Summary:

- Netflix is set to release its earnings on October 17th, following the market’s close. I foresee a strong likelihood that the stock may experience a sharp decline following the announcement.

- I think Netflix is approaching the saturation point for subscriber growth and may have exhausted its ability to increase prices further. These factors have contributed to somewhat lackluster DAU trends.

- Data from Sensor Tower shows that Netflix experienced negative month-over-month DAU growth for all three months in Q3, a trend not seen since late 2021, when the stock dropped sharply.

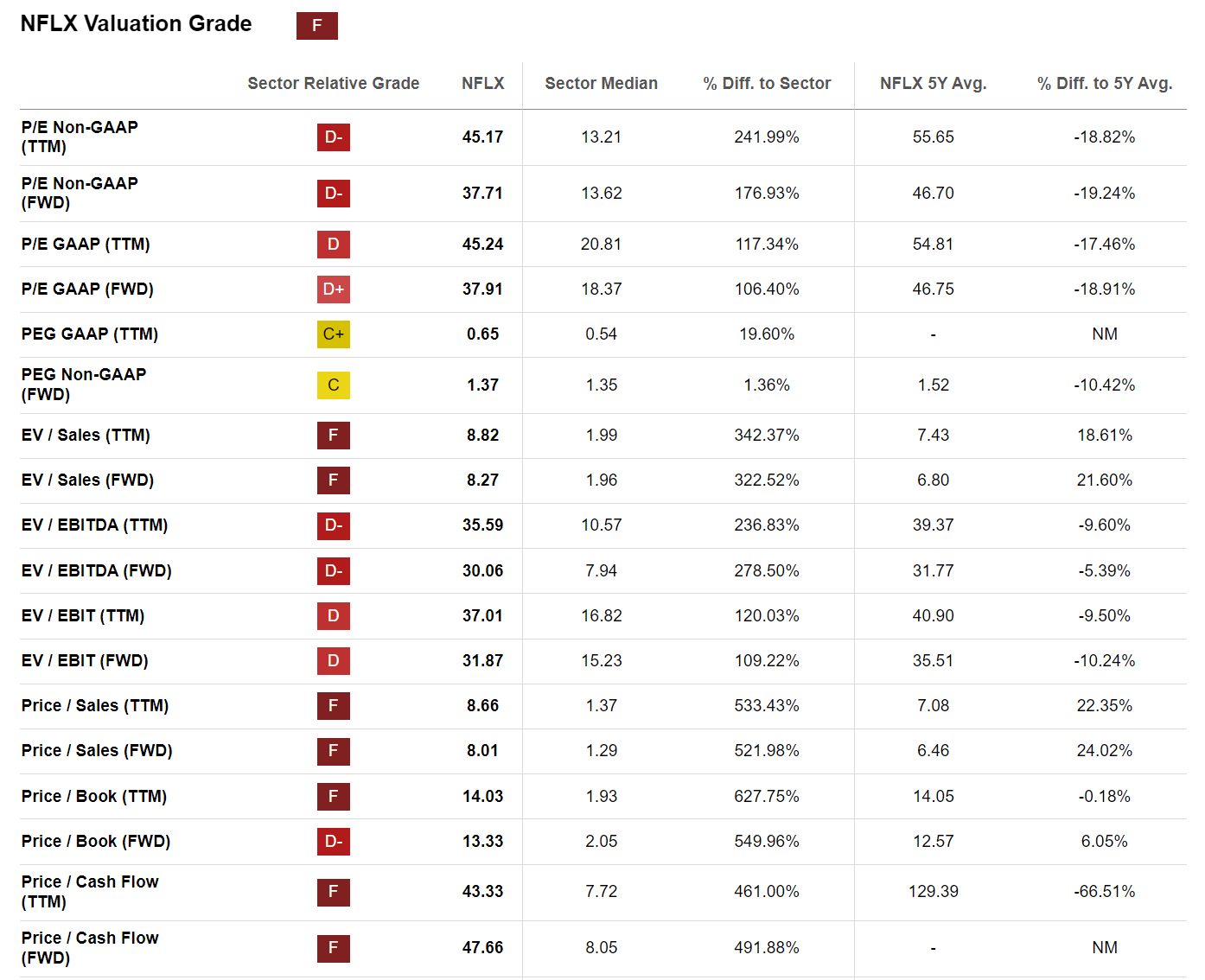

- As we approach the Q3 earnings report, I don’t see any valuation metrics that could offer protection from potential downside risks, with shares trading at 38x 2025 earnings.

Marvin Samuel Tolentino Pineda

Netflix (NASDAQ:NFLX) is scheduled to report earnings on October 17th after the market closes, and I project a probability that shares may drop sharply on the announcement. While I see little risk to Q3 reporting estimates, with revenue and operating income expected at $9.76 billion and $2.62 billion, respectively, according to analyst consensus estimates collected by Refinitv, I see significant downside risk to guidance. In a nutshell, I argue the streaming company is closing in on the subscription penetration ceiling, while the company has likely also exhausted its pricing leverage. These two variables combined have let to somewhat disappointing user/ DAU trends, with the first signals of slowing user engagement visible already in Q3. Indeed, according to Sensortower data, Netflix has seen negative MoM DAU growth for all three months in Q3, something that has not happened since late 2021 (shortly after shares dropped sharply).

Heading into Q3 reporting, I don’t see valuation to protect from downside. In fact, NFLX shares are currently valued at approximately 38x estimated 2025 earnings. This is a significant premium (>100%) to the average multiple in the Communication Sector.

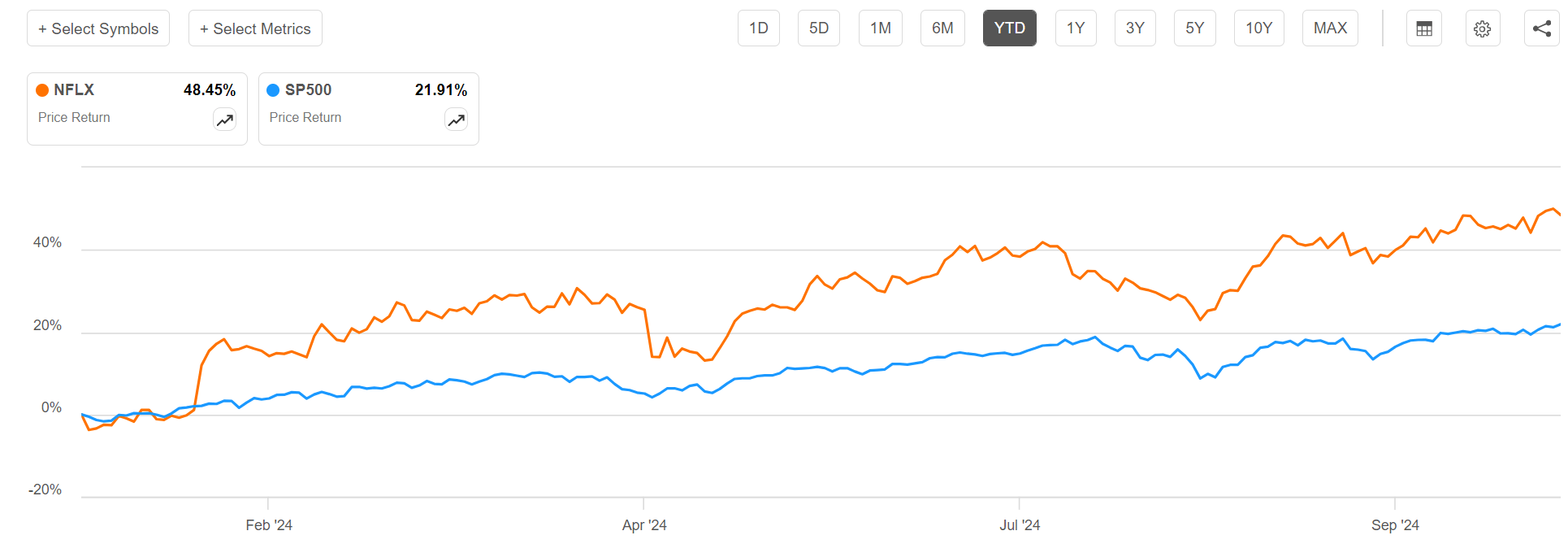

For context, Netflix stock has outperformed the broader market this year. Since January 1st, NFLX shares are up about 48%, whereas the S&P 500 (SP500) has gained approximately 22%.

Seeking Alpha

Slowing DAU Momentum Could Spell Trouble For Net Adds …

Netflix has seen 9.3 and 8.1 million of subscriber net adds in Q1 and Q2 2024, respectively. And while management has not given precise guidance for upcoming Q3 2024, the company has said it expects Q3 2024 net adds to be “lower” than for the same period in 2023, which was reported at 8.76 million. Thus, Q3 trends should have been still robust in the months leading up to the end of September. Looking at below trends relating to Netflix’ user engagement momentum, however, I expect net adds to slow sharply post-Q3. According to my expectations, signs of this thesis could be reflected already in Q4 guidance.

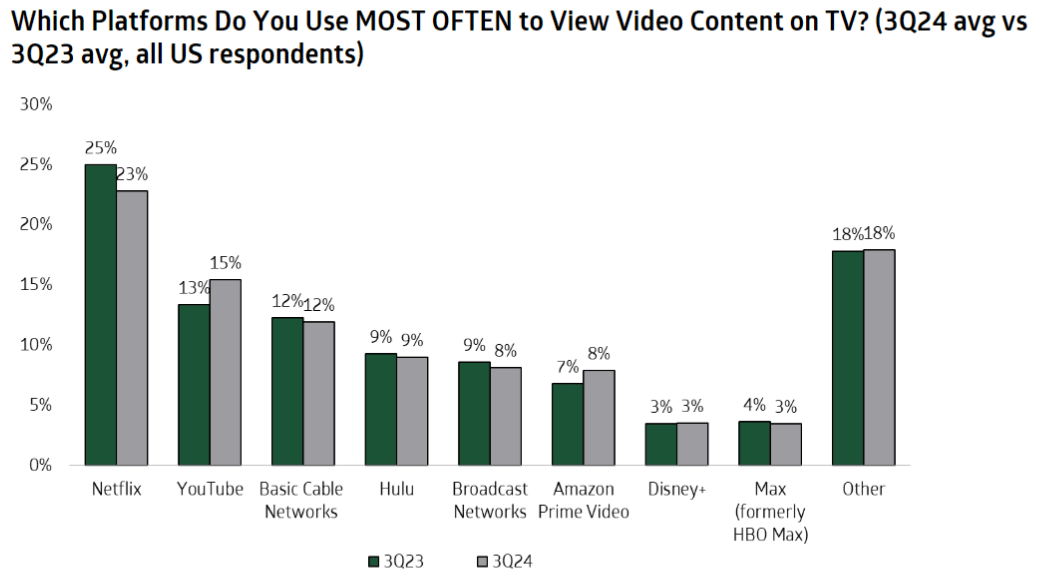

Based on insights from a recent TD Cowen survey for the U.S., Netflix remained the most popular platform for living room viewing in Q3 2024, with 23% of respondents stating they use it most often to watch video content on their TV. However, Netflix has lost approximately 200 basis points worth of market share compared to the same period one year ago, with YouTube and Amazon Prime Video showing notable YoY market share gains (Source: TD Cowen research note on Netflix, dated October 7th).

TD Cowen

Weak momentum for the Netflix platform was indicated by app data as well. According to Sensortower data mapped by BofA BofA, Netflix’s daily active user trends in Q3 showed negative growth, with QoQ growth around -(2-3)% and YoY growth negative by approximately 11%. Indeed, Netflix has seen negative MoM DAU growth for all three months in Q3, something that has not happened since late 2021: Growth in July, August and September was -2%, -2% and -3%, respectively (Source: BofA research note dated October 7th: Internet/e Commerce September app data: Mixed trends with Amazon DAU acceleration a bright spot).

BofA; Sensortower

… While Pricing Looks Stretched

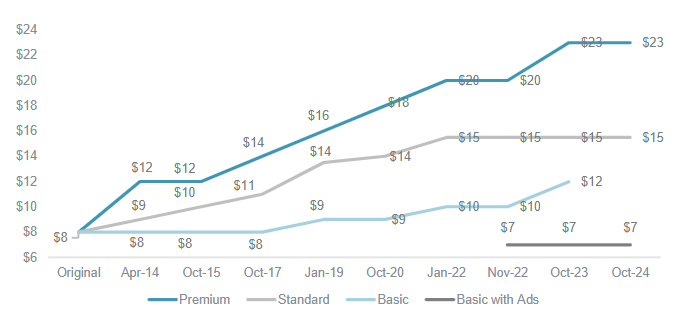

Price increases have been one of the key growth drivers for Netflix over the past few years, as evidenced by the enclosed chart (Source: Piper Sandler research note on Netflix, dated October 7th).

Piper Sandler

But from the current base, further price hikes look increasingly difficult, as Netflix’ comparable value is falling sharply. In 2023, prices for the Basic and Premium plans rose by $2-3, with the Premium plan now costing $22.99 per month. Meanwhile, competitors like Disney+ and Max offer comparable services at lower costs: Disney+ costs $7.99/month with ads or $13.99/month without, and Max offers ad-supported plans for $9.99/month or ad-free for $15.99/month. Additionally, Netflix’ crackdown on password sharing and the introduction of ads in some tiers have led to frustration among users who feel they’re paying more for reduced service flexibility. For further insights, I invite readers to visit Reddit and research the platform’s discussion on Netflix’ pricing strategy.

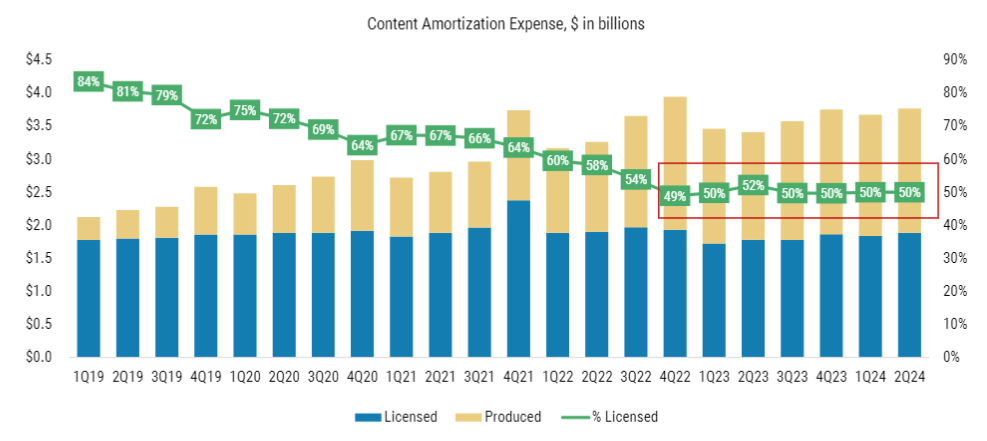

While pricing upside is looking increasingly limited, Netflix is pressured to spent more and more on content to keep users engaged and subscribed. According to Morgan Stanley data, about 50% Netflix’ content amortization expenses are now attributed to in-house content (Source: Morgan Stanley research note on Netflix, dated October 10th). This is not necessarily good, because it highlights that Netflix is increasingly transitioning away from the high-profit platform business model, and shifting towards the CAPEX and OPEX intensive movie production and distribution business model.

Morgan Stanley

Valuation Does Not Protect Downside

As we approach Q3 earnings, I don’t believe the current valuation provides much downside protection. Netflix shares are currently trading at roughly 38x estimated 2025 earnings, representing a substantial premium of over 100% compared to the average multiple in the Communication Sector.

I have previously estimated Netflix’ fair implied value at approximately $447 per share. And heading into Q3, I continue to view this estimate as reasonable, based on enclosed assumptions:

Anchored on analyst consensus estimates as collected by Refinitiv (+/- 10%), I now project that Netflix’s earnings per share for FY 2024 will range between $18 and $20 (non-GAAP), with forecasts of reaching $21.2 in FY 2025 and $26.2 in FY 2026. Post FY 2026, I continue to view an earnings compound annual growth rate (OTC:CAGR) of 3% as reasonable (approximately 75-100 basis points higher than estimated nominal GDP growth). Similarly, I maintain my base-case cost of equity estimate at 8.5%. Given the upüdates, I now estimate the fair value of Netflix stock at $447, up considerably from the prior estimate of $250, but notably below the NFLX market trading price of around $555.

Seeking Alpha

Upside Risks To Keep in Mind

While the concerns raised about Netflix’s potential subscriber saturation and the risks to its guidance are valid, there is also significant upside risk that should be considered. Despite the challenges in maintaining the pace of subscriber growth, Netflix has demonstrated an ability to innovate in its content offerings and monetization strategies. As an example, in 2022 when Netflix growth was fading, the company’s push into advertising via its ad-supported tier opened a whole new revenue stream for the company. Additionally, Netflix’s global reach, particularly in under-penetrated markets like Asia and Africa, offers substantial room for continued subscriber expansion, even if growth slows in more mature regions.

Investor Takeaway

Netflix is set to release its earnings on October 17th, following the market’s close. I foresee a strong likelihood that the stock may experience a sharp decline following the announcement. While I don’t anticipate any major risks to the Q3 earnings estimates—analysts project revenue at $9.76 billion and operating income at $2.62 billion, according to consensus estimates from Refinitiv—I do believe there are substantial risks regarding the company’s guidance. Essentially, I think Netflix is approaching the saturation point for subscriber growth and may have exhausted its ability to increase prices further. These factors have contributed to somewhat lackluster trends in user engagement and DAUs, with early signs of a slowdown already evident in Q3. Notably, data from Sensor Tower shows that Netflix experienced negative month-over-month DAU growth for all three months in Q3, a trend not seen since late 2021, when the stock dropped sharply. On that note, consensus currently projects 12% YoY growth in revenue for Netflix in 2025, according to data collected by Refinitiv. But give the trends I see, I argue that >10% YoY revenue growth is unlikely to be achievable; and expectations need to be reset..

As we approach the Q3 earnings report, I don’t see any valuation metrics that could offer protection from potential downside risks. Currently, NFLX shares are trading at around 38x estimated earnings for 2025, which represents a significant premium of over 100% compared to the average multiple in the Communication Sector.

Analyst’s Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Not financial advice

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.