Summary:

- Meta Platforms is still reporting great quarterly results and we can also expect the business to perform great over the long run.

- We can also make the argument for Meta Platforms being at least fairly valued right now.

- Nevertheless, we should be very cautious right now as the next few years might be challenging and I’m staying to the sidelines.

peshkov

Last week, on July 31, 2024, Meta Platforms Inc. (NASDAQ:META) reported second quarter results and not only did the business beat estimates for revenue as well as earnings, but the company also reported solid second quarter results and increased its top and bottom line with a high pace. Following earnings, the stock also jumped as one would expect on this news, but in the last few days since earnings were published it seems like the “bigger picture” took over and indices all around the world are suddenly in free-fall – especially in Japan the situation seems dire.

In my last article about Meta Platforms published in February 2024, I was still bullish about Meta Platforms but also argued that the bullish case was getting weaker. My conclusion included the following statement:

Over the long run, Meta Platforms is still a great investment, and I am confident Meta Platforms will trade for higher stock prices in five or ten years from now. And I also assume that the stock can run up to about $600 in the coming months (or quarters). Nevertheless, I would be a little more cautious at this point as a larger correction in the coming months gets more and more likely. A technical correction would also be the major risk I am seeing for Meta Platforms in the next few quarters and whoever is buying now might be a little late to the party or should at least not expect similar returns as in the last 12 months for the next 12 months.

And it seems like I might have been right with my statement although Meta Platforms did not run up to $600 (it reached $542 at least). It probably was a good call to turn rather cautious, but looking back I probably should have been even more cautious and rate the stock as a “Hold” already.

In the following article, I will get more cautious and definitely rate Meta Platforms only as a “Hold”. But I will explain once again why I think Meta Platforms is a great long-term investment with investors needing nerves of steel in the next few years (not only with Meta Platforms investors, I think investors will need nerves of steel in general, almost every stock investor will).

Quarterly Results

Let’s start with the last quarterly results – and as mentioned above they were great once again. But it is difficult to draw conclusions from past results as the fundamental business is often lagging investor sentiment and it also takes several months before results reflect troubles.

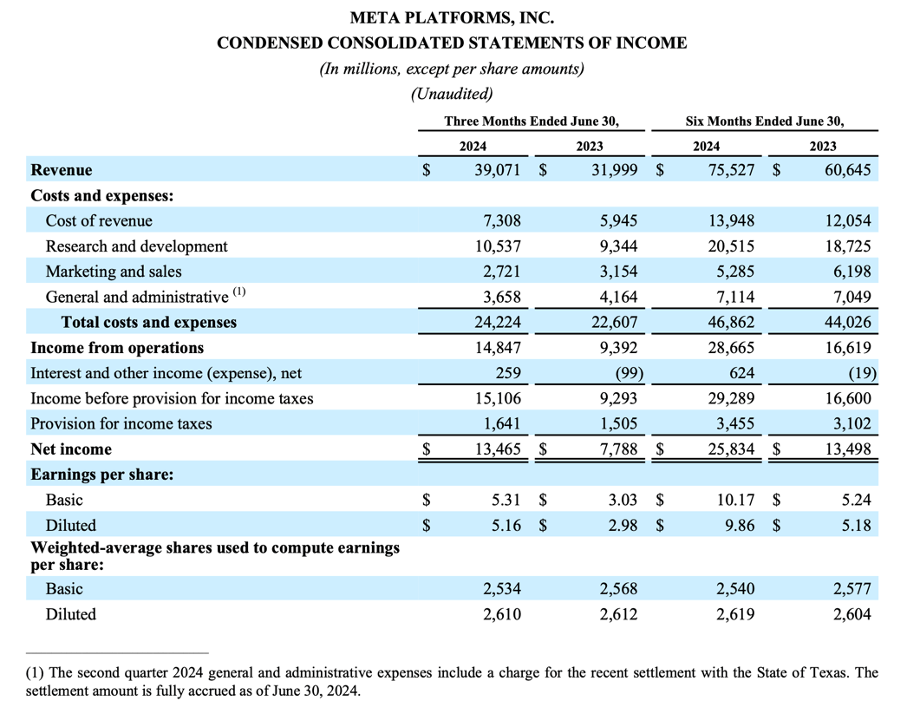

Revenue for Meta Platforms increased from $31,999 million in Q2/23 to $39,071 million in Q2/24 – resulting in 22.1% year-over-year top line growth. Income from operations increased 58.1% year-over-year from $9,392 million in the same quarter last year to $14,847 million this quarter and diluted earnings per share increased even 73.2% year-over-year from $2.98 in Q2/23 to $5.16 in Q2/24. Only free cash flow declined slightly from $10,955 million in the same quarter last year to $10,898 million this quarter – resulting in 0.5% year-over-year decline.

Meta Platforms Earnings Release Q2/24

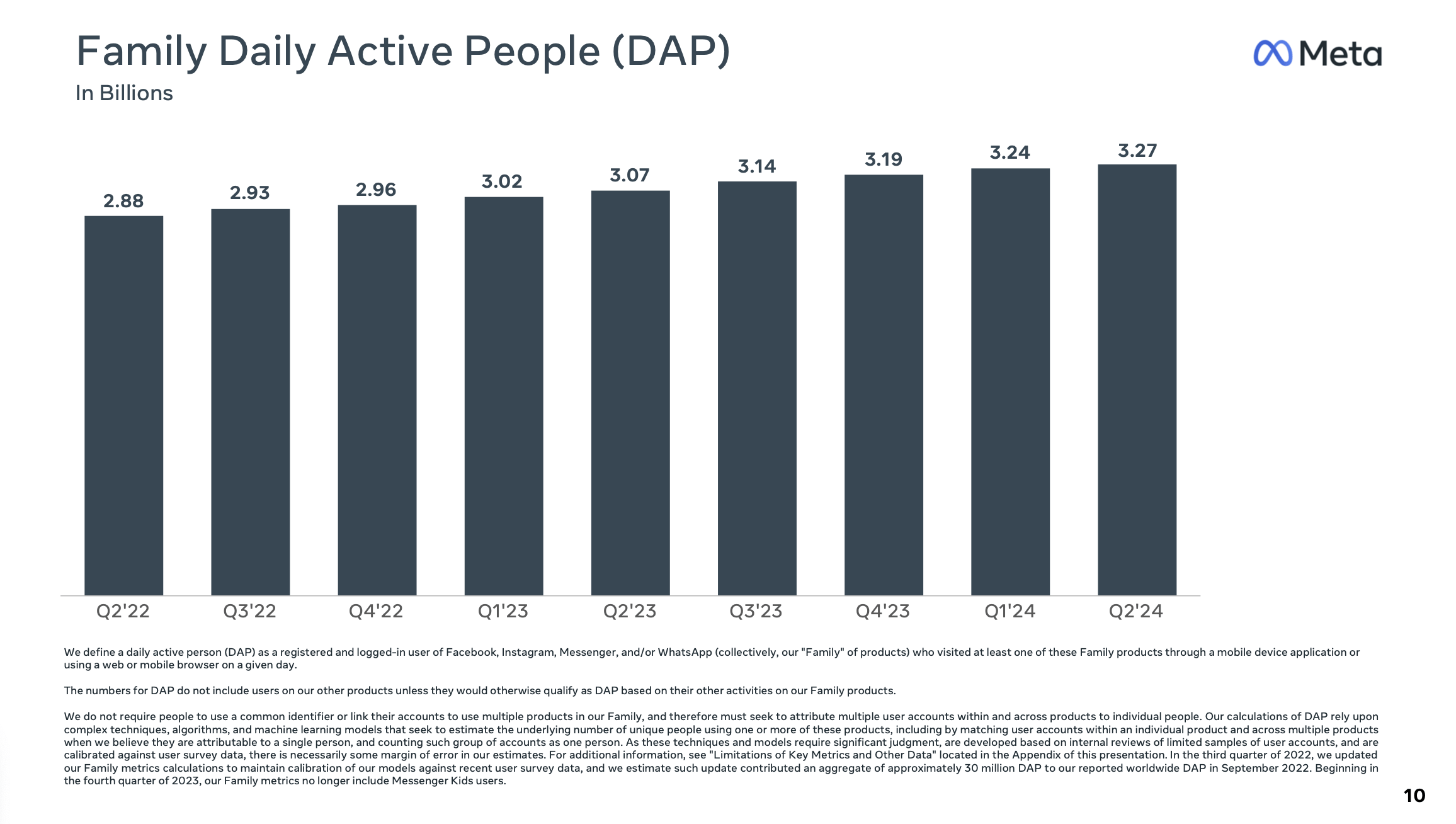

And not only the income statement is great. When looking at other metrics, Meta Platforms is also performing great. The daily active people within the Family of Apps increased from 3.07 billion in Q2/23 to 3.27 billion in Q2/24 – resulting in 6.5% year-over-year growth.

Meta Platforms Q2/24 Presentation

Additionally, ad impressions delivered also increased 10% year-over-year (with growth being especially high in the Asia-Pacific region). And average price per ad increased also 10% year-over-year (with growth being especially high in Europe and “Rest of World). Overall, the average revenue per person for the Family of Apps increased 14.1% year-over-year from $10.42 in the same quarter last year to $11.89 this quarter.

Zuckerberg Going All-In Again?

It seems like investors are getting scared once again that CEO Mark Zuckerberg might start spending huge amounts of money on projects that are not contributing to revenue or take several years or a decade before they might pay off (a situation that seems familiar). It probably was statements like the following take by Zuckerberg:

At the end of the day, we are in the fortunate position where the strong results that we’re seeing in our core products and business give us the opportunity to make deep investments for the future. And I plan to fully seize that opportunity to build some amazing things that will pay off for our community and our investors for decades to come.

Or the outlook provided by CFO Susan Li had a similar vibe:

For Reality Labs, we continue to expect 2024 operating losses to increase meaningfully year-over-year due to our ongoing product development efforts and investments to scale our — to further scale our ecosystem. While we do not intend to provide any quantitative guidance for 2025 until the fourth quarter call, we expect infrastructure costs will be a significant driver of expense growth next year. As we recognize depreciation and operating costs associated with our expanded infrastructure footprint.

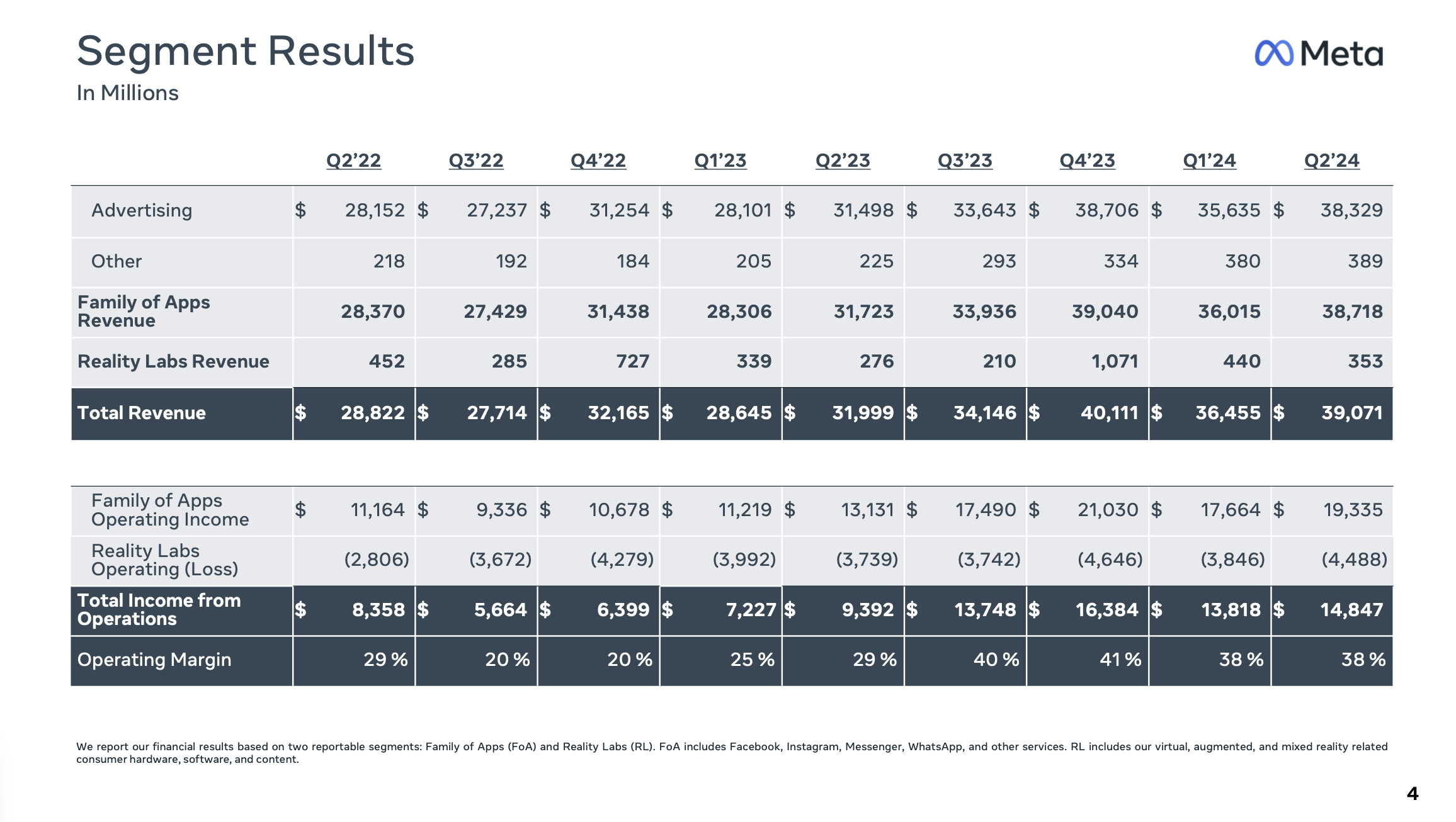

And we can understand the skepticism of investors a little bit. When looking at the segment results, it is still the Family of Apps, which is responsible for the entire operating income and almost all revenue. Reality Labs generated $353 million in revenue. Compared to the same quarter last year ($276 million in revenue), the segment increased revenue 27.9% year-over-year, but it is still only responsible for less than 1% of total revenue and still had to report a huge operating loss of $4,488 million. Compared to the same quarter last year, the operating loss increased as it was “only” $3,739 million in the same quarter last year. While revenue growth was driven by Quest headset sales, operating loss was driven by headcount-related expenses and inventory costs.

Meta Platforms Q2/24 Presentation

I personally believe in the long-term vision of Meta Platforms and Mark Zuckerberg, and I think the investments will pay off at some point in time. But we should not forget that Meta Platforms is not only about the metaverse and a long-term vision but also has a profitable business with a wide economic moat.

Long-term Vision

Meta Platforms is not only investing in long-term growth (the metaverse) but also investing in its core business and future growth projects that will generate revenue not only in a decade from now.

Threads

For starters, Threads is progressing well and during the earnings call, Zuckerberg reported that the app is about to hit 200 million monthly active users. And although Zuckerberg is reporting deeper engagement it probably will take years before the app is generating enough revenue or contributes to profits.

WhatsApp Business Messaging

Another promising segment is business messaging on WhatsApp, which is the biggest contributor to the “Other revenue” among the Family of Apps. This segment generated $389 million in revenue in the last quarter and year-over-year reported 72.9% year-over-year growth. During the last earnings call, Mark Zuckerberg also pointed out that Business AI, which is currently in alpha testing, could be a major contributor to revenue:

Over time, I think that just like every business has a website, a social media presence, and an email address, in the future I think that every business is also going to have an AI agent that their customers can interact with. And our goal is to make it easy for every small business, eventually every business, to pull all of their content and catalog into an AI agent that drives sales and saves them money.

When this is working at scale, I think that this is going to dramatically accelerate our business messaging revenue. There are a lot of other new opportunities here that I’m excited about too, but I’ll save those for another day when we’re ready to roll them out.

Core Business

And while Threads and Business Messaging can drive growth in the years to come, the major part of revenue and operating is still stemming from the core business – the advertising business. And this business will be driven by two different factors (as management pointed out during the last earnings call). Revenue performance will be driven by the ability to deliver engaging experience as well as the effectiveness at monetizing that engagement over time.

The first factor is Meta Platform’ ability to deliver engaging experiences. And Meta Platforms is especially focused on including video and in-feed recommendations. More than half of recommendations in the United States is coming from original posts and especially in India retention and engagement on WhatsApp is particularly promising. Aside from driving engagement, Meta Platforms also must monetize this engagement. And in improving monetization efficiency, artificial intelligence is playing a central role. Meta Platforms is improving ad delivery by adopting more sophisticated modeling techniques made possible by AI advancement (like the Meta Lattice ad ranking architecture). And with the company’s Advantage + suite of solutions, a 22% higher return on ad spend for U.S. advertisers can be reported.

During the last earnings call, Zuckerberg also mentioned that Facebook is obviously becoming more popular again with young users, which is a good sign:

I’m particularly pleased with the progress that we’re making with young adults on Facebook. The numbers we are seeing, especially in the US, really go against the public narrative around who’s using the app. A couple of years ago, we started focusing our apps more on 18 to 29 year olds and it’s good to see that those efforts are driving good results.

Intrinsic Value Calculation

Now it gets trickier. As always, we are also calculating an intrinsic value by using a discount cash flow calculation or we look at simple valuation metrics to determine if a stock is a good investment or not. And in case of Meta Platforms, we have a business constantly reporting high growth rates (still double-digit growth although growth rates slowed down) and analysts are also expecting high growth rates for the years to come. And as argued above, we have plenty reasons to expect solid growth for Meta Platforms over the long run.

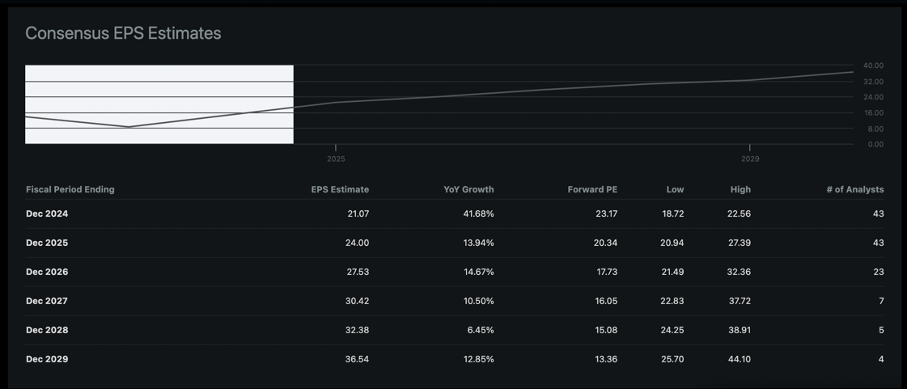

In the last three years, Meta Platforms grew revenue with a CAGR of 16.21%, operating income with a CAGR of 12.69% and earnings per share with a CAGR of 13.80%. When looking at longer timeframes, the annual growth rates are even higher. And between fiscal 2024 and fiscal 2029, analysts are expecting earnings per share to grow with a CAGR of 11.64%.

Seeking Alpha Earnings Estimates

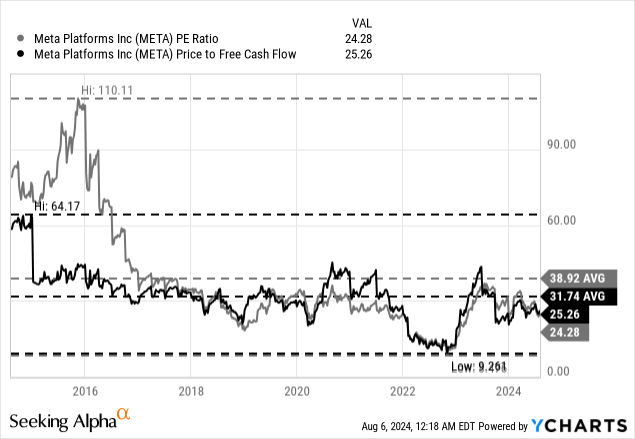

On the other hand, we have a stock trading for reasonable valuation multiples. At the point of writing (and in a volatile environment), the stock is trading for around 25 times earnings as well as 25 times free cash flow and for a business which seems to be able to grow in the double digits with a high level of consistency such a valuation multiple certainly seems reasonable.

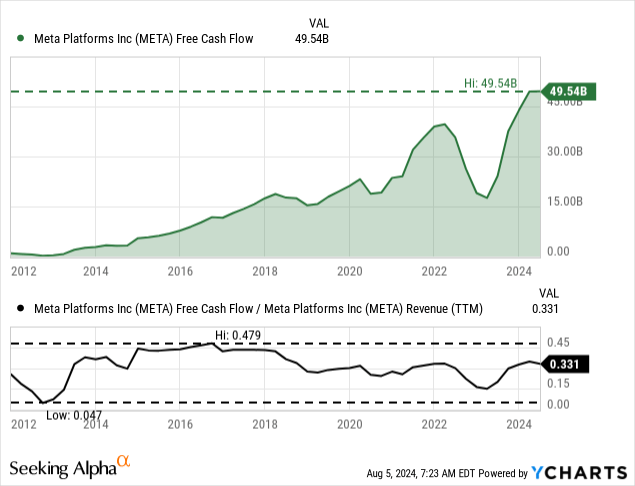

We can also use a discount cash flow calculation to determine an intrinsic value for the stock. As basis for our calculation, we can take the free cash flow of the last four quarters, which was $48,573 million. Additionally, we are calculating with a discount rate of 10% and with 2,610 million outstanding shares. When calculating with these assumptions, Meta Platforms must grow 6% annually from now till perpetuity in order to be fairly valued and when looking at previous growth rates as well as expected growth rates, we should argue that Meta Platforms is at least fairly valued and if the stock will continue to drop it might quickly become a bargain.

But we must keep in mind that the free cash flow in the last four quarters was the highest number Meta Platforms reported on a trailing twelve-month basis. However, when comparing free cash flow to revenue, Meta Platforms is generating about 33 cents of free cash flow from every dollar of revenue – a metric in line with past numbers and far away from the peak a few years ago. And although current revenue is not unrealistic high, we must keep in mind that in case of a global recession advertising revenue will probably stagnate or even decline. And with a lower free cash flow and maybe declining top and bottom line, investors suddenly might not attribute a 25 times valuation multiple to the stock anymore.

And we must also keep in mind that 6% growth till perpetuity is a high growth rate. A business growing at such a rate till perpetuity would constantly grow (at least) at twice the pace of the overall economy in the United States. History has shown us several examples of companies outpacing GDP growth for several decades and I think Meta Platforms could also be one of these companies. But we can also make the argument that we should not calculate with more than 3% growth till perpetuity. And in that case, Meta Platforms has to grow between 12% and 13% in the next ten years to be fairly valued – a growth rate that the company might not achieve in the next few years (considering a looming recession).

A Warning

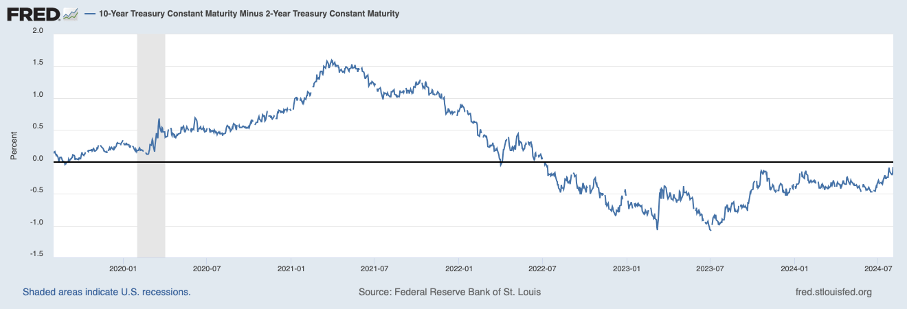

In the last few days, the global stock markets suddenly shocked investors with high levels of volatility and especially the stock market in Japan declined steeply. And I certainly will not say I told you so at this point as I certainly did not know the stock market will decline now. But I have mentioned again and again that we should be cautious as the stock market is extremely overvalued and I warned that the inverted yield curve is sending a strong warning sign for an upcoming recession and bear market in the United States.

The market will probably not plummet in a straight line and of course there is always the possibility of the stock going higher again. But the yield curve (especially the 10-year minus 2-year treasury yield) is giving us another warning sign. After the yield curve inverted several quarters ago, the yield curve is now getting close to re-inverting again – another step that almost always happened before a recession.

FRED

And Meta Platforms is neither cheap nor expensive at this point and the stock is not trading at unreasonably high valuation multiples like some other AI-related stocks or other hyped stocks. But I still see the risk of Meta Platforms declining rather steep in case of a global recession and steep bear market.

Conclusion

Meta Platforms is a great business and a great long-term investment. And I personally will hold on to my shares and I am pretty confident in 10 years from now the stock will trade at a higher price than right now. Nevertheless, I don’t think now is the time to buy and over the coming quarters I rather see the stock at $400 or $300 than at $500 or $600.

And although the stock might seem undervalued at $400 or lower, we should be extremely cautious. The stock will plummet first before the business will follow and although Meta Platforms will grow over the long run, it might certainly take a hit in the next few years. We should stay to the sidelines at this point and Meta Platforms – like many other high-quality businesses – is only a “Hold”.

Analyst’s Disclosure: I/we have a beneficial long position in the shares of META either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.