Summary:

- Exxon Mobil Corporation will report its first-quarter earnings with a predicted decline in revenues of 7% compared to the previous year.

- Exxon has a mixed track record of beating revenue estimates, but a better track record of beating earnings per share estimates.

- XOM’s shareholder yield is lacking compared to its peers, suggesting potential for increased shareholder returns.

zodebala

Article Thesis

Exxon Mobil Corporation (NYSE:XOM) will report its first-quarter earnings results on Friday (April 26th). In this article, we will take a look at what investors can expect from the upcoming earnings report, while also delving into the longer-term outlook for Exxon Mobil.

Past Coverage

I have covered Exxon Mobil Corporation in the past, most recently in October 2023. In that article, I asked whether Exxon Mobil would acquire Pioneer Natural Resources (PXD). And, indeed, Exxon Mobil announced a takeover of Pioneer later that month. I gave Exxon Mobil a neutral rating back then, with shares of the company having risen by 15% since. But since the broad market (S&P 500 (SPY)) has risen by 15% as well, the neutral rating worked out fine, as Exxon Mobil delivered an in-line return relative to other equities.

Upcoming Quarterly Earnings From Exxon Mobil

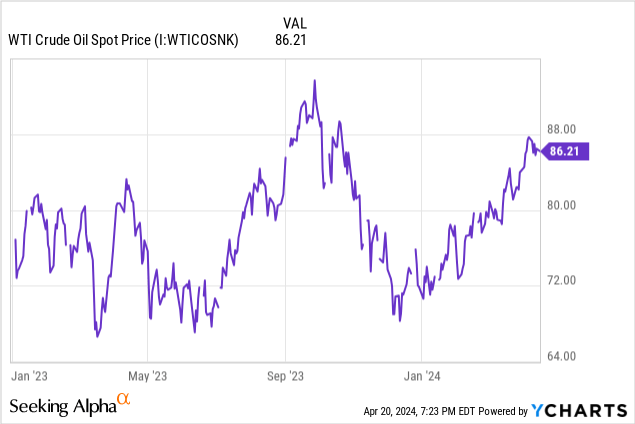

Exxon Mobil Corporation will report its first-quarter earnings results on Friday before the market opens. The analyst community is forecasting that the supermajor will report revenues of $81 billion for the January to March period. This would represent a decline of 7% compared to the previous year’s period. Looking at how oil prices have changed in that time frame, we see the following:

Oil prices, for WTI, have started into 2023 at around $75. They started into 2024 at around $70, thus a little lower. While oil prices improved considerably in 2024 so far, the first quarter wasn’t especially strong from an average price perspective. 2023 had a better first quarter, although oil prices declined during the second quarter, whereas crude oil rose during this year’s second quarter — at least so far. It thus makes sense to assume that Q1 of 2024 was weaker than Q1 of 2023 for most oil producers. The good news is that Q2 2024 oil prices are looking better than Q2 2023 oil prices, thus Exxon Mobil and its peers should be able to report positive year-over-year results during the second quarter — that is also what the analyst community is expecting.

When looking at the consensus estimate from Wall Street analysts, we should also consider how Exxon Mobil has fared versus estimates in the past. Over the last 12 quarters, Exxon Mobil has beaten revenue estimates 8 times. Unfortunately, the last four quarters saw the company miss revenue estimates. At least in the very recent past, Exxon Mobil thus does not have a strong track record when it comes to outperforming Wall Street’s expectations — which might give an indication that another revenue miss is somewhat likely.

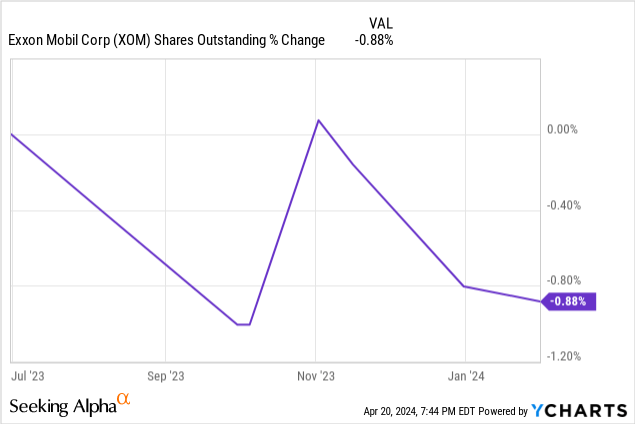

Wall Street analysts have a consensus earnings per share estimate of $2.17 for the first quarter, which would be down a pretty sizeable 23% from the profits that the company generated during the previous year’s first quarter. When it comes to beating earnings per share estimates, Exxon Mobil has a better track record compared to beating revenue estimates — the supermajor beat earnings per share estimates in 9 out of the last 12 quarters, including two out of the last four quarters. Still, a sizeable earnings decline seems likely, as lower revenues hurt profitability, all else equal. Operating leverage works against the company when revenues decline, which helps explain why profits are forecasted to pull back more meaningfully compared to revenues. While Exxon Mobil has been buying back shares in the past, its buyback pace was not overly high, as we can see in the following chart:

According to YCharts’ data, Exxon Mobil’s share count declined by just 1% over the last year and by 6% over the last three years — which isn’t enough to make a large impact when it comes to boosting earnings per share on an annual basis. If Exxon Mobil keeps buying back shares consistently, the impact will eventually be large, but a 1% reduction over the last year is not good enough to make up for the profit headwinds from lower revenues and operating leverage working against the company. Competitors with higher buyback paces, such as BP (BP) or Shell (SHEL), which have reduced their share count by 5% and 6% over the last year, respectively, are seeing a much bigger earnings per share tailwind.

What’s The Outlook For Exxon Mobil?

While the company’s reported results for the first quarter will be important, the company’s comments about the foreseeable future will be important for shareholders as well. This includes the pending acquisition of Pioneer — investors should look for clues about the timeline of this acquisition when management presents the company’s results. It is likely that acquisition-related questions will be part of the earnings call.

While the acquisition of Pioneer Natural Resources comes at a hefty price tag of $60 billion, this is an all-stock deal. Exxon Mobil will thus not have to issue any new debt to pay for the takeover, and it won’t have to access its cash pile, either. With Exxon Mobil ending the fourth quarter of 2023 with $32 billion in cash and equivalents, the company has significant spending power even following the acquisition of Pioneer. In the upcoming earnings call, management might give us some more hints about plans to utilize this cash going forward.

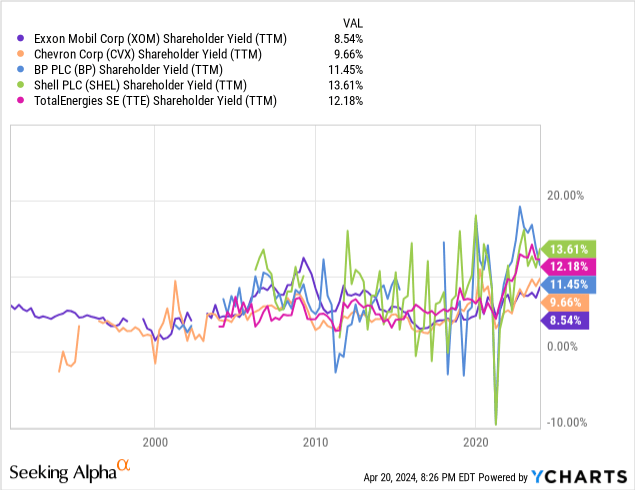

Ramping up shareholder returns is a possibility, while the company might also decide to keep a war chest in case it finds additional takeover targets. But since the company will have to digest the Pioneer takeover first, and since it could pursue all-stock deals anyway even if it were to find a new takeover target quickly, I believe that there is no need to keep a huge cash pile. Increasing shareholder returns thus seems like a viable option — especially when we consider that Exxon Mobil’s shareholder yield is somewhat lacking when compared to the shareholder yields of the other supermajors, as we can see in the following chart:

Exxon Mobil’s shareholder yield of 8.5% does not look bad at all in absolute terms. But considering the strong cash generation among oil and gas companies right now, and considering the 10%-14% shareholder yields of Exxon Mobil’s peer group, the company has some potential to increase shareholder returns for sure.

I don’t expect drastic dividend increases, as steady and reliable dividend growth is more appropriate for a Dividend Aristocrat like Exxon Mobil. But the company could increase its buyback pace — as we have seen earlier, its net share count reduction is sub-par compared to its peers that have been more active in this area.

Macro Outlook

As an energy company, Exxon Mobil is highly dependent on the macro picture. This includes both the state of the economy, as economic growth drives oil demand, and the geopolitical situation.

Economic growth in the United States has been stronger than expected during the first quarter, and the same holds true for China, which also beat expectations when it came to Q1 GDP growth. The International Monetary Fund has raised its global economic growth estimate (see link above), which should be positive for oil demand during the remainder of the year.

Tensions in the Middle East remain high, which is also supportive for oil prices. With oil trading not far from the 52-week-high, the macro environment is positive for Exxon Mobil and other energy producers.

Should a recession materialize, then oil demand would likely decline to some degree, which would hurt oil prices and thus Exxon Mobil’s earnings. Due to high-interest rates, a recession could still happen, but to me, this doesn’t look very likely in the near term — GDP growth and employment are strong.

XOM Stock Valuation And Takeaway

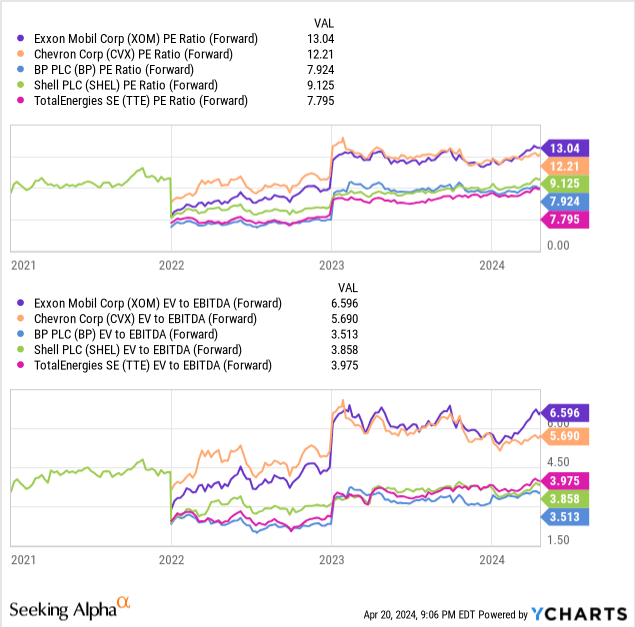

Exxon Mobil has seen its shares run up by 20% so far this year, which has brought the share price to almost $120. Here, Exxon Mobil trades at 13x forward net profits, using the analyst consensus estimate for the current year. While not a high valuation in absolute terms, this is still a somewhat elevated valuation compared to how many other energy companies are trading:

Among the supermajors, Exxon Mobil is the most expensive one today, with peers trading at 8x to 12x this year’s net profits. One could argue that Exxon Mobil’s European peers have weaker balance sheets, but even when we look at the enterprise value to EBITDA ratio instead of the earnings multiple — the EV/EBITDA ratio accounts for debt and cash on the balance sheet — Exxon Mobil still trades at a considerable premium versus its peer group.

From a valuation perspective, Exxon Mobil thus does not look overly strong. Relative to its peer group, it also has a below-average dividend yield of 3.2% today.

Exxon Mobil has some great assets, such as its Guyana business, and the company should benefit from high oil prices in the foreseeable future. But due to its rather high valuation, relative to peers, and its somewhat sub-par shareholder returns (at least for now), I don’t think it is the best energy play right now.

Analyst’s Disclosure: I/we have a beneficial long position in the shares of BP either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.

Is This an Income Stream Which Induces Fear?

The primary goal of the Cash Flow Kingdom Income Portfolio is to produce an overall yield in the 7% – 10% range. We accomplish this by combining several different income streams to form an attractive, steady portfolio payout. The portfolio’s price can fluctuate, but the income stream remains consistent. Start your free two-week trial today!