MSFT’s high FWD P/E of 31x can feel off-putting to many investors.

However, its positives far outweigh negatives (such as high valuation) and can deliver market-beating returns.

This article details the top two positives on my mind.

The first one is the potential for accelerated AI infusion, judging by the recent developments surrounding OpenAI.

The second one is the fundamental scalability of its business, as revealed by its marginal return on capital employed (MROCE).

Iryna Drozd

MSFT stock and OpenAI

I last analyzed Microsoft stock (NASDAQ:MSFT) back in August. The analysis used the rule of 40 and was based on the financials reported in its FY 2024 Q4 earnings. That article was entitled “Microsoft: Rule Of 40 Points To Buy.” It argued for a bullish thesis based on the following factors:

Assessed by the rule of 40, Microsoft is a strong buy opportunity under current conditions. It offers an excellent balance of growth and profitability with a combined score of 45.9%, surpassing the 40% threshold of the rule.

Since that writing, there have been some material developments surrounding the company, motivating an updated assessment. The top one on my radar involves OpenAI’s latest round of fundraising. The specifics of this development are quoted below. The quote is slightly edited by me and the emphases were also added by me. In the remainder of this article, I will argue for an iteration of my buy thesis based on both A) the near-term AI catalysts as reflected in the implied valuation of OpenAI in this fundraising round, and B) the superb basic economic characteristics such as return on capital and scalability.

Seeking Alpha news: Microsoft-backed OpenAI completed its latest fundraising round of $6.6B, propelling the company to a valuation of $157B, making it the second-highest valued startup in the world. “We’ve raised $6.6B in new funding at a $157B post-money valuation to accelerate progress on our mission,” OpenAI said in a statement. “The new funding will allow us to double down on our leadership in frontier AI research, increase compute capacity, and continue building tools that help people solve hard problems.“… The latest OpenAI funding round was managed by the venture firm Thrive Capital, which was founded by Joshua Kushner. AI chipmaker Nvidia (NVDA) and Microsoft (MSFT) participated in this round.

MSFT stock: AI infusion likely to accelerate

I’m optimistic about the continued infusion of OpenAI’s technologies in MSFT’s product lineups for sustainable growth. I’m especially bullish on the contributions from Azure and AI-related transformation. There was a substantial increase in the number of Azure AI customers in recent quarters. At the end of March, Azure Arc had approximately 33,000 customers. Besides the growth in quantity, I’m also impressed by the quality of the growth. Many of the new deals in recent quarters feature billion-dollar and multi-year commitments from leading names like Coca-Cola. Additionally, MSFT’s Copilot is driving a new era of AI transformation in its operations and productive offerings. With the additional funding that OpenAI has received, I expect Microsoft to continue blending AI across all layers of its products and services in the years to come.

Of course, the growth will require additional capital expenditures. Management noted in the recent earnings report that AI demands have been trending above available capacity. To meet this need, MFST will need to continuously invest in its infrastructure, especially in the area of cloud and AI infrastructure.

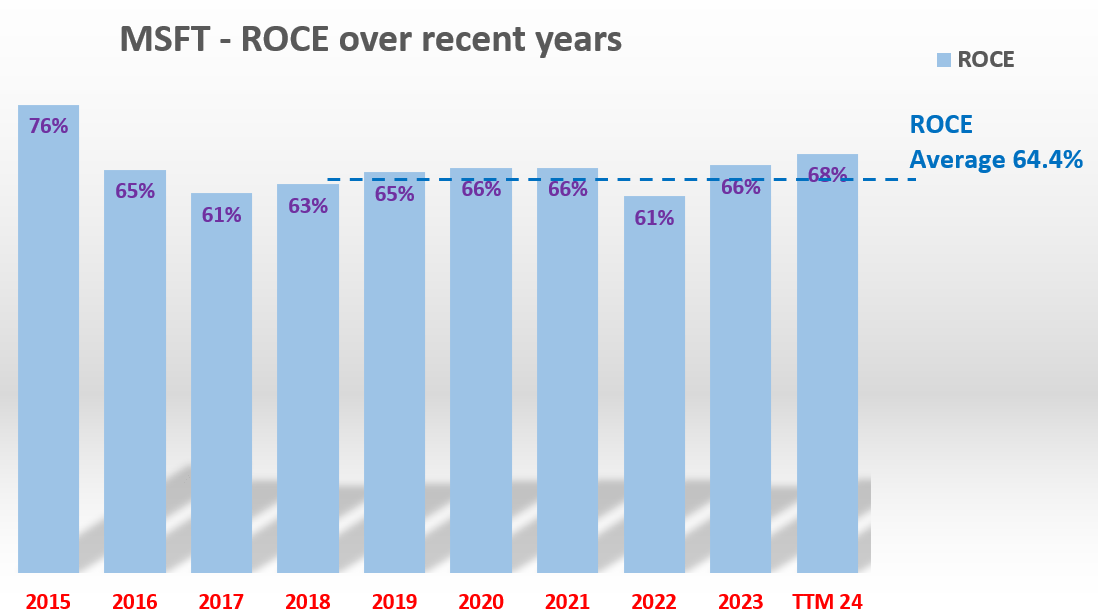

The good news is that MSFT fundamentally enjoys a capital-light and highly scalable business model. As such, I expect it to maintain a high ROCE (return on capital employed) with its new capex expenditures. The chart below provides a historical context. The chart shows MSFT’s ROCE In the past decade. The method is detailed in an earlier article, where I analyzed the ROCE of Amazon (AMZN). Here, I will just quote the end results:

For businesses like MSFT, I consider the following items to be capital actually employed 1) working capital, including payables, receivables, and inventory, 2) gross property, plant, and equipment, and 3) research and development expenses (an essential expense for a business like MSFT in my view) are also amortized and considered part of its capital employed.Under these considerations, MSFT’s ROCE has been averaging 64.4% in recent years as seen. This is not only far above the overall economy (more on this later) but also very competitive when compared with the rest of the FAANG group (or the magnificent seven).

Author

MSFT stock: Scalability revealed by marginal return

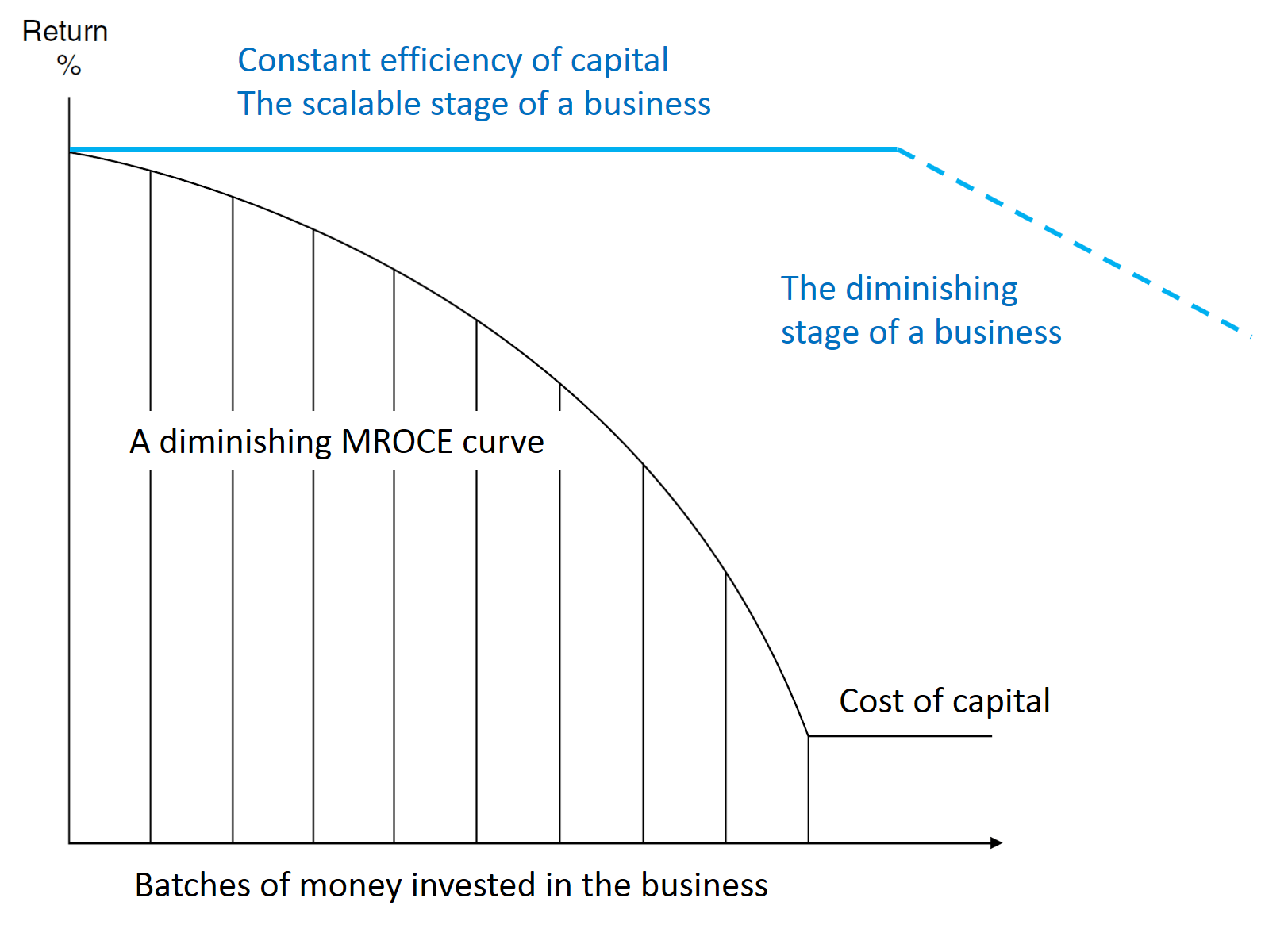

Of course, high ROCE is only half of the equation here. Berkshire Hathaway (BRK.B) (BRK.A) CEO Warren Buffett noted this a long time ago. In his mind, “the best business to own is one that over an extended period can employ large amounts of incremental capital at very high rates of return.”

What he’s referring to here is the marginal return on capital employed, or MROCE. Businesses will always first invest their money in capital projects with the highest expected return. If there’s money left after this, the business will seek the next project with the second-highest expected turn. And so on. The result is a diminishing return marked by a shrinking MROCE as shown in the chart below.

Source: author

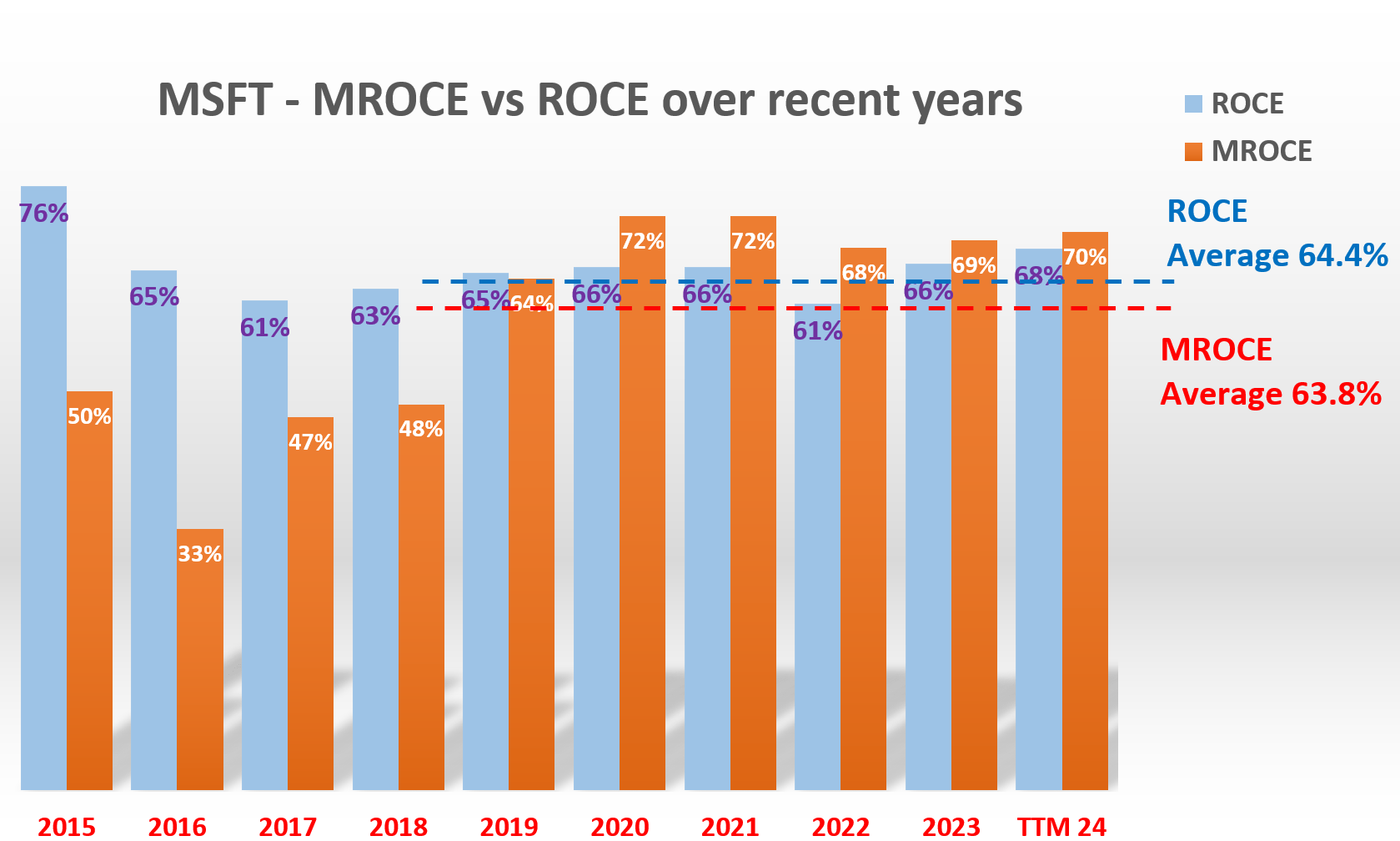

The next chart below shows my calculation of MROCE for MSFT in the past few years. The calculation was performed in a few steps, which are also outlined in the AMZN article referenced above. And again, here I will only quote the end results:

First, the capital employed (“CE”) was calculated for each year. Second, then the incremental of CE YOY was calculated. Then finally, the ratio between the incremental earnings YOY and incremental CE YOY was calculated to approximate the MROCE. During years when there were large fluctuations in either the incremental earnings or the capital employed, a multi-year running average was taken to smooth the fluctuations. The results show that MSFT has been able to maintain an MROCE that is essentially the same as the average ROCE so far (63.8% vs 64.4%) as seen.

The small discrepancies are largely due to rounding off errors and the running average. To me, this analysis suggests that MSFT is not at the point where diminishing returns have occurred yet. Looking ahead, given the potential of AI infusion as analyzed above, I expect MSFT to maintain high ROCE and MROCE at the same time for years to come.

Author

MSFT stock: Valuation in focus

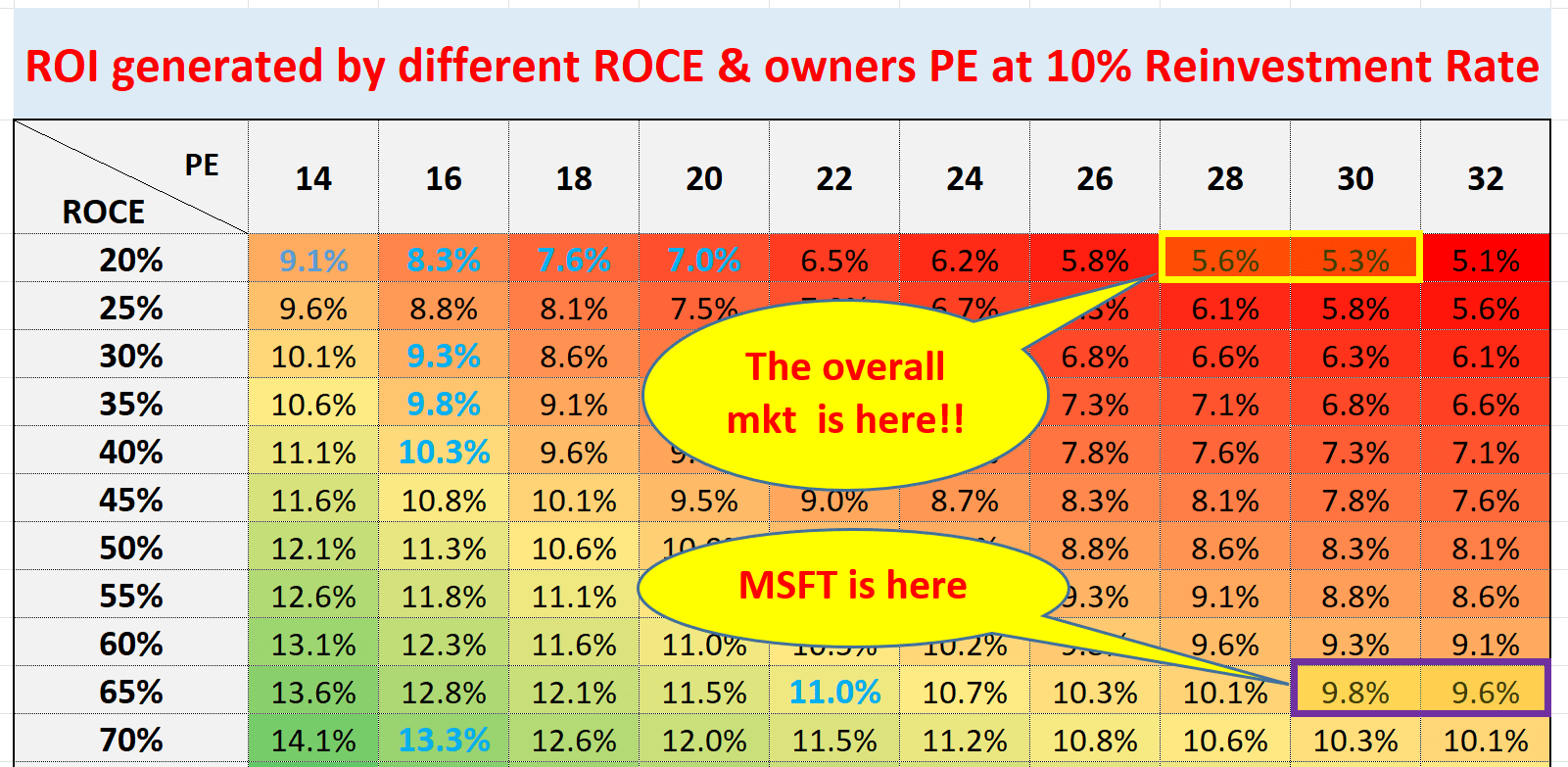

On to valuation. The P/E multiple can feel off-putting for many investors. The stock is currently trading at an FWD P/E of 31x, quite expensive both in absolute and relative terms. However, I want to argue that the valuation, as off-putting as it feels, can still deliver market-beating returns for long-term investors who think like a business owner. Details of my long-term return projection are shown below (and the projection model is described in my earlier article). The takeaways are:

The long-term ROI for a business owner is simply determined by two things: A) The price paid to buy the business, and B) the quality of the business. More specifically, part A is determined by the owner’s earning yield (“OEY”) when we purchased the business. And that’s why P/E is the first dimension in the chart. Part B is determined by the quality of the business and that is why ROCE (return on capital employed) is the second dimension in the chart.

The long-term earnings growth rate is estimated by the product of the ROCE and the Reinvestment Rate.

Under current conditions, MSFT is trading at around 31x FWD P/E, translating into an OEY of ~3.2%. With an average ROCE of 64.4% as aforementioned, its long-term growth rate is projected to be about 6.4% assuming a 10% reinvestment rate. Hence, I anticipate a total ROI of around 9~10% from MSFT under current conditions, which is above what I expect from the S&P 500 (around 5~6%) by a sizable gap. Finally, as an additional advantage for MSFT, the average economy’s MROCE is nowhere near MSFT’s 63.8% as the overall economy’s underlying business model is far less scalable than MSFT’s (with its SaaS model and annuity-like income streams).

Author

Other risks and final thoughts

Besides the requirements of sizable capex expenditures in the next few years, there are a few other downside risks worth mentioning. Some of these risks are common to both MSFT and its peers, and some of them are more particular to MSFT but not to other tech stocks. The primary macroscopic risks shared by Microsoft and its tech peers are economic downturns and increasing competition. Recent job data shows negligible odds for a hard landing, and tech stocks can respond sensitively during recessions. More specific to Microsoft are the risks associated with its reliance on Windows and Office, which account for a significant portion of its revenue. The emergence of alternative products (such as Google’s web-based productive suites) and competitors could negatively impact Microsoft’s financial performance from these segments.

All told, my overall view is that the positive outweighs the negative, resulting in a skewed return/risk profile under current conditions. To recap, the top positive on my list is the potential for accelerated AI infusion, judging by the recent developments surrounding OpenAI and the fundamental scalability of MSFT’s business model as revealed by its MROCE.

Analyst’s Disclosure:I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.

As you can tell, our core style is to provide actionable and unambiguous ideas from our independent research. If your share this investment style, check out Envision Early Retirement. It provides at least 1x in-depth articles per week on such ideas.

We have helped our members not only to beat S&P 500 but also avoid heavy drawdowns despite the extreme volatilities in BOTH the equity AND bond market.

Join for a 100% Risk-Free trial and see if our proven method can help you too.