Summary:

- Alibaba Group Holding Limited reported strong earnings, beating analyst expectations, but cash generation was weak; however, aggressive buybacks continue to reward shareholders.

- Revenue grew 5% year-over-year, with Cloud Computing and International Digital Commerce showing promising growth, despite a challenging Chinese consumer environment.

- Adjusted earnings per share declined slightly, but share repurchases provided a 5% tailwind, highlighting Alibaba’s commitment to returning value to shareholders.

- Despite risks from China’s real estate market and potential trade tensions, Alibaba’s low valuation and growth prospects make it an attractive investment opportunity.

maybefalse

Article Thesis

Alibaba Group Holding Limited (NYSE:BABA) (OTCPK:BABAF) has reported strong earnings results that beat the analyst consensus on both lines. While cash generation was sub-par during the quarter, Alibaba continued to reward shareholders handsomely with buybacks. Shares pulled back over the last couple of weeks, which is why Alibaba is now very inexpensive again.

Past Coverage

I have written about Alibaba Group Holding Limited in the past here on Seeking Alpha, most recently one year ago, when I gave the company a Buy rating. Shares are up since then, although they were up more in late September and early October on the back of China stimulus enthusiasm that has since waned to some degree. With one year having passed since my most recent article on Alibaba, and with the company reporting its most recent earnings results today, it is time for an update on the Chinese e-commerce player.

What Happened?

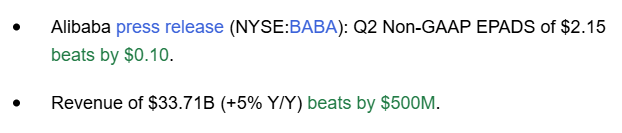

Alibaba Group Holdings Limited reported the results for its most recent quarter on Friday morning. The headline numbers looked like this:

Alibaba Group Holdings Limited earnings results (Seeking Alpha)

The company delivered a double beat, relative to what Wall Street analysts were forecasting, which naturally is a good result. Compared to BABA’s track record, relative to expectations, this was positive as well, as Alibaba has sometimes missed revenue and/or earnings per share estimates over the last two years or so.

The market’s reaction wasn’t positive, though, with shares trading down 3% at the time of writing. The broad market’s weak performance on Friday morning might help explain this relatively weak share price performance on the day of the earnings release. Investors may also be unhappy with BABA’s cash generation during the period — more on that later.

Alibaba’s Earnings Results: The Good And The Bad

Starting with Alibaba Group Holding’s top line, we see that revenues rose 5% compared to one year earlier. This isn’t an ultra-fast growth rate, but a solid result, considering the following factors:

- Alibaba trades at a very undemanding valuation. Thus, the company is not at all priced for a high growth rate.

- The Chinese consumer is not in a very bright spot right now, due to worries about the country’s real estate market. This is bad for consumer spending, which is why Alibaba is held back to some degree. A mid-single-digit growth rate in an environment like that is far from bad, I believe.

- Alibaba has become a massive company over the years, and maintaining a high relative growth rate becomes harder and harder as the company grows. Many other companies, including quality picks such as Apple Inc. (AAPL), have found out that growth inevitably slows down over time — AAPL’s growth rate during the most recent quarter was very comparable to BABA’s growth rate, at 6%.

Considering these factors, I find that Alibaba Group’s 5% revenue increase is far from a bad result in absolute terms. The growth rate was also higher than during the previous three quarters, suggesting that momentum is on BABA’s side right now. This does not guarantee that revenue growth will accelerate during the current quarter and beyond, but there is a solid chance of that happening, I believe.

Revenue growth was uneven across Alibaba’s different business units, with the Cloud Computing business delivering an above-average 7% growth rate compared to the previous year’s quarter. While this is not strong compared to the cloud growth rates that Amazon.com, Inc. (AMZN), Alphabet Inc. (GOOG), (GOOGL), etc. are delivering, there were some positives as well. Management stated that the public cloud growth rate during the most recent quarter was in the double digits, so with this part of the business growing over time, we might see accelerating overall cloud computing growth going forward. AI-related offerings grew at a triple-digit pace during the most recent quarter, which, of course, is great news.

While Alibaba is not considered a prime AI player by many, this data point suggests that the company nevertheless can benefit from the ongoing AI trend. If its current growth rate is maintained, this could become a major source of future revenue and earnings growth for the company.

Alibaba’s International Digital Commerce business also grew faster than the company-wide average, delivering a very nice 29% revenue gain, although from a not massive basis. Revenue came in at around $4.5 billion for the quarter, which is equal to a little more than 10% of the total. As this business continues to grow, its growing importance and growing revenue contribution for Alibaba, both on an absolute basis and on a relative basis, could help lift the overall business growth rate in the coming years. Management argues that investments in parts of Europe and the Middle East were among the growth drivers during the period, and I expect that these investments will continue, hopefully continuing to deliver an impressive growth rate for BABA’s IDC business.

Of course, business growth alone does not translate into strong returns — profits are even more important. On that front, BABA’s results didn’t look too strong, as adjusted earnings were down slightly compared to one year earlier, with adjusted EBITDA declining by 4% year-over-year. Management argues that this is due to increased growth investments — we will see whether those will pay off in the coming quarters. Looking at reported results, i.e., non-adjusted numbers, Alibaba managed a reasonable 5% operating income gain. The difference between the stronger GAAP growth rate and the weaker adjusted growth rate can be explained by lower share-based compensation expenses. Those are excluded from the adjusted result, while they are included in GAAP metrics, thus an expense decline results in rising profits, all else equal.

Net earnings per BABA share (technically an ADS), on an adjusted basis, totaled $2.15 for the period, which was down slightly compared to one year earlier. Earnings per share declined less than company-wide net profit, however, which is attributable to the fact that Alibaba’s share repurchases have reduced the company’s share count meaningfully over the last year. Overall, there was a 5% tailwind for earnings per share from the buybacks Alibaba did over the last year, which is pretty nice — AAPL’s famed buybacks, for example, reduce the share count by only 3% or so per year.

Alibaba continued to pursue buybacks aggressively during the most recent quarter, spending another $4.1 billion on share repurchases — around 2% of the company’s market capitalization. I like BABA’s aggressiveness when it comes to buybacks, as there was no good reason to hold billions of dollars of cash on the balance sheet without using that capital in a way that creates shareholder value.

The cash flow picture, unfortunately, wasn’t overly strong: Cash from operations totaled $4.5 billion during the quarter, or $18 billion annualized. While that is a strong number in absolute terms and relative to the company’s market capitalization of around $200 billion, the number was down compared to the previous year’s quarter. Management argues that this is due to the aforementioned increased investments in areas such as International Digital Commerce and AI Cloud offerings. If that is true and this is a temporary pullback, there is no reason to worry, but I would like to see the metric improve again in the coming quarters.

BABA: Cheap Again, But Not Risk-Free

At the end of September and in early October, enthusiasm about Chinese stimulus spending made BABA soar to as high as $118 per share. Since then, however, shares have pulled back by a lot. Now, with shares trading below $90 once more, BABA has gotten very inexpensive again. Based on current estimates for this year, BABA is valued at just 10x net profits. For a company with a strong franchise, an excellent market position, AI exposure, and some business growth, that is not at all a high valuation.

Alibaba is not risk-free: Exposure to the Chinese consumer means that a worsening real estate downturn in the country is a risk to consider, while an escalating trade war with the US could negatively impact Alibaba as well. These risks shouldn’t be ignored, but I also do not think that they make an investment in BABA impossible — in a diversified portfolio, BABA could have a place.

While cash generation was sub-par, results looked very solid apart from that. With revenue growth picking up compared to the last couple of quarters, with BABA trading at a very undemanding valuation, and with buybacks continuing at a strong pace, I am bullish on BABA overall. I sold my BABA position in late September during the China euphoria (I missed the top) but might re-enter BABA in the next couple of days.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Analyst’s Disclosure: I/we have a beneficial long position in the shares of GOOG either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

I might buy BABA in the next couple of days.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.

Is This an Income Stream Which Induces Fear?

The primary goal of the Cash Flow Kingdom Income Portfolio is to produce an overall yield in the 7% – 10% range. We accomplish this by combining several different income streams to form an attractive, steady portfolio payout. The portfolio’s price can fluctuate, but the income stream remains consistent. Start your free two-week trial today!

The primary goal of the Cash Flow Kingdom Income Portfolio is to produce an overall yield in the 7% – 10% range. We accomplish this by combining several different income streams to form an attractive, steady portfolio payout. The portfolio’s price can fluctuate, but the income stream remains consistent. Start your free two-week trial today!