Amazon.com, Inc.’s Q3 2024 report exceeded expectations with strong revenue and EPS growth, driven by its twin growth engine — AWS and Ads.

While Amazon stock popped +6% post-ER, insider selling by Jeff Bezos at $200 hindered a breakout above multi-year resistance.

Despite robust fundamentals, Amazon’s stock is slightly overvalued post-earnings and its 5-year expected CAGR return of ~14% has dropped below our investment hurdle rate, rendering AMZN a “Hold.”.

Emma McIntyre/Getty Images Entertainment

Introduction

Last week, in my earnings preview, I rated Amazon.com, Inc. (NASDAQ:AMZN) stock a modest “Buy” based on its robust business fundamentals and favorable long-term risk/reward [reasonable valuation], despite acknowledging a dicey technical setup for AMZN stock:

Going into its Q3 2024 report on 31st October 2024, Amazon.com, Inc. stock is trading at a key make-or-break level. On one hand, a positive quarterly report could trigger a powerful bullish breakout above multi-year resistance range of ~$190-200 per share. And, on the other hand, a rejection here could confirm a bearish double-top pattern that can culminate in a significant drawdown in AMZN stock.

Author (TrendSpider)

Technically, AMZN stock is finely balanced, with a big breakout or breakdown on the table. With Amazon’s stock holding above key short-term moving averages [10-week and 20-week MA], i.e., technical momentum is bullish going into the Q3 print. However, with weekly RSI and MACD rolling over, a strong rejection and pullback from here cannot be ruled out.

Considering AMZN’s fundamental, quantitative, valuation, and technical data, I don’t like it as a short-term earnings trade. However, for the long-run, AMZN is still an attractive investment at current levels.

Key Takeaway: I rate Amazon stock a modest “Buy” in the $180s-$190s.

In today’s note, we will review Amazon’s Q3 2024 report and reevaluate its long-term risk/reward and technicals to formulate an informed investment decision on the technology conglomerate.

How Did Amazon Fare In Q3 2024?

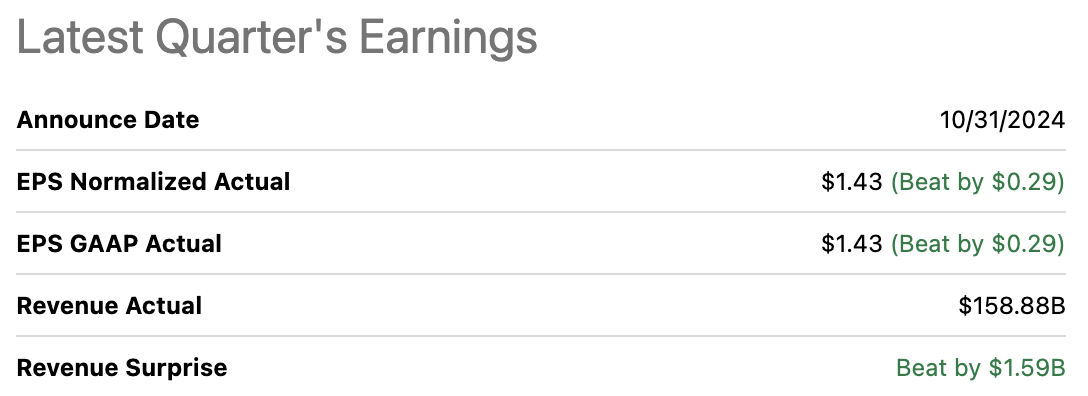

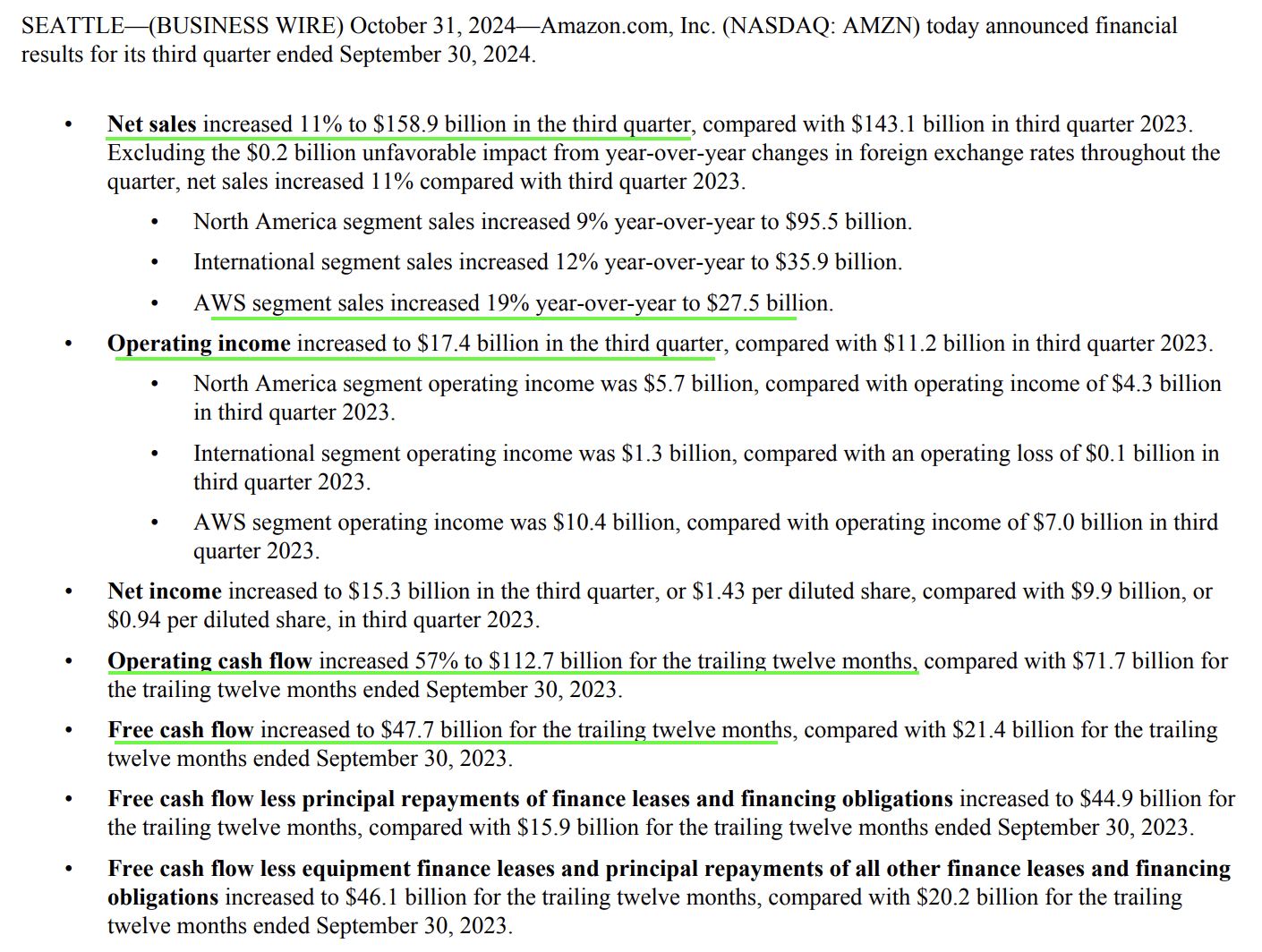

For Q3 2024, Amazon reported strong headline numbers that blew past consensus estimates on both top and bottom lines, with revenues rising +11% to $158.9B [vs. est. $157.3B] and normalized EPS coming in at $1.43 per share, well ahead of street expectations of $1.14 per share:

SeekingAlpha

Amazon Investor Relations

While Amazon is an operating leverage story at this point, the business continues to grow at a healthy pace driven by broad strength across retail/e-commerce, AWS Cloud, and Digital Ads. Furthermore, with AWS’s AI business revenues growing at a triple digit y/y growth rate [~3x faster than AWS did at similar scale back in its early days], the top-line momentum at Amazon is unlikely to fade anytime soon.

Amazon Investor Relations

At TQI, Amazon is one of our largest holdings, and if you have been following my work, you know that the twin growth engine of AWS and Ads is the crux of our investment case. And, based on Amazon CEO, Andy Jassy’s prepared remarks on the Q3 2024 earnings call, this twin growth engine is firing on all cylinders (emphasis added):

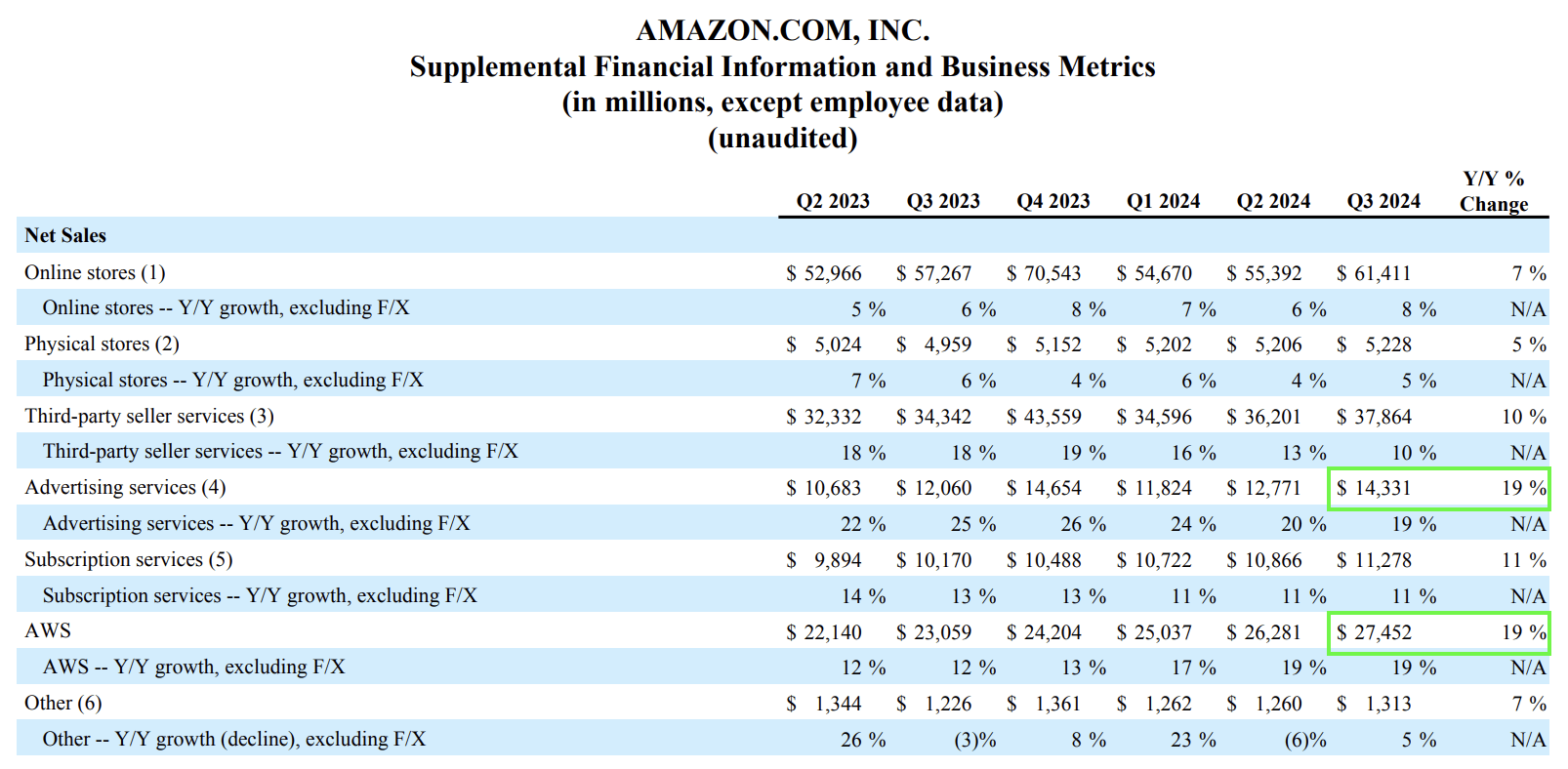

In advertising, we remain pleased with our progress, generating $14.3 billion of revenue in the quarter, 18.8% year-over-year growth. Our expansive reach, ability to service relevant offers to our customers, opportunity to engage customers from the top of the funnel to point of purchase, and leading capabilities around measuring outcomes at every touch point provide all types of brands with full funnel advertising at scale.

With sponsored products, we’re seeing meaningful growth on a very large base, and we see further opportunity in driving even better performance for advertisers by further improving the relevancy of the ads we show and by providing additional optimization controls. At the same time, some of our newer offerings are in their very early days. We’re just entering our first broadcast season for Prime Video advertising, following a very strong showing at upfronts. And we’re continuing to support brands of all sizes with our Generative AI-powered creative tools across display, video and audio, including our video generator that uses a single product image to curate custom AI-generated videos. While we’re generating a lot of advertising revenue today, there remains considerable upside.

AWS grew 19.1% year-over-year and now stands at a $110 billion annualized run rate. We’ve seen significant reacceleration of AWS growth for the last four quarters. With the broadest functionality, the strongest security and operational performance and the deepest partner community, AWS continues to be a customer’s partner of choice. There are signs of this in every part of AWS’s business. We see more enterprises growing their footprint in the cloud, evidenced in part by recent customer deals with the ANZ Banking Group, Booking.com, Capital One, Fast Retailing, Itaú Unibanco, National Australia Bank, Sony, T-Mobile, and Toyota.

Companies are focused on new efforts again, spending energy on modernizing their infrastructure from on-premises to the cloud. This modernization enables companies to save money, innovate more quickly, and get more productivity from their scarce engineering resources. However, it also allows them to organize their data in the right architecture and environment to do Generative AI at scale. It’s much harder to be successful and competitive in Generative AI if your data is not in the cloud.

The AWS team continues to make rapid progress in delivering AI capabilities for customers in building a substantial AI business. In the last 18 months, AWS has released nearly twice as many machine learning and GenAI features as the other leading cloud providers combined. AWS’s AI business is a multibillion-dollar revenue run rate business that continues to grow at a triple-digit year-over-year percentage and is growing more than 3 times faster at this stage of its evolution as AWS itself grew, and we felt like AWS grew pretty quickly.

The advent of Generative AI has triggered a gold rush, and cloud hyperscalers are spending billions and billions of dollars to capture this opportunity. In 2024 alone, Amazon is projected to spend ~$75B in CAPEX, with the majority of this spend going into AI infrastructure. While CAPEX growth rates should ease somewhat as we move into 2025, Amazon has entered into a new CAPEX spending cycle. Fortunately, this time around, Amazon’s core businesses are generating more cash than ever — with TTM Operating Cashflow increasing 57% y/y to $112.7B and TTM FCF rising +128% to $47.7B in Q3 2024.

Amid its ongoing revenue mix shift towards faster-growing, higher-margin AWS [cloud] and Ads businesses, I continue to believe that Amazon’s cash flows and profits are set to rise significantly in upcoming years. And at some point, I see Amazon turning into an infinite buyback pump akin to some of its Mag-7 peers like Apple (AAPL), Microsoft (MSFT), Alphabet (GOOGL), etc.

What’s Next For Amazon?

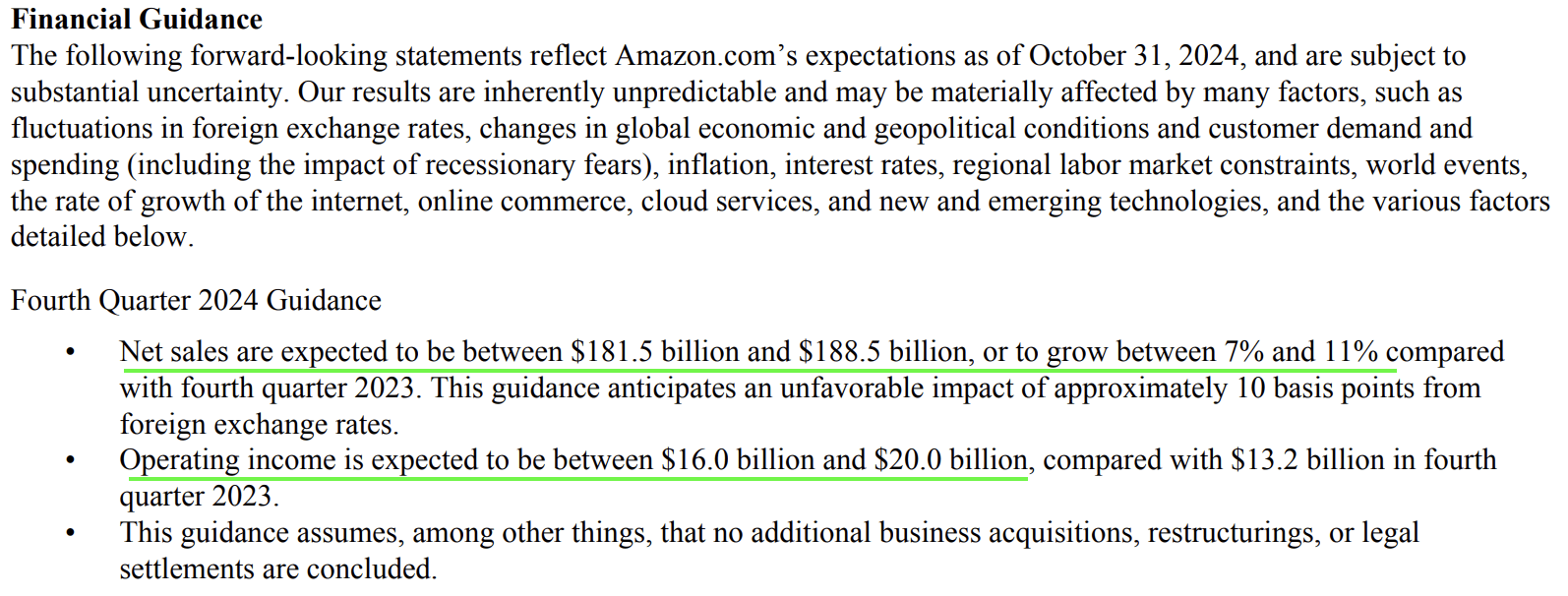

Heading into the Holiday season, Amazon’s management has guided for Q4 2024 net sales of $181.5-188.5B (growth of 7-11% y/y) and operating income of $16-20B (+21-51% y/y).

Amazon Investor Relations

With the unemployment rate holding steady at 4.1% and the long-end of the treasury yield curve shifting up recently, the Fed is likely to pause its rate-cutting cycle at the November meeting. The prevailing market conditions are filled with uncertainties, but as long as economic resilience persists, given its management’s history of sandbagging guidance, Amazon will likely continue to deliver robust business performance in the next quarter and beyond.

Amazon Fair Value And Expected Return

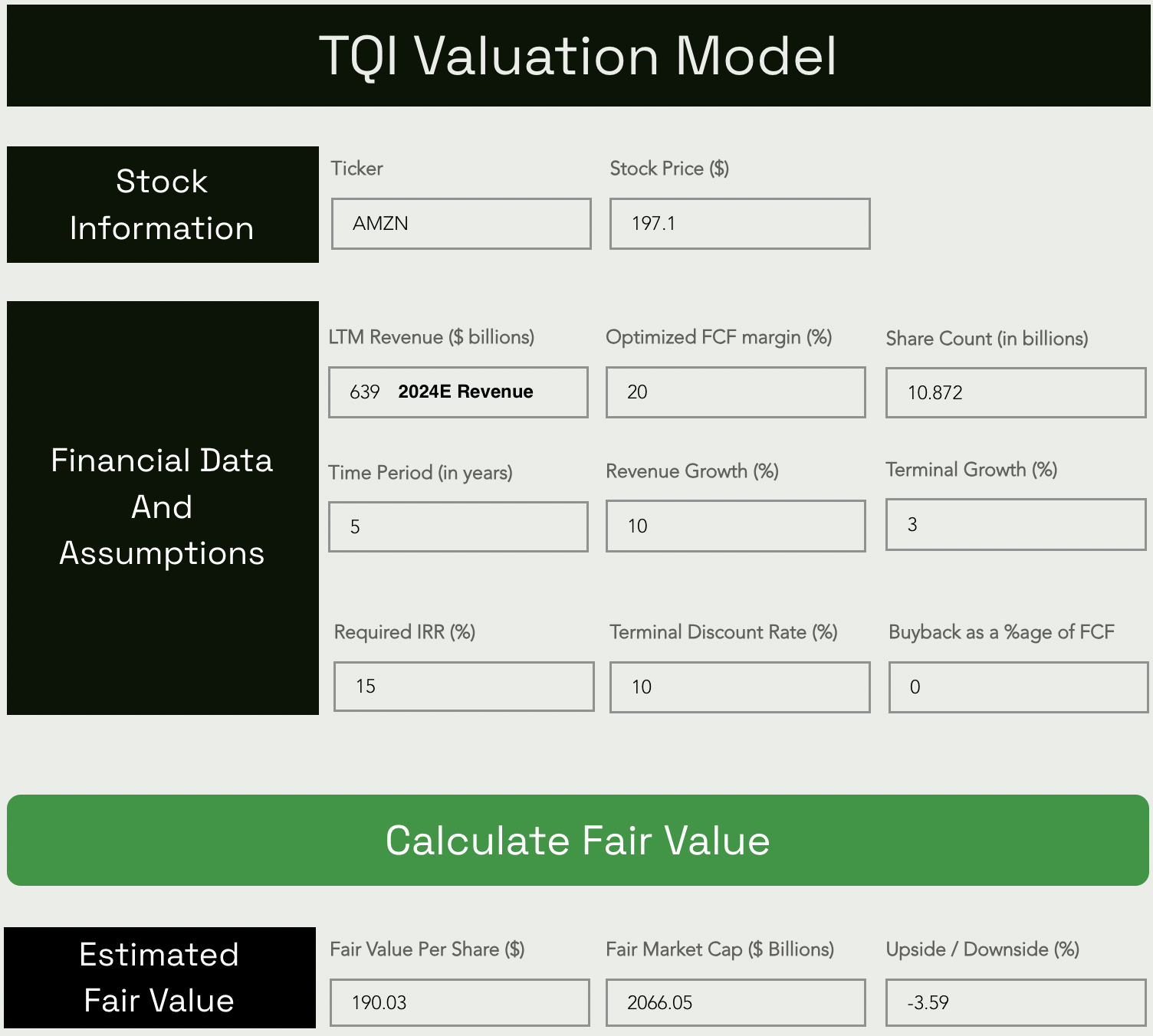

In light of Amazon’s Q3 2024 report, TQI’s fair value estimate for AMZN stock has moved up slightly to ~$190 per share (or $2.07T). As we do with all of our valuations, we continue to utilize conservative assumptions for future growth rates [5-year CAGR sales growth of 10%] and optimized FCF margins [20%].

With AMZN stock jumping up from $189 to $197 post-ER, it has become slightly overvalued. However, Amazon is still one of the most reasonably valued names in the big tech basket!

TQI Valuation Model (Free to use at TQIG.org)

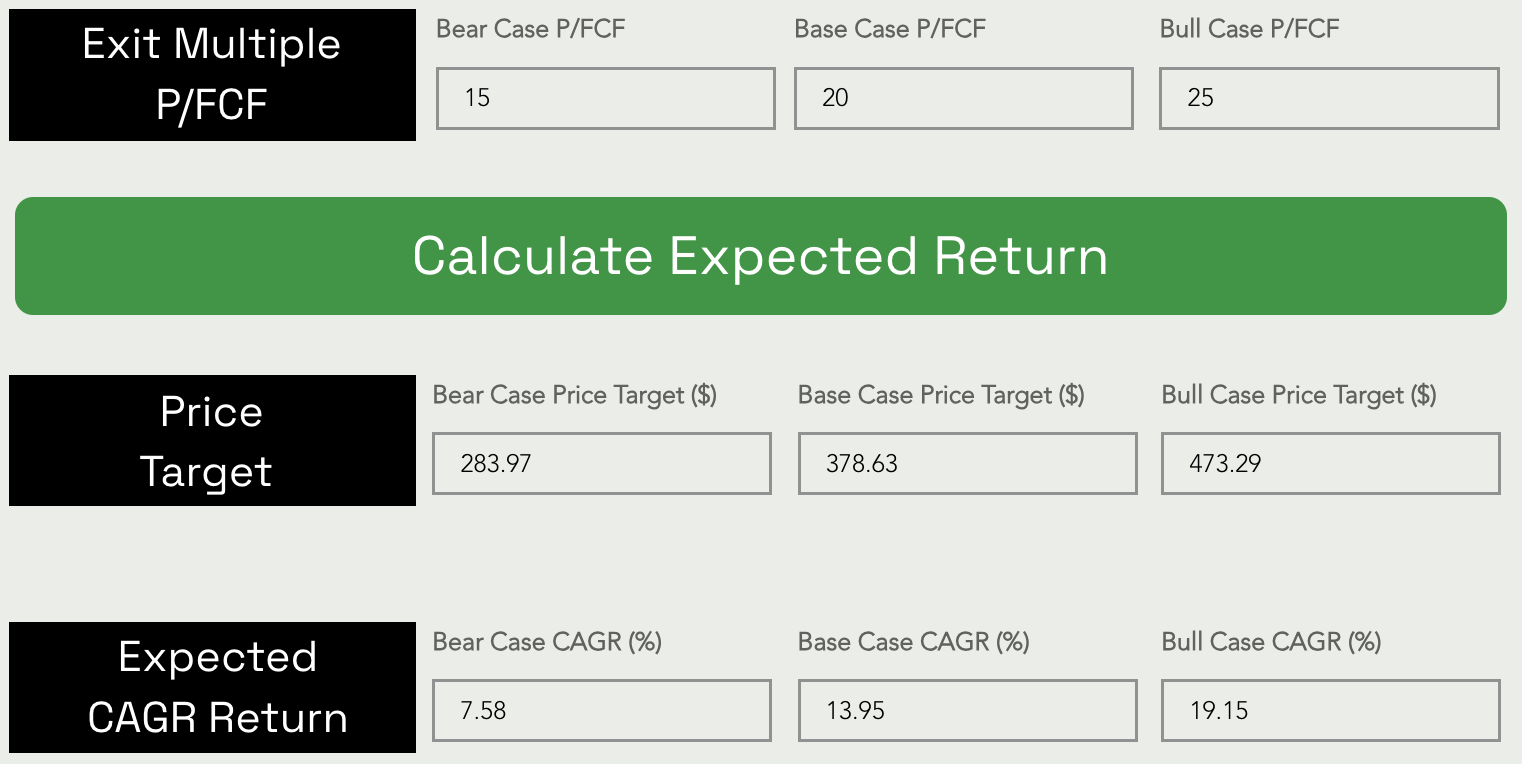

Predicting where a stock will trade in the short term is impossible; however, over the long run, a stock will track its business fundamentals and obey the immutable laws of money. If the interest rates were to return to artificially low levels (i.e., ZIRP), higher equity multiples would be justifiable. However, I work with the assumption that interest rates will eventually track the long-term average of ~5%. Inverting this number, we get a trading multiple of ~20x (P/FCF).

Assuming a base case exit multiple of 20x P/FCF, I see Amazon’s stock price rising from ~$197 to ~$378 per share at a CAGR rate of ~14% over the next five years.

TQI Valuation Model (Free to use at TQIG.org)

As you can see above, Amazon’s 5-year expected CAGR return has slipped under our investment hurdle of 15%, i.e., AMZN is now a “Hold” under our valuation process.

Now, with S&P 500’s (SPY) long-term annual return of 8-10%, AMZN stock could still be an attractive investment for investors willing to accept a somewhat lower return (especially since our model does not consider buybacks/dividends, which are only a matter of time given Amazon’s rapidly rising free cash flows).

Insider Selling And Technicals

In the absence of a severe economic downturn, Amazon’s business momentum will likely continue unabated in upcoming quarters, with AWS and Ads serving as the key pillars of profitable growth at the technology behemoth. The business is in fine fettle, and while the valuation is not as attractive as it has been in recent weeks and months, AMZN is still a decent long-term investment.

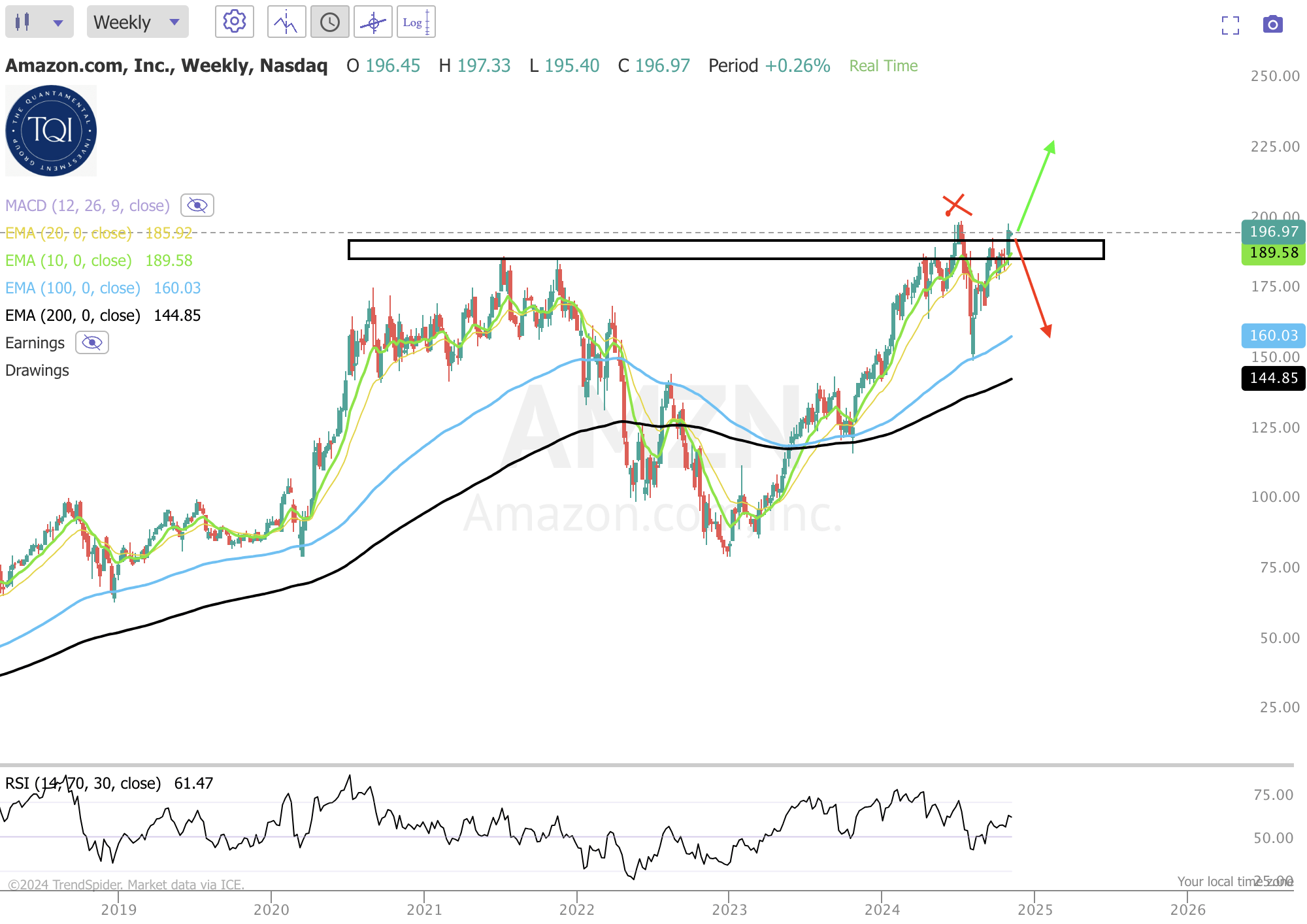

From a technical standpoint, I expressed optimism about Amazon stock breaking past multi-year resistance in the $190-200 range on a strong Q3 report ahead of earnings. While AMZN did jump up to the top of this resistance range post earnings, it failed to break past a Jeff Bezos-powered selling wall at $200 with Amazon’s Founder and Chairman selling $3B worth of shares on 1st November 2024.

Author (TrendSpider)

Now, Bezos owns more than 10% of Amazon. If he continues to sell billions of dollars’ worth of shares at that $200 level into open market, increased supply of AMZN shares due to insider selling could lead to another rejection from this multi-year resistance zone. On the downside, I see the $145-160 range as a potential long-term support for Amazon stock.

Concluding Thoughts: Is AMZN Stock A Buy, Sell, Or Hold?

As of Q3, Amazon’s business momentum remains strong, with its twin growth engine of AWS and Ads firing on all cylinders — supported by healthy expansion of its retail/e-commerce ecosystem. The technical setup for AMZN remains dicey, with massive insider selling from Jeff Bezos threatening to derail the attempted breakout from a multi-year resistance range. While I continue to like and own Amazon, its long-term risk/reward as measured by 5-year expected CAGR return has slid under our investment hurdle rate. Hence, I am downgrading AMZN stock to a “Hold” rating.

Key Takeaway: In the high $190s, I rate Amazon.com, Inc. stock a “Hold.”

Thank you for reading, and happy investing! Please share any questions, thoughts, and/or concerns in the comments section below.

Analyst’s Disclosure:I/we have a beneficial long position in the shares of AMZN either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.

We Are In An Asset Bubble, And TQI Can Help You Navigate It Profitably!

Your investing journey is unique, and so are your investment goals and risk tolerance levels. This is precisely why we designed our investing group – “The Quantamental Investor” – to help you build a robust investing operation that can fulfill (and exceed) your long-term financial goals.

At TQI, we are pursuing bold, active investing with proactive risk management to navigate this highly uncertain macroeconomic environment. Join our investing community and take control of your financial future today.