Alphabet is trading at a significant discount to its peers despite robust business momentum and strong outlook, making it a buying opportunity.

Antitrust issues and AI chatbot disruption are valid concerns, but they are unlikely to have any immediate material impact.

Consensus estimates for Q3 2024 predict impressive revenue and EPS growth, with Alphabet likely to exceed expectations based on historical performance.

Using a 10% discount rate, Alphabet’s fair value is estimated at $136.87 per share. While Alphabet is slightly overvalued, I see potential for significant long-term gains.

Justin Sullivan

Introduction

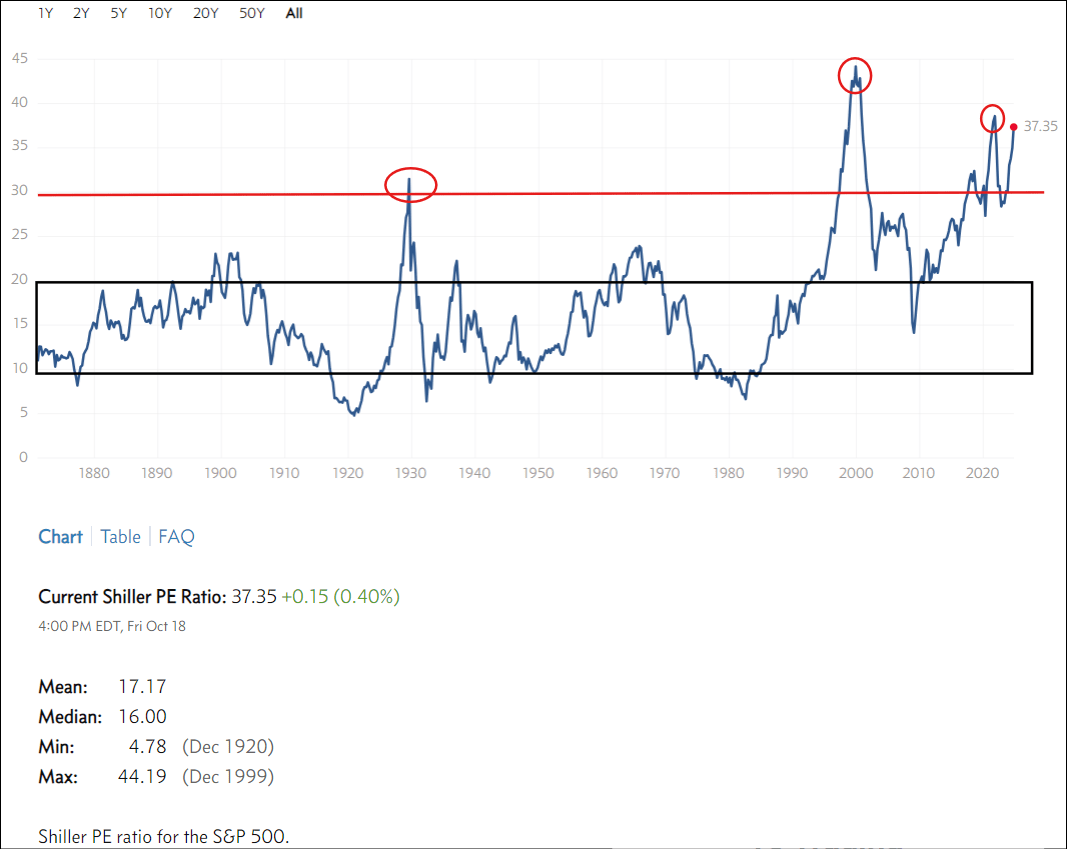

From a historical standpoint, equity market valuations are bubblicious, with the S&P-500 Shiller PE ratio currently sitting at ~37.35x – the highest level outside of the dot-com bubble [1999-2001] and the ZIRP bubble [2021].

Author, Multpl

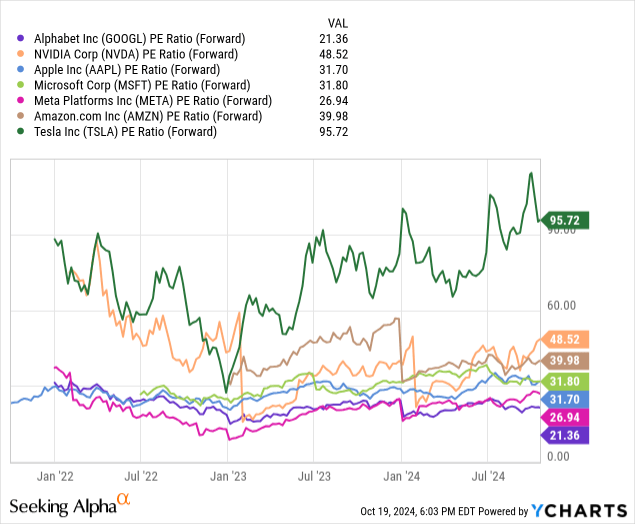

While market generals, i.e., mega-cap tech conglomerates, are now as or more expensive than at the 2021 peak, Alphabet Inc. (NASDAQ:GOOGL)(NASDAQ:GOOG) is an outlier – trading at a 20-50%+ discount to its “Magnificent 7” peers heading into its Q3 2024 report on 29th October 2024.

Now, last month, we zeroed in on anti-trust issues as the primary factor behind Alphabet’s relative discount and viewed the anti-trust fear-driven stock weakness as a buying opportunity:

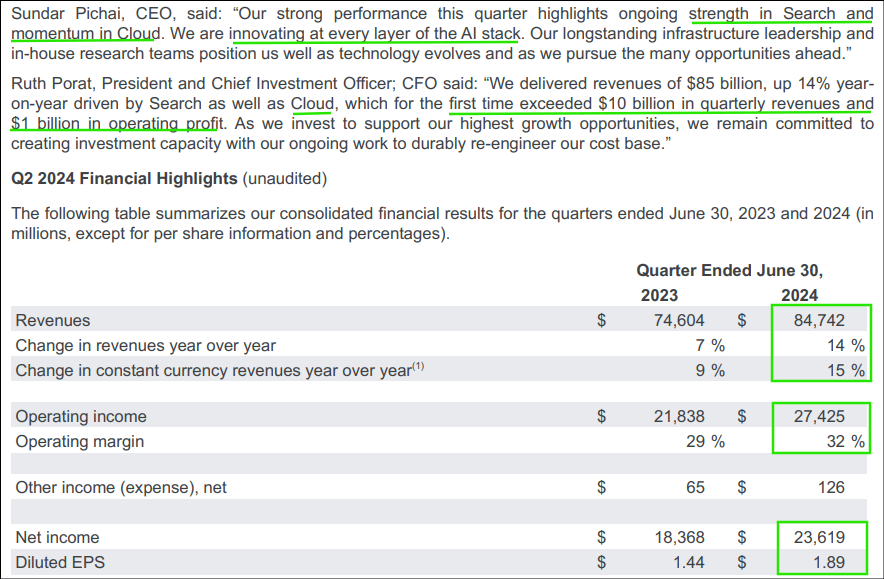

Given Alphabet’s robust business performance in Q2 2024 – revenue growth re-accelerating to +14% y/y, operating margins expanding by 300 bps y/y to 32%, and diluted EPS jumping +31% y/y – I think it is natural for market participants to ascribe GOOGL’s lack of participation in the broad market bounce off of early-August lows to its recent loss in the “Search” monopoly antitrust case and the kick-off of a second antitrust lawsuit [centered around Alphabet’s ad-tech business] last week.

Alphabet Investor Relations

While Alphabet faces no immediate remediations, a federal judge declaring Google a monopolist is an unnecessary distraction:

After having carefully considered and weighed the witness testimony and evidence, the court reaches the following conclusion: Google is a monopolist, and it has acted as one to maintain its monopoly. It has violated Section 2 of the Sherman Act.

Now, I have no clue which way the stock will swing based on the potential outcomes of these antitrust lawsuits. I am no legal expert, but I think Google will challenge any future negative verdicts—and it could be years before something happens on the fines/breakup front.

Yes, Alphabet’s antitrust woes could lead to a multi-year price and/or time correction in GOOGL stock similar to what Microsoft experienced from the early 2000s to the mid-2010s [especially in the event of a hard landing]. On the flip side, we know that Mr. Market tends to have the memory of a fish, and Alphabet’s antitrust headline-driven weakness could just as well be a temporary blip.

Basing an investment decision on the potential outcome of a lawsuit is a fool’s errand, and I would never indulge in that game. With that said, Alphabet’s business performance remains robust in the face of negative antitrust headlines, and its long-term risk/reward has improved enough to warrant a rating upgrade. Hence, I am upgrading Alphabet to a “Buy”.

Key Takeaway: I rate Alphabet stock a “Buy” in the $150s.

In today’s note, we shall preview Alphabet’s upcoming report and re-evaluate GOOGL stock using TQI’s Valuation Model to see if it’s a buy/sell/hold.

What Is The Earnings Forecast For Alphabet?

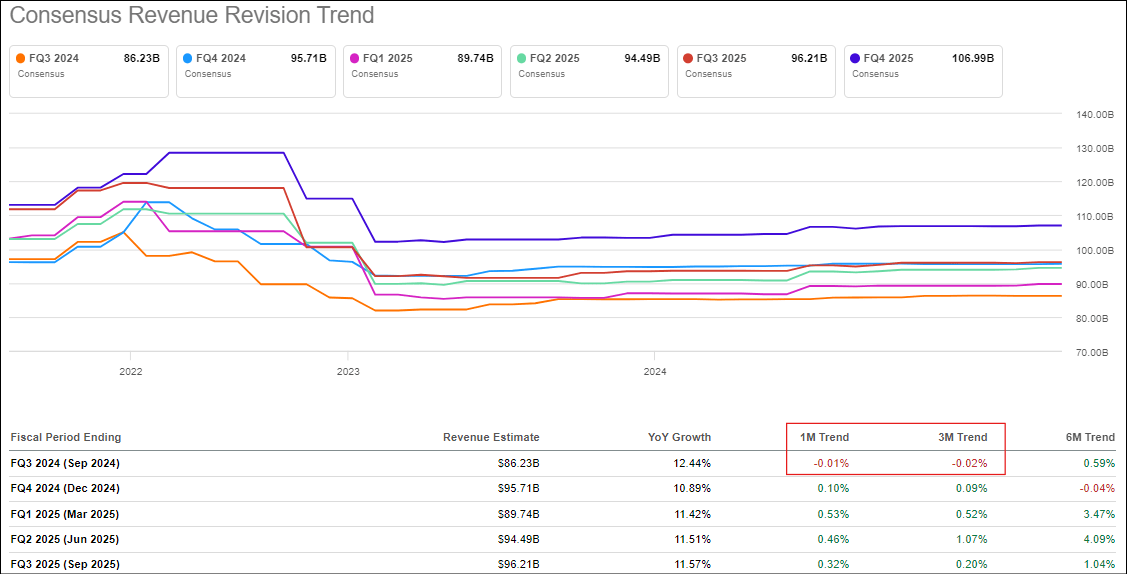

According to consensus analyst estimates, Alphabet will deliver total revenue of $86.2B (+12.4% y/y) for Q3 2024, with estimates ranging from $84.9B to $87.5B. While concerns about AI chatbots ending Google’s Search dominance aren’t entirely invalid, they are undoubtedly premature, given Alphabet’s market share trends and robust business momentum.

SeekingAlpha

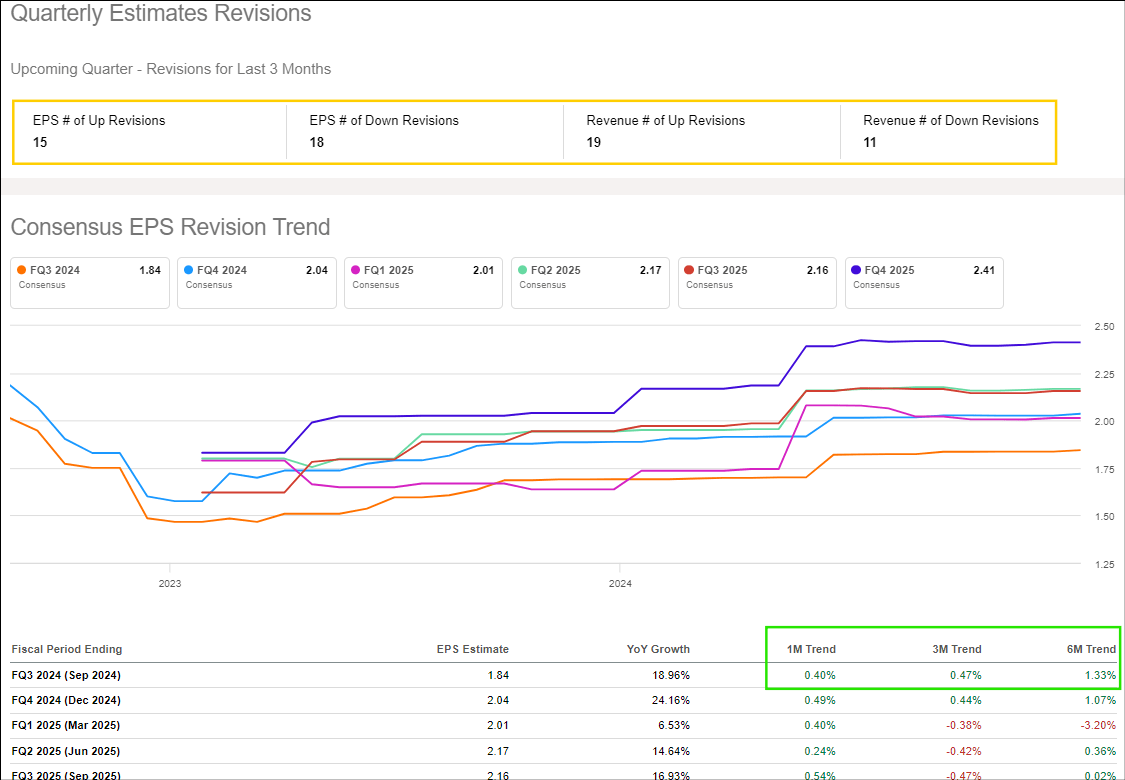

In addition to healthy top-line growth, Alphabet’s non-GAAP EPS is expected to keep outpacing sales growth this quarter, with the consensus EPS estimate sitting at $1.84 per share [+18.9% y/y].

At Alphabet’s humongous scale, a double-digit top and bottom line growth rate is mighty impressive. That said, Alphabet’s revenue and EPS revision trends for Q3 look quite mixed heading into the print. Despite EPS “Down” revisions outnumbering “Up” revisions, EPS revision trends are slightly positive on a 1-month, 3-month, and 6-month basis.

SeekingAlpha

SeekingAlpha

On the other hand, revenue revision trends are slightly negative despite 19 “Up” revisions and only 10 “Down” revisions on Q3 projections. Since the quantum of revisions is insignificant, I believe Alphabet is primed to deliver a solid quarterly showing yet again.

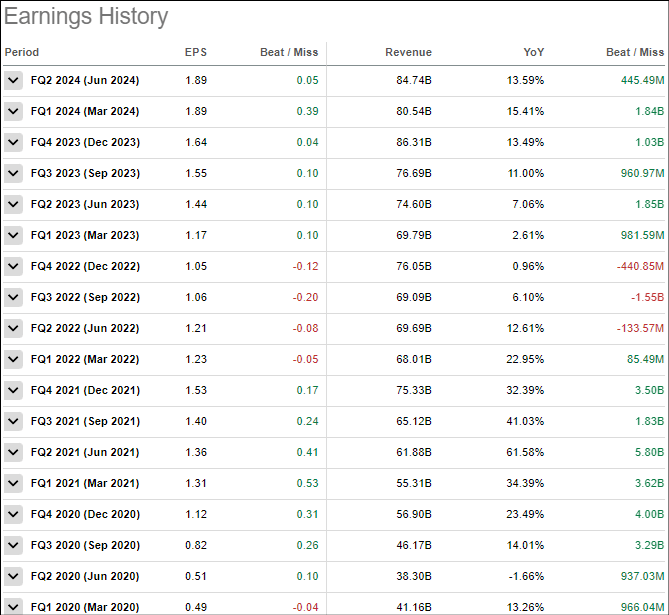

In recent quarters, Alphabet’s revenue and EPS beats have narrowed; however, GOOGL’s management has a long-standing track record of exceeding consensus street estimates, and I wouldn’t be surprised to see another beat next week.

SeekingAlpha

On a relative basis, Alphabet is attractively priced and appears to be a decent hideout for long-term investors in a pricey stock market! However, is GOOGL’s long-term risk/reward high enough to warrant the allocation of fresh capital?

Concluding Thoughts: Is GOOGL Stock A Buy, Sell, Or Hold?

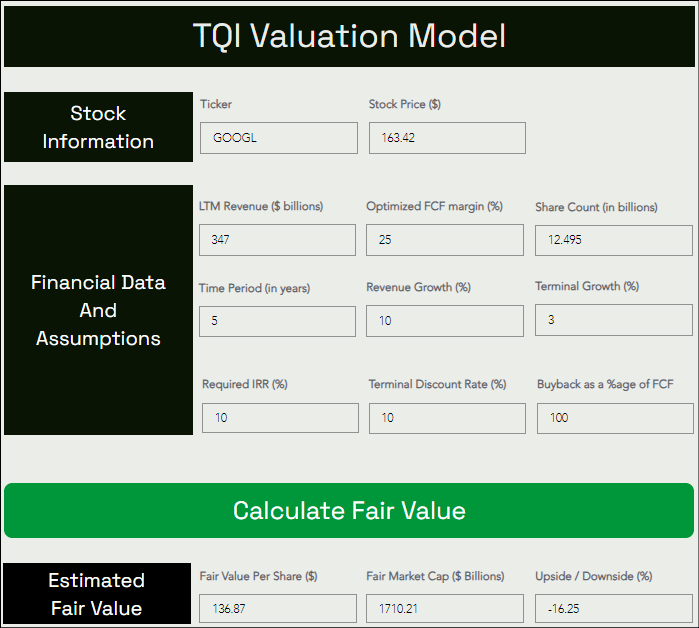

With the year drawing to a close, I am using Alphabet’s 2024E revenue of $347B (instead of TTM revenue) as the base for today’s valuation exercise. For modeling-period sales growth and optimized FCF margins, I am sticking to our previous assumptions of 10% CAGR and 25%, respectively.

Generally, I utilize a 15% discount rate in my DCF models. However, considering Alphabet’s business resilience and robust cash flow generation, we will continue to rely on a lower discount rate of 10%, which I have only used for Microsoft (MSFT) and Apple (AAPL) in the past.

All other assumptions are relatively straightforward, but if you have any questions, please share them in the comments below.

Here’s my updated model for GOOGL:

TQI Valuation Model (Free to use at TQIG.org)

As you can see above, TQI’s fair value estimate for Alphabet has moved up from $129.49 per share (or $1.62T market cap) to $136.87 per share (or $1.70T in market cap). With GOOGL stock trading at ~$163.4 per share, it is still in the overvalued territory; however, if we add back Alphabet’s huge cash hoard of $100B+ (~$8 per share), the valuation premium is less than 15%.

TQI Valuation Model (Free to use at TQIG.org)

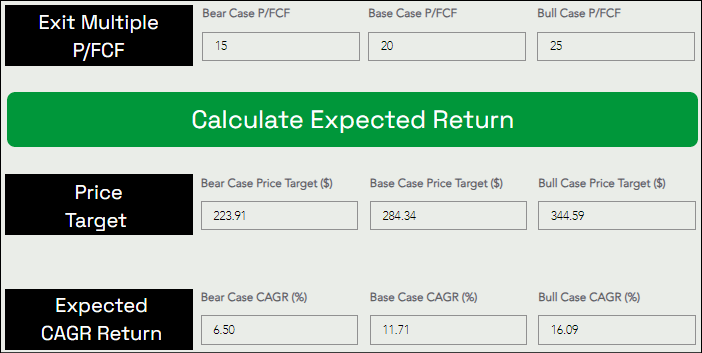

Assuming a base case P/FCF (exit) multiple of ~20x, Alphabet’s stock could rise from $163 per share to $284 per share at a CAGR rate of ~12% over the next five years. With GOOGL’s expected CAGR returns beating our investment hurdle rate of 10% for high-quality, low-volatility stocks, I continue to like the idea of buying GOOGL stock ahead of its Q3 2024 report.

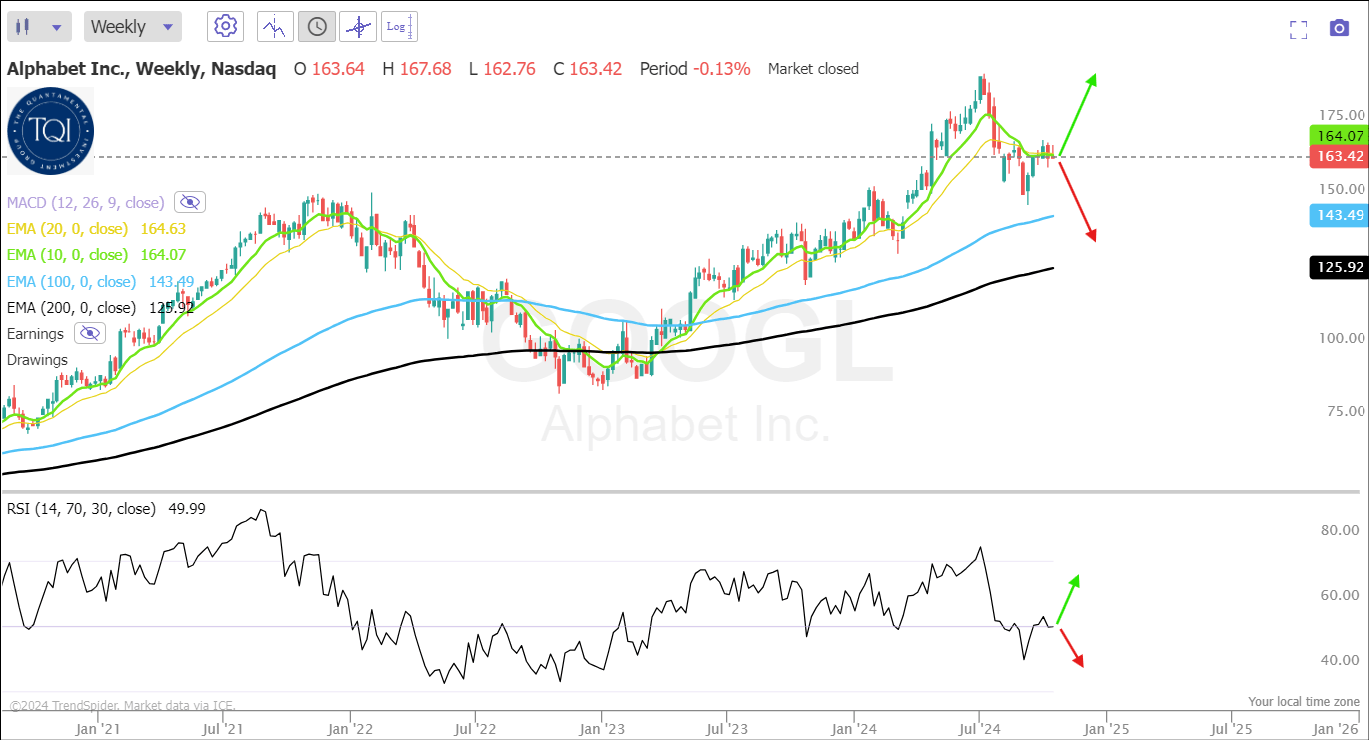

From a technical perspective, Alphabet’s momentum is still bullish, with the stock sitting at 10-week and 20-week moving averages. As long as GOOGL holds these support levels, the digital advertising giant could trade back up to recent highs in the $190s in the near to medium-term future.

Author, TrendSpider

Contrastingly, a breakdown from current levels cannot be ruled out, given the recent rollover in Weekly RSI from 70+ to ~50. In that scenario, GOOGL could find support in the $125-$145 range. While I would like to buy GOOGL at my fair value estimate of ~$136 per share, I can see Alphabet stock going in either direction. Hence, I prefer accumulation using a 12-24 month plan – avoiding all guesswork.

Key Takeaway: Heading into Alphabet’s Q3 2024 report, I continue to rate GOOGL stock a “Buy” in the $160s.

Thank you for reading, and happy investing! Please share any questions, thoughts, and/or concerns in the comments section below or DM me.

Analyst’s Disclosure:I/we have a beneficial long position in the shares of GOOGL either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.

We Are In An Asset Bubble, And TQI Can Help You Navigate It Profitably!

Your investing journey is unique, and so are your investment goals and risk tolerance levels. This is precisely why we designed our investing group – “The Quantamental Investor” – to help you build a robust investing operation that can fulfill (and exceed) your long-term financial goals.

At TQI, we are pursuing bold, active investing with proactive risk management to navigate this highly uncertain macroeconomic environment. Join our investing community and take control of your financial future today.