Summary:

- Keith Gill, also known as Roaring Kitty, expresses belief in GameStop’s ability to reinvent its business model and highlights confidence in management.

- GameStop’s substantial cash reserves of nearly $4 billion offer real option value for exploring new business opportunities and rejuvenating its market position.

- The article proposes a transformation strategy for GameStop, including the establishment of a digital storefront, a subscription-based gaming service, and the acquisition of exclusive content.

- While I do acknowledge that a GameStop investment is highly risky, I believe that the value of the company’s implied real options exceeds the company’s market cap of <$10 billion.

Dennis Diatel Photography/iStock Editorial via Getty Images

The GameStop (NYSE:GME) hype is back. Following a volatile ride for GameStop shares over the past few weeks, on Friday Keith Gill, also known as Roaring Kitty on X and YouTube and u/DeepF***ingValue on Reddit, returned to YouTube to express his belief that GameStop’s business model could be reinvented and to emphasise his confidence in the company’s ability to do so. Roaring Kitty said:

I wanted to hop on [the stream] and re-iterate viewpoints that I held previously […] There was a two part thesis two it. And the second part of the thesis was related to a reinvention of the business model, or a transformation. We are [now] in that second part of that […] What could they transform into […] It becomes a bet on management, in particular Ryan Fu***** Cohan and his crew […] Also, you have a company with so many people rooting for it, myself included. And they are sitting on billions and billions of dollars of cash.

For context, Gill attracted more than half a million visitors to his livestream.

In a nutshell, Keith argued that investing in GME is essentially a bet on Ryan Cohen and his management team–something that is hard to value, but substantial in value nevertheless. In this article, I try to expand on Roaring Kitty’s argument about GameStop through the lens of real options. Real option theory rejects the idea that the valuation of a company is simply a function of tangible, value (like stable cash flows and assets), and adds the idea that the value of potential investment is also a consideration of implied “options” that a company might have in the future. This approach is particularly relevant in situations where there is significant uncertainty and flexibility in decision-making.

While I do acknowledge that an investment in GameStop is a highly risky proposition with potential for significant loss of capital, I also point out that GameStop’s implied value anchored on real options theory is irrefutable: With close to $4 billion cash, GameStop management does have the capital to explore a complete business model reinvention within the $350 billion global game market.

A Brief Look At The Legacy Business

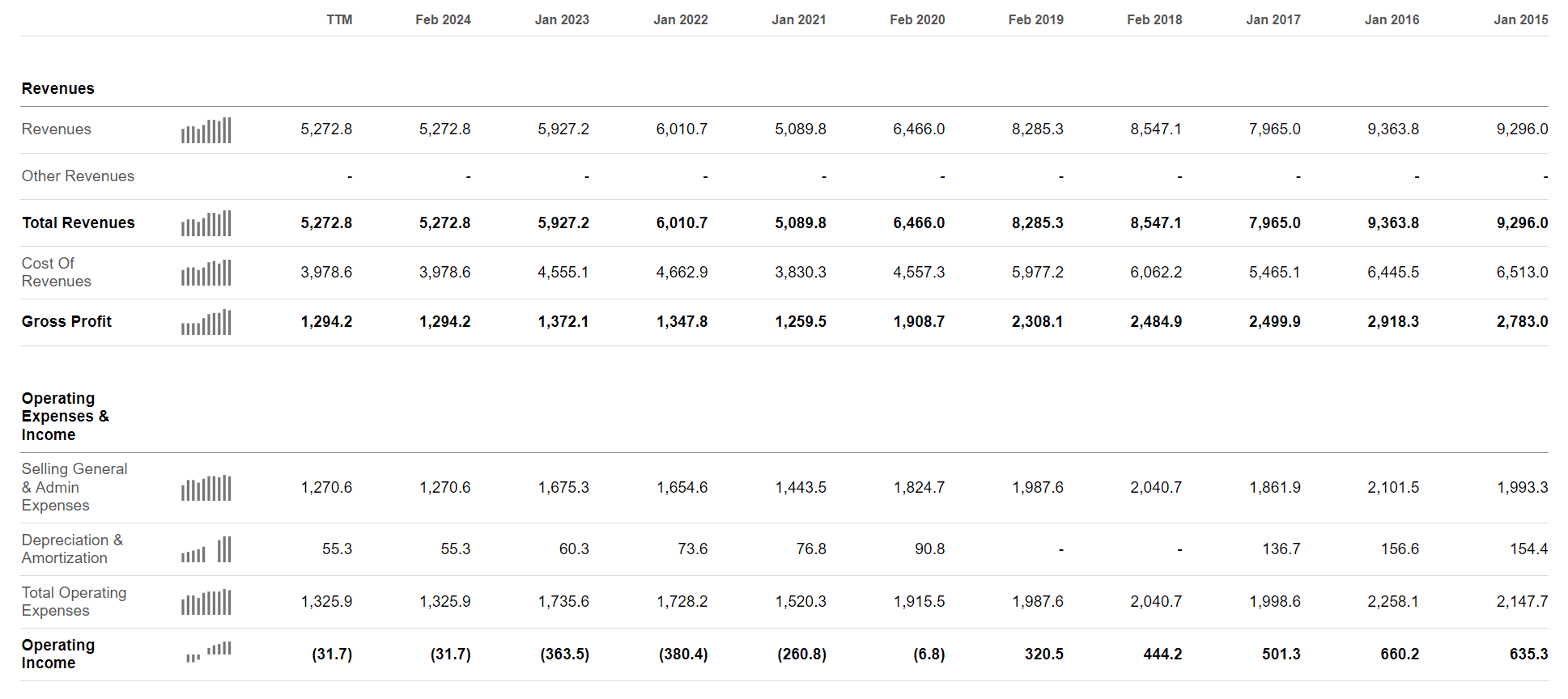

GameStop, historically recognized for its brick-and-mortar retail business in the gaming industry, has faced significant challenges in recent years. With the gaming market increasingly shifting towards digital platforms, the company has seriously struggled to remain relevant and profitable. On that note, sales dropped from $9.3 billion in 2015 to $5.3 billion for the trailing twelve months, reflecting a negative CAGR of approximately 7%. Over the same period, operating income slumped from positive $635 million, to negative $32 million.

Seeking Alpha

Q1 2024 was more of the same–giving indication of a struggling legacy business. During the period from January to end of March 2024, GameStop’s revenues were $882 million, down from $1.24 billion for the same period one year earlier. And while Selling, general and administrative expenses improved to $295 million (vs. $346 million in Q1 2023), net loss for the first quarter was $32.3 million. On the bright side, GameStop closed Q1 with little financial debt (emphasis mine).

long-term debt remains limited to a low-interest, unsecured term loan associated with the French government’s response to COVID-19.

Projected $4 Billion Cash Reserves Offers Strategic Real Option Value

Together with preliminary Q1 results, GameStop also submitted a SEC filing that would allow GameStop to raise equity capital by selling up to 75 million common shares in the open market. This share issuance is additional to the 50 million share sale announced less than one month earlier (already completed with close to $1 billion in proceeds). Projecting a successful share sale of the 75 million shares program at an average price of about $25-30 dollar would suggest that GameStop is on track to end Q2 2024 with close to $4 billion of cash. Please note that this is a projected figure based on the assumption that GameStop manages to sell all 75 million shares at a $25-30 price range. The final number could be different to $4 billion – also higher.

This is where things get interesting: GameStop’s substantial cash reserve of nearly $4 billion now offers the company real option value, providing strategic flexibility to explore new business opportunities and potentially rejuvenate its market position. In fact, with $4 billion of cash, GameStop’s strategic options are not merely limited to restructuring of its core business, but expand to bold M&A and new venture opportunities, which could shift the company’s core business by 180% (figuratively speaking).

Understanding Real Options …

Real options provide management with the right, but not the obligation, to undertake certain business initiatives, allowing companies to adapt to changing economic, technological, or market conditions. Unlike financial options, which are traded securities, real options pertain to tangible assets or strategic decisions that can enhance a company’s future value. These options include opportunities to expand, defer, or abandon projects, providing economic value and strategic flexibility.

… And What GameStop Management Could Do

Now with, $4 billion of cash GameStop management’s optionality is extensive, and even a Monte Carlo Simulation may fail to project all the possible outcomes of future events. Currently, GameStop management has not been very vocal sharing insights into the company’s strategy. In a broader context, however, I expect Ryan Cohan and Co. to push towards a platform business model for digital games distribution or streaming, positioning itself as the Netflix of gaming. (Note that also Netflix reinvented itself from a struggling DVD rental service to a highly successful digital platform streaming business).

If investors find that GameStop does address the strategic steps as outlined below, then there is a strong argument for a GME bull case, in my opinion. If GME rejects or fails to address these issues, then the company’s real option value would likely shift materially.

Become The Netflix Of Game Streaming

In my view, this transformation hinges on three strategic pillars: the expansion of a (1) digital storefront, the (2) launch of a subscription service paired with significant investment in cloud gaming technology, and the (3) acquisition of exclusive content alongside robust community-building efforts.

In more detail, the first pillar to transform GameStop should involve establishing a digital storefront that offers an extensive digital library that offers a wide range of games, from AAA blockbusters to indie gems. In that context, GME would be emulating the successes of platforms like Steam and Epic Games Store. The second pillar of GameStop’s transformation strategy is the launch of a subscription-based gaming service, coupled with a significant investment in cloud gaming technology. This new service will operate similarly to Xbox Game Pass or PlayStation Now, providing users with access to a vast array of games for a monthly fee (think streaming). Such a service will create recurring revenue streams. Offering tiered subscription plans with varying benefits can attract both casual and hardcore gamers. The third pillar focuses on differentiating GameStop through exclusive content and fostering a strong community. On that note, securing exclusive content by partnering with game developers will be a key differentiator. GameStop may even decide to develop its own games (another real option the company has).

GameStop can leverage its strong brand recognition and loyal customer base to develop a comprehensive digital gaming platform, positioning itself as a direct competitor to established digital storefronts like Steam, Epic Games Store, and GOG. By investing in platform development, introducing subscription services, and forming exclusive partnerships, GameStop can create a unique value proposition. This expansion provides flexibility in scaling the platform and diversifies revenue streams, reducing reliance on declining physical game sales.

Transform Into All-You-Can-Play Stores

Together with building the streaming service, GameStop should downsize its store count in underperforming locations, while repurposing the remainder of stores towards all-you-can-play amusement parks. In that context, GameStop stores could transform into a vibrant, interactive gaming space where customers can pay a flat fee to access a wide variety of games and gaming experiences for a set period. These repurposed stores would feature the latest consoles, VR setups, arcade machines, and perhaps even dedicated areas for competitive gaming and tournaments. The idea is to create a social environment where gamers can explore new titles, participate in gaming events, and enjoy a communal gaming experience. On a more emerging growth perspective, GameStop could be utilizing physical stores for VR/AR demonstrations establish GameStop’s relevance for the next leg of

Estimating GameStop’s Real Option Value

I propose to calculate the implied real option value for GameStop using the Black-Scholes model adapted for real options. In that context, we’ll need to make several key assumptions. Here are the assumptions we’ll need:

- Current Value of the Project: The present value of expected future cash flows from the digital platform project.

- Exercise Price: The cost required to implement the option (e.g., the investment needed for the digital platform development).

- Time to Expiration: The time period over which the option is valid, typically representing the time frame for decision-making

- Volatility: The standard deviation of the project’s returns, representing the uncertainty or risk associated with the project’s cash flows.

- Risk-Free Rate: The risk-free rate of return over the option period, usually based on government bonds or similar instruments.

Now, let’s define these assumptions more concretely for GameStop’s business model reinvention upside:

- Current Value of the Project: I advise every investor/reader to apply their own assumption here. Personally, I like to build on the Netflix comparison, and argue that a 10x P/B value on a successful streaming transformation should be reasonable. Projecting GameStop’s tangible book value at $4,300 billion by end of Q2 2024. Moreover, I apply a 33% probability of success to the projects, so my final estimate would trend towards $12.900 billion.

- Exercise Price: I argue that the exercise price needed to capture the value of the project is equal to GameStop’s cash position, $4.000 billion.

- Time to Expiration: Give the strategic, long-dated nature of the project, I go with 5 years

- Volatility: I propose to anchor the volatility estimate on excess share price volatility, above what. While this is hard to estimate, 150% looks reasonable to be.

- Risk-Free Rate: Probably an estimate close to the 10-year yield is fair, thus 4%

Plugging these values into the black-scholes formula suggests that the real options value of GameStop’s transformation upside is about $12.3 billion (compared to a market cap of <$10 billion currently).

What To Consider

Quantifying the precise value of real options can be challenging due to their inherent uncertainty and the subjective nature of potential future benefits. Moreover, successfully implementing new digital and technological initiatives requires significant investment and time, with potential risks of execution failure. I also highlight that the valuation is very sensitive to assumptions (like all valuation estimates), and I advise every investor/reader to apply their own assumptions for valuation purposes. On that note, my valuation exercise presented above should not be viewed as an accurate valuation takeaway, but more like a stimulating, intellectual exercise to open a discussion about value beyond tangible, predictable cash flows. At the same time, investors should consider that GameStop’s has multiple real options, whose intrinsic value should be stacked together (as far as projects are not mutually exclusive).

Conclusion

In my opinion, and as Keith Gill also pointed out on the stream, GameStop’s $4 billion cash reserve provides substantial real option value, offering strategic flexibility to navigate its struggling core business and explore new opportunities. By leveraging real options in digital expansion, technological innovation, strategic partnerships, and operational optimization, GameStop has optionality to capture new opportunities for growth and value creation.

Charlie Munger, Warren Buffett’s long-term business partner in value investing once termed the Lollapalooza Effect, which refers to the phenomenon where multiple factors act together to produce a large, often extraordinary, outcome. In that context, I argue that GameStop’s potential to mix a Lollapalooza Effect is irrefutable, as the company owns a notable brand in a multi-billion market, enjoys strong consumer support, committed and capable management team, as well as $4 billion in cash (with the ability to raise even more capital). So, concluding, while I do acknowledge that a GameStop investment is highly risky, I believe that the value of the company’s implied real options exceeds the company’s market cap of <$10 billion.

Analyst’s Disclosure: I/we have a beneficial long position in the shares of GME either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Not financial advice

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.