Summary:

- The CEO’s speech at the BofA Conference yesterday has infused optimism by reiterating a commitment to enhance offerings and drive innovation.

- PayPal’s new digital advertising venture holds significant potential due to the vast industry size; even a small market share could greatly boost revenue.

- Valuation analysis shows a fair share price estimate of $74 with a compelling 17% upside potential.

Pgiam/iStock via Getty Images

Introduction

I had a ‘Strong Buy’ thesis for PayPal’s (NASDAQ:PYPL) stock in March. The recommendation keeps up well because the stock gained 6.3%, compared to +4.3% from the S&P 500. The company continues moving towards its revised strategy focusing on profitable growth.

In yesterday’s conference, the CEO reiterated his commitment to innovate and constantly improve the experience for customers. These are not just beautiful words, as they align with recent steps of expanding partnerships and adding more functionality for cryptocurrencies adopters. The move to expand into the digital advertising business is a smart move as the company leverages tons of customer behavior data thanks to billions of transactions processed every quarter. Capturing a percent of this huge industry can bring PayPal billions of dollars in additional revenue. Q1 performance was strong, and the valuation is very attractive even despite the stock’s fair value decreasing from $80 to $74. All these favorable factors mean I am inclined to reiterate PYPL’s ‘Strong Buy’ rating.

Fundamental analysis

The CEO, Alexander Chriss, shared some thoughts during yesterday’s BofA Global Technology Conference. I found some bullish insights in his words. First, he emphasized that he is happy with the management team after the shakeup. Having a team of professionals sharing the same strategic vision will likely help Mr. Chriss in leading PayPal’s transformation. Second, he stated that the company will continue prioritizing the most meaningful and impactful initiatives, compared to the previous practice of being spread too thin across various initiatives. Third, Mr. Chriss emphasized the importance of innovation velocity to speed up better serving all members of PayPal’s ecosystem.

Recent updates confirm that these three statements from the CEO are not just words. For example, the company recognizes strong momentum in digital assets as it recently made its own stablecoin, PayPal USD (‘PYUSD’), available on Solana blockchain. The company’s growing interest in cryptocurrencies look like a promising venture as Statista forecasts that cryptocurrency payments are expected to grow at a CAGR of nearly 17% between 2023 and 2030.

PayPal also continues expanding Venmo’s reach. For example, starting from April, both PayPal and Venmo collaborated with the Visa+ peer-to-peer payment system. Enabling cross-platform money transfers will likely enhance the company’s ecosystem and increase the appeal for users transferring funds across various platforms.

Grand View Research

Another strong strategic move is the decision to expand into the digital advertising business. Couple of weeks ago the company announced that it is hiring Uber’s (UBER) former head of advertising to run digital ads business line. The move is sound because PayPal processes billions of transactions per quarter. With the modern AI tools, it is highly probable that the company will be able to monetize this big data by selling targeted ads. According to Grand View Research, digital advertising market is expected to observe double digit CAGR by 2030. That said, there is a strong market opportunity for PYPL. Stellar Q1 reports from the world’s two largest digital advertising players, Google (GOOGL) and Meta (META) suggest that the industry is regaining momentum after an uncertain 2022-2023.

KBV Research suggests that digital advertising can become a trillion-dollar industry by 2030. This means that capturing just a percent of this pie will add $10 billion to PYPL’s annual revenue by 2030. This is solid compared to the company’s TTM $30 billion revenue. To conclude, there is a great potential to drive revenue growth from this new venture.

Q1 2024 10-Q report

Despite the company reporting its earnings more than a month ago, any fundamental analysis is incomplete without the latest earnings review. Moreover, PayPal’s performance was solid in Q1, and this is another positive sign for investors.

Revenue grew by 9% YoY fueled primarily by increasing transaction revenues. Number of payment transactions per active account grew by 13% meaning that the slight decrease in number of active accounts did not have much effect on the top line.

The management’s cost discipline is apparent as profitability outpaced revenue growth. Operating income grew by 17% YoY, much faster than revenue. This allowed it to increase non-GAAP EPS by 27% YoY.

In summary, I like how the company performs under new management. Q1 performance is a good indication of the focus on more high-quality revenue growth and discipline in spending. The management is committed to innovating and improving customers’ experience, which is evident from recent initiatives. I see great potential from the new digital advertising business line, which can become a ten-billion business over the long-term in my view.

Valuation analysis

Last time I modeled PYPL’s discounted cash flow (‘DCF’), I arrived at an $80 fair share price. DCF assumptions are fluid, and the model has to be periodically updated.

Not much changed in the monetary environment, so I reiterate the same 11.5% WACC. There was a notable FY 2024 consensus revenue forecast downgrade since March. In my previous DCF model it was $34.4 billion of FY 2024 revenue, now it is downgraded to $32 billion. I incorporate this change as well as the updated revenue growth forecasts for 2025-2028. High single digit growth looks sound for PayPal, considering all opportunities and growth initiatives. On the other hand, the management’s cost efficiency initiatives helped to improve TTM FCF margin from 17.19% to 21.37%. This improvement is also incorporated into my DCF model together with the expectation that PYPL will be able to drive FCF expansion at least by 50 basis points per year. According to Seeking Alpha, there are 1.05 billion PYPL shares outstanding. The constant growth rate is 3%, aligning with current inflation levels.

Calculated by the author

My updated fair share price estimate is $74. This is $6 lower than the previous target due to more conservative base year revenue assumptions. On the other hand, a 17% upside potential is still compelling.

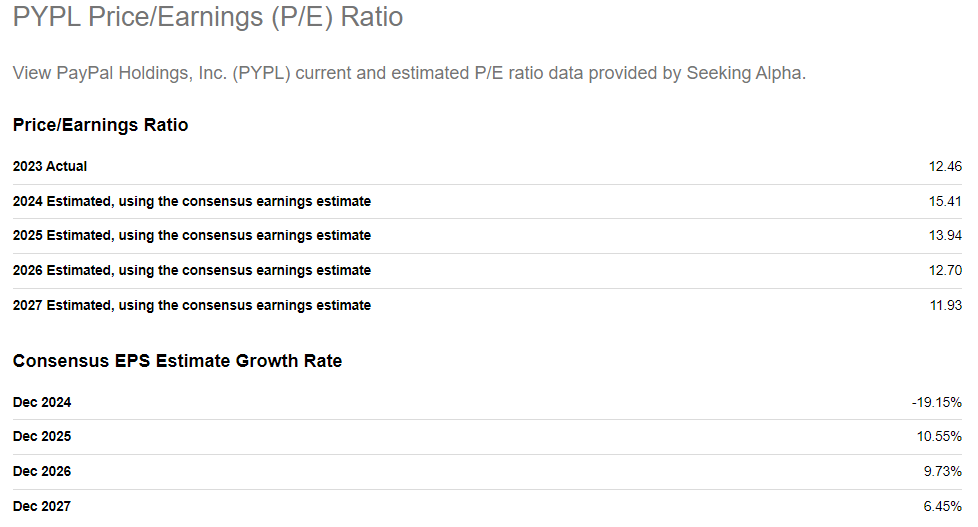

PayPal’s current P/E ratio is 12.5, extremely low for a growth company. FY 2024 is a ‘Transition Year’, and the EPS is expected to dip. However, consensus projections reveal solid EPS rebound in 2025-2027. Looking at PYPL’s current and forward P/E ratio I am confident that the stock is undervalued.

SA

In summary, PYPL’s valuation is compelling from the DCF point of view and the P/E ratio’s point of view. I downgrade my target price from $80 to $74 but there is still a compelling 17% upside potential.

Mitigating factors

PayPal’s innovations and ventures into new areas appear promising. On the other hand, there is always a significant level of uncertainty and execution risk when companies embark on new projects. Innovations might require higher-than-expected budgets, or benefits from introducing new features might come out lower than costs. Electronic payments space is rapidly transforming with powerful entrants like Apple and Google significantly expanding into this industry over the last few years. Innovation speed is vital because technologies might become obsolete in the modern fast-paced world.

The company’s financial performance significantly depends on total payment volume. If TPV declines, PayPal’s transaction-based revenue will move in the same direction. The TPV heavily depends on the health of the broader economy. Despite the U.S. economy demonstrating unexpected resilience, we should not forget that monetary policy is tight, and Fed is still not ready to start cutting rates. If the monetary policy remains that tight for the next few years, the economy might face a recession, which will definitely adversely affect the TPV.

Conclusion

Despite the target price downgrade, I remain extremely bullish. The upside potential is still compelling. Positive fundamental developments increase the probability of sustainable share price growth closer to its fair value. Therefore, I believe that PYPL is still a ‘Strong Buy’.

Analyst’s Disclosure: I/we have a beneficial long position in the shares of PYPL either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.