Summary:

- Tesla, Inc. shares have surged over 42% recently, largely driven by Donald Trump’s re-election and CEO Elon Musk’s close association with him.

- Despite impressive cost-cutting and delivery forecasts, the limited growth story may not justify Tesla’s massive stock rally, warranting caution.

- Potential risks include the elimination of the EV tax credit in the US, which could significantly impact Tesla’s income statement.

Michael M. Santiago

Over the last week, one of the biggest winners in the market has been Tesla, Inc. (NASDAQ:TSLA). The electric vehicle maker has seen its shares soar after former President Donald Trump was re-elected to be the US’s top leader, and Tesla CEO Elon Musk has been by his side lately. At this point, it certainly seems that the fundamentals don’t support this massive move, which is why I’ve become a lot more cautious now on Tesla shares.

Previous coverage of the name:

Last month, I covered Tesla after the company reported a nice Q3 margin surprise, helping to send shares higher. Investors cheered management’s ability to further cut costs, while also being impressed by a better than expected delivery forecast for both the current period and 2025. Tesla clearly showed that it was the leader in the EV space, which was a key reason why shares traded at a significant premium to its competitors.

While Tesla shares were up about 9% in the after-hours session when my article was published, the rally has taken off considerably since. Despite the S&P 500 (SP500) only being up about 3% since my previous article, Tesla has delivered a more than 42% gain, with a large chunk coming recently. Should the rally continue like we’ve seen recently, shares could easily hit a new all-time high by this time next week.

Shares continue to soar:

With Donald Trump winning, plenty of investors have been believing good things are ahead for Elon Musk and his businesses. On one hand, Musk himself thought he’d end up in jail if Kamala Harris won, so the Trump win seemingly has reduced those chances significantly. Of course, there are questions over whether Elon Musk could potentially have to serve two masters. The Tesla CEO has been a vocal supporter of the Chinese government, which has provided the company with numerous benefits to date. If Donald Trump takes a hard stance against China, Elon Musk may have to choose a side, which could hurt the company in either of its top two sales markets.

The key question is: How will Tesla itself fare under a second Trump administration? The President-Elect has made it clear that he wants to roll back electric vehicle tax credits, which one would think could impact the EV leader’s sales. Trump’s mission to drive down energy prices may also hurt the electric space as well, as it would reduce potential fuel savings for consumers. However, Trump may want to throw Elon a bone for his campaign support, so maybe the situation isn’t as dire as originally thought.

Tesla’s near term prospects:

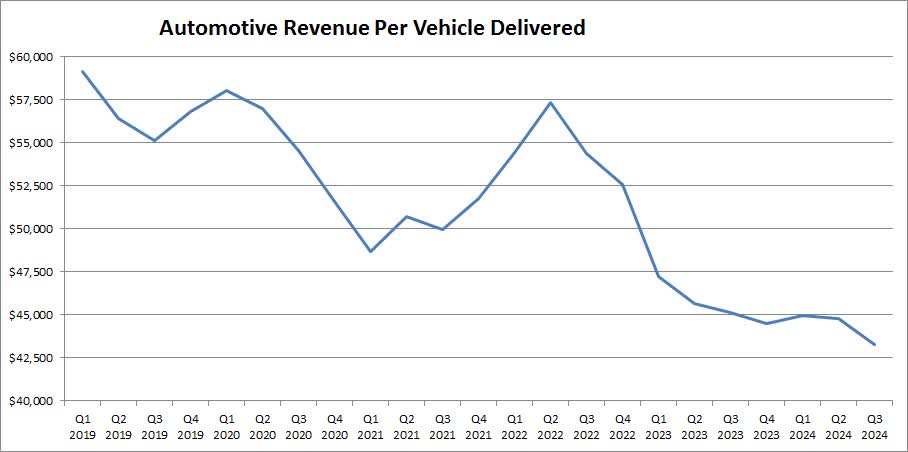

One of the key items for Tesla recently has been price cuts. To keep unit sales growing as interest rates have risen, and some countries have rolled back their incentives, the company has reduced prices on several models. As the chart below shows, automotive revenues per vehicle delivered, including leases and credit sales, hit a multi-year low in the most recent quarter.

Tesla Average Revenue Per Delivery (Company Earnings Reports)

The elimination of the EV tax credit in the US could dramatically impact things for the company. For now, let’s just assume that Tesla loses half of the credit’s value in revenue, or $3,750 per vehicle. Noted company watcher Troy Teslike estimated just over 157,000 deliveries for Tesla in the US in Q3, which would equal a loss of about $589 million in total revenue. While that would only mean about a 2.34% loss to Q3’s top-line number, it would mean a 14.6% loss to automotive gross margins and 27.2% loss to GAAP net income if you assume no other associated cost cuts.

As I discussed previously, Tesla management has called for a delivery record in Q4, saying that 2024 deliveries will top the 2023 total. This implies at least 515,000 vehicles to be sold in the current period, which many did not see possible going into last month’s report. The company has already started Q4 with some inventory discounts and other promotions, while the rally in the US dollar could provide an additional headwind to overall selling prices.

On the Q3 conference call, Elon Musk called for 20% to 30% growth in vehicle deliveries next year, after this year’s potentially slight increase. While this means that the 2024-2025 period will be well below the 50% a year target that management previously had, that guidance was better than most were expecting. A lot of this has to do with the further ramp of the Cybertruck and the launch of more affordable vehicles.

However, this likely means average selling prices will continue to decline, especially if sales of the cheaper vehicles cannibalize the Model 3 and Y, which itself could result in more price cuts. Currently, street analysts are looking for more than 16% revenue growth next year, although a good chunk of that is likely to come from the Tesla Energy segment, that’s growing much faster than the automotive business currently.

A look at valuations:

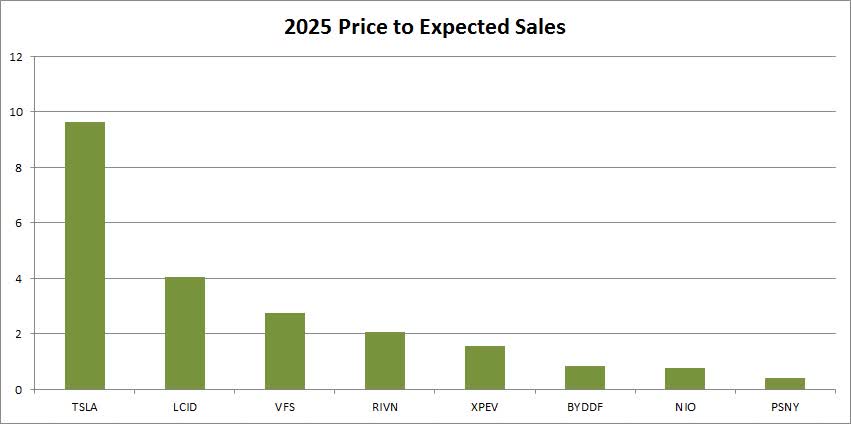

Tesla has always traded at a premium to other automakers based on its potential growth profile. In the past, investors were hoping for significant revenue growth from increasing deliveries, but now most of those hopes are more on the profits associated with autonomous vehicles. In the chart below, you can see how Tesla matches up on a price to expected sales basis for 2025 vs. other EV names as of early Monday afternoon — Lucid Group (LCID), VinFast (VFS), Rivian (RIVN), XPeng (XPEV), BYD Company (OTCPK:BYDDF), NIO (NIO), and Polestar (PSNY).

EV Price To Sales (Seeking Alpha)

Currently, Tesla shares are approaching 10 times their Street expected revenue for next year, more than double any other name on this list. When you look at total revenue growth, however, these other names are almost all expected to grow much faster in percentage terms, mostly due to lower revenue base amounts. The rest of the comparison group averages less than 1.8 times, with the three Chinese names barely averaging over 1.0 times. Let’s not also forget that traditional US automakers like Ford (F) and General Motors (GM) are only averaging about 0.3 times their expected 2025 revenues.

Final thoughts and recommendation:

Shares of Tesla have seen a massive rally since Donald Trump won last week’s election, building from their Q3 earnings report bump. Investors are hoping that Elon Musk’s support for the Presidential candidate will pay off for Tesla eventually. It is possible, however, that Trump’s potential policies could be a negative for Tesla and other EV names, especially if the US EV credit is reduced or even eliminated next year.

Given the massive rally, I am reducing my rating on Tesla shares to a sell today. I wouldn’t fault any investor for taking a 40% plus gain on a large cap stock like this over just a few weeks, especially with the valuation where it is currently. However, I’m not going to suggest that you run out and short Tesla shares today because the next $50 move could just as easily be up as it could be down. Locking in some quick profits seems like a logical move, and as we get more clarity on the Tesla 2025 vehicle lineup and President Trump’s potential policies, we can look at the rating on shares again then.

Analyst’s Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Investors are always reminded that before making any investment, you should do your own proper due diligence on any name directly or indirectly mentioned in this article. Investors should also consider seeking advice from a broker or financial adviser before making any investment decisions. Any material in this article should be considered general information, and not relied on as a formal investment recommendation.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.