Summary:

- Warren Buffett???s Berkshire Hathaway increased its stake in OXY to 29%, with 255.3 million shares, showing strong confidence in the company???s management and strategic direction.

- Occidental reported $2 billion in total operational cash flow and $2.4 billion in cash flow before working capital, demonstrating solid operational performance.

- Occidental acquired CrownRock for $12 billion, boosting its inventory by 33% at sub-$40-a-barrel break-even and expecting to increase output by 170,000 barrels of oil equivalent per day by 2024.

- Occidental is investing $600 million in the STRATOS direct air capture plant in Texas, aiming to remove 500,000 tons of CO2 annually, backed by a $550 million strategic partnership with BlackRock.

jetcityimage

Investment Thesis

Operational excellence, a diversified portfolio, and free cash flow growth ensure that Occidental Petroleum (NYSE:OXY) remains one of Warren Buffett’s top picks in the energy space. Buffett has already purchased 255 million shares, making up 29% of the oil and gas company’s ownership. Buffett continues to build his stake in the company, as it looks like a bargain at these levels.

Since our last coverage in January, OXY’s stock price has increased from $58 to $62, reflecting a gain of 7%. Our previous bullish thesis remains intact, supported by steady progress in financial performance and strategic initiatives. OXY’s long-term potential is bolstered by Buffett’s continued confidence and the company’s strategic growth efforts.

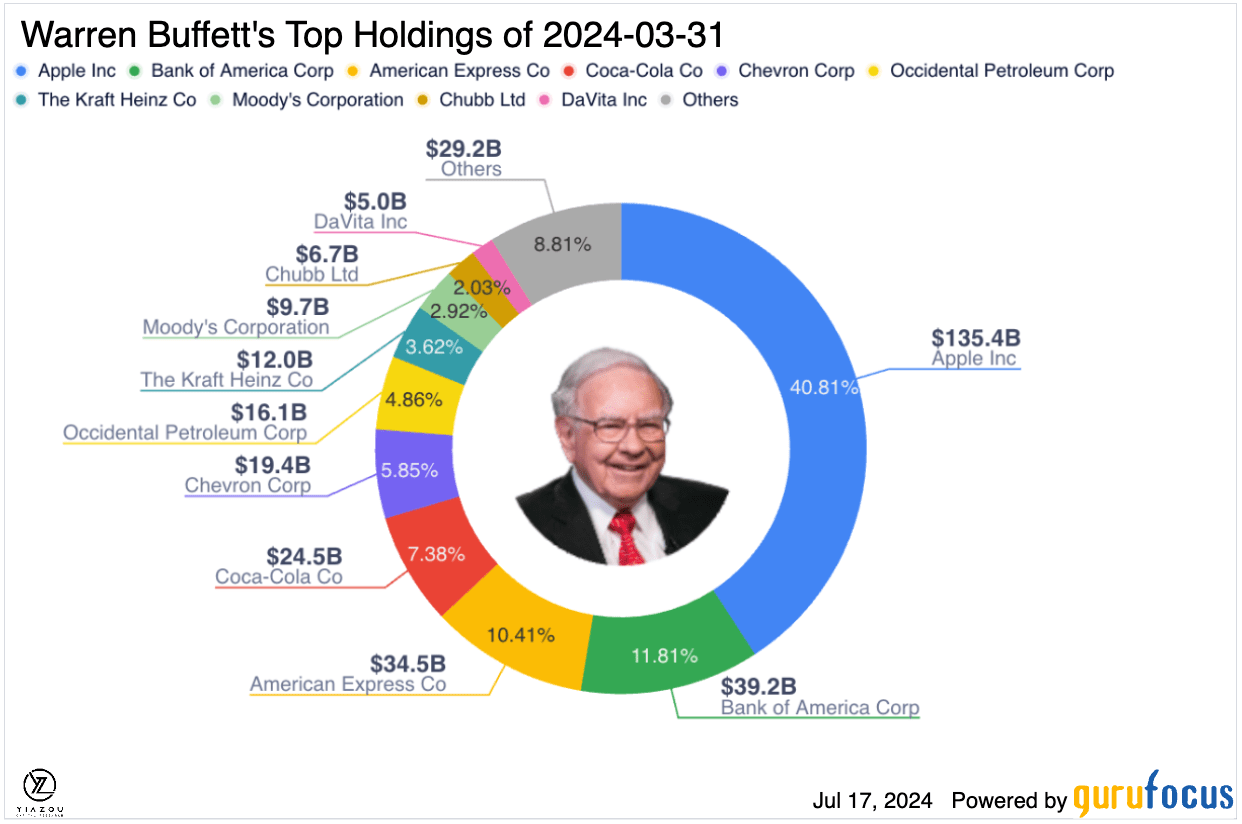

Buffett Boosts Occidental Stake to 29%, Eyes Potential 40% Without Full Control

Warren Buffett continued purchasing shares of Occidental Petroleum, which seemed to bring its stake up to 28.8% with nearly 255.3 million shares. This makes Occidental Berkshire’s sixth-biggest holding. The common shares include the warrants to buy 83.9 million more at $59.62 each and Berkshire’s 84,897 shares of preferred stock. The warrants’ exercise and preferred redemption could bring Berkshire’s ownership above 40%. Though that’s possible, Buffett has publicly proclaimed that he won’t take control of the company.

Warren Buffett made a massive investment in Occidental because he had a lot of faith in the management and the strategy that this company adopted. He started buying after reading through a transcript of an earnings call and felt that the approach was well aligned with his investment philosophy. He praised Occidental CEO Vicki Hollub for managing well. The recent increase in stake shows continued confidence in performance and strategic direction for the firm.

GuruFocus

Occidental Thrives With $2 Billion Cash Flow and Rising Output

The investment spree is driven by Buffett’s confidence in Chief Executive Officer Vicki Hollub, a sentiment confirmed by the recent financial results. The oil and gas juggernaut benefited from solid operational performance, as teams delivered at high levels across oil and gas, OxyChem, midstream, and marketing segments. Consequently, total operational cash flow totaled $2 billion, and cash flow before working capital reached $2.4 billion.

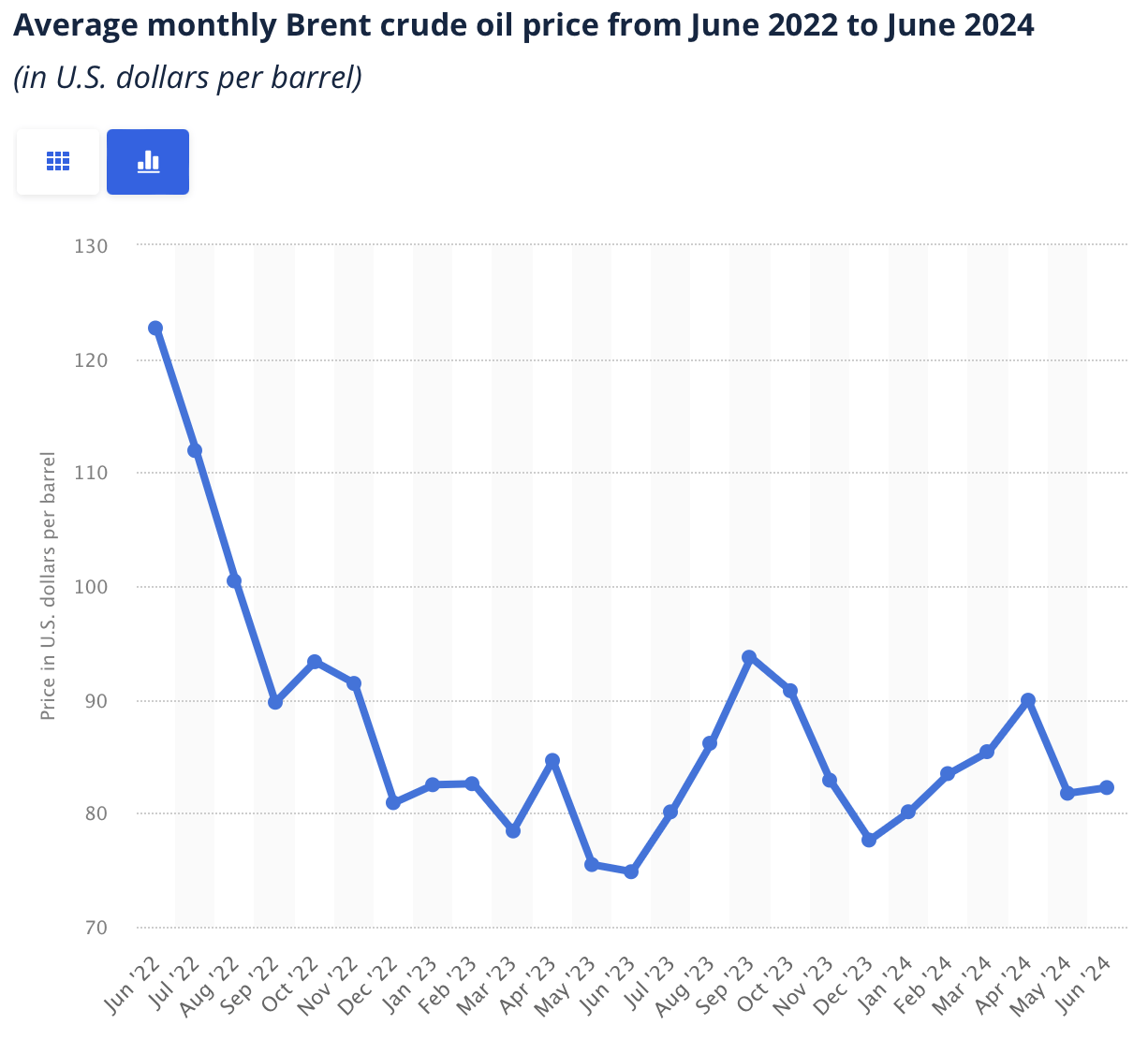

The company delivered a net income attributed to shareholders of $718 million or $0.75 a share and adjusted income of $604 million or $0.63 per diluted share. It generated $1.2 billion in oil and gas pretax income compared to $1.6 billion in the fourth quarter. The slight drop was due to lower crude oil prices and domestic crude volumes. Average crude prices were down by about 4% in the quarter, averaging around $76 a barrel.

Despite worries that crude oil might face challenges due to the move towards other forms of energy, the complete elimination of fossil fuels is yet to be anticipated in the near future. The main business of producing crude oil is still solid, particularly with the International Energy Agency (IEA) predicting that worldwide oil use will rise from 103.2 million barrels a day to 105.6 million by 2030.

The expectation of only a slight decrease in oil demand after 2030 is why Buffett is very optimistic about the oil company’s future. The company has been increasing its output, achieving an average of 1.1 million barrels of oil daily in the first quarter, which is close to the middle of its expected range.

statista

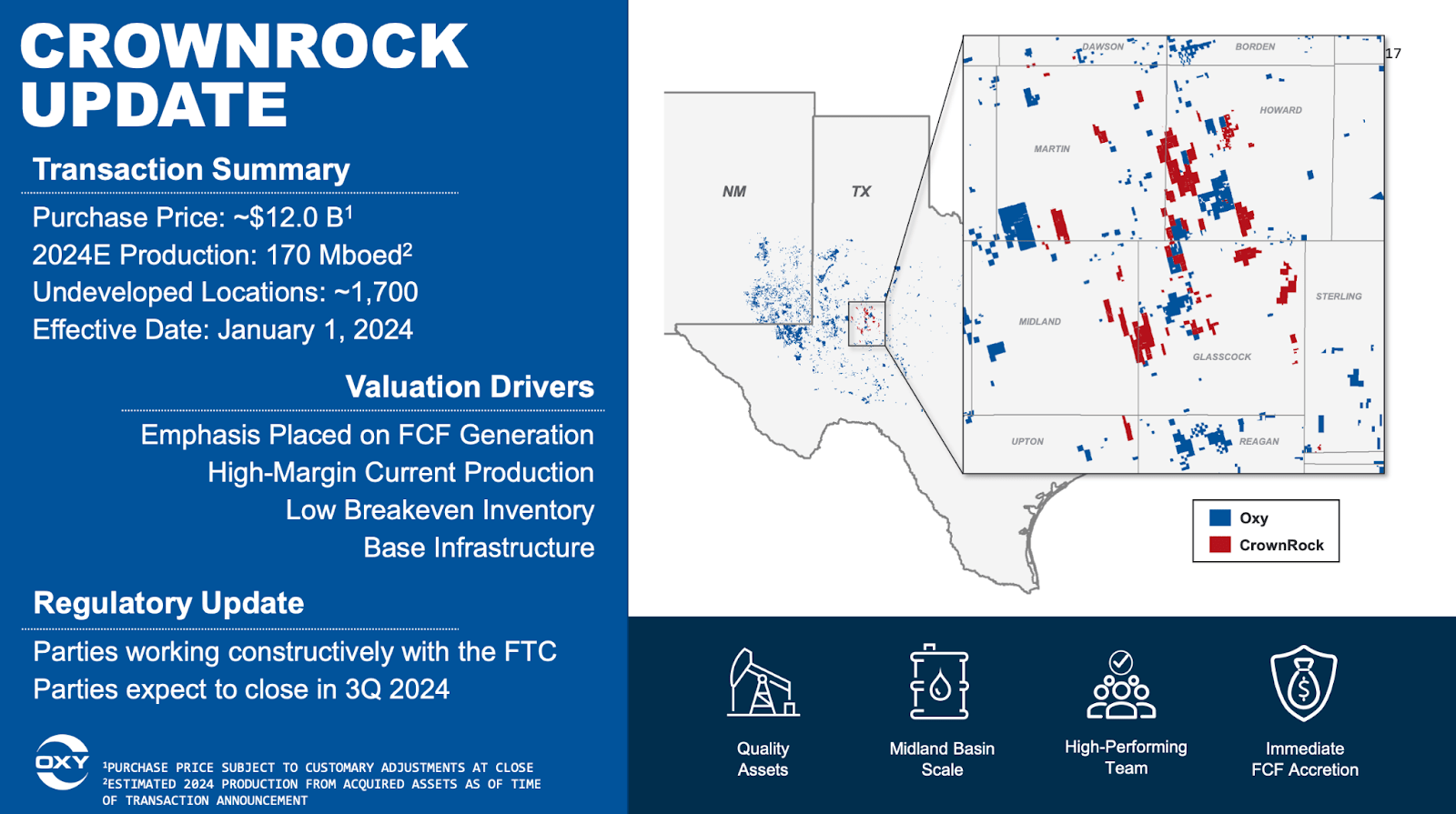

OXY Expands Permian Power: $12 Billion CrownRock Deal to Boost Production and Cash Flow

Occidental Petroleum has also moved to enhance its foothold in the Permian Basin to bolster production by acquiring CrownRock for $12 billion. With the acquisition, the company will expand its presence into the largest oilfield. It is also acquiring a critical low-breakeven and development-ready inventory in the Permian Basin through CrownRock, which owns over 94,000 net acres of premium pay assets and infrastructure.

The deal would strengthen the company’s inventory levels by 33% at a break-even price of sub-$40 a barrel. The agreement is expected to boost output by 170,000 barrels of oil equivalent per day by 2024. Meanwhile, the CrownRock buyout should also see annual free cash flow surge by $1 billion when oil pricing stabilizes north of $70 per barrel.

In addition, after completing the CrownRock buyout deal, OXY expects to divest $4.5 billion to $6 billion. Following the sale, the company must pay a portion of its outstanding principal debt below $15 billion. The firm expects the debt reduction to enable its resumption of stock repurchases under COG’s commitment to returning value to shareholders.

OXY

Expanding Chemical Business and Carbon Capture for $1 Billion Non-Oil Earnings by 2026

In addition to pursuing growth in the lucrative oil and gas business, Occidental Petroleum has also been diversifying its business empire as it positions itself for the future. The company has been investing and expanding its chemical business as it continues to build a carbon capture and storage platform. The investments are expected to grow the company’s non-oil earnings by over $1 billion by 2026.

OxyChem is the company’s chemical business that manufactures vinyl basics and specialty chemicals used in pharmaceuticals, water disinfectants, and detergents. The unit generates significant cash flows that have helped shrug off some volatility in the core oil and gas business. For instance, it earned a pretax income of $260 million in the first quarter, which was $10 million above the guidance.

The $10 million increase was driven mainly by strong demand for the company’s polyvinyl chloride and vinyl chloride monomer and lower ethylene costs. The firm is pouring a lot of resources into growing OxyChem’s production capabilities. It’s updating and broadening its Battleground site and improving multiple plants along the Gulf Coast.

In 2023, Occidental Petroleum began the first investment phase for its plant upgrades, which it aimed to complete by 2025. The fruits of these enhancements are starting to be seen, with the full benefits expected by 2025. At the same time, it will complete the Battleground site by mid-2026. The company estimates the investments will result in another $300 million to $400 million in earnings over time.

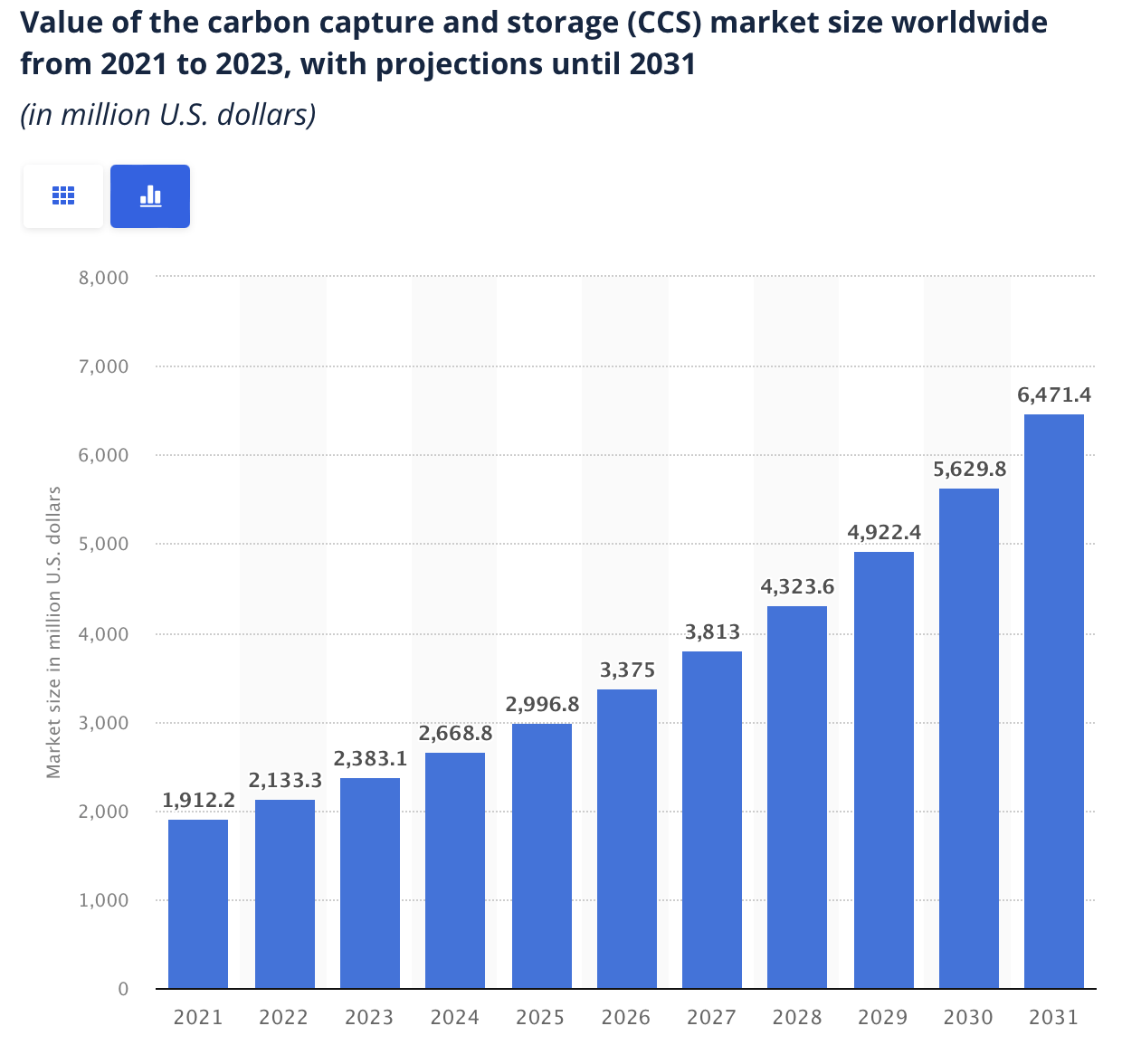

Occidental Targets $4 Trillion market with $600M STRATOS Carbon Capture Plant

In addition, it has positioned itself to benefit from the increasing drive to remove carbon from the air. This could cost $600 million and involve constructing a STRATOS direct air capture (DAC) plant in Texas for Oxy Low Carbon Ventures. The plant can remove as much as 500,000 tons of Carbon dioxide annually and should come online before the end of the year.

While it is in the early stages of commercializing the DAC technology, it is well positioned to generate significant value by the growing push to reduce CO2 emissions to combat global warming. The firm has also secured a strategic partnership with BlackRock (BLK), which will guarantee $550 million in funding towards the development costs of STRATOS.

Since carbon capture and sequestration is expected to become a $4 trillion industry by 2050, Occidental Petroleum is one of the companies well-positioned to benefit from its DAC technology, which it acquired last year following a $1.1 billion acquisition of Carbon Engineering.

Statista

Concluding Thoughts

Even as the company diversifies its business empire, it remains a top stock pick in the energy sector for passive income. In May, the company increased its quarterly dividend to $0.22 a share, taking its annualized dividend to $0.88, translating to a yield of about 1.4%.

In addition to the dividend offering, the stock has gained about 3.4% year to date. While underperforming compared to the overall market’s 19%, it trades at a forward price-to-earnings multiple of 17, slightly above the S&P 500 energy sector’s P/E of 13.

While net debt was approximately $19.6 billion in the first quarter, the debt-to-equity ratio had already fallen to 0.67 from a high of 1.9 at the close of the deal in 2019 to buy Anadarko for $55 billion. This clearly and vividly indicates that the company is doing things right regarding peeling off higher indebtedness.

If oil prices stay above $70 per barrel, Occidental Petroleum will not have trouble generating heavy revenues and free cash flows. The CrownRock acquisition is likely to enhance its capacity to increase production further while strengthening its prospects in the industry, with oil output at $40 a barrel.

In addition to oil and gas, two potential catalysts for OxyChem and Oxy Low Carbon Ventures businesses will likely spur growth over many years as the global economy shifts toward lower-carbon energy. Of course, the company pledged that a significant portion of cash flows would reduce $3.7 billion in debt, but pledged stock buybacks and higher dividends were aimed at returning value to shareholders.

Analyst???s Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.