Summary:

- Rivian shares have plummeted from $179 to $10, representing extreme highs and lows in the EV sector.

- The stock is oversold and could be due for a rebound, potentially forming a bullish double bottom.

- Rivian stands out as a leader in the EV industry with successful collaborations and potential future deals with major companies like Ford, Amazon, and possibly Apple.

400tmax/iStock Unreleased via Getty Images

Rivian Automotive, Inc. (NASDAQ:RIVN) shares have been crushed over the last couple of years. I remember when I saw this stock trading up to around the $170 range, and I was wondering what are people thinking, paying this much for the stock. However, now I am wondering what people are thinking and doing, selling this stock for about $10. It seems like the former highs and the current lows represent extremes. Clearly, this stock was a sell when it was trading at extremely high levels, but I think it looks like a speculative buy around $10.

The whole EV sector has crashed to various degrees. Tesla (TSLA) shares were trading around $260 a few months ago and now it trades for $172. Lucid is down to about $3 per share, and Fisker (OTC:FSRN) shares can be bought for a dime and could be delisted from the NYSE. Seeing this kind of price action is not helpful in terms of sentiment for this sector as a whole. But, there is a washout going on in this industry and we could be at a moment of capitulation. Through this washout process, the higher quality EV companies will eventually continue to emerge as industry leaders, while some companies could end up bankrupt or selling their assets. It’s clear that Tesla will remain a leader, but I also think the market is big enough for Rivian to be successful as well. Let’s take a closer look below:

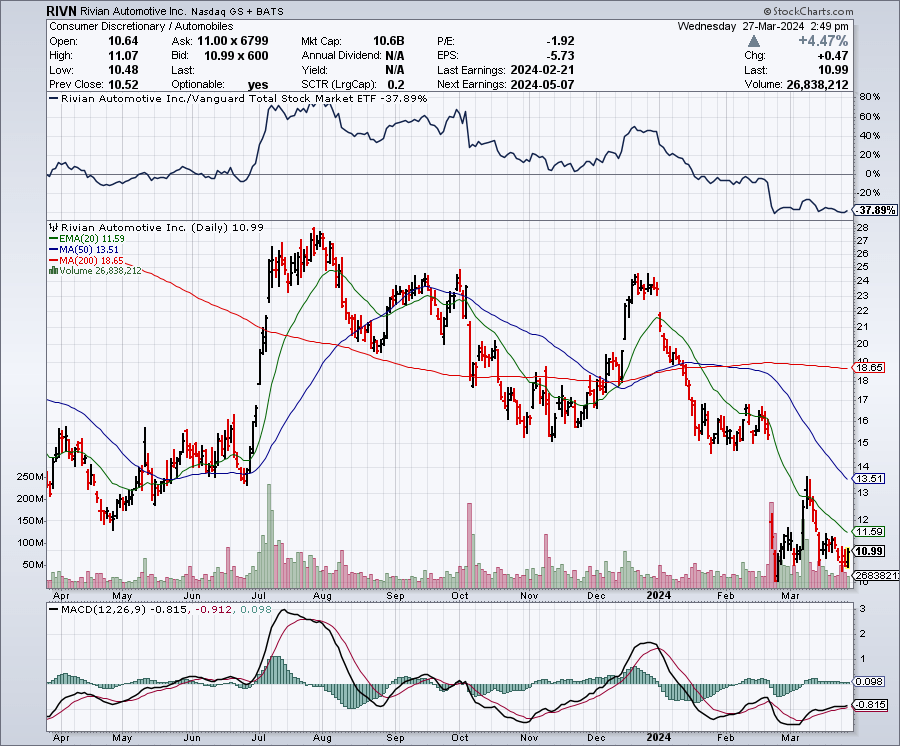

The Chart

As the chart below shows, Rivian shares have had many ups and downs for the past several months. This stock was trading in the $20 range at the start of this year, but it has just about been cut in half. The stock is trading well below the 50-day moving average which is $13.65, and the 200-day moving average which is $18.67. Rivian shares are oversold and could be due for a rebound. Also worth noting is that this stock plunged to around the $10 level in late February and then jumped to about $14 in early March, and now once again is back to the $10 range. If this level around $10 holds, this could be setting the stock up for a potentially very bullish double bottom.

StockCharts.com

Why Rivian Stands Out As A Leader

The EV industry appears to be going through a shakeout and that could be bringing capitulation to many stocks in this sector. It seems clear that Tesla is going to do just fine in the long-run, and I believe Rivian is going to survive this shakeout and be one of the leading EV companies. Some of the other companies in this sector appear to have too many challenges. One reason I see Rivian as a standout in this industry is because it has signed successful collaborations and deals with other major companies such as Ford (F), and Amazon (AMZN), in the past. I think this speaks to the quality of this company and I believe more collaborations could come in the future.

There are reports that Apple (AAPL) recently shelved plans to create an electric vehicle. However, I would not be surprised if Apple decided to collaborate in some way with Rivian. There has even been speculation that Apple could buy Rivian and I believe this makes more sense than starting from scratch. Whether this happens or not, I do think it is likely that Rivian will announce more important deals with other major companies. I also see a lot of potential for Rivian in terms of commercial vehicles, such as the vans that Amazon uses for deliveries. A recent Forbes article points out a number of reasons why it could make sense for Apple to buy Rivian, including the perception that Tim Cook and Rivian’s CEO Robert Scaringe would be compatible and so would Apple be with Rivian under its belt. The article states:

“And whatever price Scaringe might want for Rivian would be pocket lint for Cook, who would likely just do a stock swap deal and remain fairly hands-off in terms of Rivian’s development, which seems well on its way.

Putting Rivian under Apple’s umbrella would give Scaringe the vast, vast financial and R&D resources he now needs to compete with Tesla – and everyone else – going forward. For Cook and Apple, they would finally get the vehicles compatible with their tech and market expansion goals, vehicles that are already on the market, with many more to come.”

Earnings Estimates And The Balance Sheet

Analysts expect Rivian to post a loss of about $4 per share on revenues of $4.87 billion in 2024. In 2025, the loss is expected to decline to $2.62 per share while revenues jump to around $7.8 billion. In 2026, the loss is expected to narrow to $2.09 per share and sales are expected to surge again to about $12.2 billion. Obviously, no one wants to see continued losses, but the growth in revenues is phenomenal, if these estimates hold true. When investors see this type of growth, it is easier to overlook losses and losses are often part of the deal when a company is growing at a blistering pace. We have seen that to be the case in the past with many companies, including Amazon.

As for the balance sheet, Rivian has about $4.92 billion in debt and $9.37 billion in cash. This is a strong balance sheet, although it will weaken in the next couple of years, unless the company tightens the spending and there are signs it is moving to cut costs.

Recent Downgrades

A number of analysts recently downgraded Rivian shares and this clearly has created more selling lately as some shareholders appear to be capitulating when it comes to the EV sector. The latest downgrade I saw came on March 25, 2024, from an analyst at Mizuho Securities in which it lowered its price target on Rivian to $12. For many of us, a downgrade from a Wall Street analyst that is made when a stock is already trading at or near 52-week lows is lacking credibility. Especially when the stock has lost nearly 90% of its value from the all-time high. Where were the $12 price targets for Rivian shares when it was trading for $100 or $150, or $170 per share, because that’s when it would have been prescient and helpful. I bring all this up because I see these recent downgrades as being very late, and ill-timed, and as a sign of a potential capitulatory bottom for this stock.

New Products And Other Upside Catalysts

In early March, 2024, Rivian unveiled some new models including the R2 (a mid-size SUV), the R3 (a mid-size crossover), and the R3X (a sportier version of the R3. One recent Seeking Alpha article stated that the R2 model received 68,000 orders in the first 24 hours. The article also went on to point out that Rivian is implementing cost cuts which could help investor sentiment. Improved financial results from these cost cutting measures could be an upside catalyst in the coming quarters. The R2 is expected to start at $45,000 and has a 2026 delivery estimate.

(C) 2024 Hearst Autos, Inc. All Rights Reserved

In late March, Rivian announced a deal whereby Rivian owners could charge their vehicles at Tesla’s SuperCharger Network. This shows yet again how Rivian is able to collaborate with other major companies, even a competitor like Tesla. I believe more deals with other companies are coming and this could be a major upside catalyst for Rivian shares. Thes deals could involve a big order for some of its commercial vans, or it could be something with Apple, etc.

Potential Downside Risks

The fact that this company doesn’t have a very long track record is a potential downside risk. As a relative newcomer to the auto industry, it might not be as experienced in handling certain challenges, like perhaps, a major recession. The biggest concern I have is with the losses, especially as these losses are expected for at least the next couple of years. For this reason, I was happy to hear that Rivian recently decided to delay and reduce capex.

In Summary

I see a few reasons why it could make sense to buy Rivian shares now, although I also don’t plan to buy a big position, since I see this stock as speculative. One of the things I like most, is that it is far less speculative and far less risky at $10, than when it was at $179 per share. The chart shows this stock is oversold and there is the potential for a bullish double bottom to be forming as well. I feel that sentiment towards the EV sector is too negative now, and that is something contrarian investors can appreciate. If Rivian is successful in cutting costs and delivering some new models like the R2 in 2026, this stock could be a very rewarding buy to make now.

No guarantees or representations are made. Hawkinvest is not a registered investment advisor and does not provide specific investment advice. The information is for informational purposes only. You should always consult a financial advisor.

Analyst’s Disclosure: I/we have a beneficial long position in the shares of RIVN either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.