Summary:

- Palantir Technologies Inc.’s Q3 earnings were strong, with revenue up 30% YoY to $726M and EPS beating estimates, but the stock remains expensive.

- US Commercial revenue surged 54% YoY, driven by AI demand, while US Government revenue grew 40% YoY, showing strong segment performance.

- Palantir’s cash flow remains robust with $435M in adjusted free cash flow and $4.6B in cash, but valuation is at nosebleed levels.

- Despite impressive growth, Palantir’s stock is expensive at $42 per share and the stock is rallying more, making it even pricier.

- Consider selling at a premium here.

Ghulam Hussain

Palantir Technologies Inc. (NYSE:PLTR) has been a powerhouse stock this year, really rallying hard and taking our house position higher with it. We have been in and out of tactical trades in this name, but have enjoyed a core position that has really ramped up. It has rallied so hard that we have had near-term concerns about a reversal, and we’re anxiously awaiting the just-announced quarterly earnings. We believe this was a strong report, and in this column we discuss the highlights that stand out to us.

Palantir Q3 earnings in context

In the just-reported quarterly earnings, we saw performance which was ahead of consensus estimates on revenues, while earnings per share print a penny above expectations. We also saw a raise on the guide. Solid quarter overall. As the company continues to grow, the pace of revenue growth is slowing versus past years. The law of large numbers is kicking in here. Still, the growth is strong and there is room for more governments and more businesses to contract with Palantir in our opinion.

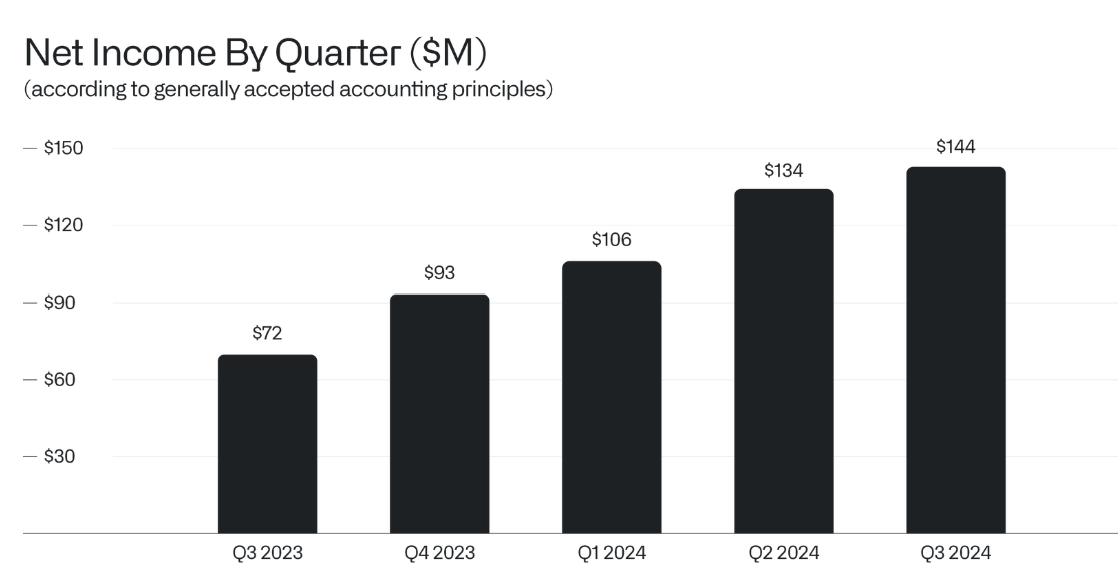

Palantir Q3 earnings revenue growth and profitability

With that said, the pace of revenue growth remains strong. Total revenue grew 30% year-over-year to $726 million, beating estimates by $21 million. Palantir’s profitability was in line at $0.10 per share. Being consistently profitable is a win, but make no mistake, shares are at a premium to the actual and projected future earnings. While Palantir can grow into this valuation, it is expensive. Still, the trend in earnings is definitely positive:

Palantir Q3 2024 shareholder letter

This is slow and steady growth, and quite positive. Now, that said, Palantir has two reporting segments in both the Government and Commercial segments.

Palantir Q3 earnings segment performance

This company is an AI winner. And we know that commercial revenue is benefitting from AI. US Commercial growth is back, and strong. US commercial revenue grew 54% year-over-year and 12% quarter-over-quarter to $179 million, strong, while the US commercial customer count grew sizably year-over-year. This is a testament to the sales team at the company, but the sales and marketing teams are not extravagant. This reacceleration stems from demand for Palantir’s AI offerings, which is why when the stock was sub $10 we called it the real AI winner. That is right, getting our investors at BAD BEAT Investing, Seeking Alpha’s premier trading service, into the stock sub-$10.

Commercial revenue has continued to be pretty strong, but Government results have been mixed for several quarters. But with ongoing international conflicts and new partnerships being made with defense companies, we think this supports ongoing growth. In Q3, US Government revenue grew 40% year-over-year and 115% quarter-over-quarter to $320 million. Of course, the US Government is the largest customer in this segment.

Can the pace of growth remain strong with tough comps to lap? Keep an eye on the customer count

So we do question whether the pace of growth can be maintained, or even expanded. With the larger numbers being reported and being compared to, the percentage change increases are harder to be massive when comps are made to larger revenue numbers. This is something to keep in mind when considering the pace of growth coming down.

Still, the growth is there. We have seen previously that the pace of customer growth by count had slowed. There had been an average regular growth of about 30 customers a quarter coming into H1 of 2024, but we have seen a recent bump thanks to the expansion of the sales team, and they are delivering. So we saw a 39% increase year-over-year in total customer count. Customer count growth has expanded versus recent quarters, and this is very bullish in our opinion.

Cash flow is king

Palantir remains cash flow positive, and very much so. Adjusted free cash flow was $435 million for the quarter, and the 16th straight quarter for which this was positive. The other major positive is that the company has $4.6 billion in cash and equivalents and no debt. This is also positive. Cash from operations was $420 million, representing a 58% margin, while the adjusted free cash flow margin was 60%. On a trailing 12-month basis, adjusted free cash flow is over $1 billion.

Palantir stock is at nosebleed valuation levels

The growth is there, but the stock is inarguably expensive. It is really expensive. When we consider the valuation, thanks to the growth, Palantir stock has only gotten more and more expensive. Given that the market will now be looking for heavy ongoing EPS growth, not just sales and customer growth, the valuation is incredibly rich here at $42 per share, even more since the stock is rallying after hours. And the analyst expectations for EPS growth are not all that impressive, frankly.

Seeking Alpha PLTR Earnings Estimates

Sure, the 32% growth this year is impressive, but for the next two years, growth expectations show a slowing as the comps get tougher to lap. Palantir will need to really continue to overdeliver and really up future guidance to see the stock rally from here. So here at $42 (or higher on the rally now) we are at about 34 times sales looking forward. That is fine for a company with rampant growth, but anticipated revenue growth of some 20% is tough to justify such a valuation. The EV/EBITDA on a FWD basis is 90X, with a price to cash flow over 100X. These valuations are difficult to come by without wildfire-like growth. We like the company, own Palantir Technologies Inc. stock, and while the growth is respectable, shares are inarguably extremely expensive.

Take home

The performance of Palantir Technologies Inc. stock has been wonderful, but undoubtedly the stock is expensive. The results in Q3 were very strong. Continue to watch margins and customer counts. We are positive about the prospects for the company and think we see Palantir continue to win more and more contracts, convert more customers, and deliver strong results. However, the price of the stock merits a hold here. Long-term we like the stock, in the near term traders should continue to embrace the volatility and consider selling option premium for income, especially on this bump. The increased guide was impressive, and this is one we like to continue running our house position.

Analyst’s Disclosure: I/we have a beneficial long position in the shares of PLTR either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.

Come trade with us

Get more with our playbook to significantly grow your wealth by embracing a blended trading and investing approach at our one-stop shop.

Our prices go up at the end of the month, but right now we have a big sale on the current price. Join NOW and you can lock in 75% of savings versus the $1,668 some members pay, this sale will end when 3 more members sign up.

We invite you to try us out, with a money back guarantee if you are not satisfied (you will be). Let’s win together. Come take the next step. START WINNING!