Summary:

- Snowflake has been one of the worst-performing AI megatrend beneficiaries, and the company just appointed a new CEO to right the ship.

- Make no mistake, Snowflake is growing fast, just not as fast as they could be considering the huge opportunities ahead for cloud and AI.

- After reviewing Snowflake’s business, unique value proposition, growth opportunity, new CEO, valuation, and risks, we conclude with our strong opinion on AI as a theme and Snowflake as an investment.

Snowflake: New CEO, Big AI Opportunity BlackJack3D

Fads come and go. Megatrends (such as urbanization and the internet) change the world. Certainly, megatrends can get ahead of themselves (there was an internet bubble in the early 2000s, and more recently China built entire cities expecting rapid pockets of urbanization that never happened). Some investors wonder if Artificial Intelligence (“AI”) is a fad, a megatrend that has gotten ahead of itself, or is still in its infancy. In this report, we address this question with a variety of data points and a special focus on big-data AI stock Snowflake (NYSE:SNOW) (including its business, growth opportunity, new CEO, valuation, and risks). We conclude with our strong opinion on AI as a theme and Snowflake as an investment opportunity.

20+ Top AI Stocks

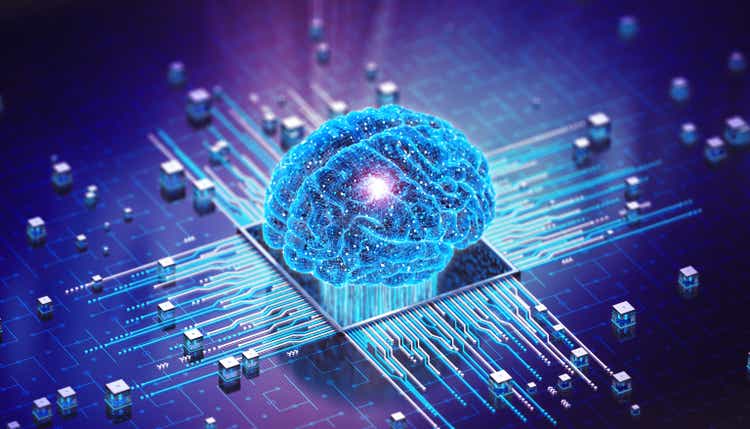

Before getting into Snowflake, the following table first includes comparative data on 20+ top AI stocks (you likely recognize many of them). The companies are ranked by year-to-date performance, and you can clearly see Snowflake is one of the worst performers.

data as of market close: 3/28/24 (Stock Rover)

(SMCI) (SOUN) (NVDA) (VRT) (PSTG) (MU) (META) (CRWD) (ANET) (AMD) (AMZN) (ISRG) (NET) (GOOGL) (AAPL)

The table includes additional data points we will refer to throughout this report, including expected revenue growth rates (for this fiscal year and next), profit margins, valuation, research & development spending, analyst ratings, and more.

AI Market In Perspective

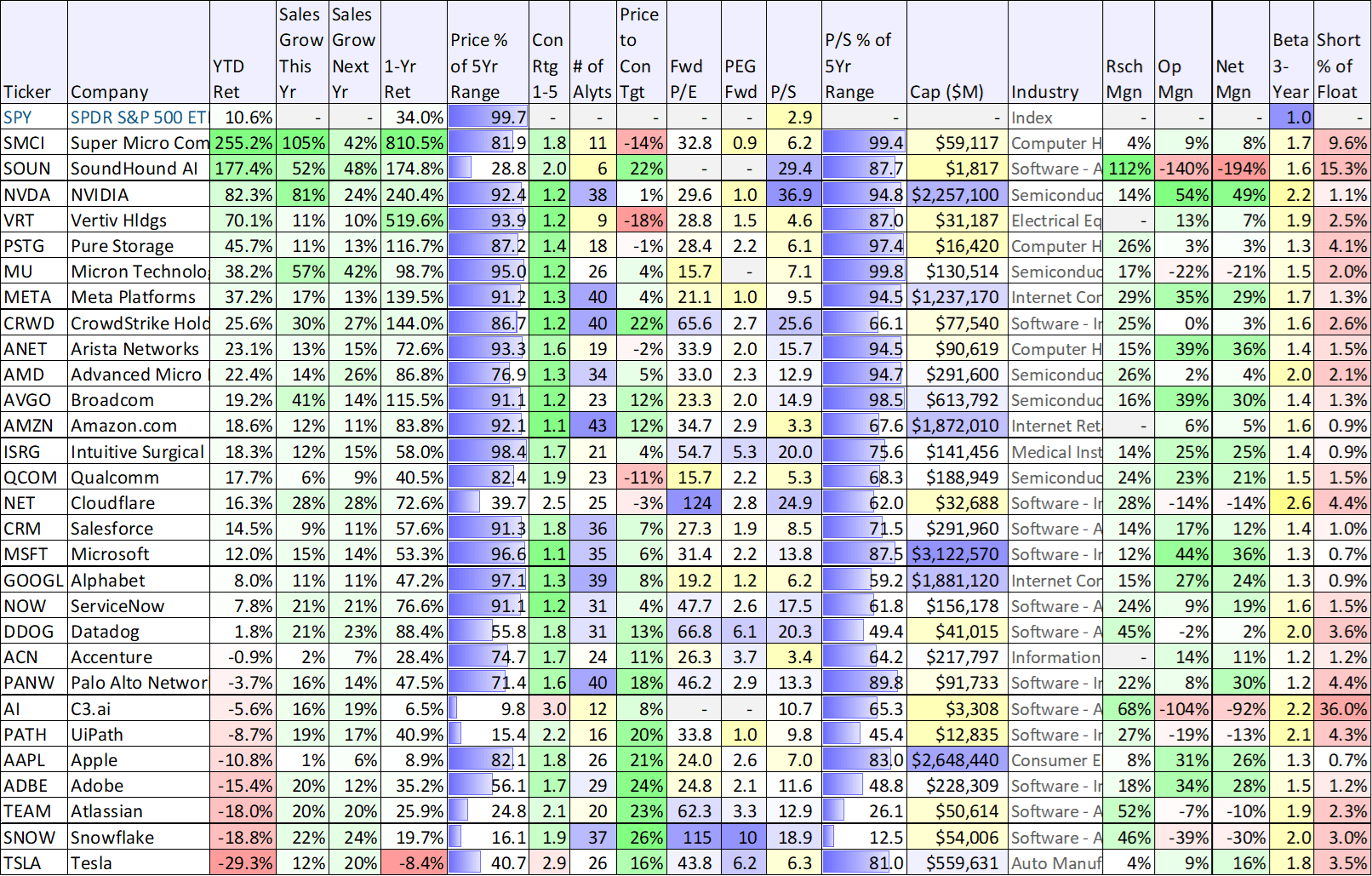

Critically important to Snowflake as an investment theme (i.e., megatrend), you can see an estimate (below) of just how large the AI market is expected to grow by the end of the decade.

Statista

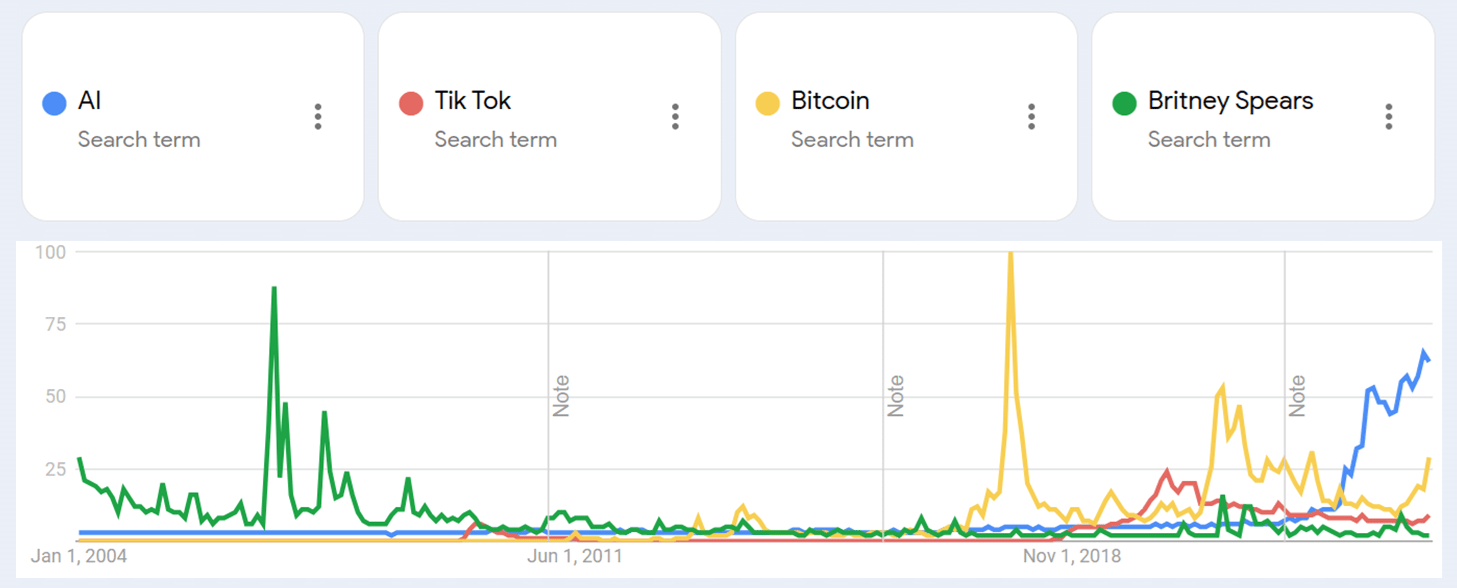

And for a little more perspective, here is a look at how the term “AI” has been climbing recently among Google searches (and as compared to a few historical search terms). AI is clearly increasingly a “hot” search term.

Google

In our view, AI is a much bigger deal than the other comparative search terms in the chart above.

And for more perspective, here is what Nvidia (NVDA) CEO Jensen Huang had to say about it at a Microsoft (MSFT) Ignite conference in November 2023:

“Generative AI is the single most significant platform transition in computing history… In the last 40 years, nothing has been this big. It’s bigger than PC, it’s bigger than mobile, and it’s gonna be bigger than the internet, by far.”

So with that backdrop in mind, let’s get into more detail on one very big player in the AI race, Snowflake.

Snowflake:

Snowflake![]()

Snowflake is a “big data” company, and without big data, the explosive growth in AI (that the market has been experiencing) would not be possible.

However, for all the hype surrounding this big-data cloud company, the shares have been a bust. Revenues continue to scream higher (see our table above), but profits scream lower and CEO Frank Slootman has just “stepped aside” (he’s now Chairman) to allow relative company newcomer (and AI expert) Sridhar Ramaswamy to take the reigns as the new CEO. The big question is whether Snowflake is a victim of unachievably high expectations or a disruptive megatrend beneficiary trading at an increasingly compelling price.

Overview:

Snowflake pioneered the data cloud where organizations unite their siloed data to achieve better and faster results. And with the explosion in data (courtesy of the digital revolution, and now ramping even faster thanks to AI) Snowflake addresses very real challenges and its sales are growing rapidly.

Snowflake Investor Presentation

However, as mentioned, profits are non-existent at this stage as the company focuses instead on its long-term growth vision.

Snowflake’s Value Proposition

There are two main reasons why Snowflake has a unique opportunity, and incredible potential, among the wave of burgeoning AI businesses. First, it’s the only multicloud data offering of its kind available on Amazon Web Services, Microsoft Azure, and Google Cloud. The “cloud agnostic” layer of Snowflake’s solution offers a huge advantage over everyone else in the market.

Second, Snowflake already has its platform in place thereby creating the potential for a wide moat ecosystem. For example, new CEO Sridhar Ramaswamy chose to lead Snowflake (versus many other opportunities he was offered), and this is how he explained why at the Morgan Stanley Technology conference in early March:

“Snowflake stood out in terms of a technology company that had the ability to create enormous value today with the products that we have with customers. It’s the existing opportunity, plus that ability to add on so much more.”

“It is a sort of platform mentality plus the ecosystem that is possible, plus the fact that it is an incredibly rich vein to be mined for many years to come. It’s really the culmination of all of these things that made me think that this was the place that I wanted to be spending many years.”

Concerning Forward Guidance:

Snowflake recently delivered healthy quarterly results but provided forward guidance significantly lower than expectations thereby causing the shares to fall sharply (and this comes on top of disappointing performance over the last year as the share price has dramatically underperformed, see data table above).

As a result, CEO Frank Slootman has been replaced (he is now the Chairmen) in favor of new CEO Sridhar Ramaswamy (who joined Snowflake in 2023 in connection with the company’s acquisition of Neeva, the world’s first AI-powered search engine, where he was Co-Founder and CEO).

On one hand, it’s very disappointing to see Snowflake shares dramatically underperform peers over the last year (especially as so many companies related to AI have soared), but on the other hand, it is good to see the company proactively addressing the issues before they get worse.

Essentially, Snowflake has been growing fast, but it has not been innovating and growing fast enough as compared to the AI opportunity. This is why the company has removed Slootman from day-to-day operations and brought in hard-nosed technologist, Ramaswamy. To drive more innovation and faster.

But to also get into the weeds a bit, Snowflake has “evolved” its forward guidance process (to reflect in 2024 similar macroeconomic headwinds as 2023) thereby delivering guidance below street expectations. Per CFO Mike Scarpelli on the quarterly call:

“We are forecasting increased revenue headwinds associated with product efficiency gains, tiered storage pricing and the expectation that some of our customers will leverage Iceberg Tables for their storage.”

Snowflake’s guidance is also conservative in that:

“We are not including potential revenue benefits from these initiatives [tiered storage pricing and Iceberg Tables] in our forecast.”

These assumption changes have impacted long-term guidance to a level lower than street expectations.

New CEO Sridhar Ramaswamy:

On the most recent quarterly call, new CEO Ramaswamy described Snowflake as a “once in a generation company” and explained:

“There’s no AI strategy without a data strategy. And this has opened a massive opportunity for Snowflake to address.”

This is encouraging as Ramaswamy has a history of success at Neeva and prior to that at Google, according to Snowflake’s website:

“prior to founding Neeva, Sridhar led Google’s Advertising business, which he helped grow from $1.5 billion to over $100 billion. During his 15 years at Google, he was responsible for all advertising and commerce products – search, display and video advertising, analytics, shopping, payments, and travel.”

It’s also encouraging because the company is making changes to address the massive market opportunities ahead (in data, especially related to AI), and Ramaswamy will hit the ground running (with his already strong history of introducing new products to address customer demands).

For example (according to Slootman on the quarterly call), since joining Snowflake (in a non-CEO role) in May 2023, Sridhar has already been:

leading Snowflake’s AI strategies, bringing new products and features to market at an incredible pace. He led the launch of Snowflake’s Cortex [for generative AI], Snowflake’s new fully-managed service that makes AI simple and secure.

Financially Speaking:

Snowflake is not profitable. In fact, its losses are growing. The company has a stated goal focused on revenue growth, not profits (to capitalize on the market opportunity), but at some point, Snowflake needs to move toward profitability.

And considering the company just guided for fiscal 2025 growth of around 22% versus consensus estimates of almost 30%, the company needs to start innovating value for customers faster.

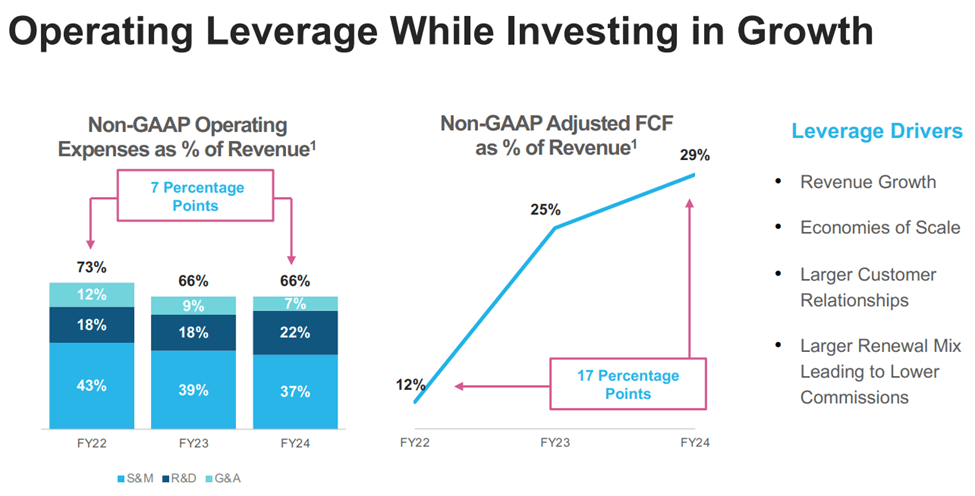

Snowflake is making small gains in margin improvements and cash flow generation, but it’s not enough as revenue growth slows and the valuation remains high (see the PEG ratio above (price/earnings to growth)). This is where new CEO Ramaswamy’s product innovation history will hopefully prove invaluable in reaccelerating Snowflake, especially considering the research margin (i.e., spending on research as a percent of revenues) is extremely high (see table above).

Snowflake Investor Presentation

Basically, Snowflake needs to start creating more value for customers through innovation and they need to do it faster (we’ll see if Ramaswamy can deliver).

Massive Market Opportunity:

As a reminder, Snowflake’s market opportunity is truly enormous. According to its website, the company’s vision is for its platform to be:

“the engine that powers and provides access to the Data Cloud, creating a solution for applications, collaboration, cybersecurity, data engineering, data lake, data science, data warehousing, and unistore. Snowflake’s vision is a world with unlimited access to governed data, so every organization can tackle the challenges and opportunities of today and reveal the possibilities of tomorrow.”

The amount of data in the world is enormous because everything is being digitized and moved to the cloud, and now artificial intelligence is driving even more data creation that can be used to develop solutions. AI needs a data solution, and Snowflake has a huge opportunity here. They are positioned better than almost everyone else to succeed in this area (based on what the company has accomplished already, see customer examples below).

Snowflake Investor Presentation Snowflake Investor Presentation

AI, and the great cloud migration, are a market megatrend that will last for many years, and now Snowflake needs to do a better job of capitalizing on it (they’ve been doing a good job, just not as good as expectations).

Valuation:

As mentioned, Snowflake is growing revenues rapidly, but so are the company’s net losses. For example, the price-to-sales ratio has come down from insanely high levels during the pandemic to around 18.9x now (still very high, but not as compared to where it was). And the company’s PEG ratio (price/earnings to growth) is the highest of any company in our earlier table (10x).

Encouragingly, Wall Street analysts continue to rate the shares a “buy” and believe they have 26% upside from here (more than many other AI stocks). Overall, Snowflake’s share price and valuation have come down, but they are still not “cheap” due to continuing high expectations for the business opportunity.

Risks:

- Data Security: One of the biggest risks that Snowflake faces is data security. The company basically has access to everyone’s data. Of course, Snowflake claims its platform allows users to share data securely and in a governed fashion, but any data breaches could create huge legal, financial, and reputational challenges.

- Innovation is also a risk, as mentioned. The new CEO needs to deliver more value-adding products and faster.

- Competition is also a risk. For example, new multicloud data solutions could emerge to compete. Or, large cloud providers (such as Amazon Web Services, Google Cloud, and Microsoft Azure) could adopt their own multicloud solutions thereby creating new competition. Also, Databricks presents a unique source of competition.

Snowflake Versus Databricks:

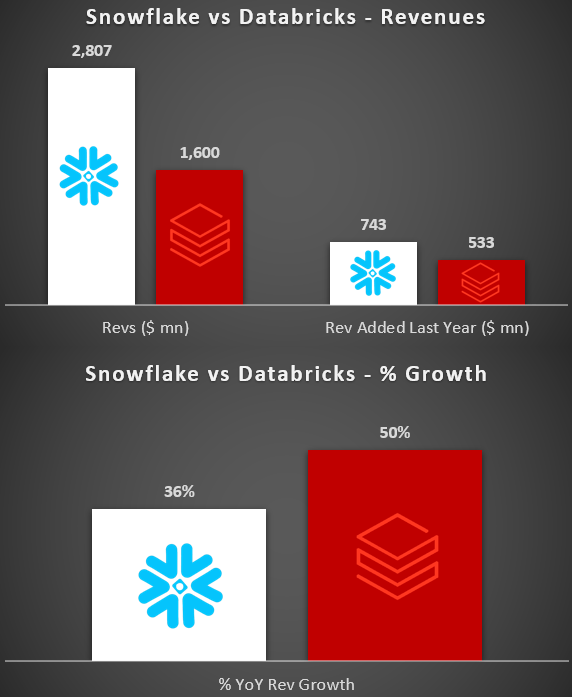

Databricks presents a unique risk for Snowflake, especially related to AI. For example, users increasingly argue Databricks (private company) is able to better handle larger data workloads, on its one platform, thereby making it better to handle AI (whereas Snowflake machine learning capabilities are only available through add-on tools like Snowpark). For perspective, here is a look at revenue growth for Snowflake versus competitor, Databricks.

(source: X (@techfund1))

The Bottom Line

There have been plenty of highly successful companies that were first unprofitable for many years (Amazon is a great example). Snowflake is currently very unprofitable, but it’s also growing revenues fast. Unfortunately, the company is not growing revenues as fast as Wall Street expects and the shares are down big.

And despite recent declines, the shares are still not “cheap” on a valuation basis. This makes sense because the opportunities that lie ahead (big data, cloud, AI) are so great (and the company is still relatively young in its “j-curve” journey). At this point, it just comes down to execution.

We appreciate the company proactively inserted Ramaswamy as the new CEO instead of sticking with the wrong guy for the job for too many years (Slootman seems great, it’s just he doesn’t have the strong AI development background that Ramaswamy does). And the company’s latest revenue growth guide (which came in below Street expectations) may have intentionally set the bar low making it easier for the new CEO to excel. Time will tell if Ramaswamy is able to accelerate the company’s value execution.

As disciplined long-term investors, we’re willing to take the risk. The opportunity presented by the digital revolution, the cloud, and now AI is truly enormous, and patient long-term Snowflake shareholders stand to benefit, perhaps handsomely, over the long term. Time will tell. Long Snowflake.

Analyst’s Disclosure: I/we have a beneficial long position in the shares of SNOW either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.

–

If you are looking for income investment ideas, consider Big Dividend PLUS where you’ll get instant access to our High Income NOW Portfolio (28 holdings, 9.8% current yield). Be sure to take advantage of our Easter Sale.