Summary:

- Lucid Group, Inc. beat top and bottom-line expectations for Q3 last week and is unfortunately seeing expanding losses on an operating and net income level.

- The EV maker confirmed its annual production target of 9,000 EVs, however.

- Lucid’s valuation is difficult to justify given its huge losses and reliance on steady capital raises, making it a highly speculative investment.

- Without significant delivery growth, Lucid and other EV makers will struggle to achieve profitability, making shares appear overvalued relative to fundamentals.

JannHuizenga

Lucid Group, Inc. (NASDAQ:LCID) submitted its third-quarter earnings sheet last Thursday, and the electric vehicle (“EV”) company beat bottom and top-line expectations. The EV maker saw a decent Q3 ’24 ramp in terms of deliveries as well, but Lucid did not make any progress in terms of narrowing its losses. The EV company, however, did confirm its annual production target of 9,000 electric vehicles, which indicates that at least the demand situation for Lucid did not deteriorate in the September quarter.

I believe Lucid remains a highly speculative EV investment for investors that could have an asymmetric return profile in case the Gravity SUV, which is expected to hit the market next year, has a good market reception. Considering that Lucid did not manage to contain its losses in the third-quarter, I am not prepared to risk a position at this point.

Previous rating

I rated shares of Lucid a hold in August after the EV maker reported second-quarter results which raised concerns for me at the time: Saudi Arabia To The Rescue. In the third-quarter, Lucid’s operating losses grew further, despite a higher production and delivery volume. Further, Lucid raised $1.7B in equity recently, which is boosting the company’s liquidity profile, but which highlights persistent dilution risks for shareholders. I don’t see an especially attractive risk profile after Q3 ’24, and I maintain my hold rating.

Q3 earnings, delivery ramp, widening losses

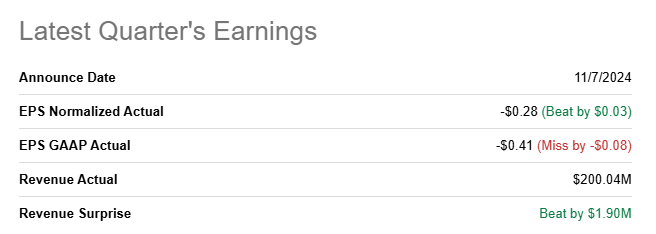

Lucid delivered both a bottom and top-line beat in the third fiscal quarter: the EV maker had an adjusted loss of $0.28 per-share, which beat the consensus estimate by $0.03 per-share. The top line came in higher than expected as well, at $200M, beating the average prediction by $1.9M.

Seeking Alpha

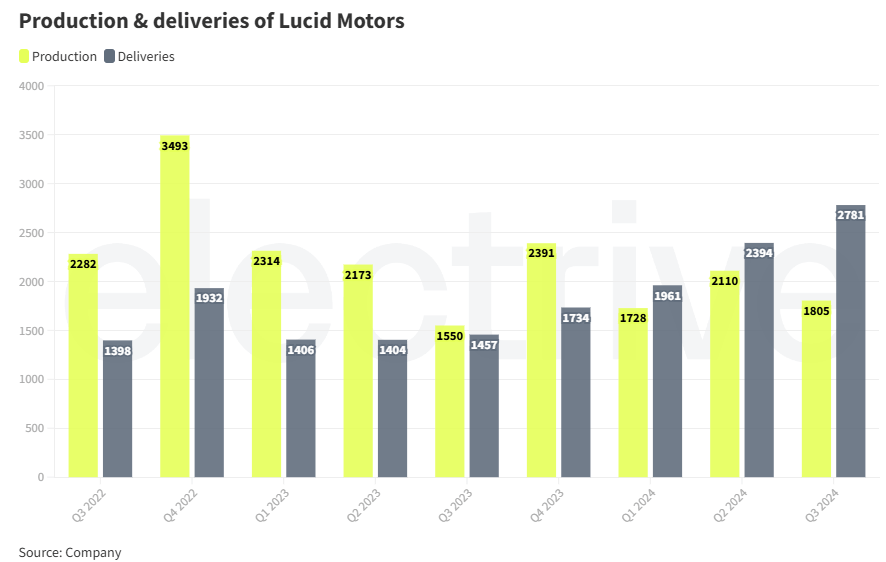

In terms of deliveries, Lucid is seeing a consistent ramp. Lucid delivered 2,781 electric vehicles to customers in the third-quarter, showing 91% growth year-over-year. The delivery figure also surpassed the consensus estimate of 2,242 electric vehicle deliveries, so deliveries is one area in which Lucid is actually quite well right now. Production totaled 1,805 electric vehicles, showing a year-over-year growth rate of 16%.

Electrify

While Lucid did report a significant increase in deliveries, the company just doesn’t have enough scale yet to make a difference in terms of its profitability profile.

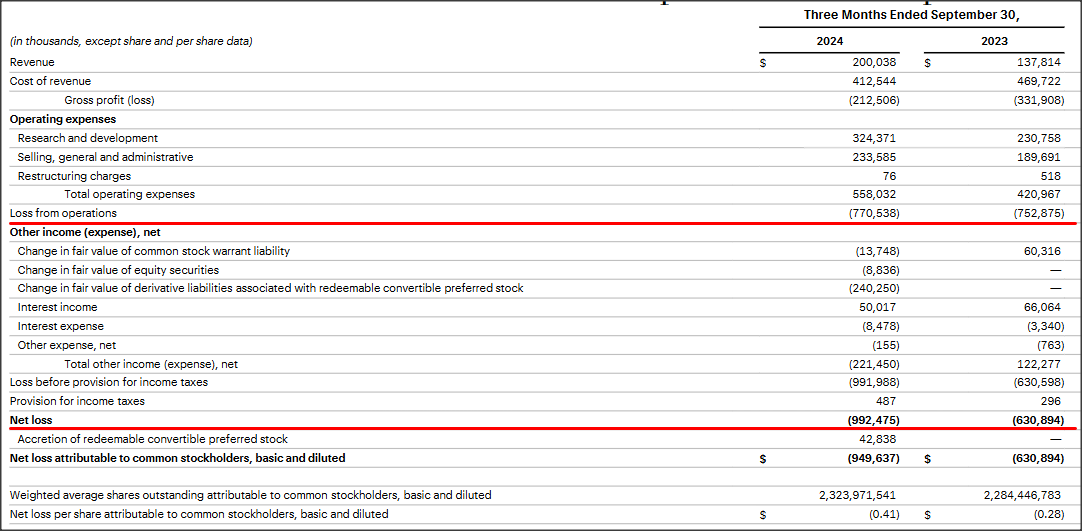

In the third-quarter, the EV maker generated revenues of $200M, showing 45% year-over-year growth. However, since Lucid is still very early in terms of ramping up its deliveries and still investing a lot of money into R&D, the company’s loss from operations actually expanded year-over-year in the September quarter. In the third-quarter, Lucid generated an operating loss of $771M, which widened from $753M in the year-earlier period. The same is true for the company’s net losses: in the most recent quarter, Lucid generated a net loss of close to $1.0B, showing a year-over-year surge of 57%.

The main reason for Lucid’s weak profitability profile is that the company has not yet grown into sufficient scale to support an earnings turnaround… and this indicates that the company will most likely experience many more quarters of pain. Further, the company, as I indicated, is still spending heavily on Research and Development and with the Gravity SUV set to go into production in Q4 ’24, investors are likely going to see expanding losses in the fourth-quarter as well. The implication here is that Lucid will most likely remain highly unprofitable and continue to depend on its wealthy backer, the Saudi Arabia PIF, to support the company’s expansion.

Lucid

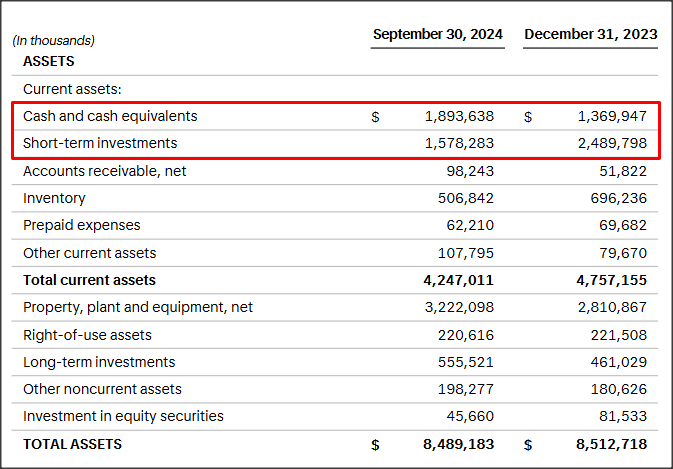

While the profitability picture is not yet where I would like it to be, the balance sheet looks a lot better. This is mainly because Lucid is in a comfortable position to be able to tap into the deep pockets of Saudi Arabia’s sovereign wealth fund, the Public Investment Fund. As of the end of September, Lucid had $3.5B in cash and investments sitting on its balance sheet, compared to $3.9B at the end of FY 2023.

Lucid

Lucid announced in October that it was selling 262.4M new shares, which allowed the company to raise $1.67B in cash. While Lucid can access funds from PIF, Lucid has drastically increased its share count in the last several years as well, which has been one reason for the company’s poor share performance. In the past three years, the share count has increased by 83% and investors should expect continual capital raises going forward.

Lucid’s valuation

Lucid’s valuation, in my opinion, is difficult to justify given its relatively low overall production volume. Like other EV makers, including Rivian Automotive (RIVN), the company has suffered from demand weakness which has weighed not only on total expected delivery volumes, but which also significantly impacted the profitability timeline. Lucid also cut its delivery outlook multiple times last year, which has further led to a loss of investor trust.

Shares of Lucid are currently valued at a price-to-revenue ratio of 3.7X, which makes the EV start-up much more expensive than Rivian (RIVN) stock, which is trading at a forward (FY 2025) P/S ratio of 2.0X. Rivian recently lowered its production guidance for FY 2024 to below 50k units, a fact that led me to down-grade shares to hold. Still, Rivian has a significantly higher output level than Lucid. I have also had a very favorable opinion on Tesla (TSLA), which is by far the most expensive large-cap EV stock, with a forward price-to-revenue ratio of 8.9X.

In my last work on Lucid, I stated that the EV company had a fair value of $2.50 per-share, based off a 3X fair value P/S ratio that I was willing to pay at the time. Since consensus estimates have declined since August and the EV maker now has an average consensus revenue prediction of $1.78B for next year, I calculate a fair value market cap, based off a 3.0X P/S ratio, of $5.3B or ~$2.00 per-share.

Risks with Lucid

Lucid is not yet profitable, and it may take years before the EV maker can actually generate some real profits. The company is losing money on each vehicle it sells and Lucid is not in a position to drastically scale its production, which would be required to improve Lucid’s profitability profile. What would change my mind about Lucid is if the EV firm saw a significant acceleration of its deliveries, positive booking/reservation momentum for the company’s newest EV product, the Gravity SUV, in case those numbers get released, and a change in direction of consensus revenue estimates.

Final thoughts

Lucid beat top and bottom-line expectations last week, and the EV manufacturer did not cut its production target for FY 2024. However, the rest of the earnings report did not look too great: the EV company reported an expansion in its losses, especially on a net income basis. Lucid Group, Inc., given the current business setup and profitability profile, is still too expensive, in my opinion, and the EV maker has considerable dilution risks going forward considering that it is still losing so much money. In order for shares to revalue higher, Lucid must grow its deliveries significantly and work towards self-sufficiency.

Analyst’s Disclosure: I/we have a beneficial long position in the shares of TSLA, RIVN either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.