Summary:

- Adobe is investing in new AI tools to enhance productivity in the digital space, leading to double-digit growth in its Digital Media segment.

- The majority of Adobe’s revenues come from high-margin subscriptions, providing predictability and strong free cash flows.

- Adobe’s valuation is in-line with its historical P/E ratio, but the introduction of AI products like Adobe Firefly could drive further growth and attract new users.

Cinefootage Visuals

Adobe (NASDAQ:ADBE) is a leading software company and investing heavily into the roll-out of new AI tools that enhance users’ productivity and effectiveness working in the digital space. Adobe is seeing double-digit top line growth in its two most important segments, Digital Media and Digital Experiences, and the company has launched new products such as Firefly or Acrobat AI Assistant to make its products more appealing to users. Adobe is set to benefit from the overall growth of the generative AI software industry and has a broad product suite to fall back on to leverage the strength of new AI technologies. Adobe’s business is high-margin and free cash flows are in an uptrend!

Double-digit top line (subscription) momentum, high-margin business model

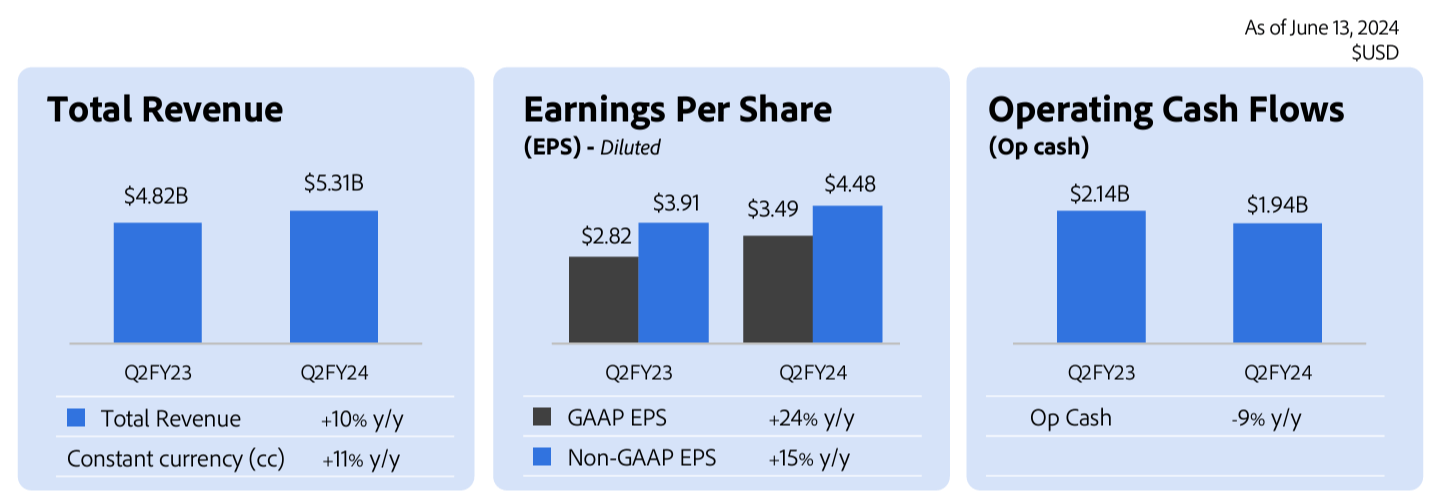

Adobe is most known for its catalog of productivity and creator tools such as Photoshop, Premiere and Lightspeed which have become household names in the creative industry. The beauty of the company’s business model and product suite is that Adobe collects an overwhelming amount of its revenues in the form of subscriptions. These subscriptions tend to be recurring and generate therefore a very high level of top line and cash flow predictability for Adobe. In the second fiscal quarter (which ended on May 31, 2024), Adobe generated $5.31B in revenues, showing 10% year over year growth. Of those $5.31B in revenues, 95% ($5.06B) came entirely from subscriptions.

Adobe

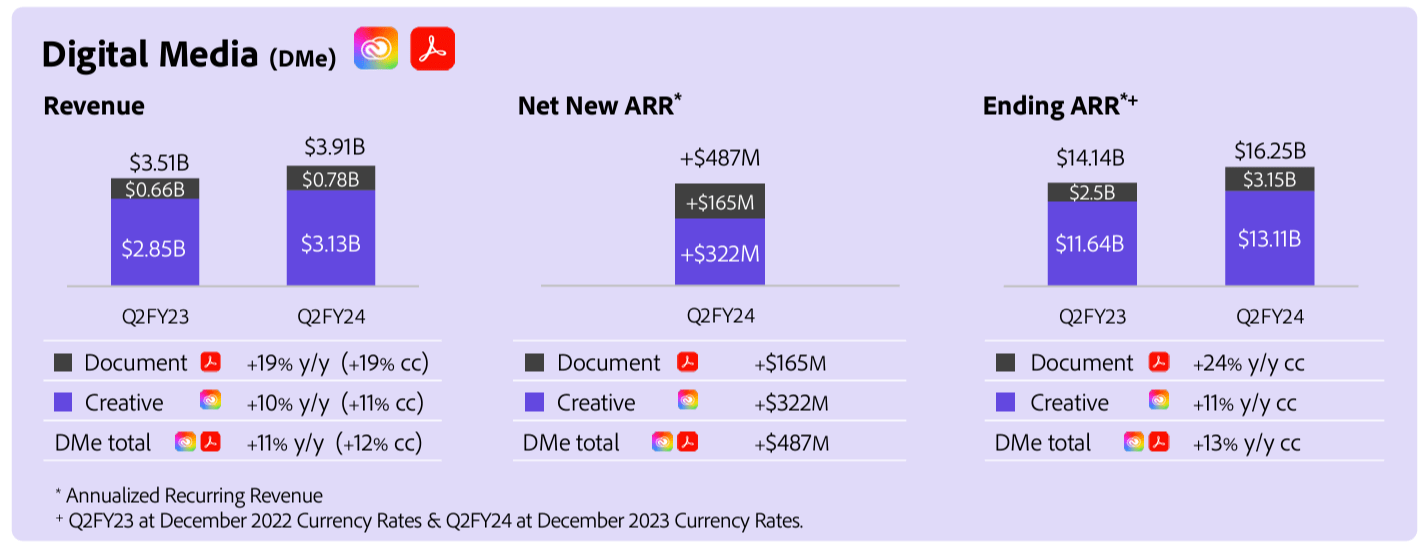

Adobe’s business is segregated into three business segments: Digital Media, Digital Experience and Publishing. In the first segment, Digital Media, Adobe consolidates its Document and Creative Cloud services. Digital Media services include Adobe Firefly, a generative AI tool that can help creators, as an example, to fill images with AI-generated content. It therefore promises creators and agencies considerable productivity gains through the use of automated image creation tools. This segment, not surprisingly, grew revenues 11% year over year to $3.83B in FQ2’24 and had the highest subscription revenue share (76%).

Adobe

Adobe’s Digital Experience segment provides data insights and supports users’ workflows. This segment generated $1.33B in revenues (24% of subscription revenue), much less than Digital Media, but it still saw 9% top line growth. The last segment, Publishing and Advertising, generated $74M in revenues and is not really that material for Adobe.

Adobe benefits from the roll-out of new AI tools that are, to some extent, still in the beta phase, like Adobe Firefly. This tool is part of Adobe Creative Cloud and is a generative AI software tool that has huge applications in the creation of photo-realistic pictures. Adobe, for instance, recently debuted its Firefly Image 3 Model, which allows Generative Fill, Generative Remove and Text-to-Image functions in order to boost productivity around image creation and editing. With AI clearly offering creators huge productivity gains and simplifying workflows for digital marketing agencies (as an example), the launch of AI image creation tools could make Adobe’s underlying product suite much more attractive for users going forward.

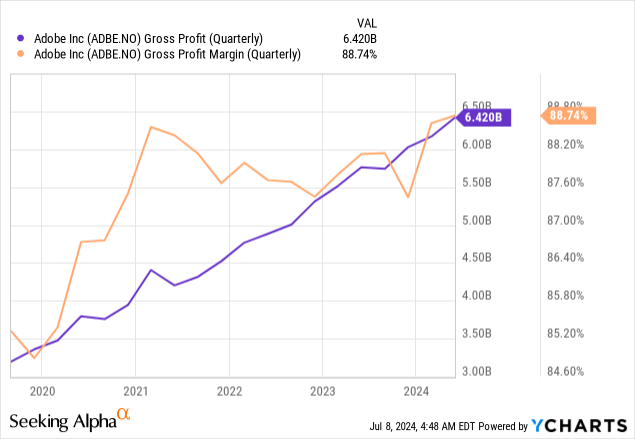

Besides a catalyst for continual top line growth through the launch of AI products, Adobe is running a very profitable software business. The software company has benefited from a strong, multi-year uptrend in its gross profits as well as margins.

Strong free cash flow trajectory

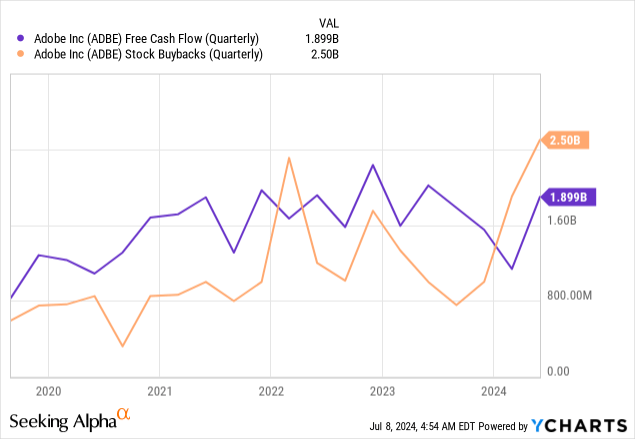

Adobe’s high-margin software business, which is built on a small number of high-performance productivity tools is seeing strong free cash flows, and I believe tools like Adobe Firefly, promises such significant productivity gains for creators that Adobe is set to see accelerating product uptake going forward. Adobe generated $1.9B in free cash flow in the last quarter and is buying back a ton of its shares (as you can see below).

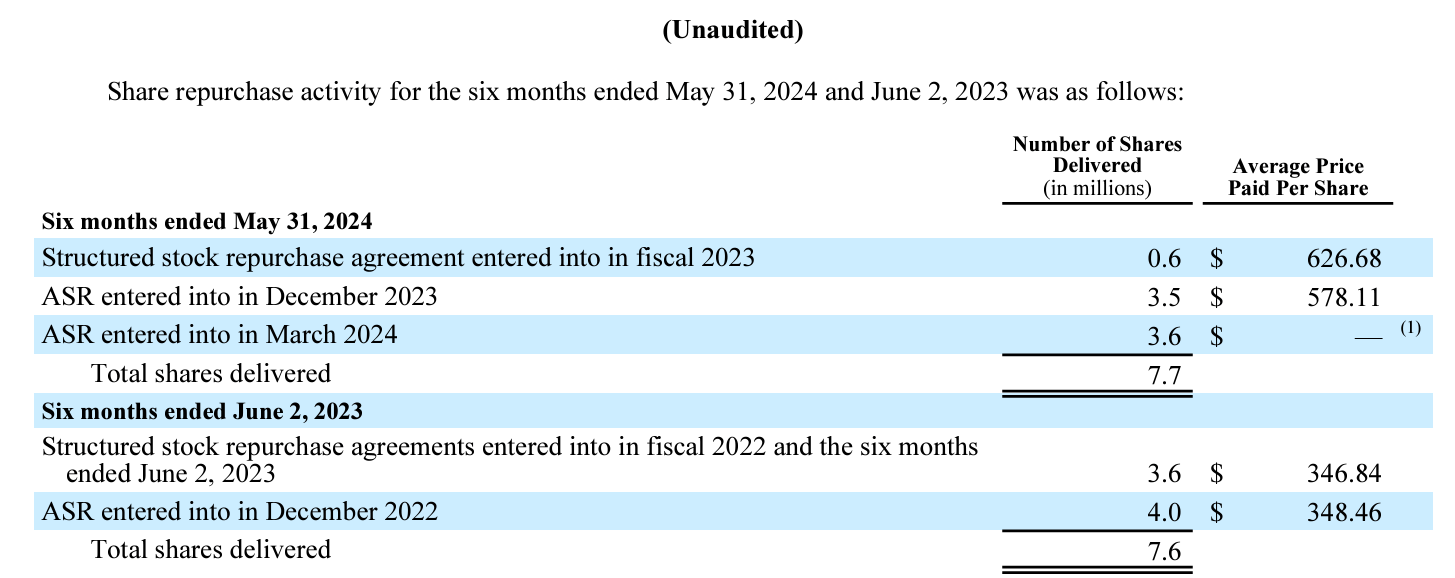

In March, Adobe’s Board of Directors authorized the repurchase of $25B of the company’s shares. Adobe has entered into a number of accelerated share repurchase agreements with financial institutions, and the software company repurchased 7.7M shares. Going forward, I expect Adobe to continue to repurchase more shares and potentially exhaust the stock buyback authorization way before it is set to expire (March 14, 2028).

Adobe – 10Q

Adobe’s valuation

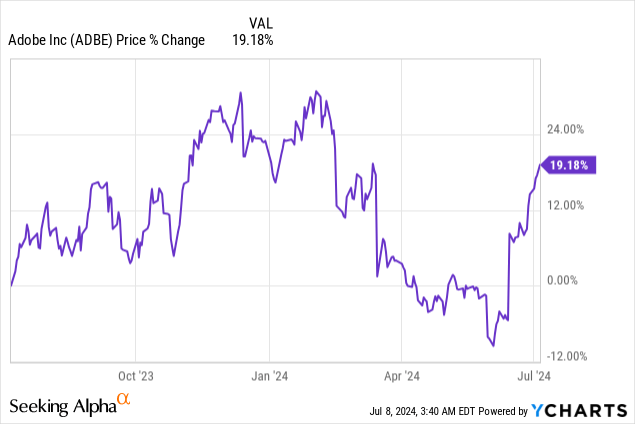

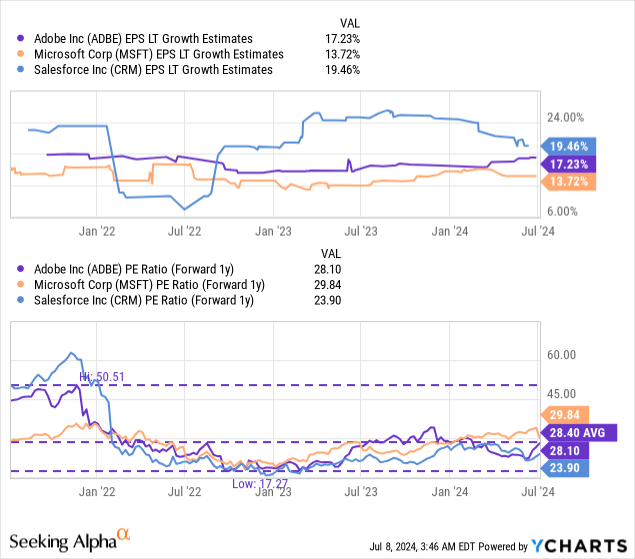

Adobe is a software generative AI company focused on productivity and could therefore be compared to Microsoft (MSFT) or Salesforce (CRM). Adobe is currently valued at a price-to-earnings ratio of 28.1X and the software business has seen renewed upside momentum after its well-received second fiscal quarter earnings report in June that showed healthy top line momentum as well as strong subscription growth, especially in Digital Media and Digital Experiences.

In the long term, Adobe is expected to grow its earnings per-share 17% annually, compared to 19% for Salesforce and 14% for Microsoft. While I believe that Adobe is a good bet on the AI generative software market and I like the company’s Adobe Firefly product as a conversion magnet, Salesforce also represents very deep value: shares of Salesforce sold off sharply after the latest earnings report which I saw as a unique opportunity to double down on the CRM applications provider given its deep earnings value.

Adobe is selling just slightly below its 3-year average P/E ratio of 28.4X, but the roll-out of AI-specific products could make the company’s underlying product suite much more attractive to users going forward… so I see catalysts for continual revenue growth here. For those reasons, I believe Adobe, while not cheap, has upside revaluation potential.

In my opinion, Adobe could be valued at 30.0X forward earnings given its double-digit EPS growth rate, strong profitability (based off of gross margins and free cash flows) and AI catalysts: A 30.0X P/E ratio implies a fair value of $617. This is a dynamic number, and it may change depending on Adobe’s subscription revenue and free cash flow momentum going forward.

Risks with Adobe

Adobe is a software play that has a unique product suite in the market that is aimed at the creative sector. Therefore, Adobe is seeing a very high percentage of recurring subscription revenues, mainly in Digital Media. This limits the risks drastically, in my opinion. What I see as a risk, however, is the emergence of new image creation tools that could be better than Adobe Firefly. While Firefly offers a huge opportunity for Adobe to make its existing product suite more attractive to users, Adobe is hardly the only company that invests in generative AI image software. If Adobe gets outcompeted on its AI image technology, the catalysts discussed in this article may not be realized.

Closing thoughts

Adobe is seeing double-digit top line momentum, including in its subscription business, which is driven chiefly by Digital Media and Digital Experiences. What I like about the software company is that 95% of Adobe’s revenues come from subscriptions, and Adobe runs a high-margin business as well. The free cash flow trajectory is encouraging, and the company is buying back a ton of its own shares. Adobe is currently valued at a P/E ratio of 28.1X, which doesn’t make it a bargain, but I see continual upside revaluation momentum as the company leverages its current AI product strength!

Analyst’s Disclosure: I/we have a beneficial long position in the shares of ADBE either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.