Summary:

- Microsoft’s AI-driven platform, Copilot, is expected to drive significant revenue growth and redefine enterprise productivity.

- Recent updates to Copilot, including automation of routine tasks and sophisticated coding capabilities, show Microsoft’s commitment to integrating AI across multiple disciplines.

- Analysts project that Copilot could generate approximately $10 billion in annual revenue by 2026, indicating strong market confidence in Microsoft’s AI strategies.

jewhyte

Investment Thesis

Heading into FY Q3 Earnings, I believe Microsoft’s (NASDAQ:MSFT) strategic bet with their development and integration of the AI-driven platform, Copilot, has positioned the company well for the quarterly call and in terms of driving business going forward.

Microsoft Copilot, launched in late 2022, has quickly become a key tool within Microsoft’s suite both for software engineers (through GitHub) and non-coding tasks as well.

I believe recent analysis shows that the market for Copilot is massive, with some projections suggesting the tool could help Microsoft generate approximately $10 billion in annual revenue by 2026, assuming an 18% adoption rate among targeted users (keep in mind this tool was not launched until November 1st last year). So in just 3 short years, getting to $10 billion in revenue is incredible.

With this, I believe the potential revenue shows the scale Microsoft is thinking at: they really aim to deploy their AI tools across multiple disciplines and verticals for people who use their current offerings, reflecting both the market’s vast capacity for AI integration and Microsoft’s ability to capture significant market share.

While I have not written since before the FY Q2 earnings report over the winter, I remain bullish on Microsoft, seeing Copilot and its broader AI strategy as core pillars for growth. I believe Microsoft stock is a strong buy heading into the call on the 25th.

Why I Am Doing Follow-Up Coverage

In January, I wrote about Microsoft’s pursuits in the Gaming sphere and how these are under-appreciated. Copilot (while much more widely known) I believe offers a similar upside for the company and incredible productivity growth for its users.

Fiscal Q3 earnings are set to come out on April 25th, after the bell. With this, I wanted to do a follow-up to show how Copilot is continuing to get better and why argue (before the quarterly report) why this quarter may be key to the Copilot story to the bottom line.

Microsoft’s latest enhancements to Copilot are poised to redefine enterprise productivity beyond helping users code simple functions using GitHub or write better research inside Microsoft Word.

Recent key updates include automation of routine tasks like sending and tracking invoices and sophisticated coding capabilities that allow developers to refactor and optimize code automatically within their applications. I believe these advancements are designed to streamline operations significantly outside just the world of Microsoft Office. These are automations that can impact departments like accounting, which while they likely use Microsoft Excel, use other software right now for tracking and sending invoices (think Quickbooks – not a Microsoft product).

To me, these new capabilities are part of Microsoft’s broader strategy to embed more sophisticated AI-driven functionalities into its suite of products. With this, I believe the upcoming company-wide build developer conference in May is expected to be a platform for unveiling these features (and more).

Background On Copilot

Introduced on September 21st last year, Copilot quickly became a core feature for enterprise users with over 300 seats in November when it launched (November 1st).

The tool’s robust adoption reflects the strong demand, and perceived value among large organizations (since they rolled this out for companies that have over 300 seats). I imagine small businesses will benefit immensely as well, but their usage hasn’t yet jumped the same way large enterprises have.

Piper Sandler analysts have projected that Copilot could generate about $10 billion in revenue by 2026, assuming an 18% adoption rate among eligible users.

I even think this projection may indeed be conservative given Copilot’s integration across Microsoft’s extensive software ecosystem (on top of small business and personal adoption, which we really haven’t seen yet).

For instance, Copilot now aids in automating tasks ranging from data analysis to content generation directly within user workflows in Microsoft 365. Small businesses cannot afford to hire data entry analysts or copy editors. AI will provide a huge lift to them.

With the tool priced at $30 per user per month, I believe Microsoft has aligned Copilot’s capabilities with a price point that most users can afford, especially when they think about the productivity gains it will provide.

The enthusiasm around Copilot is also reflected in the customer research. Analysts at Jefferies noted that thousands of organizations were in the queue for its general availability launch.

When this tool was launched in November, there was only 2/3rds of the quarter available for Microsoft to begin to ship this out to customers. I am really excited to see how this tool performed in their FY Q3 (normal Q1) given the full 13 weeks of time to get this in users’ hands.

FY Q3 Expectations

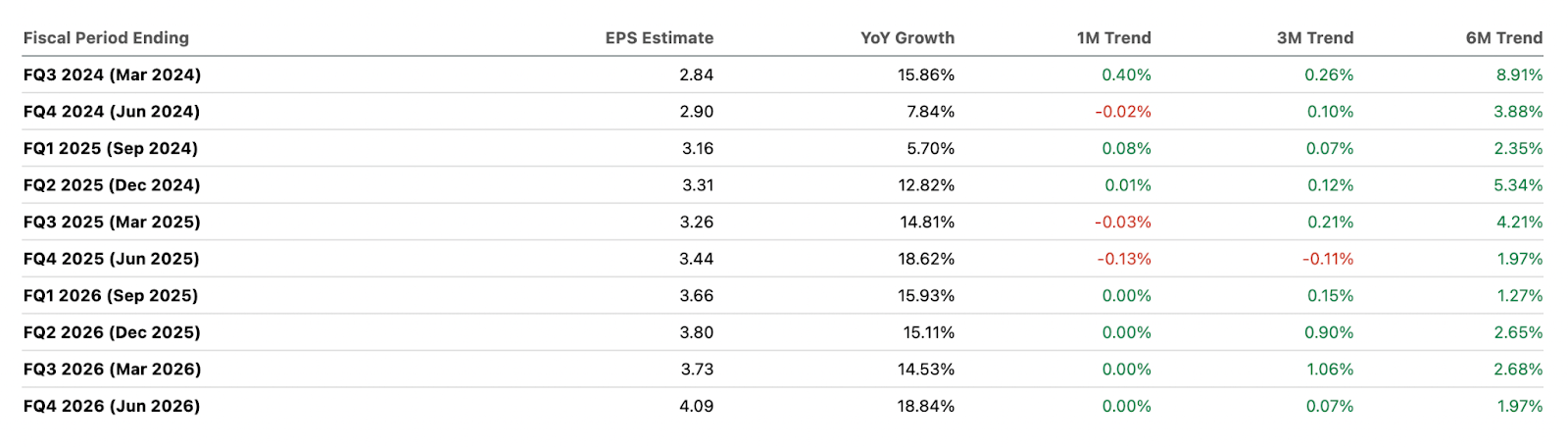

For the upcoming FY Q3 earnings, I will admit expectations are fairly high, driven by upward revisions by sell-side analysts in the EPS forecasts. If Microsoft hits these numbers (and I think they will in part due to Copilot) the EPS estimates suggest a strong performance boost.

Analysts are projecting a consensus EPS (Earnings Per Share) of $2.84, which marks solid year-over-year growth of approximately 15.86%. With this, revenue expectations are robust, with consensus estimates predicting revenues to reach $60.85 billion, reflecting a growth of 15.12% compared to the previous year.

What I Am Looking For On The Call

For me, I started with the last earnings call to set expectations for this one. In the last earnings call, Copilot was a big part of the story and was highlighted 52 times.

Last quarter, the company had powerful testaments to how Copilot was being rapidly adopted:

GitHub revenue accelerated to over 40% year-over-year, driven by all-up platform growth and adoption of GitHub Copilot, the world’s most widely deployed AI developer tool. We now have over 1.3 million paid GitHub Copilot subscribers, up 30% quarter-over-quarter – FY Q2 Call

On top of this, the enterprise adoption we saw just in Q4 was powerful:

[Copilot] is already being used by over 10,000 organizations including An Post, Holland America, PG&E. – FY Q2 2024 Call

So for me, seeing how these figures have updated since the last call is a must. I’ll be focusing not on whether the mentions of Copilot have increased since the last quarter but more on use cases for how people are leveraging these powerful tools. Last call management briefly mentioned how Copilot is “expanding [its] TAM by integrating Copilot into third-party systems too.” I am going to pay close attention to how they are doing this. We already know Copilot is now being used in places like invoice tracking, more qualitative data like this will be essential for me.

With this, I am particularly interested in obtaining specific figures related to the adoption of Copilot (much like how they did last quarter). For me, this includes the number of Copilot seats or licenses sold, which will provide a clearer picture of its market penetration.

An added bonus will be if management breaks out the actual revenue they are receiving from Copilot (run rate at the end of the quarter). I think the number may shock some analysts. For example, we already know that there are 1.3 million GitHub Copilot Subscribers. If we take an average blended monthly cost of $18/month (enterprise is higher at $39/seat/month) we get an ARR from Copilot of over $250 million per annum already. I think the estimates for $10 billion in revenue by 2026 are more than doable. They may be conservative. These results are heavily skewed below the enterprise costs per seat and do not include any Microsoft Office Copilot Features.

Valuation

Currently, Microsoft stock trades at a 30% premium compared to its sector, but I believe the stock justifies this premium with a gross margin approximately 49% above the sector median. The company’s current non-GAAP forward P/E is 35.33, while the sector median is 27.02. The company’s current gross margins sit at a staggering 69.81%, far above the sector median of 48.95%.

Although the forward P/E ratio may seem high, especially given the high-interest rate environment we live in, I really think investors need to focus on the robust growth we have seen so far from Copilot, plus what Copilot has in store going forward. I think Copilot is set to outperform expectations.

If the company outperforms this earnings season, I anticipate a 10-15% stock price increase, especially if forward P/E ratios adjust to 45-50% above the sector median from the current 30% premium above the sector median, reflecting Microsoft’s strong product offerings.

How This Compares To My Previous Earnings Estimates

When I wrote about Microsoft’s gaming division in January, I discussed how Microsoft’s gaming sector might boost the company’s market cap by up to approximately 14% given stronger penetration in the industry given the Activision deal has now closed. On the last earnings call, management noted that “Activision contributed approximately 4 points to revenue growth…”

Since then, the stock has risen by about 4%. Including the potential 10-15% stock price uplift from Copilot, I think there is strong upside potential in the stock. However, I am merging my remaining upside potential from Gaming (10% upside) with the Copilot upside I think is available. I think this now makes my upside estimates conservative, given it gives the stock multiple catalysts/avenues to leverage to push the shares higher.

Risks Going Into Earnings

For me, going into the earnings call, the biggest risk I see is expectations. Expectations for Microsoft are fairly high this quarter, given the notable analyst revisions over the past six months.

Analysts have increased their EPS estimates by 8.91% during this period, reflecting a strong optimism surrounding Microsoft’s performance, particularly in areas like AI with products such as Copilot. These are the highest upward revisions analysts have penciled in for any quarter over the next 3 fiscal years (including the current fiscal year).

Microsoft Earnings Estimate Revisions (Seeking Alpha)

While the expectations are buoyed by these positive revisions, they obviously also pose a risk. If Microsoft fails to meet these heightened expectations, especially related to Copilot, it could lead to the company’s stock re-rating lower.

However, I’m optimistic and I think this will not happen. The long-term outlook remains positive, underpinned by the transformative potential of what Copilot can do for people in industries like programming to accounting. These are the real areas which are expected to drive future growth and efficiency.

Bottom Line

Going into Microsoft’s fiscal Q3 earnings, all eyes are on Copilot, its flagship AI tool, which I believe is further expected to redefine enterprise productivity. This earnings report is crucial, as it will reveal the extent of Copilot’s integration and its contribution to Microsoft’s revenue. Analysts remain optimistic, projecting substantial growth spurred by AI capabilities, with Copilot potentially driving around $10 billion in revenue by 2026.

The high expectations, buoyed by a significant 8.91% increase in EPS estimates over the last six months, indicate strong market confidence in Microsoft’s AI strategies, in my opinion, not overoptimism. Overall, I think the stock remains a strong buy. I’m looking forward to seeing how Microsoft reports.

Analyst’s Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Noah Cox (account author) is the Managing partner of Noah’s Arc Capital Management. His views in this article are not necessarily reflective of the firms. Nothing contained in this note is intended as investment advice. It is solely for informational purposes. Invest at your own risk.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.