Summary:

- PayPal’s growth is driven by Venmo’s user engagement, omnichannel payments, AI-leveraged advertising, and cryptocurrency integration, despite regulatory and competitive challenges.

- Regulatory risks from CFPB’s new BNPL rules and the upcoming presidential election could impact PayPal’s operational costs and regulatory landscape.

- Despite competition from Stripe and Square, PayPal’s innovations and strong financial performance, including increased free cash flow and EPS growth, support a ‘Buy’ rating.

- PayPal’s current valuation appears undervalued compared to historical metrics, suggesting long-term growth potential and financial strength are not fully recognized by the market.

Sundry Photography

Thesis

PayPal Holdings, Inc. (NASDAQ:PYPL) stands as a top American fintech company, focusing on online payments and digital financial services. This article takes a closer look at PYPL, diving into some key issues along the way. We’ll explore potential regulatory challenges from the Consumer Financial Protection Bureau’s (CFPB) new rules extending credit card protections to BNPL providers, as well as how the Presidential election could shape the regulatory landscape. I’ll also touch on Bernstein’s recent downgrade over competition and valuation concerns, and wrap up with what investors might expect from the earnings report coming on October 29, 2024.

PayPal’s Consumer Base and Growth

With so many people using it, PayPal has become a household name. About 80% of Americans have used it in recent years. I’m on it all the time, especially as everything goes more cashless these days. For example, here in Florida, I don’t need quarters for a trip to the beach anymore. Parking in Palm Beach is pushing $10 an hour now, but thanks to PayPal’s integration with the ParkMobile app, I can (reluctantly) pay up and still hit the ocean. That’s just one of the many ways everyday folks like me use it.

Venmo’s Rising User Engagement

Building on its growing consumer base, PayPal’s subsidiary Venmo is making a big impact on the company’s success. Venmo, which has gone from being a quirky way to pay your friends for pizza to a full-on financial player, is now driving some serious success for PayPal with a 30% boost in monthly active users for both the app and its debit card in the second quarter, showing that consumer interest is on the rise.

PayPal has decided to make itself more useful for the routine parts of life. With a 5% cash-back offer on groceries and gas, the company is smartly nudging itself out of its e-commerce niche and into more everyday spending.

Strengthening its omnichannel approach, PayPal is now integrating with Apple Pay and Google Wallet, using NFC technology to tap into offline purchases and offer smooth payment options both online and in stores.

For those unfamiliar, NFC or Near-Field Communication is a technology that lets devices, like smartphones, send payment info to a terminal when they’re close together. PayPal uses this technology so you can make quick and secure payments by simply tapping your phone at a store’s checkout, without needing to swipe a card or handle cash.

Innovations Driving Business Growth

On the innovation side, PayPal’s Fastlane feature for guest checkouts has given merchants a serious boost, taking returning users’ checkout success from 40%-50% up to a solid 80%. This not only makes the checkout process smoother, but also drives double-digit growth in conversions, making PayPal a go-to platform for businesses.

At the same time, PayPal has been fine-tuning its monetization strategy through Braintree, having pricing-to-value discussions with big companies and rolling out extra services like risk management and foreign exchange. Such actions have supported its revenue streams and provided even greater value for enterprise customers.

PayPal’s AI-Leveraged Expanding Advertising Business

On top of everything else PayPal’s got going on, its advertising business is quietly shaping up to be quite the growth opportunity. The company is leveraging its massive consumer data to deliver ads that hit the mark better for merchants, which could lead to stronger returns on investment for advertisers and boost PayPal’s revenue streams. Meanwhile, they’ve also been very busy cutting costs and boosting efficiency, thanks to automation and AI helping them streamline operations and keep spending under control, all while freeing up more cash flow.

So, basically, PayPal has a ton of data about what people are actually buying, not just what they’re looking for. That means they can build detailed profiles of their customers — like knowing their favorite color, size, or what they’ve bought in the past. With the customer’s permission, PayPal can let merchants use this info to target ads specifically to the right person, at the right moment, making the ads way more effective.

For example, if someone is on a website, and the merchant already knows they wear a size large and love blue, they can show them a personalized “buy now” option that fits those preferences. PayPal’s unique position lets them connect merchants with customers through this system, helping businesses make smarter advertising choices. On top of that, the PayPal app itself has a built-in shopping experience where merchants can get even more exposure, targeting customers based on things like recent purchases — like knowing someone who bought a tent might be planning a camping trip.

Cryptocurrency and Strategic Partnerships

PayPal’s leap into the world of cryptocurrency was, in many ways, like the moment my mother joined Instagram — unexpected, slightly bewildering, but oddly inevitable. In 2020, without much ado, PayPal launched crypto services that enabled you to hold, buy, and sell digital currencies such as Bitcoin and Ethereum right inside your PayPal account.

In 2023, PayPal further expanded its crypto offerings by launching its own stablecoin backed by U.S. dollar reserves that promises to make transactions faster and cheaper, whether you’re dealing in the usual cash or digital currencies. And since PYUSD is pegged to the U.S. dollar, it offers a steady alternative to the maddening roller coaster that most other cryptocurrencies offer. Naturally, PayPal is eager to see it used in Web3 and decentralized apps.

At the same time, they’ve smoothly integrated PYUSD into PayPal’s ecosystem, even bringing Venmo into the mix. On top of that, they’ve expanded PYUSD across multiple blockchains, including Ethereum and Solana. Solana, by the way, stands out for offering faster and cheaper transactions.

Fast forward, and PYUSD has already hit a $1 billion market cap. On top of that, PayPal has teamed up with big names like Amazon and Shopify, locking in its position in e-commerce and boosting both checkout integration and transaction volumes.

Global Reach and Operational Efficiency

PayPal’s making moves beyond just cryptocurrency and partnerships, with its growing active accounts and transaction volume showing its global reach and efficiency. In the second quarter, active accounts jumped by almost two million, pushing the total to 429 million. Monthly active users also climbed 3% year-over-year, hitting 222 million.

The company posted an 11% bump in total payment volume (TPV) both in the U.S. and internationally, fueled by strong performance in places like continental Europe and Asia. On top of that, PayPal’s non-GAAP operating margins grew by 230 basis points, reaching 18.5%, showing they’re tightening up operations even more.

Competition Concerns

Despite all the good news coming out of PayPal’s quarterly reports (strong growth, operational improvements, and a general sense that they’re humming along quite nicely), Bernstein has raised a cautionary eyebrow. Apparently, they’re not entirely convinced PayPal can keep its throne in the increasingly jam-packed payments landscape. So much so, they went ahead and downgraded the stock.

The main issue? The fast-changing payments industry is putting pressure on PayPal to hold on to its competitive edge. Newer fintech players like Stripe and Square are grabbing market share with sleek, mobile-friendly payment solutions that come with lower fees and more flexible, developer-friendly platforms. Stripe has really made waves by simplifying online payment processing, especially for e-commerce, while Square dominates with point-of-sale solutions. These up-and-comers are rolling out specialized services for businesses and consumers, like Stripe’s developer-focused options and Google Pay’s growing presence among Android users. These companies tend to be more nimble, making it easier for them to quickly launch new features and keep up with the demand for a better user experience.

Also, some caution flags are popping up in PayPal’s credit business, which took a hit with year-over-year revenue down because of stricter risk management and higher loss rates. On top of that, the transaction takes rate dropped, mainly due to the faster growth in big companies and the effects of foreign exchange fees. PayPal’s outlook for the second half of the year is based on steady macroeconomic conditions, but if the economy takes a turn, their forecast could be thrown off.

Mature U.S. Market and Growth Limits

A curious dilemma PayPal finds itself in is that, while it pushes ahead with grand expansion plans, the majority of its U.S. consumer base, folks like you and me, are already well-acquainted with the platform. In fact, when you look at it from a different angle, the fact that 80% of us have already taken the plunge leaves PayPal staring at the uncomfortable reality that growth in this mature market might be running on fumes.

Then there’s Braintree, one of PayPal’s key moneymakers, which is expected to putter along at a slower pace. Why? Because the company is now getting bogged down in strategic pricing talks with big enterprises, which could slow down PayPal’s overall growth.

Regulatory Risks from BNPL Rules

Regulatory risks are ramping up for Buy Now, Pay Later (BNPL) players like PayPal and Klarna (KLAR), thanks to new rules from the CFPB. These new guidelines essentially take the protections you’d expect from a good old-fashioned credit card and slap them right on top of BNPL. So now, when you decide to split that pricey purchase into four easy payments, you’ve got the same rights as if you’d whipped out a Visa — think disputes, refunds, and, of course, clearer billing.

These changes could hike up operational costs as providers scramble to upgrade their systems to stay compliant. Naturally, PayPal and others aren’t thrilled. They say the rules came down too fast, and what works for credit cards doesn’t quite fit the BNPL model. Now, they’re pushing back, which has sparked some legal battles and might drive their costs up even more.

Valuation Concerns vs. Growth Potential

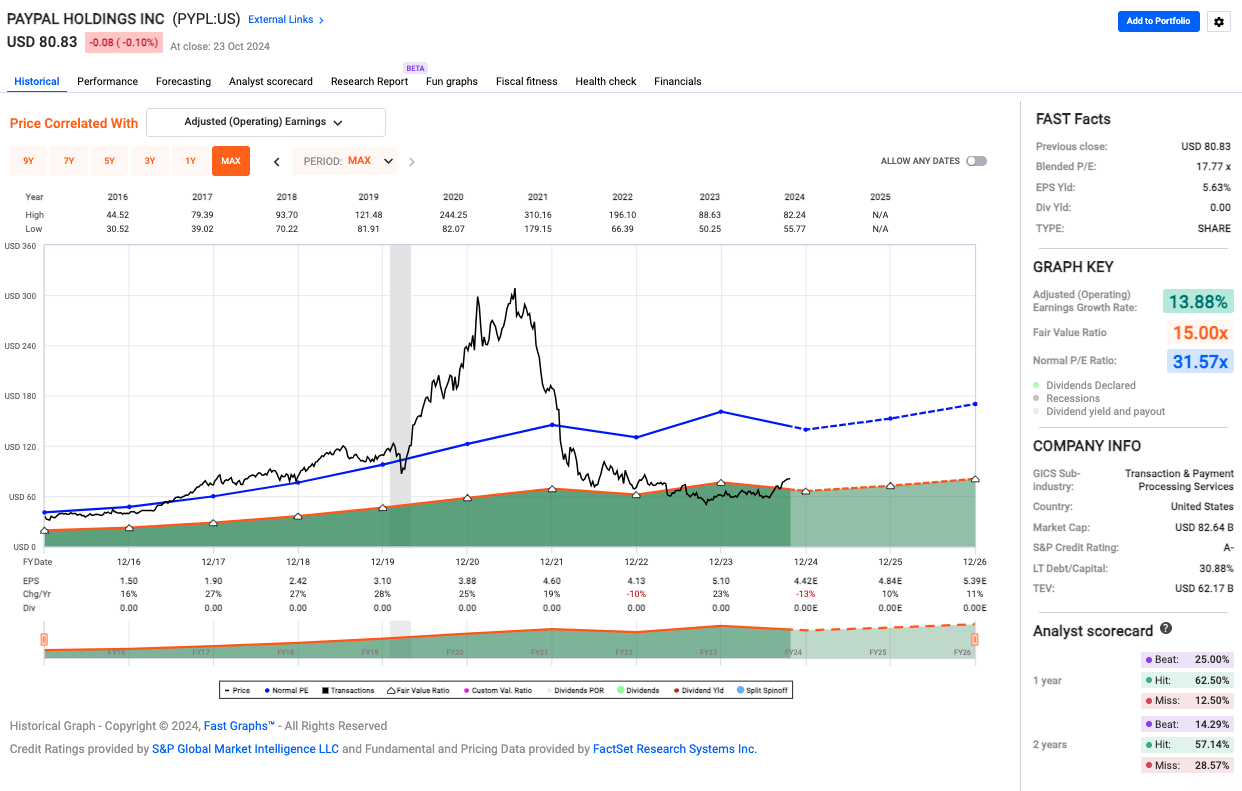

Fast Graphs

While regulatory challenges and uncertainties in PayPal’s transformation process may create some risks, going back to Bernstein’s overvaluation take, I believe it’s overstated. With a blended P/E ratio of 17.77x, it’s looking undervalued compared to its usual 31.57x, which suggests to me that the market isn’t fully recognizing PayPal’s long-term potential, and this disconnect could be tied to inflation worries.

That said, revenue growth at 13.88% is solid, showing PayPal is handling its core business well. But the market’s hesitance to boost the stock price likely comes from that competition sentiment, which might be overdone here, as the EPS yield of 5.63% shows PayPal’s still got strong earning power. Overall, the bottom line, in my opinion, is that I don’t think the valuation fully matches PayPal’s growth potential or financial strength.

In terms of financial performance, PayPal boosted its free cash flow target to $6 billion for 2024, mostly to fund stock buybacks, showing its serious about returning value to shareholders. In the second quarter, revenue was up 9% on a currency-neutral basis.

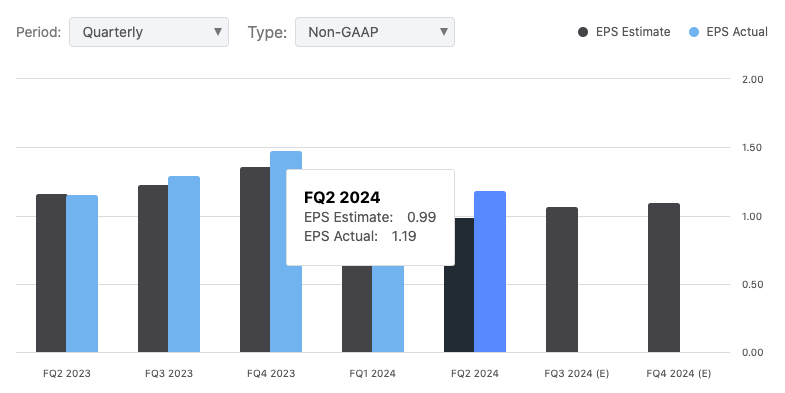

Seeking Alpha

Transaction margin dollars jumped 8%, the best growth PayPal has seen in that area since 2021, while non-GAAP earnings per share shot up 36% year-over-year to $1.19. Looking ahead, PayPal raised its full-year guidance for both transaction margin dollars and non-GAAP EPS, with earnings projected to grow in the low to mid-teens in 2024.

Political Landscape Impact on Regulations

Finally, with the presidential election looming ever closer, companies like PayPal and Square could see some changes depending on who takes office. If Donald Trump finds his way back to the Oval Office, we could be looking at a lighter regulatory touch. For instance, he could roll back things like credit card late fees, meaning less oversight and lower costs for payment platforms.

However, should Kamala Harris take the helm, it’s likely that PayPal and its digital cousins will still have to endure the same regulatory attention they’ve been getting. The current administration is already keeping a close watch on payment platforms, so, for companies like PayPal, it would be a case of “meet the new boss, same as the old boss,” with scrutiny remaining very much the order of the day.

Final Takeaway

I’m initiating coverage of PYPL here with a ‘Buy’ rating. Even with regulatory risks and increased competition, PayPal’s mix of growth drivers, from Venmo’s user base to new ways to pay, including omnichannel payments, and a growing crypto and advertising ecosystem, sets it up well for future growth. It also looks cheap on the price-to-history scale, and the company’s strong results and its ability to deliver value to shareholders are proof of long-term conviction.

Analyst’s Disclosure: I/we have a beneficial long position in the shares of PYPL either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.