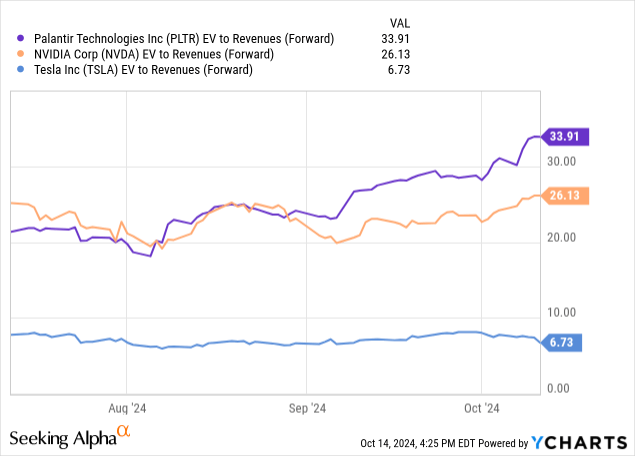

Palantir is significantly overvalued, with a forward EV-to-sales ratio of 34 and a forward price-to-cash-flow ratio of 111.3, making it a high-risk investment.

Despite expected strong Q3 results – I estimate 35% year-over-year normalized EPS growth and $710 million in revenue – the current valuation is unsustainable.

The Company’s commercial revenue growth, driven by its AI Platform and boot camps, is promising, but its reliance on wartime economics poses long-term risks.

Given the speculative nature of its current valuation, consider selling PLTR stock now, as a significant correction is likely.

DKosig

In my last analysis of Palantir (NYSE:PLTR), it was clear to me that the company was overvalued based on its fundamentals. However, despite this, the stock has increased by 45% since the article. Although it may be disappointing to lose out on these gains in the short term, over the long term, I think those on the sidelines will be quite pleased that they did not allocate to the company during the current high valuations. To put it simply, I estimate that Palantir will likely be weighed down by the market in due course (not as a result of operational defects, but simply as a result of excessive enthusiasm from the market initially).

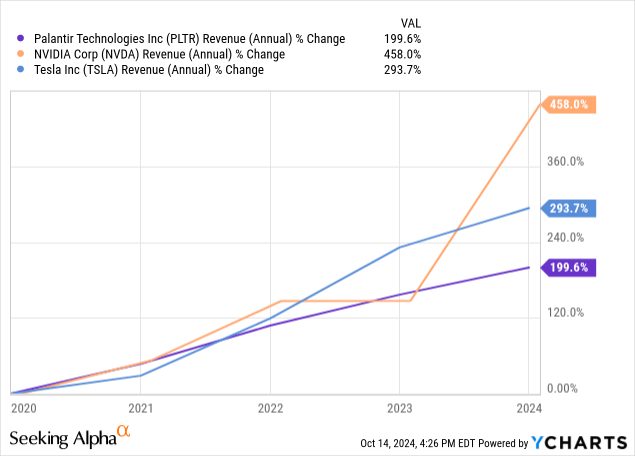

Now, with Q3 results approaching, I am still very skeptical of the viability of Palantir as a long-term holding due to its valuation. However, I expect that the company will report very strong Q3 results. My estimate is above management’s guidance for revenue, and my normalized EPS year-over-year growth estimate is above the consensus. That being noted, this has to be placed into context. Palantir is currently significantly overvalued based on my fundamental peer analysis of the company alongside NVIDIA (NVDA) and Tesla (TSLA). I consider now to be a very poor time to initiate or add to a position. I also believe at the present valuation, selling is valid.

Firstly, Palantir has been placing more emphasis on its commercial revenue growth recently. This has been supported by Palantir’s Artificial Intelligence Platform (‘AIP’), which has been facilitated by rapid customer onboarding through initiatives like AIP boot camps. I expect management to put particular emphasis on this in the Q3 earnings call – AIP’s adoption is not limited to existing Palantir customers using Foundry or Gotham, so it also gives smaller-scale customers a chance to engage with Palantir’s AI capabilities. This has broadened the company’s target market, and I expect this to have supported its revenue growth in Q3 significantly.

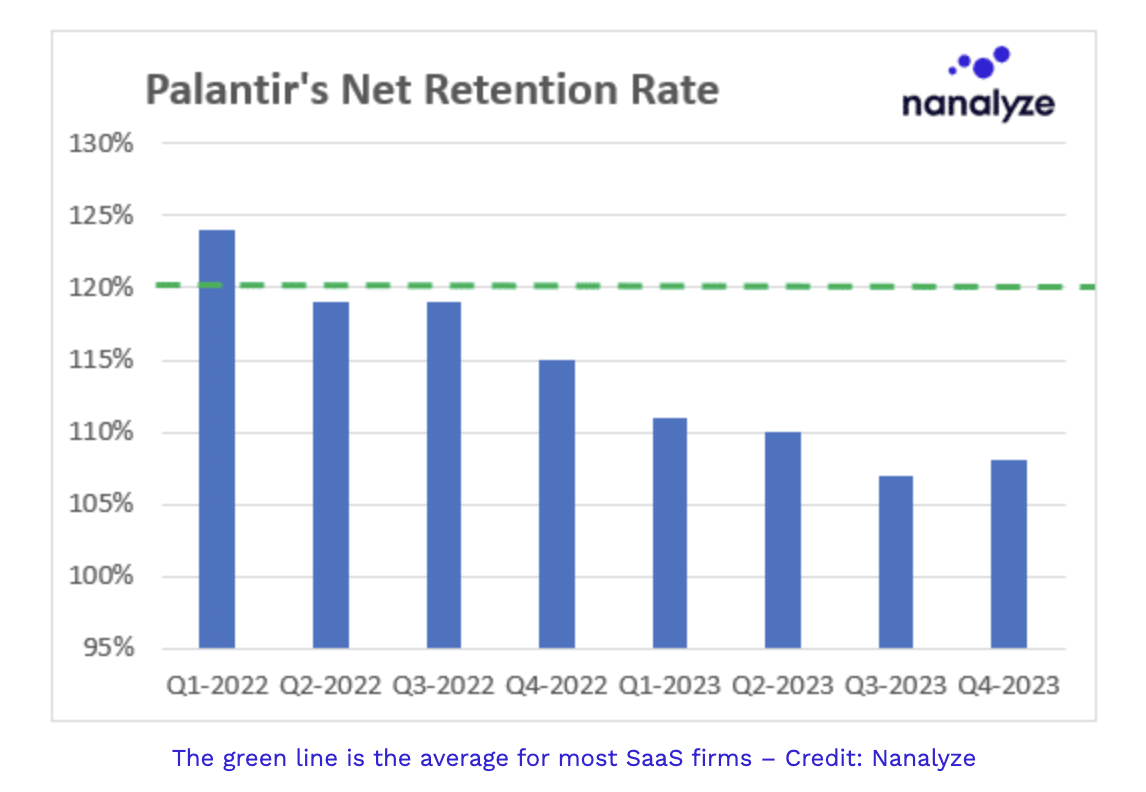

In Q2 2024, Palantir‘s U.S. commercial customer count grew by 83% year-over-year and 13% quarter-over-quarter, reaching 295 customers. This trend is likely to continue through Q3, driven by the increasing adoption of AIP. Furthermore, Palantir’s net revenue retention rate was 114% in Q2 2024, up from 110% a year ago. This is significant because, for quite some time, the company had been neglecting to report this transparently, according to a report from Nanalyze:

In 2021, Palantir provided this metric across all four of their revenue segments (government, commercial, U.S. government, U.S. commercial). Then, they started providing it at an aggregate only, and finally swept it into the footnotes when the trend started looking like this. [see below] – Nanalyze

Nanalyze

I feel positive about the uptrend recently (in results following the graph’s timeframe), and I expect we might even see some further progress on this in Q3. However, a big part of this could be due to momentum from Palantir’s focus on sales at the moment, including from its boot camps. As a 120% net revenue retention rate is considered average in SaaS, and with Palantir still likely to report below this in Q3, I’m certainly cautious given the company’s incredibly high valuation at the moment.

The fact that Palantir is focusing on its commercial revenues is positive, in my opinion, as while it is exposed to wartime economics, I expect this will not be a heavy revenue generator for Palantir over the long term. Primarily, I believe this because, from my analysis, while international relations are tense at the moment, the nature of warfare today – with nuclear deterrents threatening species extinction – makes large-scale conflict less likely to manifest. Tensions with Russia are likely to ease in the long term if the U.S. does not prioritize NATO expansion, and the Taiwan issue with China seems more like a tension over international relations than an economic power struggle. This is especially true as TSMC (TSM) continues to diversify internationally. Based on my macroeconomic analysis, with potential changes in the White House and stronger value-driven leadership in Western global politics, the need for Palantir’s heavy defense capabilities could diminish over time. That said, at present, geopolitical tensions remain high. Therefore, strong growth in Palantir’s Q3 government revenues is quite likely, in my view. In Q2, its U.S. government revenue grew 24% year-over-year and 8% quarter-over-quarter to $278 million. In Q3 2023, its government revenue grew by 12% year-over-year. I estimate Palantir may report 20% or higher year-over-year government revenue growth in Q3, given the current geopolitical climate.

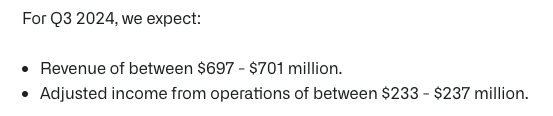

For Q3, I estimate that the company will achieve 35% year-over-year normalized EPS growth (largely supported by the fact that the company has emphasized profitability in recent reports) and total revenue of $710 million (due to substantial tailwinds from its AIP and boot camp models, with particular growth accruing from its commercial contracts). Therefore, I am very bullish on Palantir from a pure operational and financial front leading up to the results. I even expect that the stock could rally following the Q3 report. However, let me tell you why Palantir is not a good long-term investment at the present valuation.

Valuation Update: Significantly Overvalued And Highly Speculative

As I mentioned, since my last analysis, Palantir stock has gained 45% in price. This makes the investment problematic for fundamentally oriented, long-term investors like myself. Palantir now trades at a forward EV-to-sales ratio of 34 and a forward price-to-cash-flow ratio of 111.3. This makes the investment very high risk, given how high these ratios are compared to its other high-growth technology peers.

Based on the above charts, there is no strong fundamental reason why Palantir should be valued as highly as it currently is. In fact, allocating to Palantir at such a high valuation, based on its future growth prospects, is largely speculative. Therefore, I believe it is prudent for investors to question whether allocating to Palantir at its present valuation is wise or misguided (with some discernment, I expect the consensus should lean toward the latter). That said, given the market’s irrational tendency to trade on momentum and sentiment – especially with strong Q3 results likely – further speculative valuation gains could compound in the near term. I strongly urge investors to view these as ‘unrealized gains.’ I believe Palantir stock is due for a significant correction.

I have maintained that a price-to-sales ratio of approximately 17.5 is fair for Palantir, and I still consider this accurate today. Whether the market corrects the company’s valuation to this level in a year, two years, or five years is immaterial to me. If I plan to hold Palantir for ten years or more based on its long-term operational prospects, now is not an ideal time to invest. My fair value P/S ratio of 17.5 suggests that the company is more than 120% overvalued, given its current TTM P/S ratio of 38.6 (based on a rational, relative market valuation compared to other distinct, one-of-a-kind companies like Tesla and NVIDIA).

Tesla

NVIDIA

Palantir

Forward operating cash flow growth

1.8%

150.4%

69.5%

Forward price-to-cash-flow ratio

59.5

49.4

111.3

Risks Review

Palantir is operationally strong, but investors should not lose sight of the fundamentally oriented value investing principles that keep portfolios steady over the long term. Buying Palantir at an EV-to-sales ratio greater than technology peers NVIDIA and Tesla is foolish. Investors should consider selling because we are unlikely to see the current stock price for a while once a correction ensues.

While management has carefully diversified the business between government and commercial sectors, it is still dependent on wartime economics for a substantial portion of its growth trajectory. I don’t particularly like this, especially as over the long term my analysis convinces me that international relations should stabilize and the need for heightened defense mechanisms in times of war will be much lower than current tensions may temporarily indicate. This is why I am much more supportive of Palantir’s government sector prospects, and I am pleased it is growing this segment substantially at the moment.

Palantir Q2 2024

Government Revenue

54.7%

Commercial Revenue

45.3%

Despite growth in its commercial revenues, Palantir still faces a conflict of interest between commercial growth and defense growth. Investors may argue that Palantir’s diversified focus between the two sectors acts as a synergy, but I believe a heavier commercial emphasis will take precedence over time. This is likely to cause periods of revenue and operational instability, as the company will have to reallocate resources and remain agile amid market dynamics. This creates pockets of weakness, which could open up weak earnings reports, toppling its unstable valuation held up on speculative sentiment.

Conclusion

Palantir is certainly a U.S. defense asset and a viable long-term holding, but not at the current valuation. Every portfolio needs to be risk managed, and after Palantir’s recent price expansion and the fact that medium-term scaling of its revenues in a manner achieved by NVIDIA is unlikely, there is no reason why it should be trading at a higher EV-to-sales ratio. While I strongly believe in the long-term growth of Palantir operationally, I consider now a good time to sell. Value is everything in long-term investing, and Palantir is overvalued amid high levels of speculation over its future growth rates related to unique offerings in classified AI.

Analyst’s Disclosure:I/we have a beneficial long position in the shares of TSLA either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.