Summary:

- Despite Tesla’s popularity among investors and electric vehicle fans, a detailed understanding of the business is crucial.

- Analyzing the business, we see that beyond all the potential products and services, it is a carmaker at heart.

- There is a huge future potential in autonomous vehicles and the introduction of robotaxis, but these innovations are still a long way off.

- Tesla’s core business is struggling with its Chinese competitors, and fundamentals are deteriorating, making the company uninvestable for now.

Richard Drury

Investment Thesis

For a long time, Tesla (NASDAQ:TSLA) has dominated the electric vehicle market. Under the leadership of Elon Musk, the company has invested a lot of money into technologies like self-driving cars, which has paid off in vehicle sales. In the Western Hemisphere, Tesla is still the biggest electric vehicle seller.

However, this dominance is now being questioned. Chinese carmakers entered the electric vehicle market, and despite the initial wary of the European customers, their relative cheapness makes them very attractive. These are not low-quality cars, either. Tesla was forced to slash prices to compete, and things are looking tough for the business.

Tesla still has the potential to continue growing, especially through new ventures like licensing its FSD technology and the “robotaxis” that will be introduced in August this year. However, as I’ll explain further in this article, these ventures seem well off in the future, and it will take some time until these are profit-generating. I think these ventures are not discounted enough by the market.

Despite the current struggles, I rate Tesla a “Hold”, because of its potential future. I think it is difficult to get the timing of these future earnings right, which does not give us enough margin of error to have conviction in buying or selling.

Introduction

News is full of stories about Tesla’s downturn and how Elon Musk is failing with its electric vehicle business. I believe most people have an incorrect perception of the company. Therefore, before the company’s earnings this month, I wanted to analyze how the company really earns money, and if what those news stories say is true.

Even though investors (including me) may say they know the business, I still wanted to start with a company description. I think it is very important to get it right. We’ll talk about how the company prospered after 2019, and what caused the decline in the last two years.

I will also mention some of the new products and services Tesla is expected to introduce in the future, and how they affect today less than people think. Let’s get right into it.

Company Description

While many people would think there is no need to introduce Tesla, I think understanding the business correctly is essential. The company is often celebrated as a “pioneer in autonomous vehicles”, “future licensor of all electric vehicles”, or even a “pioneer in the clean energy transition”. These may or may not be true. I’ll define it as what it really is today. At its core, Tesla is a high-quality manufacturer of fully electric vehicles with little exposure to energy generation and storage.

The electric vehicle business requires little introduction. Tesla manufactures five different consumer vehicles, including models 3, Y, S, X, and most recently, Cybertruck. These target different customer segments. For example, while Model 3 is a four-door mid-size sedan that might be suitable for families, Cybertruck is a full-size electric pickup truck that has a stainless steel exterior.

The company makes money from direct sales of vehicles, as well as used vehicle sales, public charging at Tesla Superchargers, and in-vehicle (or in-app) upgrades. Additionally, like many other car companies, Tesla provides purchase financing and insurance to its customers.

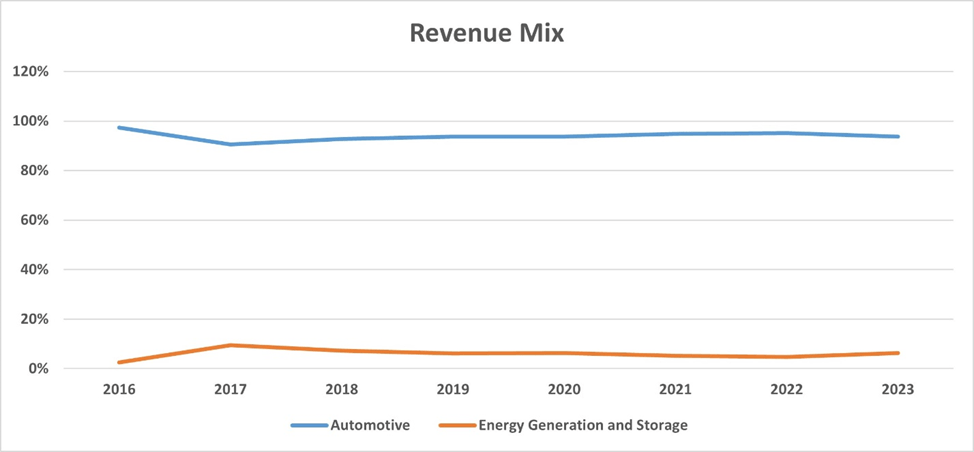

Tesla’s second business area, Energy Generation and Storage, focuses on creating lithium-ion battery storage solutions for homes and businesses. They also offer retrofit solar energy systems, including their innovative Solar Roof.

Despite the considerable attention this segment receives in the media, it contributes a minor share to the overall revenue. 94% of the revenue mix is related to the automotive segment.

Understanding the following charts and how Tesla makes money is crucial for the rest of this article. Tesla is an electric car company that has helped (and still helps) the industry transition into cleaner – though not entirely clean – energy.

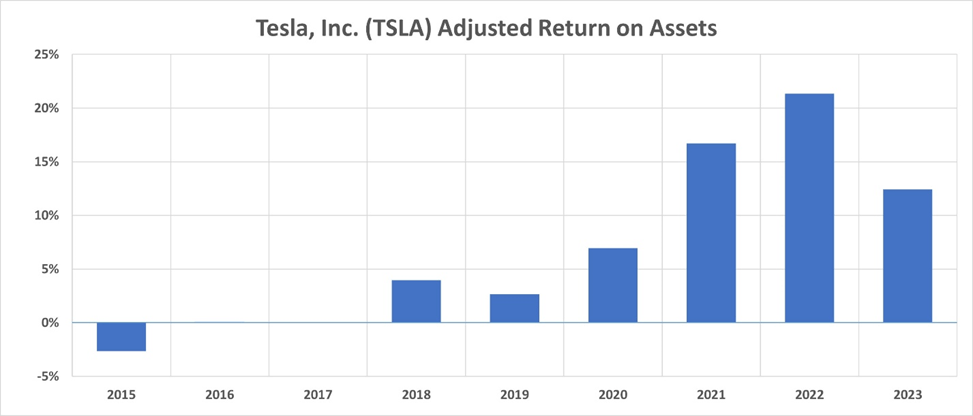

S&P Capital IQ

Tesla really took off after 2019. In 2015, based on adjusted return on assets [ROA] figures, it was still unprofitable. The launch of the Model X at the end of that year marked a turning point, bringing Tesla’s profitability above zero, although it wasn’t yet making money. The introduction of Model 3 in 2017, a more affordable model compared to previous ones, seems to be the catalyst that made Tesla turn profitable.

Throughout the years, and especially after 2019, Tesla’s adjusted ROA surged higher and reached 21% in 2022.

S&P Capital IQ – Author

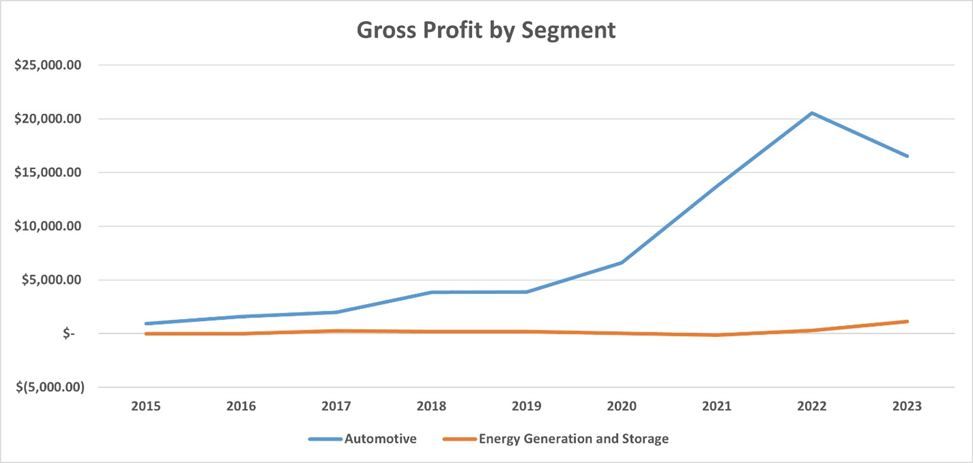

This success was mainly driven by its EV sales and margins. A look at the gross profit by segment chart below shows how gross profit started rising after 2019. This was what made ROA, and also the stock price jump. With expectations of higher profits, the stock increased from $22 in January 2019 to $407 in November 2021.

S&P Capital IQ

Now, let’s delve into the reasons for the profitability decline in 2023 and what the future holds for Tesla.

Tesla’s Dominance over the EV Market Is Beginning To Wane

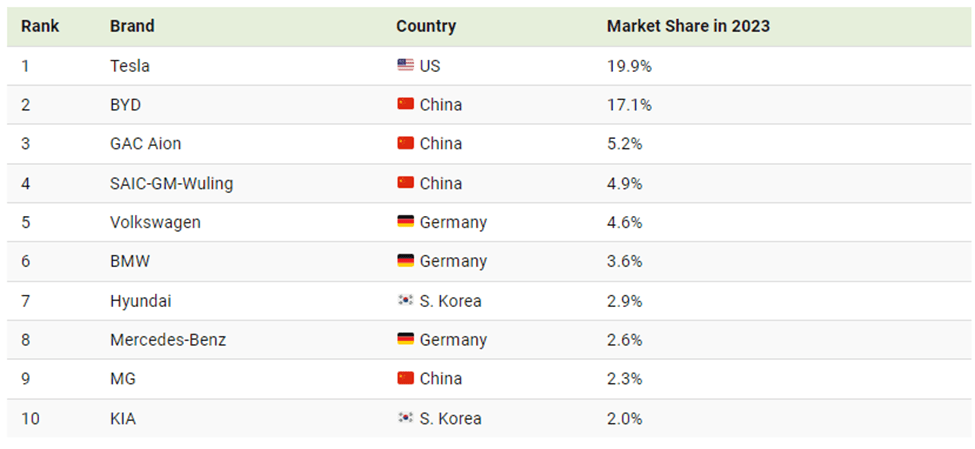

Electric vehicles have a history that dates back to the early days of automotive development, but it was Tesla’s production of the Roadster in the 21st century that set a new standard for what electric cars could be. This is a great example showing how crucial Tesla’s position in the EV market has been so far. Although many brands introduced different models, Tesla protected its position thanks to its advanced technology. As of 2023, Tesla remained the top electric car seller, capturing nearly 20% of the market share.

visualcapitalist.com

Investors are starting to be concerned about the company’s leading position in the market, as Chinese competitors are rising. In terms of the number of cars produced, BYD (OTCPK:BYDDF) has already surpassed Tesla. And to make matters worse, Chinese cars are, in general, cheaper. That is why Tesla slashed prices, causing the massive margin decline seen above. So far, this has been limited in Asia.

Now, Chinese cars are slowly making their way into Europe. While Europeans are more familiar with Tesla and may be wary of Chinese brands initially, I expect this bias to not last long. As Chinese electric cars become more competitive in terms of technology and prices in Europe, Tesla will suffer in the region.

This surge of the Chinese EV industry is also recognized by auto executives in Europe BMW’s CEO called it an imminent risk to Europe’s auto industry. There is a chance that Europe will impose extra tariffs on Chinese electric cars to protect Western brands, but that is not certain and may cause “unintended consequences”.

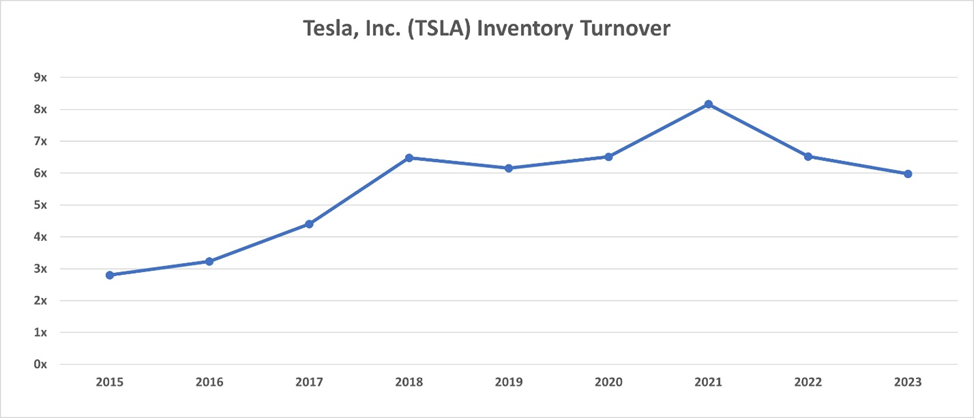

This competition is not only hurting pricing but unit sales in general. The inventory turnover in 2023 was at its lowest level since 2017.

S&P Capital IQ

Regardless of which way this story goes, it is clear that Tesla faces a lot more competition than it faced in the last decade, and it is hurting margins.

What Tesla Can Become Is A Different Question

Based on my personal observations, especially from social media discussions there’s a tendency to focus more on Tesla’s potential future rather than its current state. This speculative outlook is intriguing for several reasons.

Firstly, the dream among electric vehicle enthusiasts is a full transition to EVs, eventually leading to the widespread adoption of autonomous or self-driving vehicles. Tesla’s advancements in self-driving technology, including its Full Self-Driving [FSD] capabilities, are genuinely exciting. I believe the company can turn this expertise into a competitive advantage in the future.

Elon Musk has also talked about licensing their FSD technology to other car companies. This would be a huge transformational change in Tesla’s operating model, and if autonomous cars are fully adopted in the future, licensing revenue can surpass car sales.

Additionally, Tesla is expected to unveil “Robotaxi” on August 8. Tesla initially mentioned robotaxis back in 2019 and expected them to start operating in 2020. This prediction was off by half a decade, but it seems like the company is finally going ahead with the project. The introduction of robotaxis is eagerly anticipated, though regulatory hurdles will likely delay their presence on the streets on roads.

The challenge with these futuristic visions is their very long-term nature. Tesla’s technology may be developing fast, but it will take time for regulation to keep up with it. Immediate visions of driverless taxis and FSD licenses are still a way off.

The market used to price in these potential products and services into the stock price, which are now being discounted more appropriately as the stock price falls.

Upcoming Earnings Call

Tesla has its Q1 2024 earnings call on April 23, 2024. Wall Street analysts are expecting revenue of nearly $23 billion and net income of $1.6 billion. Compared to the same quarter one year ago, this would mean slightly lower revenue and significantly lower net income.

The upcoming earnings discussion will be particularly significant, as shareholders are keen to understand management’s perspective on increasing competition, production volumes, and future margin expectations. Additionally, there might be some remarks regarding the robotaxi initiative that is going to be introduced in August.

For investors, the focus remains sharply on profitability metrics. Even if Q1 margins don’t show any improvement, management’s comments about if and when they expect profitability to recover are going to be crucial. Lower-than-expected production numbers and negative margins outlook may drive the share price even lower.

I believe due to the recent majority of negative news, management will try to paint a positive picture of Tesla’s competitiveness in Europe and new technologies like robotaxis. However, news I am hearing suggests that it will be difficult to do so. I expect lower-than-expected unit sales in Europe and Asia, and lower inventory turnover going forward, which would strengthen my case to call this name a “stay away” investment.

Despite All The Negative News, It’s Not Looking Cheap

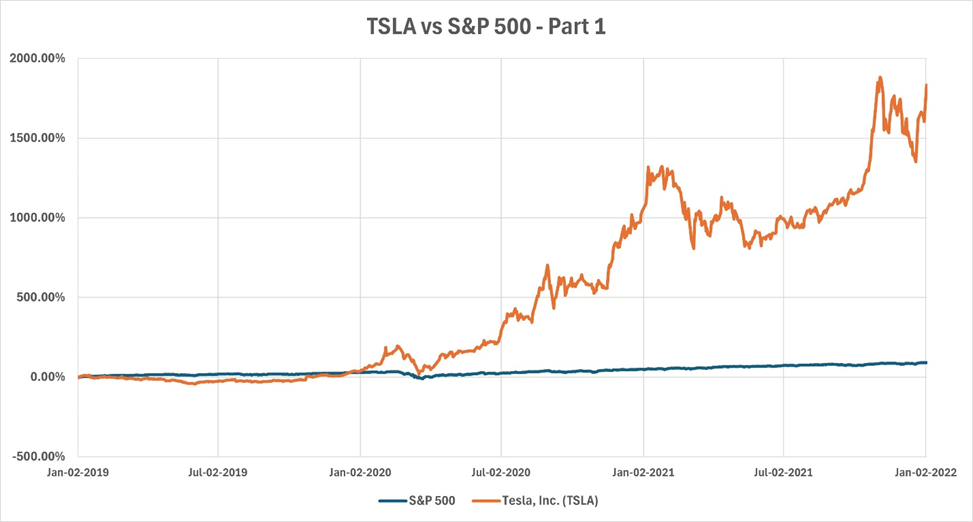

The story I told above about how Tesla took off and became immensely more successful after 2019 can be observed by looking at the stock. See it below. The surge of the Tesla stock makes the jump of the S&P 500 index look insignificant, which actually nearly doubled in three years from the beginning of 2019 to the end of 2021.

S&P Capital IQ

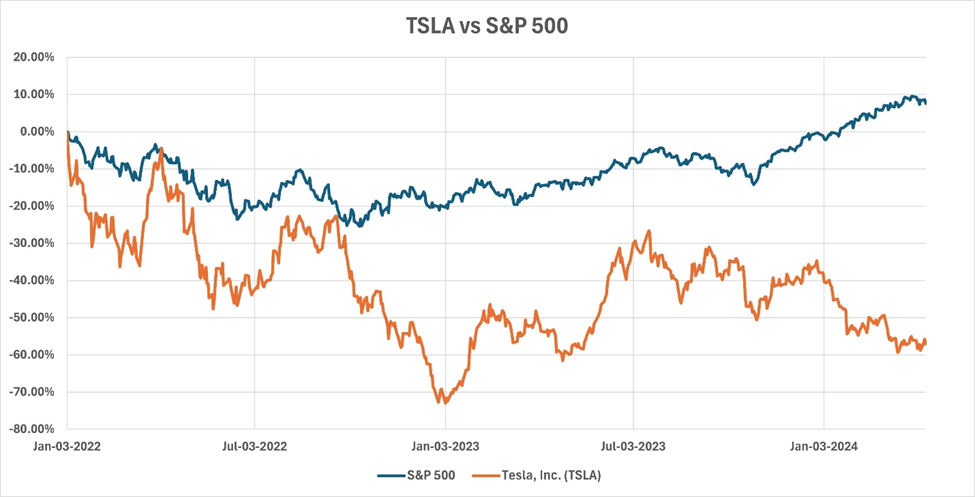

At the end of 2021, Tesla was seen as a very high-growth company, not as a traditional car manufacturer. And this made sense, to some extent. However, indications of the company struggling to grow as much began in 2022. Until now, Tesla investors have been hit with mostly negative news. In 2022, the stock was down nearly 70%. While it recovered a bit in 2023, investors holding the stock since 2022 are still in the red.

S&P Capital IQ

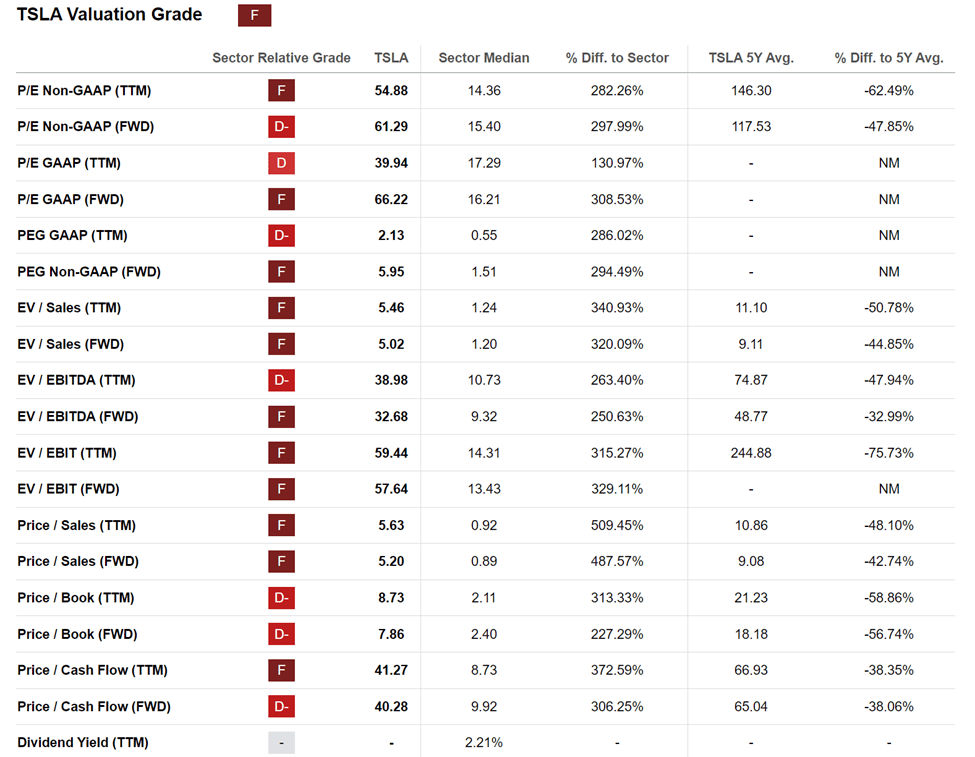

One could think that after this huge decline, the stock is now cheap. However, by various measures, it still looks expensive. Find below Seeking Alpha’s valuation grades based on different multiples, which have never been better than a D since 2021. A comparison of Tesla’s multiples to the sector median shows that the market still prices Tesla as a high-technology growth company rather than a car manufacturer, which is what it really is.

Seeking Alpha – TSLA Valuation

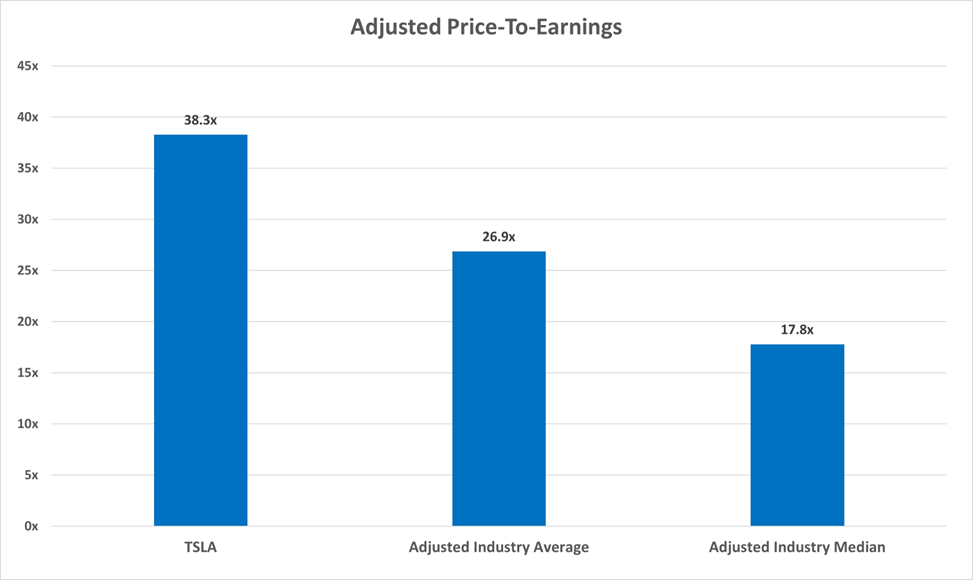

More specifically, a comparison of Tesla’s adjusted price-to-earnings (P/E) ratio against that of the global car industry—including both primarily electric vehicle manufacturers and traditional automakers like Ford (F) and General Motors (GM) —highlights Tesla’s significant overvaluation. While Tesla’s robust balance sheet and promising future justify its trading at higher multiples to some extent, I think we are going to see this difference in multiples decline as growth expectations are cut.

Currently, Tesla’s valuation is nearly double that of the median for the global car industry.

S&P Capital IQ – Author

Regardless of the current stock price and fair value of the stock, as the market sees Tesla more like a car maker and less like a technology giant building the future, I think valuations will drop. We need to see improving fundamentals and more tangible steps regarding the commercialization of new technologies for this company to be a buy.

Final Thoughts

Tesla is a very high-quality company. It is widely accepted as the pioneer in electric vehicles, and it is expected to continue this leadership in autonomous vehicles. However, the company faces strong headwinds that cause the fundamentals of the automotive business to deteriorate.

The rise of competition from China cannot be ignored and the expansion of Chinese electric vehicles into Europe needs to be tracked. But regardless, Tesla struggles not only with declining margins but also with pressures on inventory turnover.

Selling cars is the core business and will be for a longer time than the market thinks. As this business loses its competitive advantage, Tesla becomes uninvestable. There is a chance I am not accounting for potential products and services and earnings they will generate. However, in my opinion, any significant contributions from these innovations are on a distant horizon.

If I see an indication of car sales profitability recovering or the business model changing in the near future and the profit mix shifting towards new technologies, there might be an argument to be made to invest in this business.

Despite the current challenges, considering the potential for Tesla to launch new, profit-generating products and services over time, I assign a “Hold” rating to the company.

Analyst’s Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.