Summary:

- Google’s stock has surged after a major drop in 2022 and AI doubts in 2023.

- Google’s Q1 earnings report showed surprisingly strong performance in Search, YouTube, and Cloud, leading to positive revisions in earnings estimates and more potential upside for the stock.

- The company’s decision to introduce a dividend could lead to a higher P/E multiple over time and increased demand for its stock.

- My year-end 2024 and 2025 price targets for Google.

photosvit/iStock via Getty Images

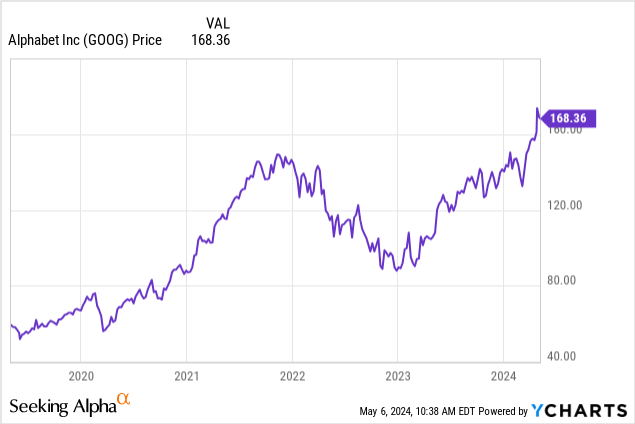

After a brutal 2022/early 2023, Google stock (NASDAQ:GOOG) (NASDAQ:GOOGL) has been on a tear. It was only last February that Google’s AI tool Bard gave a wrong answer in a presentation, sending the company’s market cap down $100 billion in one day. Panicked analysts proclaimed the end of Google, and fund managers dumped the stock. But since then, business has never been better, with GOOG now up roughly 77% from that fateful Bard presentation. Last month, Google soared after delivering a huge earnings beat, driven by YouTube and search. Google also just did something that I thought was incredibly savvy, which was to declare its first-ever dividend.

Google’s New Dividend Should Support A Slightly Higher P/E Multiple Over Time

Historically, Silicon Valley tech CEOs have been incredibly stubborn about refusing to pay dividends or split their stock. But now, Google’s new dividend allows it to be included in dozens of dividend-oriented funds and ETFs, either now or down the road once it has a sufficient dividend history. This creates additional demand for Google stock and can support a higher floor and ceiling for the company’s P/E ratio. The dividend move follows a similar announcement by Meta (META). Also, since many dividend funds make raising the dividend each year a condition of index inclusion, I expect both of these companies to raise their dividends, perhaps doubling their payouts in the next five years or so.

To be fair, Google’s dividend isn’t huge. They’re starting it off by paying $0.20 per quarter– at current prices that’s only a 0.48% yield. But consider that there are hundreds, if not thousands, of dividend-oriented ETFs and mutual funds out there with various criteria for inclusion (either mechanical or manager-selected). Additionally, many individual investors prefer stocks that pay at least some dividend. It’s difficult to ballpark what paying a dividend would be worth for Google, but I think a reasonable guess is that the company should command an additional turn of the P/E multiple as a result, or roughly $7-$8 per share.

Is this an educated guess? Sure. But consider that Apple (AAPL) started paying a dividend in 2012. Today, Apple now trades for a higher forward P/E ratio (~28x) than Google (~22x). It’s certainly not from Apple’s growth – Google has a much higher expected growth rate in earnings, while Apple’s earnings have been revised down. Popularity is certainly some of it, but Google has better growth prospects than Apple, and there’s no good reason for the 27% premium in valuation. Perhaps the dividend will help close it.

Google’s Earnings Proved Naysayers Wrong

Google reported Q1 earnings last month, with big beats on both revenue and profits. For the quarter, Google earned $1.89 vs. analyst expectations of $1.51. What drove the beat? Google CEO Sundar Pichai highlighted three drivers for the quarter on Google’s Q1 conference call.

- Search. Search revenues were up 14% year-over-year as the overall economy remained strong, and the company fine-tuned its process for tailoring advertisements to consumers.

- YouTube. YouTube is a great product for consumers, and advertisers are rapidly increasing their ad spend on the platform at a roughly 20% annual clip.

- Improved cloud profitability. Cloud in particular is interesting because it was losing money for Google for so long. Now, Google has the scale to profitably compete with Amazon and Microsoft (MSFT) in cloud. Google Cloud is also growing 25%-30% annually for the time being.

Additionally, modest cost-cutting through layoffs has helped keep expense growth increasing slower than revenue growth. Google delivered big growth numbers on a massive base, helping to power the powerful bull run in the stock over the past year.

Google Valuation And New Price Target

After Google’s earnings report and conference call, Wall Street analysts have quickly revised earnings estimates higher for Google for this year and coming years. Analysts now expect $7.53 in earnings for 2024 and $8.54 in earnings for 2025. Moving out to 2026, analysts are calling for earnings of $9.83.

All else being equal, if Google is able to deliver on the level of earnings currently expected by analysts, the stock will have roughly 31% upside over the next 1.5 years. This assumes that the forward P/E multiple remains steady at around 22.5x. This isn’t an exact science, but this implies a year-end price target of around $192 and a year-end 2025 price target of $221. To this point, Google has a clear path to $200 and beyond.

Taking future earnings estimates and applying the present P/E multiple is a classic way to set price targets for stocks, especially growth stocks. However, you also have to be careful assuming that high multiples will remain high in the future, particularly if future growth slows down. In Google’s case, however, I think the company deserves its multiple of 22.5x. While the entire market is richly valued, Google has past and projected earnings growth that should be at least 15%. It’s quite reasonable to assume the current trends in Search, YouTube and Cloud will continue. Google isn’t a recession-proof stock by any means, but I feel far more comfortable paying 22.5x for Google than paying 28x for Apple (when iPhone sales could nosedive in a recession). Google’s new dividend should help support the multiple as well.

Antitrust is also a risk for Google, with the company’s antitrust trial wrapping up last week and a decision expected later in the summer. But I don’t think any of these risks are too severe: While a recession would hurt Google’s advertising revenue, it might also give the company the cover it needs to trim headcount and set up a profitable business cycle in the following years. And while Google has risks from antitrust, these cases have been going on in the background for big tech for years. If Google does stumble at some point, Lina Khan and the FTC are not likely to be the cause.

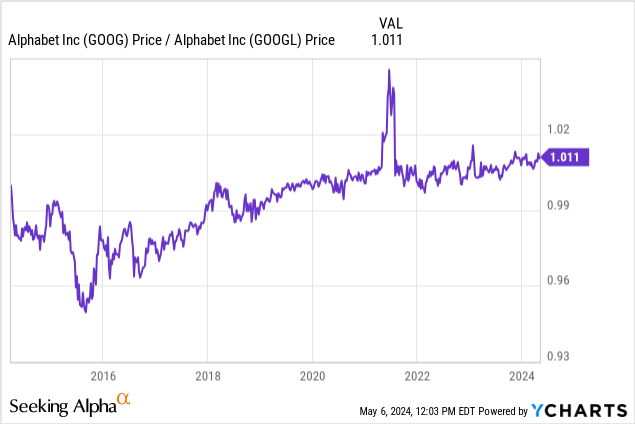

Google: Class A Vs. Class C Stock

If I’m writing a Google article, I have to include a mandatory bit on Google’s share structure and how you can exploit it to make a slightly better investment. Google has two main shares of stock that trade, Class A (GOOGL) and Class C (GOOG). So should you buy Class A Google stock or Class C? The answer is A. They’re identical in what they get you, but the class A shares are cheaper and now have the same dividend for a lower price.

Here we see the ratio between GOOG and GOOGL. They’re literally the same, so the fair value is 1. However, the market price has fluctuated over time. As of my writing this, GOOG trades for $168.47 while GOOGL trades for $166.59. GOOGL is 1.1% cheaper. They have the same dividend. So, for a 1.1% discount on your purchase, go with GOOGL. If you’re reading this in the future and are not sure which to buy, go with the cheaper option.

Bottom Line

Google’s business continues to perform extremely well. I’m raising my year-end price target on the stock to $192 and my year-end 2025 price target to $221. Initiating the dividend is a savvy move that increases the floor and ceiling for the company’s P/E multiple. To these points, Google is the best stock of the “magnificent seven” and the only one I would currently put money in. Google stock has a clear path to $200 and beyond from here. And if you buy Google, remember to buy the Class A shares (GOOGL) rather than the more common Class C shares (GOOG) for a 1.1% discount.

Analyst’s Disclosure: I/we have a beneficial long position in the shares of GOOGL either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.