Summary:

- PepsiCo reported lackluster Q2 earnings, citing inflation impacting price conscious consumers.

- Despite challenges, positive developments are on the horizon, with the stock down double digits.

- Pepsi’s strong brand appeal, international growth potential, safe dividend, and undervalued stock make it a compelling long-term investment.

Fotoatelie

PepsiCo Inc (NASDAQ:PEP) reported Q2 earnings on the 11th of July, and the results were lackluster. Management repeatedly pointed to the role inflation now plays with price conscious consumers.

Compelled by rising logistics and input costs, PEP raised prices over the last few years. In a very real sense, that resulted in the company and shareholders paying the price that consumers are unwilling to shoulder.

However, there are positive developments on the horizon, and with inflation up and the stock down double digits over the trailing 12 months, one must wonder whether the current share price presents a buying opportunity or a warning sign.

A Review Of Q3 2024 Earnings

Pepsi released Q2 earnings on the 11th of July. Adjusted EPS of $2.28, up 9% over last year, beat analysts’ estimates by $0.12. However, revenue of $22.5 billion, up 0.8% year over year, missed consensus by $100 million.

Management now guides for “approximately” 4% organic revenue growth, slightly below the prior “at least” 4% forecast. The company projects 2024 core EPS of at least $8.15, up 7% percent from 2023.

Overall, organic sales were up by 2%, boosted by a 6% jump in international sales, led by Europe and Latin America. However, growth in the US was lackluster, at best. Beverage sales were up 1%, and food sales fell by less than 1%.

To put those numbers in context, it is important to note that Pepsi’s North American sales constitute roughly three fifths of total revenue, while Latin America and Europe combined account for about a quarter of the company’s sales.

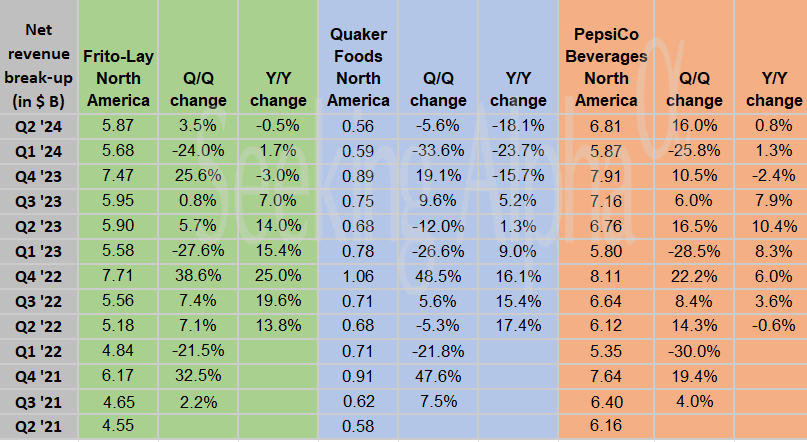

Frito-Lay North America accounts for nearly a third of Pepsi’s total revenue. Sales for that segment were down 4%.

Quaker Foods North America constitutes 3% of the company’s revenue. The recent recall of contributed to a 17% decline in that segment’s sales.

Accounting for about a third of the company’s overall revenue, the North America beverages segment recorded a 3% drop in sales.

The Quaker Oats Recall

In December of 2023, Pepsi recalled over 90 granola bar and cereal products due to possible salmonella contamination. It is important to note that the FDA issued a news release stating that, “Quaker has received no confirmed reports of illness related to the products covered by this recall.”

About a month later, the company added over 40 additional products to the list of Quaker Foods affected by the recall.

The following chart records the loss in revenue tied to the recalls but also shows that headwind is waning.

Seeking Alpha

During the earnings call, the CEO provided an upbeat and succinct overview of the effects of the recall moving forward.

Quaker, you’re all familiar with the situation. We’re recovering the supply chain by Q4, will be in almost 100% supply and obviously the business at that point will be growing materially, because we’re just refilling the shelves and pipeline. So that should be out of the picture and it will be a positive impact for us.

Ramon Laguarta, CEO

Where Pepsi Shines

With over a fifth of the market, Pepsi is the global leader in savory snacks, and Lay’s is the bestselling snack food brand worldwide. In terms of volume, with 11 of the 15 top-selling products sold in convenience stores, Pepsi’s share of the salty snacks market is more than nine times that of its closest rival.

Pepsi ranks behind only Coca-Cola (KO) among the world’s beverage providers. Although Pepsi’s worldwide nonalcoholic ready-to-drink sales are about one-third of Coke’s, Pepsi’s sells two times the volume of the third-place rival. In the sports category, Gatorade rules the roost, garnering over 40% of the volume share globally.

Although many folks recognize some of the company’s leading brands, most are probably unaware of the breadth and depth of Pepsi’s product lines. Along with Lay’s, Pepsi, and Gatorade, PEP also counts Doritos, Frito-Lay, Fritos, Ruffles, Cheetos, Aquafina, Cap’n Crunch, Cracker Jack, Quaker, Rice-A-Roni, and Tostitos among its brands.

You can then add a wide variety of products sold overseas, such as Alvalle (Spain), Walkers (United Kingdom), Smith’s (Australia), Duyvis (Netherlands), Agousha (Russia), Emperador (Mexico), Ivi (Albania, Greece, Cyprus, Serbia), Chipsy (Egypt, Serbia), Baconzitos (Brazil), Paso de los Toros (Uruguay), Simba (Southern Africa), Kurkure (Bangladesh, India, Pakistan), and Yedigün (Turkey).

Note the above are not exhaustive lists.

Pepsi’s products serve to drive foot traffic and sales, and the company’s scale provides bargaining leverage with suppliers and advertisers that equates into pricing power.

Pepsi also has a strong logistics system. Proof of that lies in Pepsi’s decades-long successful distribution partnerships with Unilever (UL) and Starbucks (SBUX).

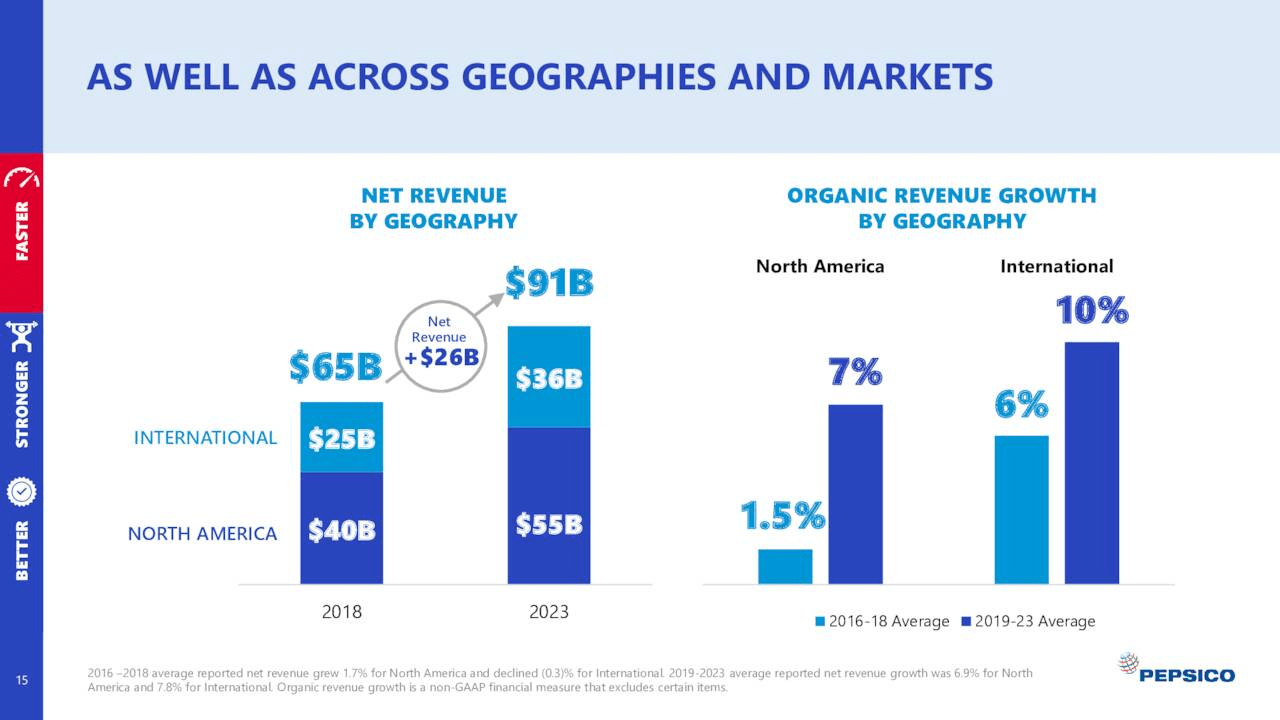

Last but far from least, Pepsi has a long growth runway in international markets. PepsiCo has been expanding its product offerings to drive demand in overseas markets.

Since roughly 80% of the world’s population lives in developing and emerging nations, as the share of the middle-class population increases in international markets, sales of Pepsi products are likely to grow markedly.

The following chart shows how revenue growth in the international market has outpaced that of North America and that it is accelerating.

2024 Pepsi presentation

2024 presentation

Debt, Dividend, And Valuation

Pepsi has an A+ credit rating, a solid investment grade level.

Pepsi currently yields 3.31%. The payout ratio is a bit under 32% and the 5-year dividend growth rate is 6.62%. Pepsi’s strong credit metrics and payout ratio indicate the dividend is safe and should continue to grow at a solid pace for the foreseeable future

Pepsi’s forward P/E of 20.89x is well below the 5-year average P/E ratio for the stock of 24.42x.

Yahoo! Finance estimates Pepsi’s 5-year PEG ratio at 1.98x, which is also below the stock’s average 5-year PEG ratio of 3.44x.

Pepsi currently trades for $163.95. The 24 analysts that follow the company have a 12-month average price target of $183.20. Seven rate PEP as a Strong Buy, 4 provide a Buy rating, 12 a Hold rating, and one analyst grades the stock as a Strong Sell.

Is Pepsi A Buy, Sell, Or Hold?

Consumers are rebelling against higher prices, and the Quaker recalls will continue to weigh on US sales for the next few quarters.

However, I view these as transitory headwinds. Over the long haul, Pepsi’s moat and brand appeal should serve investors well.

Pepsi is the most durable business in our coverage. We expect PEP shares to outperform in risk-off environments, and long term by compounding earnings ahead of peers.

Jefferies analyst Kaumil Gajrawala

Pepsi has a particular appeal for investors seeking a safe dividend growing at a solid pace, and it is important to note that over the last 5 years, the yield on Pepsi’s dividend has averaged 2.16%, while today the yield is well over three percent.

I believe that once rates are cut, the valuation of dividend bearing stocks will increase significantly, and Pepsi’s stock will ride that tide. I’ll add that a drop in interest rates will signal inflation has moderated significantly, hopefully putting a damper on a headwind that has punished Pepsi’s sales and profits.

That means snagging shares of Pepsi while it is in a rough patch should serve investors well over the long run. Investing in the stock at this juncture, following a weak quarterly report and signs that consumers are rattled by inflation, brings to mind the term, “short-term pain leads to long-term gain.”

With a wide moat, a rock-solid financial foundation, and solid growth prospects in overseas markets, I contend that Pepsi is a very safe bet over the long haul.

Put another way, you can’t buy a six pack Pepsi for the same price you could a couple of years ago, but you can snag the stock for 2022 prices.

In large part, that is why I rate Pepsi as a Buy.

I estimate PEP is trading about 9% below a fair value range. I’ll add that both the forward P/E and PEG ratios are well below the stock’s 5-year averages for those metrics.

I have a small investment in Pepsi, and I hope to add to the position as funds become available.

Here is a link to my most recent Pepsi article.

Analyst’s Disclosure: I/we have a beneficial long position in the shares of KO either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

I have no formal training in investing. All articles are my personal perspective on a given prospective investment and should not be considered as investment advice. Due diligence should be exercised and readers should engage in additional research and analysis before making their own investment decision. All relevant risks are not covered in this article. Although I endeavor to provide accurate data, there is a possibility that I inadvertently relay inaccurate or outdated information. Readers should consider their own unique investment profile and consider seeking advice from an investment professional before making an investment decision.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.