Summary:

- NIO’s September deliveries included 832 units of the new ONVO-branded L60 SUV, indicating strong demand and potential for significant Q4 delivery growth.

- ONVO-branded deliveries immediately, after only 3 days of shipments, represented a 4% delivery share in September.

- NIO also secured a strategic equity investment of $0.5B from three Chinese investors, enhancing its financial stability amid high operating losses.

- NIO’s vehicle margins are improving, suggesting a path toward profitability, and the L60’s success could boost Q4 delivery volumes to 76-78k units.

- Despite recent share price surges, NIO remains a strong long-term buy due to its delivery momentum, strategic investments, and potential to improve its financial metrics.

Robert Way/iStock Editorial via Getty Images

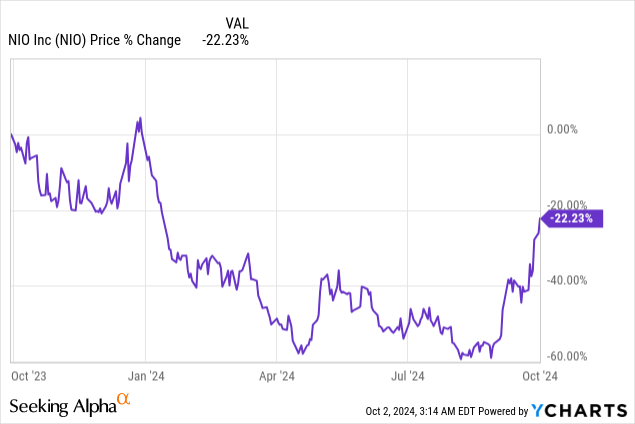

NIO (NYSE:NIO) reported monthly delivery figures for the month of September on Tuesday which included for the first time deliveries of its new ONVO-branded L60 sport utility vehicle… which were highly expected. The Chinese EV company almost breached its delivery record from June as ONVO deliveries ramped up nicely, and the current trajectory of L60 sales/deliveries implies that the EV company could see a boost to its fourth-quarter delivery volume. At the end of September, NIO also announced partnering with new strategic investors from China which invested a considerable amount of money into the EV company in order to help it grow its product portfolio and move towards profitability. I believe the risk profile has further improved here in light of these two news items and although shares of NIO have surged lately, it is not too late to build up a long position for the long term.

Previous rating

I rated shares of NIO a strong buy after the electric vehicle maker reported second quarter earnings and showed 3 PP growth in vehicle margins: Strike While The Iron Is Hot. NIO also submitted a strong outlook for Q3 deliveries which underlined the appeal of an investment in China-based EV start-ups. NIO submitted its highly anticipated update for third-quarter and September deliveries, which, for the first time, included deliveries of ONVO-branded electric vehicles. I believe NIO is off to a very good start with its low-price EV brand and I expect a significant increase in deliveries going forward.

NIO deliveries for Q3

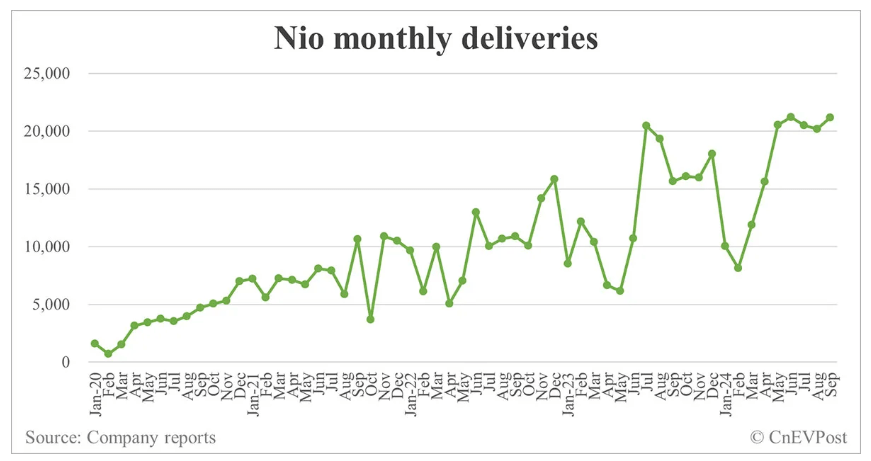

NIO delivered 21,181 electric vehicles in September, showing a year-over-year increase of 35.4%. In the previous month of August, NIO delivered 20,176 vehicles (+4% Y/Y). September was the fifth straight quarter in which the EV firm delivered more than 20,000 units to customers and this credit is in part due to NIO’s new launch of low-cost EVs that are marketed under the ONVO brand. In the entire third-quarter, NIO delivered 61,855 electric vehicles to customers which shows a Y/Y delivery growth rate of 11.6%. It was the highest quarterly delivery volume on record for NIO and the second-highest monthly delivery volume (after June 2024).

Importantly, the September delivery report broke down deliveries by brand and showed that the 21,181 delivery total included 832 ONVO-branded vehicles (representing a 4% delivery share right out of the gate). NIO just launched the ONVO brand in order to compete in a lower-cost segment and mount a challenge on Tesla (TSLA). ONVO deliveries were made up to 100% of the L60, a mid-size family sport utility vehicle, that costs approximately $21,200. Tesla’s Model Y currently costs buyers 249,900 Chinese Yuan which works out to around $34,600 so NIO’s new low-cost brand could be set to see a surge of orders and deliveries as it is easily undercutting one of its most formidable EV rivals.

It should also be noted that the ONVO L60 SUV only started shipping on September 28, 2024, therefore the delivery total of 832 vehicles was achieved in just three days.

Assuming that NIO can sustain its current delivery ramp, I expect that the EV maker will produce and deliver a couple thousand ONVO electric vehicles in the month of October. NIO guided for 61-63k quarterly deliveries in Q3 and with the ONVO now available in the market, I believe NIO’s deliveries are set for a major boost.

With ONVO deliveries now starting to ramp up in October (the first full month of deliveries), I believe ONVO is going to be able to deliver 3-5k ONVO models just this month. I also expect a quarterly delivery volume of 76-78k, but will admit that this estimate is conservative. My Q4 delivery estimate breaks down to a monthly average delivery volume of 25,666 electric vehicles, at the mid-point, with investors likely to see a growing ONVO share of deliveries in the next several months. If demand for low-price electric vehicles is a robust — as NIO’s delivery figures suggest — NIO could significantly out-perform my estimate. The launch of ONVO could also be a catalyst for NIO to accelerate its top line growth and catch up to Li Auto (LI) which has the strongest growth and profitability metrics in the China EV start-up group: Strong EV Choice, Low Price.

NIO gets a new investment

The strong delivery report for October almost buried other news that were highly favorable to NIO: the electric vehicle company secured another strategic equity investment at the end of September, this time from three Chinese investors: Hefei Jianheng New Energy Automobile Investment Fund Partnership, Anhui Provincial Emerging Industry Investment and CS Capital invested 3.3B Chinese Yuan ($470M) into NIO Holding. The investment comes at a time of high operating losses and is a positive for NIO as well as its shareholders.

NIO’s valuation

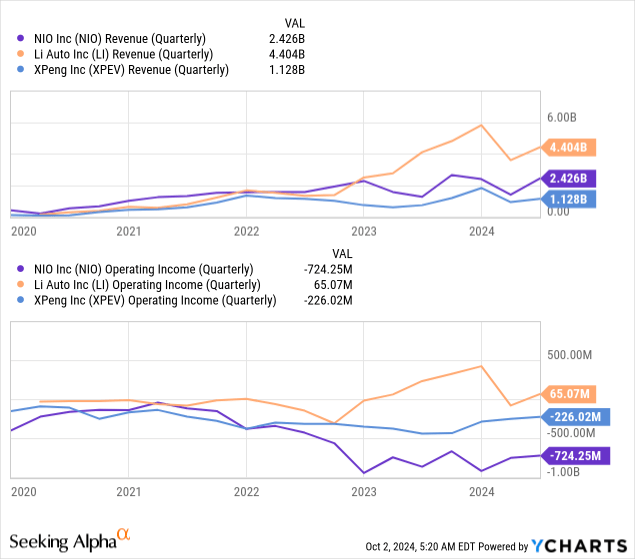

I still like NIO a lot for a number of reasons: 1) As I stated in my last work on the electric vehicle maker, NIO’s vehicle margins are improving, meaning the company retains more money for each vehicle sold. Although NIO is still losing money overall, this trend is highly encouraging, and 2) NIO’s shares are widely undervalued, in my opinion.

I would now add a third reason to buy NIO which is that the EV firm is seeing significant L60 delivery momentum which should have a very positive effect on fourth-quarter deliveries and on NIO’s overall business momentum in terms of revenue and operating income.

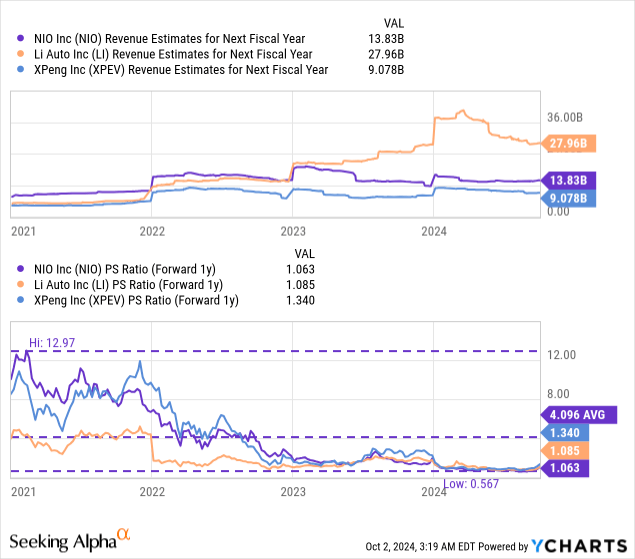

NIO is very cheap, most certainly when compared to the company’s historical valuation average. In the last five years, NIO has traded at P/S ratios ranging between 0.6X and 13.0X… which is a very wide range and reflects the rollercoaster ride of emotions that NIO has taken investors on during the last several years. Currently, shares of NIO are valued at 1.06X which compares to an industry group P/S average of 1.16X. The industry group includes two other Chinese start-up automobile manufacturers, Li Auto (LI) and XPeng (XPEV).

I believe the strategic equity investment and the L60 delivery start are justifying a strong buy rating, although NIO still needs to fundamentally improve its profitability profile. In my opinion, NIO could revalue to a 1.5X forward (FY 2025) price-to-revenue ratio, which implies a fair value of $9.90 per-share (+41% upside). In the longer term, I can see an even higher fair value, but only if the EV maker were to prove that it can grow towards profitability.

Risks with NIO

My risk assessment since my last article on NIO has not changed: the biggest risk I see for NIO is that the mass production of low-cost electric vehicles will negative effect NIO’s margins just at a time when it managed to engineer a rebound. A weakening margin profile would further delay the profit time-line for NIO and potentially be a severe headwind for the company’s valuation factor.

Final thoughts

NIO’s moment of truth has arrived: NIO delivered 832 L60 SUVs, of the new ONVO brand, to customers in just three days, indicating a very strong ramp is ahead that could make a crucial difference for Q4 deliveries. Including deliveries for the month of September, NIO has delivered more than 20k units to customers in each of the last five months. Given the current upswing in deliveries I believe NIO could reach a quarterly delivery volume of up to 78k units in Q4 which would represent more than 24% growth (at the mid-point) relative to Q3.

NIO also managed to attract strategic equity investors which is a great show of confidence at a time when the EV maker, despite improving vehicle margins, is still not profitable. I believe the risk profile here has improved and I can see further progress for the company if it can maintain strong delivery growth momentum for the L60. Shares are still cheap, most certainly in a historical context, and NIO has considerable upside revaluation potential.

Analyst’s Disclosure: I/we have a beneficial long position in the shares of NIO, LI either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.