Summary:

- Uncertainty surrounds Tesla’s valuation, with doubts about the company’s ability to sustain growth and overcome regulatory and competitive challenges.

- Tesla’s stock rating remains a strong sell for the seventh time in a row.

- Elon Musk’s ambitious projects, such as Optimus and Full Self-Driving, are met with skepticism regarding their profitability and feasibility.

choi dongsu

Something is gradually changing

This is the seventh article I have written about Tesla, Inc. (NASDAQ:TSLA), and once again the rating is a strong sell. To some of you, I may sound repetitive or even crazy, but over the months/years, my opinion about this company has never changed. In my last article, you can find my latest valuation, and I reaffirm again that Tesla is not worth more than $50 per share.

As I have always done, I would like to emphasize that rating and consideration of a company are two entirely different things. I esteem Tesla and there is no question that it has revolutionized the automobile industry; my disappointment relates to its unreasonable price per share.

At the same time, I also revere CEO Elon Musk for his achievements. Since December 2020, Tesla’s total return has been 0%, but 10 years ago, the price per share was only $15. So, I would say that the stock has proven to be a great investment for those who have believed in this company since its beginnings. Overall, at least to date, I think it is fair to characterize Tesla’s history as full of successes despite the many difficulties encountered along the way, but something is gradually changing.

My impression is that according to many investors, Tesla is still a company that can grow 30-40% per year, which is now only a distant memory. There is a lot of resistance to accepting this, and even in the face of evidence, a feeling of denial prevails. Elon Musk’s narrative about Tesla’s future is so convincing in their eyes that they don’t care that revenues are only growing by 2%, profitability has halved but the P/E (FWD) is still 90x: there is always a justification for this.

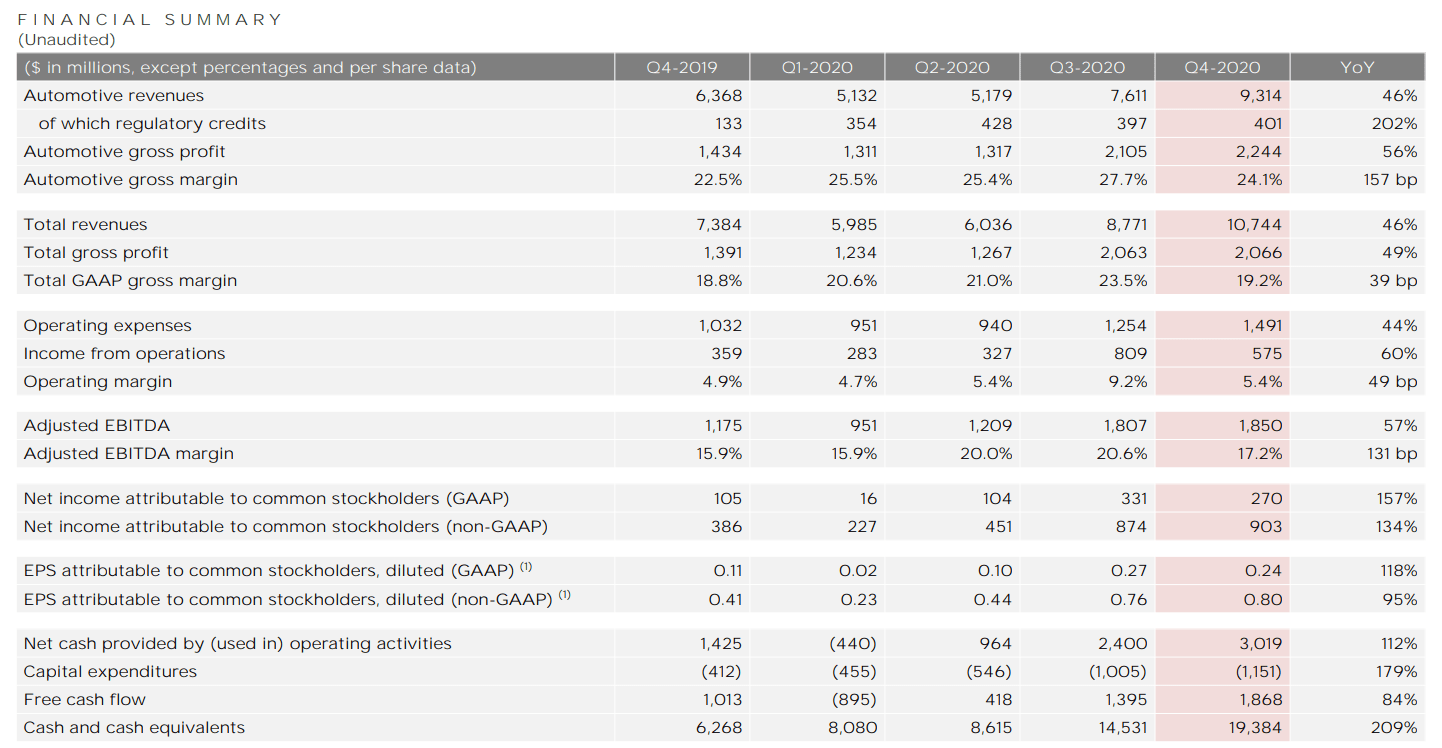

Tesla Q4 2020

If Tesla recorded the same results as the end of 2020, I would have no problem considering it fairly valued, the point is that it has been several quarters that things have gotten out of hand.

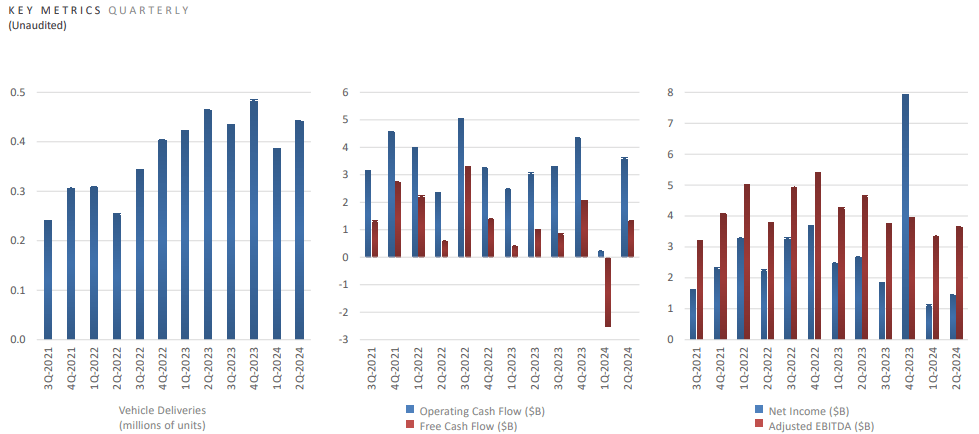

Tesla Q2 2024

I’m pretty sure that if the average Tesla investor looked at results like that (without knowing it was Tesla), I doubt they would buy this company at a P/E of 90x. However, their trust in Elon Musk’s narrative convinces them enough to go against the evidence.

This is not necessarily a mistake; everyone is free to believe what they want, and those who trusted Elon Musk long ago certainly made a lot of money. Honestly, if I could (I am only 26 years old now), I would not have invested in Tesla even in 2015 and let a gigantic opportunity pass me by. At the time, it was absurd to think that Tesla would sell almost half a million vehicles in one quarter, yet it happened. Elon Musk was right.

However, I think this time is different, and his predictions seem too unrealistic. After reading the Q2 2024 conference call, I was rather puzzled about his statements regarding Full Self-Driving (“FSD”), Robotaxis, the Tesla Network, and Optimus.

In the next section, I will analyze the ones I think are the most relevant, and I would appreciate it if you would add your perspective in the comments.

Optimus will revolutionize the world

For the few who do not know, Tesla is working on a generalized humanoid robot named Optimus. Its purpose is to be able to perform the tasks of a human being, and its use may extend into a wide variety of situations. In other words, it is literally an intelligent robot that can replace a human being for almost all intents and purposes, kind of like being in an episode of Black Mirror.

Tesla Q2 2024

Tesla is currently working on an advanced version of Optimus, namely Version 2, but Version 1 is already available and performing some tasks in Tesla’s factories. So, Optimus is already a reality, although at least for now it is not available for sale. You won’t see them around, simply because the company wants to first make sure they resolve every little problem before they start selling them: better the first damage is done to battery cells than to humans.

Personally, I can’t deny that this project is interesting. However, currently, it is still in its earliest days, so I don’t think Tesla’s price per share deserves a premium for Optimus’ potential. After all, we don’t know anything concrete about it yet.

The company plans to ramp up production in 2026, and then commercialize Optimus once Version 2 is fully developed. In any case, we don’t know what the potential customers might be, we don’t know how much it will be sold for, we don’t know when the project will be profitable, and we don’t know if companies are ready to replace their employees with robots. There are so many unknowns about this, and it is too risky to justify Tesla’s P/E for this project.

It is like I want to invest in Meta Platforms, Inc. (META) because I believe that eventually, billions of people will interact in the Metaverse. That may be, but it cannot be the main reason for the Meta investment thesis because right now, it is just pure speculation, although Meta Quests are a reality.

For Elon Musk, all these doubts seem not to exist:

I think the long-term value of Optimus will exceed that of everything else that Tesla combined. So, just simply consider the usefulness and utility of a humanoid robot that can do pretty much anything you ask of it. I think everyone on earth is going to want one. There’s 8 billion people on earth, so it’s 8 billion right there. Then you’ve got, all of the industrial uses, which is probably at least as much, if not way more. So I suspect that the long-term demand for general-purpose humanoid robots is in excess of 20 billion units. And Tesla has the most advanced humanoid robot in the world and is also very good at manufacturing, which these other companies are not. And we’ve got a lot of experience — with the most experienced world leaders in real-world AI.

In other words, he is convinced that everyone on Earth will want Optimus because it can do almost anything you ask it to do. So based on this thinking, since there are 8 billion of us, there is already a demand for 8 billion humanized robots. But there is more because if we consider all its possible industrial uses, the long-term demand exceeds 20 billion. Moreover, since Tesla is currently the company furthest ahead in this kind of technology, it will probably be the one to benefit the most. In terms of money, all this translates into a potential Tesla market cap of $25 trillion, only counting Optimus.

Frankly, I cannot agree with any of his statements, all of which are too simplistic:

- First, it is not necessarily the case that everyone wants to have a humanized robot at home just because it can fully replace a human being, assuming it can. Second, I doubt that companies will replace their employees with robots without any problem; it is simply absurd to think so, and I think it is superfluous to explain why.

- These estimates have almost no value since there is no well-defined time frame. Long-term is too general a word; it can be 10 years as well as 40 years.

- We know nothing about the profitability of this project, the competition that will inevitably come, and why Optimus will be needed by so many people.

So, the $25 trillion estimate has almost zero value as far as I am concerned. It was probably made to generate enthusiasm among investors, but it would be only a short-term consolation. Until proven otherwise, Tesla’s recent results are showing anything but a pleasant situation, and over the years the price per share will tend to its fair value.

Full Self-Driving (FSD) and Tesla Network

Elon Musk X profile

Tesla has already been talking about FSD for several years, and great progress has been made over the years. The problem is that legislation has failed to keep up with the technology, and today there are regulatory gaps in many states. Autonomous driving is allowed in some, in others it is not, and in others, it is allowed under certain conditions. In short, there is a lack of a federal law that can bring everyone together. In Europe and China, they are even more behind.

Future legislation to regulate FSD is a real risk for Tesla, as it is a technology never used on a global scale. But as well as Optimus, Elon Musk has no doubts about it:

We are fine that regulators are supportive of deploying deployment of that capability. It’s difficult to argue if you’ve got billions of miles that show that in the future unsupervised FSD is safer than humans. What regulator could really stand in the way of that? They’re morally obligated to approve. So I don’t think regulatory approval will be a limiting factor.

Unlike Optimus, I find his underlying reasoning here to be straightforward and clear; there is no doubt that autonomous driving can cause far fewer car accidents. However, there are in my view at least three obstacles to this:

- First, we do not know when there will be common regulation across countries; we do not know when FSD will begin to become widely deployed, assuming it can ever become so. Elon Musk may be too far ahead of schedule, and FSD could be implemented globally in 5-10-15 years, if not more. The world may not yet be ready for this revolution.

- Second, again there is no clear explanation of how profitable autonomous driving will be, and how profitability will be achieved. No one to date has presented such a business model, so we are facing uncharted territory.

- Third, but not least, if the world were dominated by self-driving cars many jobs would no longer exist. Personally, I do not see this as an impossible scenario, but it should be implemented in a phased manner so as not to create too great a disruption in the workforce. There would be many other considerations to make on this, this is just a starting point.

So, a business model based on autonomous driving is possible, but it depends on legislation, the people themselves (I doubt if everybody is in favor of it), and its profitability, which is not guaranteed at the moment. Overall, there is much uncertainty, yet Elon Musk has already given early estimates: in the long term, autonomous driving will add $5 trillion to Tesla’s market cap.

The plan to reach that figure seems quite complex, but that does not deter him at all. Basically, the ultimate goal is to create a Tesla app where there will be well over 20 million vehicles available 24/7 to take you wherever you want to go. In to some extent, this business segment would become a kind of Uber, but with Robotaxis. At the same time, we could almost compare it to Airbnb as well, because you can also make your Tesla available to make money from this service. In a hypothetical scenario where you know you don’t need the car for a few days, you can make it available to the app and have it work for you on those days. All of this may sound absurd today, but that is in a nutshell what the Tesla Network is getting at; a kind of Tesla fleet ready to take anyone, anywhere.

Just as with Optimus, here we are talking about an extremely ambitious project whose implementation is still in an early stage. As mentioned, there are many obstacles to overcome, and I do not believe that FSD currently can justify Tesla’s premium valuation.

Finally, it should not be overlooked that there is another major player in this market, namely Waymo, a company owned by Alphabet Inc. (GOOG) (GOOGL). Leaving aside the fact that Waymo may be better or worse than Tesla in autonomous driving, beating the Mountain View giant’s competition is certainly not easy. After all, with its annual free cash flow of over $60 billion, it can literally buy Tesla in less than a decade. By the way, just yesterday in the conference call it was announced that it intends to invest another $5 billion in this business:

With regard to other bets, we continue to focus on improving overall efficiencies, as we invest for long-term returns. Waymo is an important example of this, with its technical leadership coupled with progress on operational performance. As you will see in the 10-Q, we have chosen to commit to a new multi-year investment of $5 billion. This new round of funding, which is consistent with recent annual investment levels will enable Waymo to continue to build the world’s leading autonomous driving technology company.

CFO Ruth Porat, conference call Q2 2024.

Being part of Alphabet’s “Other Bets” segment, Waymo may so far not have received the attention it deserves: a possible IPO could really unlock its value. Investing $5 billion for Alphabet is pocket change; for Tesla, it’s basically 4 times last quarter’s free cash flow.

Conclusion

Tesla is a great company, but in my opinion, investors are assuming that there will be no impediment to the expansion of the FSD business and Optimus. Both could be the future, but we don’t yet know how, when, and whether that will actually be the case. Tesla’s valuation I believe does not deserve a premium based on these projects. Right now, the most important thing remains car sales, which are gradually declining over the quarters/years; same for profitability. Certainly, the 100% growth in Energy generation and storage revenue is good news, but it is not enough to compensate for the disappointing results of the core business and the billions invested in new projects.

Investors believe Elon Musk’s estimates are feasible; I don’t think so. Anyway, I do not rule out that the one in error could be me. In fact, I have no intention of shorting Tesla; I will simply observe its performance.

I conclude this article with one last food for thought. During the conference call, an interesting question was asked about the benefits Tesla received from the IRA tax credit and what the consequences would be if it were gone. Should Trump win the election, this could be a likely scenario. Elon Musk’s answer left me rather disoriented, as he not only did not answer the question but tried to deflect the topic, or at least that is my impression:

I guess that there would be some impact, but I think it would be devastating for our competitors. But it would hurt Tesla slightly. But long-term probably actually helps Tesla would be my guess. Yes — but I’ve said this before on earnings calls, the value of Tesla overwhelmingly is autonomy. These other things are in the noise relative to autonomy. So I recommend anyone who doesn’t believe that Tesla will solve vehicle autonomy should not hold Tesla stock. They should sell their Tesla stock. You should believe Tesla will solve autonomy, you should buy Tesla stock. And all these other questions are in the noise.

In the face of such an important question, I expected a detailed answer about Tesla’s situation, rather than deflecting the issue to how much trouble its competitors will be in. Even if they are, at least their P/E is not near triple digits. Moreover, it appears that the long-term potential of autonomous driving is so high that it will offset any negative news recently. Will this really be the case?

Analyst’s Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.