Summary:

- Walmart stock’s current dividend yield is at a record low of 1.19%, indicating overvaluation.

- The stock has a healthy growth outlook, with an expected EPS compound annual growth rate of 7.3% over the next 10 years.

- The growth has already been fully priced in with a PEG ratio of 3.8x.

Robert Way

WMT stock: dividend yield at record low

I last covered Walmart (NYSE:WMT) stock in October 2023 (see the chart below). At that time, the stock just joined the elite club of Dividend Kings after increasing its dividend payouts consecutively for 50 years. My article argued for a bullish thesis based on the following two considerations:

Dividend growth investors may complain about WMT’s low yield and slowed dividend raises in recent years. For long-term investors, the focus should be on total shareholder yield instead of dividend yield. When the total shareholder yield is considered, the picture changes quite a bit as WMT has been consistently buying back its own shares over the past at a robust pace.

In terms of valuation, given its competitive advantages, the stock deserves a valuation premium above the sector average. And its current valuation multiples are close to (or below) its historical averages. For example, its FWD earning yield of 4.13% is higher than its 5-year average of 4.01%.

Indeed, the stock prices have appreciated significantly since then, as you can see from the chart below. The stock price advanced by about 27% and the total return is close to 28%.

Seeking Alpha

The trouble with a working bull thesis is that it tends to defeat itself. As prices advance, valuation expands, and risks heighten. The remainder of this article will explain why this is exactly the case I am seeing with WMT. And for these reasons, I am downgrading the stock from my previous BUY rating to HOLD.

Given its dividend king status, its dividend yield provides a good valuation metric and an excellent starting point. As you can see from the chart below, the stock is currently yielding 1.19%, not only far below its long-term average but also near the lowest levels in at least a decade, indicating sizable overvaluation.

Admittedly, the stock has a healthy growth outlook ahead, but I think the current valuation has already priced in years of growth already, as detailed next.

Seeking Alpha

WMT stock: growth outlook

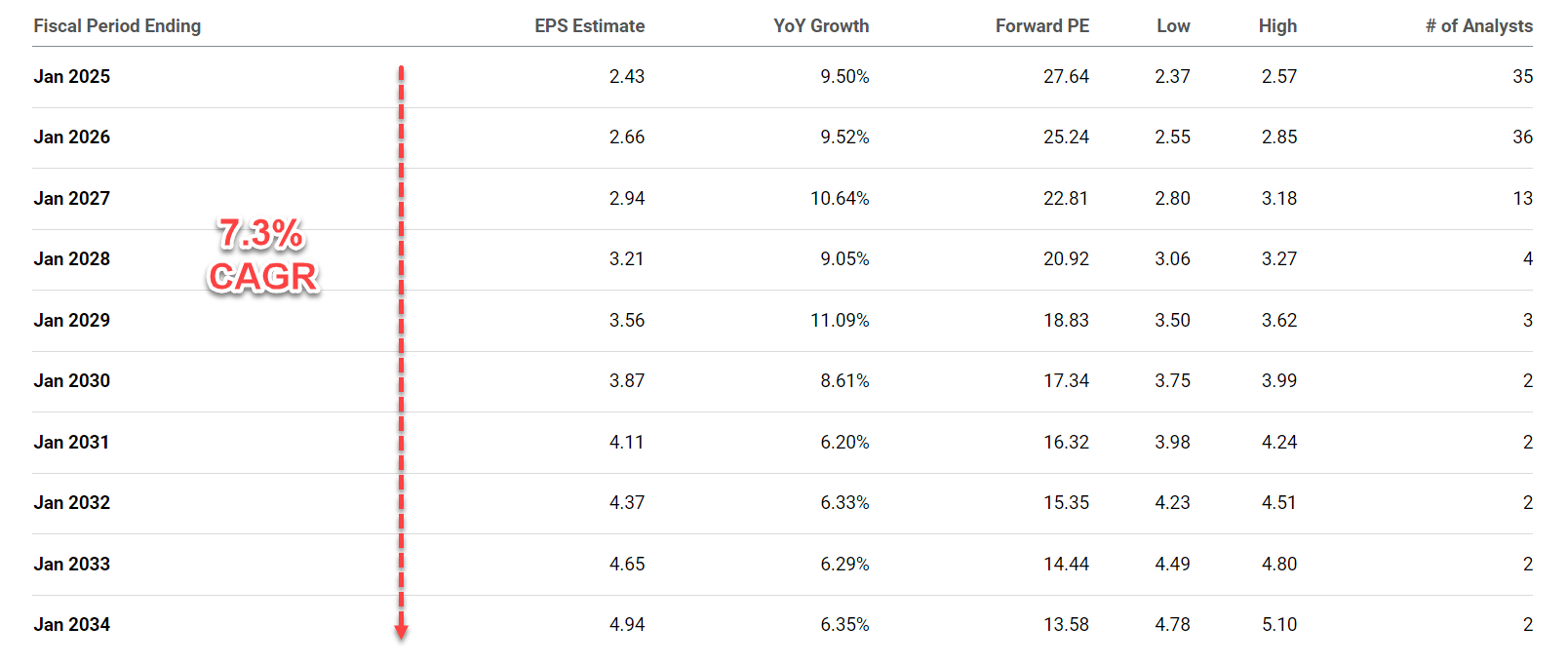

The chart below shows the consensus EPS estimates for WMT stock in the next decade. Based on the chart, the market expects WMT’s EPS to grow at a compound annual growth rate (“CAGR”) of 7.3% over the next 10 years. Such a CAGR may seem boring for growth investors, who only get excited at double-digit growth rates. However, I consider it a very healthy pace for a retail giant. At this projected rate, its EPS would grow to $4.94 by fiscal year 2034, up from the current $2.43. It is very respectable for a company with sales exceeding the GDP of many countries to more than double its earnings in a decade.

Seeking Alpha

And indeed, there are good catalysts that could support the above growth projection. I do not really consider WMT as a traditional retailer these days anymore. The company is well-positioned as a tech-powered omnichannel player. For example, the company has made significant progress toward automating its fulfillment centers in the past and has even more aggressive goals in the future. I expect it to successfully automate more than 55% of its fulfillment center volume and do even better at its Supercenters in the next 1~2 years. Subsequently, I anticipate the progress to be reflected in lower fulfillment costs, improved inventory management, and increased store efficiency, all leading to a better overall omnichannel experience for its vast customer base.

Speaking of its vast customer base, advertising is another growth opportunity for WMT. Similar to Amazon, Walmart already sells ad space on its e-commerce website and app, which features a much higher margin than retail. Its ad revenue “only” reached $3.4 billion last year. But the growth potential is tremendous. For example, last year, the growth was 28% year over year. Recently, the company announced it has agreed to acquire low-end TV maker VIZIO to leverage its user interface and serve targeted ads based on user viewing patterns. I expect the ad platform to be one of the key enablers of operating income growth in the years to come.

The problem is that, after the recent price surges, I consider such growth to be fully priced in already, as detailed next.

WMT stock: growth is fully priced

At its current P/E of around 28x (see the chart above) and a projected growth rate of 7.3% CAGR, the PEG (P/E growth ratio) is over 3.8x, too expensive in my view either in absolute or relative terms. It is far above the gold standard of 1x that GARP (growth at a reasonable price) investors seek.

Admittedly, the PEG ratio can be misleading for dividend stocks (especially dividend kings) like WMT. If a stock pays consistent dividends, investors do not need as much growth for a good total return. This is the idea behind the following PEGY ratio that Peter Lynch promotes:

For dividend stocks, Lynch uses a revised version of the PEG ratio – the PEGY ratio, which is defined as the P/E ratio divided by the sum of the earnings growth rate and dividend yield. The idea behind the PEGY is very simple and effective (most effective ideas are simple). If a stock pays out a large part of its earnings as dividends, then investors do not need a high growth rate to enjoy healthy returns. And vice versa. And similar to the PEG ratio, his preference is a PEGY ratio below 1x.

If you recall from an early chart, WMT’s current dividend yield is about 1.19%. Dividing the P/E of 28x by the sum of 7.3% CAGR and 1.19% yield, its PEGY ratio turns out to be about 3.3x, still far above the 1x threshold. To be completely fair, share repurchases have to be considered here too. As mentioned in my previous article, WMT has been consistently buying back its own shares over the past. But the current buyback is quite lower as reflected in the 0.58% of buyback yield as you can see from the next chart below. I do not anticipate the company increasing buybacks substantially in the years to come, considering its plans to invest in growth, especially in areas of e-commerce and omnichannel experiences as just mentioned.

Seeking Alpha

Other risks and final thoughts

Besides the valuation risk, WMT faces similar macroeconomic risks to its retail peers. These risks include disruptions to the global supply chain, geopolitical risks, rising inflation, etc. Supply chain disruptions, often caused by geopolitical instability or natural disasters, can lead to product shortages and higher costs for retailers. Additionally, rising inflation can squeeze profit margins as retailers struggle to raise prices fast enough to offset increasing costs for goods and labor.

And the latter point is more relevant to WMT, in my view, considering its business model. WMT’s business model focuses on lower prices and tighter margins, which could make it more sensitive to cost pressure than peers with more premium pricing strategies. More specifically, WMT’s operating expenses have increased steadily over the past (see the top panel in the next chart) and operating margins have declined in tandem (see the bottom panel). Going forward, I am anxious to see how/if it can control its expenses and stabilize its margin under elevated inflation, higher labor costs, and higher fuel costs.

To reiterate, the goal of this article is to argue for a downgrade on the stock to HOLD from my previous BUY recommendation. For existing shareholders, there is nothing wrong with holding a high-quality stock like WMT (and congratulations on a sizable capital gain!) even at a premium valuation. The stock has a healthy growth curve ahead, fueled by factors like e-commerce expansion and continued consumer demand for value. However, for potential investors, my view is that much of the growth has already been priced in, judging by the high PEG (or PEGY) ratio and record-low dividend yield.

Seeking Alpha

Analyst’s Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.

Join Envision Early Retirement to navigate such a turbulent market.

- Receive our best ideas, actionable and unambiguous, across multiple assets.

- Access our real-money portfolios, trade alerts, and transparent performance reporting.

- Use our proprietary allocation strategies to isolate and control risks.

We have helped our members beat the S&P 500 with LOWER drawdowns despite the extreme volatilities in both the equity AND bond market.

Join for a 100% Risk-Free trial and see if our proven method can help you too. You do not need to pay for the costly lessons from the market itself.