Summary:

- Alphabet announces Anat Ashkenazi as its new CFO after a 10-month search process.

- The new CFO has the potential to generate meaningful value for Alphabet’s shareholders.

- Expectations for the new CFO include providing clarity and guidance, increasing granularity in reporting, and capitalizing on strengths while preparing for potential disruptions.

shih-wei

After a long 10-month search process, Alphabet (NASDAQ:GOOG) (NASDAQ:GOOGL) finally announced Anat Ashkenazi, former Executive Vice President and Chief Financial Officer at Eli Lilly (LLY), as the company’s new CFO.

I have quite a long wishlist for the new CFO, who, in my view, has a clear path to generate meaningful value for Alphabet’s shareholders.

Introduction & Revisiting The Google Investment Thesis

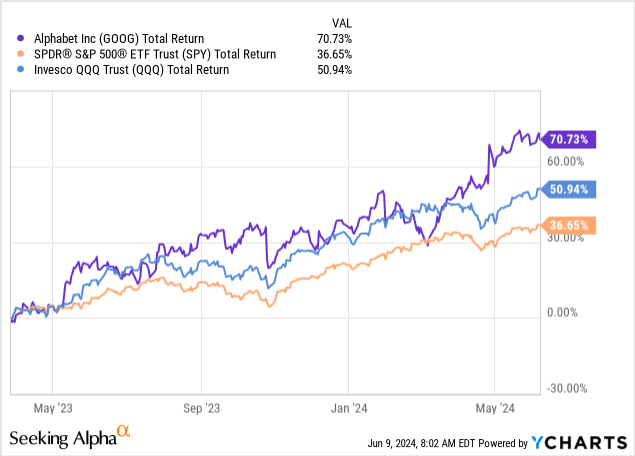

I’ve been covering Alphabet on Seeking Alpha since March of 2023, maintaining a bullish rating throughout the period. So far, we were correct:

The investment thesis here was, and remains, quite simple. Alphabet has several extraordinary assets under its umbrella, including YouTube, Android, Search, Google Cloud, and the rest of the Google suite. These are all businesses that have extremely wide moats, benefit from each other, and have very attractive margins, as well as an abundance of growth opportunities.

And the cherry on top, Alphabet, who owns all these businesses, was, and still is, relatively undervalued, compared to its historical levels and its peers.

That said, we can’t ignore the reasons for the market placing a higher risk, and therefore a lower multiple on Google’s parent for the past several years.

Three Reasons The Market Was (And Still Is) Rightfully Discounting Alphabet

Even though I had a Buy rating on Alphabet and also held shares, I had many negative things to say about the company’s complacency, capital allocation, and lack of transparency.

Side note, perhaps this is the best testament to Google’s strength, as even big critics found the company to be an attractive investment, due to a rare combination of quality and valuation.

Starting with complacency. 2023 was the year of efficiency for many companies, including Meta (META), whose CEO, Mark Zuckerberg, was the one who coined the term. After the big selloff in 2022, companies, primarily in the tech landscape, understood that investors were expecting them to cut unnecessary costs aggressively, and many of them delivered. However, during a time when Google’s rivals were aggressively laying off employees, Google was less aggressive and much more complacent, which resulted in a slower recovery of margins.

Second, capital allocation. Continuing from the complacency point, Alphabet was also slow to cut non-core activities and continued to invest heavily in some Other Bets projects. In addition, the company continued to sit on a huge ~$100 billion pile of cash, with no aggressive enough buybacks and no dividend announcement, even when the stock was plummeting.

Lastly, the company suffered from a lack of transparency, as its former CFO, Ruth Poran, was reluctant to provide any quantifiable guidance about the company’s future, both on the expenses and the revenue front.

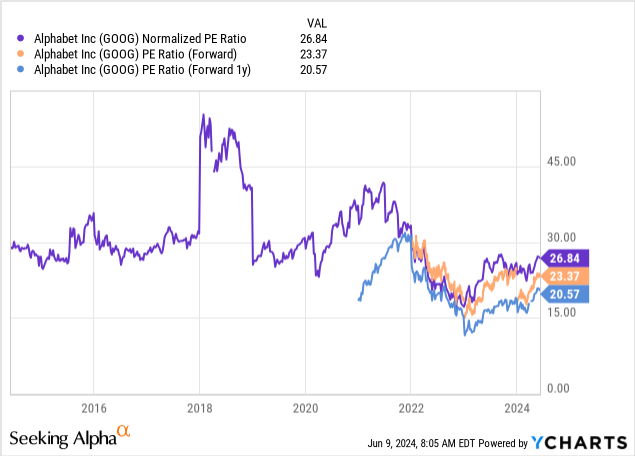

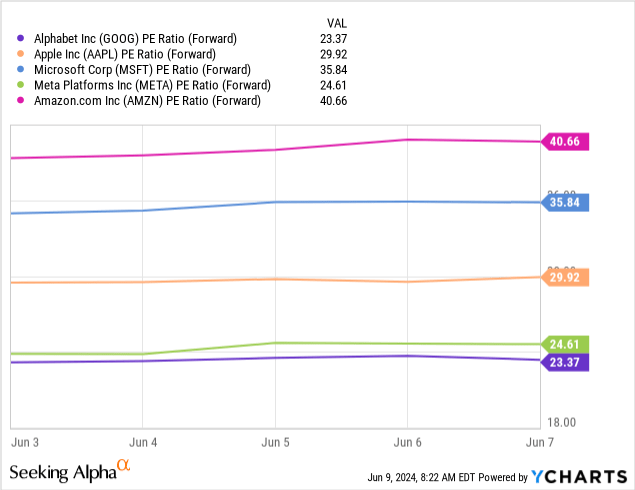

While Alphabet did improve upon the aspects we discussed above, including its largest buyback announcement ever, much better execution, improved margins, and the initiation of a dividend, we can still see the company is getting the lowest multiple in big tech, even though it’s expected to grow faster than some of the names here.

There are other reasons that justify this discount, including a higher risk of disruption to the core business from AI, and being third in the cloud behind Microsoft (MSFT) and Amazon (AMZN).

Both of the above will remain a drag on valuation for quite some time, but I still believe there’s room for multiple expansion if the new CFO changes some of the previous ways of doing things.

Expectations From Alphabet’s New CFO

Former Executive Vice President and Chief Financial Officer at Eli Lilly, Anat Ashkenazi, will start her role on July 31st, 2024. She’s been at Eli Lilly for 23 years and had multiple financial-related roles in the pharmaceutical empire.

Although she has no major experience in tech, I believe that the new CFO can be a meaningful driver of shareholder returns in the near term.

Providing Clarity & Guidance

Alphabet did not provide tangible guidance for as long as I can remember. For a company with such an expansive portfolio of businesses, it’s extremely hard for investors to gauge the amount of investments and expenses Alphabet will have in a given year. This leads analysts to heavily rely on extrapolation and historical numbers to predict next year’s numbers.

Aside from less reliable predictions, this creates a bad incentive for the management team. For instance, Meta provides an annual expense guide. If revenues come better than expected, investors will still expect expenses to come around that initial guide, which means Meta’s management is pressured into staying within its range.

For Alphabet, if revenues are better than expected, management might be willing to spend more, as long as margins remain reasonable.

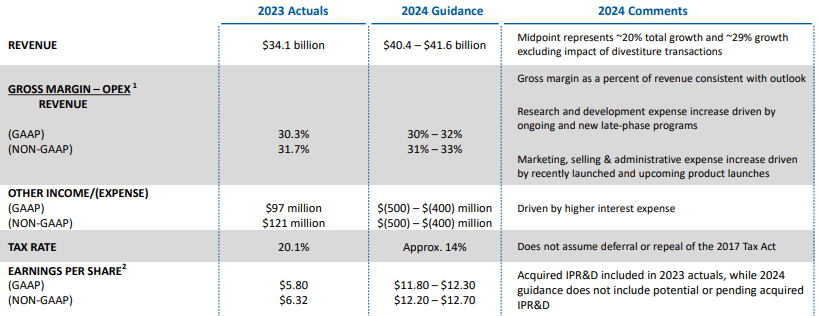

This is how typical guidance looked like, for Eli Lilly, under Anat’s leadership:

Eli Lilly Q4’23 Presentation

The company also published comprehensive quarterly presentations and provided extensive explanations about each of the P&L items.

Generally speaking, in the pharmaceuticals sector, this is the customary way of doing things, and I wouldn’t expect anything that comes close to this level of transparency.

That said, I believe that even an annual expense target could contribute to a few points of multiple expansion, and that is something I expect the new CFO to push for.

More Granularity, Especially In Other Bets

Alphabet recently changed its segment reporting, transforming its ‘Google Other’ line item to ‘Google Subscriptions, Platforms, and Devices’. That, along with Alphabet’s Other Bets, leaves a lot of room for more granularity about each of the company’s businesses within those divisions.

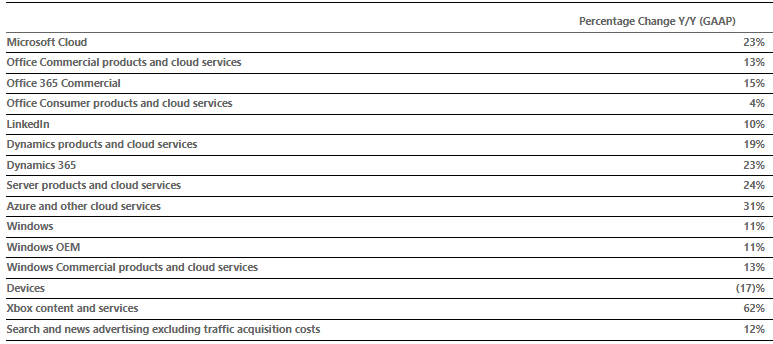

For instance, we have no idea how much money Google generates from hardware, what’s the size of YouTube’s subscription business, and the list goes on. Here’s how another very famous company and a Google competitor on many fronts, provides detail on each of its products and services:

Microsoft Q3’24 Earnings Release

There’s the old saying ‘What you don’t know can’t kill you’, but I think that in investing, uncertainty is almost always bad. I’m not saying they have to break out everything, but even some detail on each of the business lines on earning calls could be helpful.

Aggressively Capitalizing In Periods Of Strength, Preparing For Periods Of Weakness

This is the area where I’m most excited. One capability that pharma companies must possess is the ability to aggressively capitalize on successful products (i.e. Ozempic and Mounjaro). Another crucial capability is preparing for patent cliffs.

Alphabet’s portfolio consists of several jewels that are the overwhelming leaders in their verticals. One of those jewels is of course search.

In my view, there are a lot of similarities between what Alphabet is currently experiencing with some of its core products and the looming potential disruption from AI.

Although I find it very unlikely that Google will lose significant market share due to AI, and net-net I expect AI to be positive for the company, primarily due to its Google Cloud, I think the new CFO should be able to help find the right balance between milking the previous business model and preparing for the new era.

Valuation

Based on current consensus estimates, Alphabet is trading at a 23.4x multiple over 2024 earnings, and a 20.6x multiple over 2025.

We’ve already seen Alphabet handily beat Q1 estimates, and yet current consensus still seems quite low, as it reflects worse seasonality, and a margin decline from Q1, both of which I can’t find good reasons for.

Even if we take current consensus estimates as they are, I believe the base case scenario would be a 23.0x multiple on 2025 earnings by the end of 2024, reflecting nearly 12% upside. A bear case multiple would be 20.5x, and a bull case scenario is 25x.

Created and calculated by the author using data from Seeking Alpha; Based on Alphabet’s share price as of 06/09/2024.

If the new CFO delivers on the three key areas I listed above, I see no reason why Alphabet can’t experience a significant multiple expansion.

Combined with the fact I expect the company to handily beat estimates, I believe that the most likely outcome would be that we end up somewhere between the base and bull scenarios.

That leads me to a blended price target of $200 a share.

Conclusion

After the 2022 selloff, Alphabet shares recovered. Initially, the main driver for the recovery was valuation. Then, it was the inevitable improvement of the company’s legacy businesses.

From March 2024 up to today, I believe Alphabet’s leadership deserves much of the credit, as the market clearly recognized Alphabet’s management changed its tone and started executing at an industry-leading level on many fronts.

Still, there’s more to be desired, and I believe that the new CFO has the opportunity to drive meaningful improvements in the very near term.

The combination of Alphabet’s huge growth opportunities and its relatively low valuation makes it a must-have position in my view. Therefore, I reiterate a Buy rating.

Analyst’s Disclosure: I/we have a beneficial long position in the shares of GOOG either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.