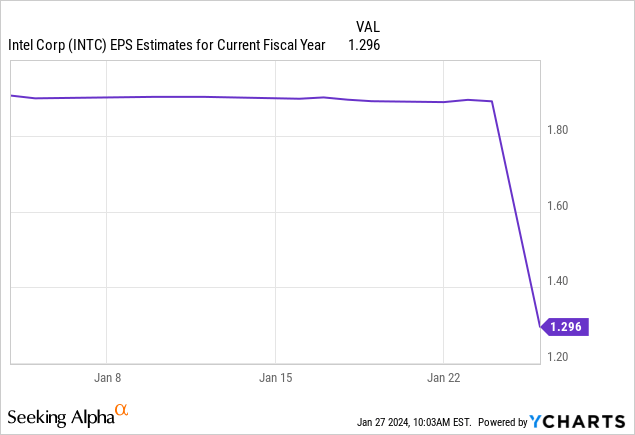

Our thesis was built on the idea that INTC won’t come close to hitting the 2024 estimates that were in place at the time. Note that at the time of the May 2023 article, INTC’s estimates had just taken a swan dive.

After the results, almost all analysts cut their estimates. You can see that by the drop in the 2024 estimates, which fell about 6%.

3 Things The Wall Street Cheerleaders Are Getting Wrong

Source: 3 Things The Wall Street Cheerleaders Are Getting Wrong

So we felt that even that lowered bar of $1.78 will not be met. Keep that in mind, that $1.78 number especially, before you judge how badly we did.

Q4-2023

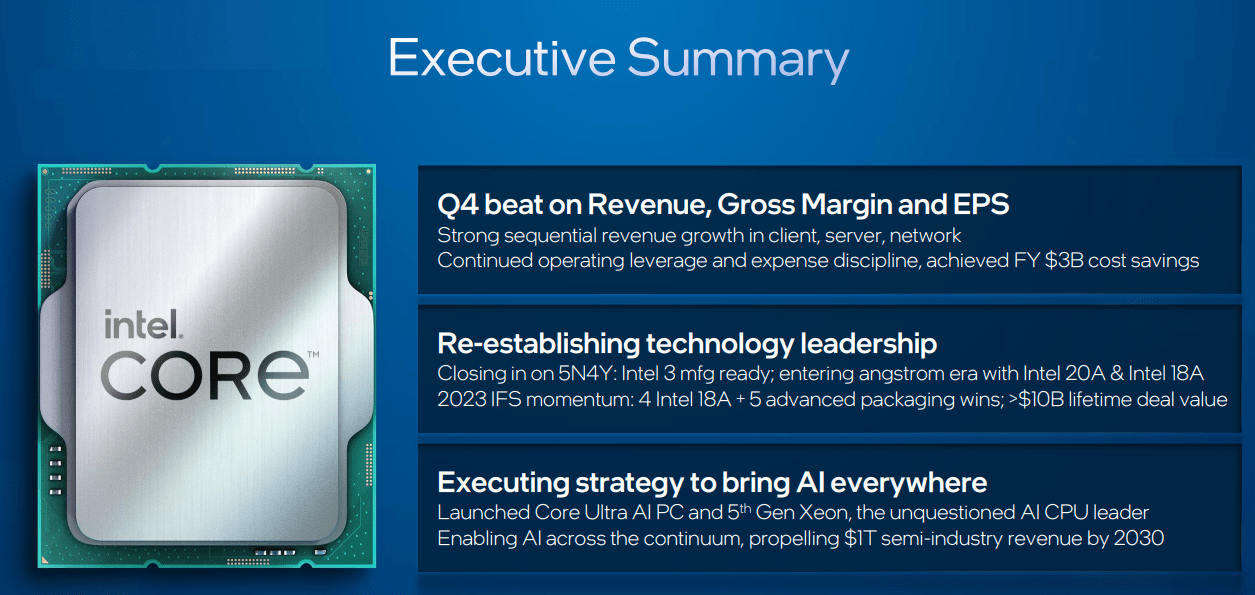

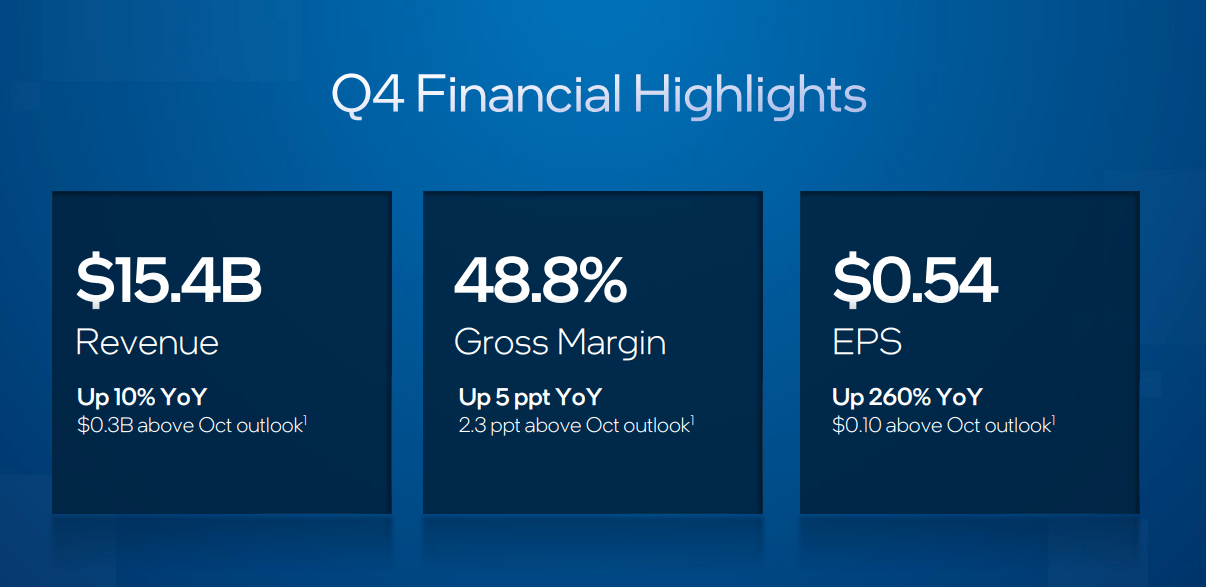

Q4-2023 was a barnburner of a quarter for INTC. The company claimed to beat on revenue , gross margins and earnings per share.

INTC Q4-2023 Presentation

That of course is strange as INTC basically leads all the analysts where it wants and hence sets itself up to “beat”. But there is no question that $0.54 of earnings is rather strong on $15.4 billion of revenue. We would have not expected gross margins to deliver this well on that small (relative to pre 2022) revenue base.

INTC Q4-2023 Presentation

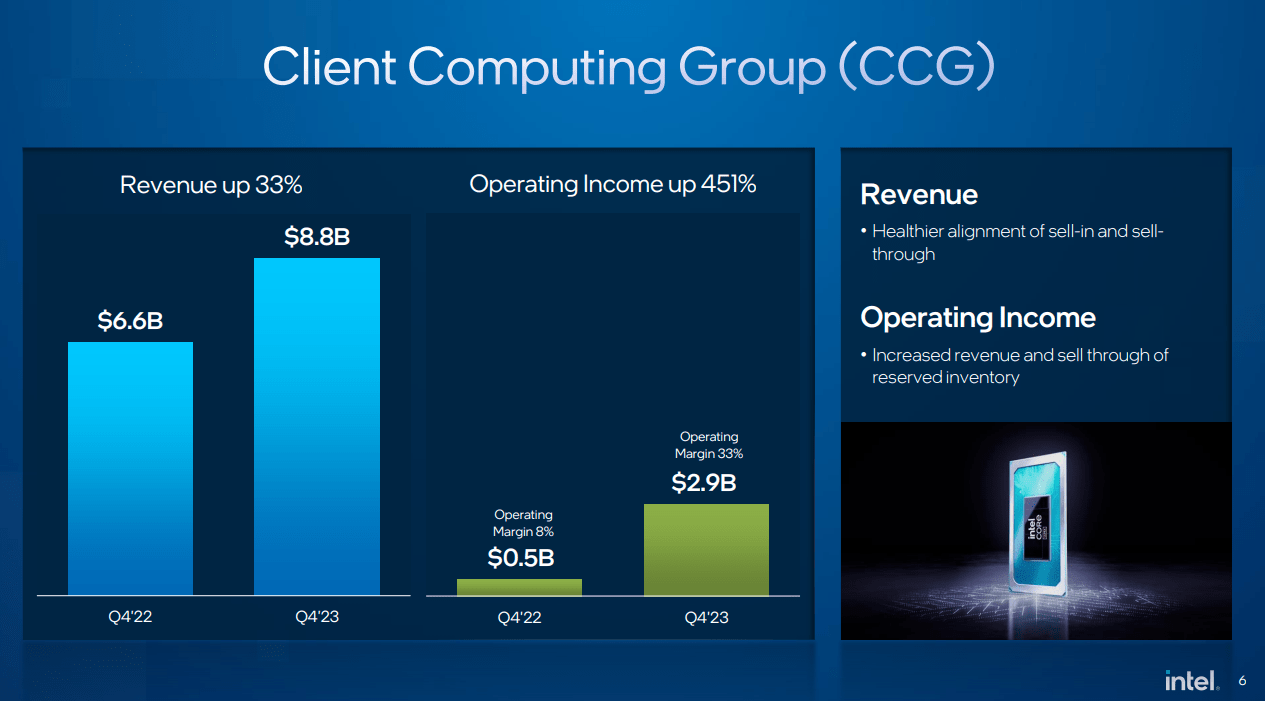

The segmental performance showed that it was essentially all client computing. Operating income from this one area was responsible for all the “beat”.

INTC Q4-2023 Presentation

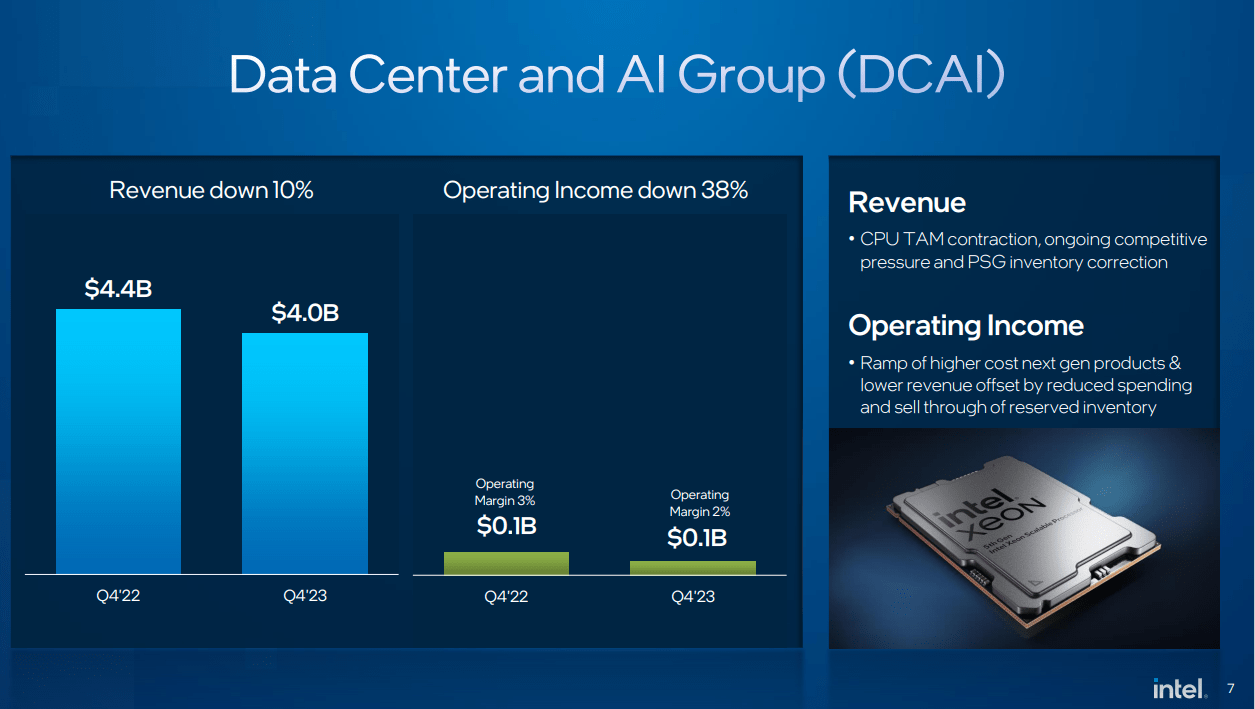

Data center revenues on the other had was down 10% in what can only be truly described as the “age of AI”. They actually have put AI group in the slide below and we don’t think this helps their case. It only helps investors realize just how far removed INTC is from anything related to AI.

INTC Q4-2023 Presentation

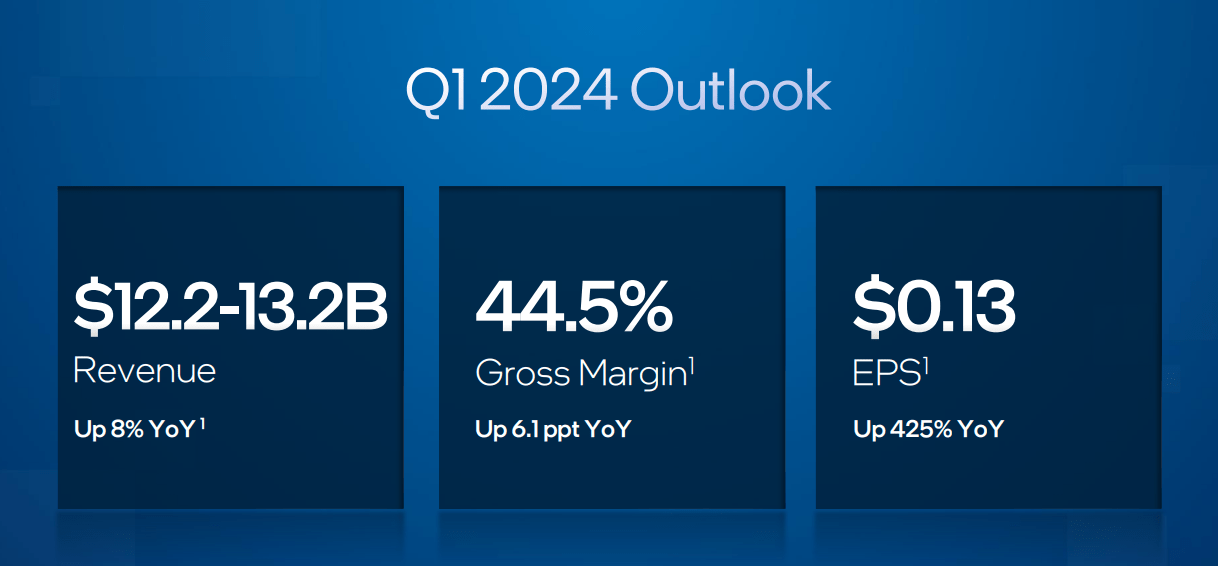

With that out of the way and the average investor believing that AI probably refers to Afghanistan Infrastructure in the case of INTC, the company dropped the second shoe.

INTC Q4-2023 Presentation

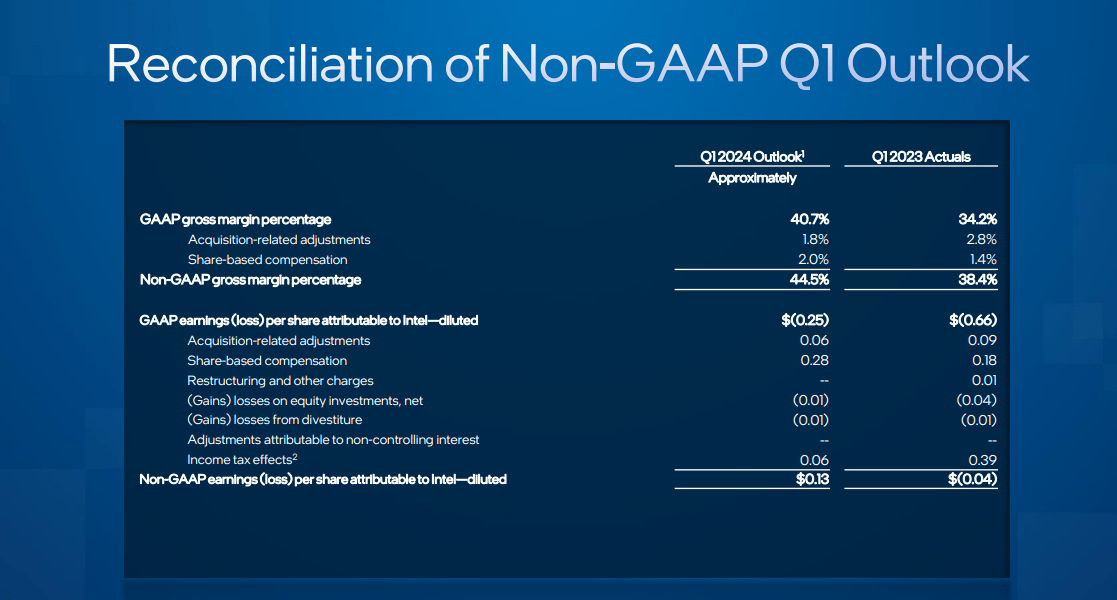

Analysts were looking for more than $1.0 billion higher in revenues and earnings per share of at least three times as high for Q1-2024. Even those earnings of 13 cents are non-GAAP. On a GAAP basis , INTC will likely show a big loss for Q1-2024.

INTC Q4-2023 Presentation

With all that done and dusted, how did we fare when we suggested INTC won’t come in the ballpark of $1.78 in earnings for 2024? Well the analysts were taking on our thesis right until the results. Average estimates were for $1.85 for 2024. Post results, we now see a $1.30 number.

Even this will require a trailblazing back half as Q1-2024 and Q2-2024 are combined estimated at 40 cents.

Outlook

Valuation compression or expansion can be one of the hardest things to deal with in investing. Some of our energy investments have fundamentally performed fantastically. They have improved their debt structure and reduced risks and yet their enterprise value has fallen.

You cannot do anything about that but reassess and then double down (we did on that name).

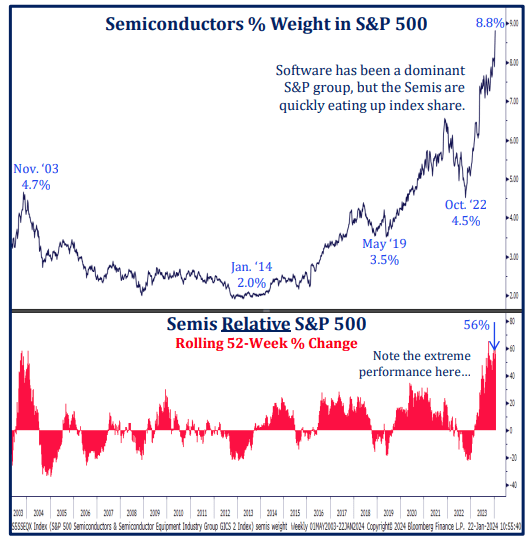

On the other hand, the flight of fantasy for some names can continue. INTC seems to be in that category. Likely boosted by passive inflows to S&P 500 (SPY) and semiconductor sector ETFs like VanEck Semiconductor ETF (SMH) . The weight of semiconductors in the S&P 500 has doubled from the five quarters back. If you believe that is totally sustainable then we have a Pringle chip to sell you.

X

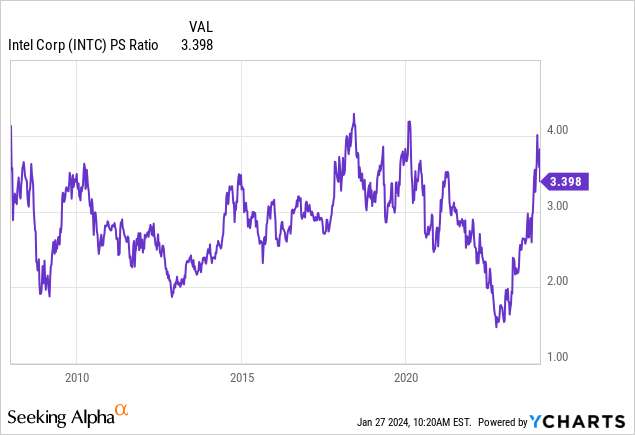

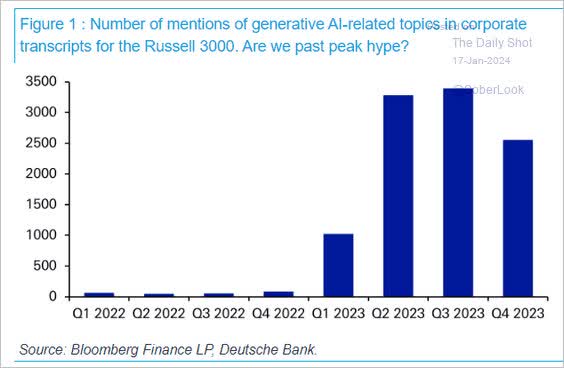

But even that boost already seems to have a ceiling for INTC at least. INTC hit a wall right at the 4X sales figure, which has historically been hard for even mega bulls to push through.

This is despite a rather “strong” performance from the metric that investors seem to care about the most. AI was mentioned 38 times on the Q4-2023 conference call. We are going to go out on a limb and suggest this is the peak for mentions. Certainly the broader enthusiasm for it seems to be past its peak.

Daily Shot As Shared By Jesse Felder On X

We continue to rate the shares a Sell and think the longer term path remains lower.

Please note that this is not financial advice. It may seem like it, sound like it, but surprisingly, it is not. Investors are expected to do their own due diligence and consult with a professional who knows their objectives and constraints.

Analyst’s Disclosure:I/we have a beneficial short position in the shares of INTC, SPY either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.

Are you looking for Real Yields which reduce portfolio volatility?

Take advantage of the currently offered discounton annual memberships and give CIP a try. The offer comes with a 11 month money guarantee, for first time members.