Summary:

- Nike, an American athletic footwear and apparel corporation, is now a $114 billion (by market cap) sportswear behemoth.

- Nike has enjoyed a unique level of brand awareness and cachet for many years, helping it to build a sportswear conglomerate with a wide lead over everyone else.

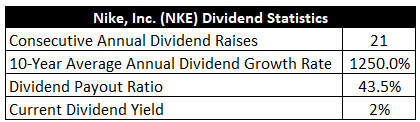

- Nike has increased its dividend for 21 consecutive years, with a 10-year dividend growth rate of 12.5%.

- Nike raised its revenue from $30.6 billion in FY 2015 to $51.4 billion in FY 2024, a compound annual growth rate of 5.9%.

hapabapa

Nike Inc. (NYSE:NKE) is an American athletic footwear and apparel corporation. Founded in 1964, Nike is now a $114 billion (by market cap) sportswear behemoth that employs more than 80,000 people. FY 2023 sales can be broken down geographically as follows: 44%, North America; 28%, EMEA; 15%, Greater China; and 13%, APLA.

As the world’s largest seller of athletic footwear and apparel, Nike is in a league of its own and the true kingpin of its industry. The company has spent decades investing in its core Nike brand (along with the ancillary Jordan brand), creating a “brand halo” where initial footwear products that become wildly popular resulted in a bevy of successful offerings across broader sporting products (including apparel and equipment).

Nike has enjoyed a unique level of brand awareness and cachet for many years, helping it to build a sportswear conglomerate with a wide lead over everyone else. To put a number on this, it’s estimated by Morningstar/Euromonitor that Nike has a ~23% share of its China market. That is dominant. And this preeminence feeds on itself, where the brand power and consumer mindshare leads to automatic/repeated purchases. It also helps Nike to navigate the changing retail landscape (e.g., offering direct-to-consumer purchases, bypassing retail partners and improving margins).

Now, both footwear and apparel are only becoming more and more competitive. Furthermore, rising tension between the US and China isn’t doing Nike any favors. But this remains a dominant business with excellent fundamentals, and its revenue, profit, and dividend all appear set to continue growing for years to come.

Dividend Growth, Growth Rate, Payout Ratio and Yield

To date, Nike has already increased its dividend for 21 consecutive years. Good stuff. Nike is now only a few years off from becoming a Dividend Aristocrat, and I don’t see why the company won’t get there. The 10-year dividend growth rate of 12.5% goes to show just how strong Nike has been with its dividend raises over the years. That said, due to a variety of factors, recent dividend raises have been in a high single-digit range (between 8% and 9%).

Still, that’s enough dividend growth to move the needle, especially when you pair that with the stock’s starting yield of 2%. By the way, it is very rare to see this stock with this kind of yield. For perspective, that’s 100 basis points higher than its own five-year average. Yes, this 2% yield is double the stock’s five-year average yield of 1%. This has typically been a low-yielding, high-growth stock. But growth has recently slowed, and the market has adjusted the yield higher (by sending the stock price lower) in order to compensate for this. That said, a fairly modest payout ratio of 43.5% easily covers the dividend and gives Nike some flexibility around the sizing of future dividend raises.

The last couple of years haven’t been kind to Nike, and competition is more fierce than ever, but the dividend is, in some ways, more appealing than it’s ever been. The stock’s yield is at a record high, and yet the dividend growth isn’t that far off from historical norms. If that doesn’t catch your attention, I don’t know what will.

Revenue and Earnings Growth

As appealing as the dividend profile is, though, many of the numbers are based on what’s happened in the past. However, investors must always be thinking about what may happen in the future, as today’s capital gets risked for tomorrow’s rewards. That’s why I’ll now build out a forward-looking growth trajectory for the business, which will be of service when the time comes later to estimate fair value.

I’ll first show you what the business has done over the last decade in terms of its top-line and bottom-line growth. And I’ll then reveal a professional prognostication for near-term profit growth. Amalgamating the proven past with a future forecast in this way should give us what we need to sketch out a rough idea of where the business could be going from here.

Nike raised its revenue from $30.6 billion in FY 2015 to $51.4 billion in FY 2024. That’s a compound annual growth rate of 5.9%. I usually like to see a mid single-digit (or better) top-line growth rate from a mature business like this, and Nike delivered.

Meantime, earnings per share grew from $1.85 to $3.73 over this 10-year period, which is a CAGR of 8.1%. A high single-digit bottom-line growth rate from a large business in a competitive space is solid, in my view.

Nike isn’t setting the world on fire with growth, but these are very respectable results. Now, recent results have been lumpy, and competitors are putting up incredibly strong numbers (indicating some eating of Nike’s lunch). That said, the $3.73 in EPS for FY 2024 would have actually been $3.95 if not for restructuring charges. And that $3.95 is still nearly 60% higher than pre-pandemic FY 2019’s EPS.

That is not bad at all, even if Nike isn’t crushing it as much as it used to. Looking forward, CFRA forecasts that Nike will compound its EPS at an annual rate of 2% over the next three years. It makes sense to be unenthusiastic over the next few years, as even Nike itself recently lowered FY 2025 guidance and is calling for revenue to be down mid single digits (compared to prior guidance of a low-single-digit drop in revenue).

CFRA does highlight how Nike “…continues to be the leader in active footwear and apparel across the globe and has shifted its focus, like most apparel and footwear companies, to its direct-to-consumer business to grow margins and improve its consumer relationships.”

Speaking more on that last point, Nike gets an estimated 44% of its annual revenue from DTC. This helps margins, offers relationship control, and insulates the company from physical retail challenges. But CFRA adds that Nike is “… now facing slowing demand across each of its markets.” CFRA then touches on the nagging competitive theme: “Nike is also facing fresh competition from HOKA and On and is experiencing top-line growth deceleration.

Putting it all together, I think it’s fair to say that Nike isn’t quite the dominant force in athletic footwear and apparel that it used to be. There are some chinks in the armor, and its moat doesn’t seem as wide as it used to be. To this point, CFRA says the quiet part out loud: “We expect Nike revenues to grow low single digits over the next five years, as we believe Nike is no longer a growth company and will now grow in line with global growth.”

That’s probably disappointing to read for long-time shareholders who had penciled in higher growth rates over the long haul. It’s likely even more brutal news for those who were buying shares at over $170/each in 2021. Look, this isn’t devastating. But it does mean dialing back expectations and modeling in lower growth when valuing the business.

To be fair, it’s extremely difficult to stay an industry’s dominant force for decades on end. Nike has done an admirable job of doing this, but the industry has become tougher. Ceding some share of market isn’t the worst thing in the world, but Nike will have to continue to protect its brands, aggressively market its products, innovate, and win consumers over in China so that it can remain globally competitive in a tougher industry.

Boiling it down, Nike still seems capable of high single-digit EPS growth over time, which would power similar dividend growth (although FY 2025 will almost certainly be underwhelming). Beyond the revenue growth, Nike has buybacks (the outstanding share count has been reduced by nearly 15% over the last decade) and higher margins from DTC.

There’s also the flexibility around dividend growth stemming from the payout ratio. I think investors would be unwise to expect Nike’s 12%+ dividend growth of a bygone era to return. But more recent dividend growth of 8%+ could persist.

And those buying in now are able to lock in a yield that’s twice as high as usual. Not a terrible situation at all after the stock’s rerating by the market.

Financial Position

Moving over to the balance sheet, Nike has a fantastic financial position. The long-term debt/equity ratio is 0.5, while the interest coverage ratio is over 33. As good as these numbers are, they belie the strength of the balance sheet. I say that because Nike ended FY 2024 with more cash on hand than long-term debt, putting the firm in a net cash position. Love this balance sheet.

I also love the profitability. Return on equity has averaged 40.3% over the last five years, while net margin has averaged 10.6%. Remarkably, Nike has consistently produced very high returns on capital without much leverage.

Fundamentally speaking, even with recent stumbles, Nike is undoubtedly a high-quality business. And with economies of scale, unrivaled brand recognition, IP, R&D, and a global distribution network, the company benefits from durable competitive advantages.

Of course, there are risks to consider. Litigation, regulation, and competition are omnipresent risks in every industry. Competition, in particular, has been a rising risk for Nike, as newer competitors are having great success in the marketplace and chipping away at Nike’s lead.

Being a global company, Nike faces currency exchange rates and geopolitics. Nike’s heavy reliance on China adds risk, with rising US-China tensions and possible China nationalism leading to a preference for local brands. While the company has a large DTC presence, Nike is vulnerable to physical retail and the changes occurring therein.

Fashion trends change quickly, and this is something that can leave even a giant like Nike behind. Marketing and R&D will continue to require a sizable cash burn commitment. The company must continue to innovate around its products and partner with the right athletes in order to stay visible and relevant.

Overall, I don’t see especially high risks when it comes to Nike, even if the risks are elevated relative to where they’ve been in the past. However, after the stock down nearly 60% from all-time highs, the market’s rerating of this stock has also priced in far more risk already.

Valuation

The P/E ratio of 20.2 is as low as I’ve ever seen it on Nike’s stock. We can compare that to its own five-year average of 36.9 to see how far the mighty has fallen. To put it another way, its current earnings multiple is almost half of what it’s usually been. That’s a substantial delta.

The P/CF ratio of 17.6 is also just under half of its own five-year average of 30.1. And the yield, as noted earlier, is significantly higher than its own recent historical average.

So the stock looks cheap when looking at basic valuation metrics. But how cheap might it be? What would a rational estimate of intrinsic value look like?

I valued shares using a dividend discount model analysis. I factored in a 10% discount rate and a long-term dividend growth rate of 8%. In the past, an 8% L-T dividend growth rate expectation out of Nike was easy, if not downright pessimistic. Nowadays, it actually might be stretching things.

As I showed earlier, I do see a case for Nike to continue its more recent dividend growth trajectory (that’s been north of 8%). That would stem from low single-digit revenue growth, modest margin expansion, buybacks, and a slight modulation of the payout ratio. If Nike doesn’t do anything to reclaim its dominance, 8% will prove to be too difficult to hit. However, I fail to understand why Nike would just sit around and allow the competition to eat its lunch. Nike only needs to recapture a portion of its past magic to make this 8% mark achievable and set the company and stock up for solid long-term results.

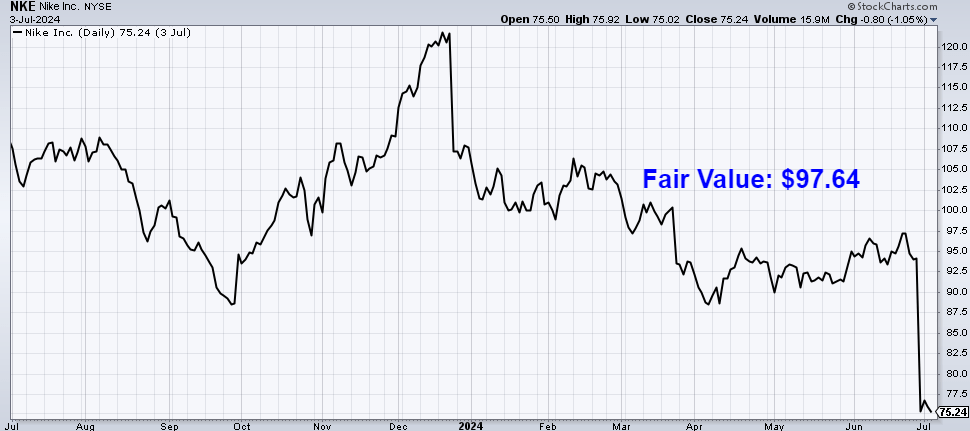

The DDM analysis gives me a fair value of $79.92. The reason I use a dividend discount model analysis is because a business is ultimately equal to the sum of all the future cash flow it can provide. The DDM analysis is a tailored version of the discounted cash flow model analysis, as it simply substitutes dividends and dividend growth for cash flow and growth. It then discounts those future dividends back to the present day, to account for the time value of money since a dollar tomorrow is not worth the same amount as a dollar today.

I find it to be a fairly accurate way to value dividend growth stocks. A lot of air (pun intended) has been taken out of the stock’s valuation, and my model shows moderate undervaluation. But we’ll now compare that valuation with where two professional stock analysis firms have come out at. This adds balance, depth, and perspective to our conclusion.

Morningstar, a leading and well-respected stock analysis firm, rates stocks on a 5-star system. 1 star would mean a stock is substantially overvalued; 5 stars would mean a stock is substantially undervalued. 3 stars would indicate roughly fair value. Morningstar rates NKE as a 5-star stock, with a fair value estimate of $124.00.

CFRA is another professional analysis firm, and I like to compare my valuation opinion to theirs to see if I’m out of line. They similarly rate stocks on a 1-5 star scale, with 1 star meaning a stock is a strong sell and 5 stars meaning a stock is a strong buy. 3 stars is a hold. CFRA rates NKE as a 3-star “HOLD”, with a 12-month target price of $89.00. I came out light this time around, despite what may have been a slightly aggressive model. Averaging the three numbers out gives us a final valuation of $97.64, which would indicate the stock is possibly 23% undervalued.

Bottom line: Nike Inc. is still the world’s dominant force in athletic footwear and apparel. Its brand power remains unrivaled. There is some work to do to right the ship, but this is a terrific business. With a market-beating yield, a double-digit long-term dividend growth rate, a moderate payout ratio, more than 20 consecutive years of dividend increases, and the potential that shares are 23% undervalued, the stock’s epic drop from all-time highs may be presenting a great long-term investment opportunity for dividend growth investors.

Note from D&I: How safe is NKE’s dividend? We ran the stock through Simply Safe Dividends, and as we go to press, its Dividend Safety Score is 99. Dividend Safety Scores range from 0 to 100. A score of 50 is average, 75 or higher is excellent, and 25 or lower is weak. With this in mind, NKE’s dividend appears Very Safe with an unlikely risk of being cut.

Disclosure: I’m long NKE.

Editor’s Note: The summary bullets for this article were chosen by Seeking Alpha editors.