After rocketing up to $120 per share on the back of China’s stimulus announcements, Alibaba Group Holding Limited’s stock has returned to its breakout point in the $80s.

In Q2 FY2025, Alibaba saw revenue growth of 5% y/y, driven by improved monetization in Taobao & Tmall, and triple-digit AI-related product revenue growth in Alibaba Cloud.

Despite a 70% y/y drop in free cash flow due to heavy investments across its core businesses, Alibaba’s robust financial foundation supports ongoing stock buybacks.

Fair value estimate for BABA stock is ~$217, with a potential upside of +150%, making it an incredible investment opportunity despite China’s geopolitical and macroeconomic challenges.

Alibaba’s resilient business performance, cheap valuation, and shareholder-friendly policies make it a “Strong Buy” at ~$80, with a potential 44% CAGR over five years.

maybefalse

Introduction

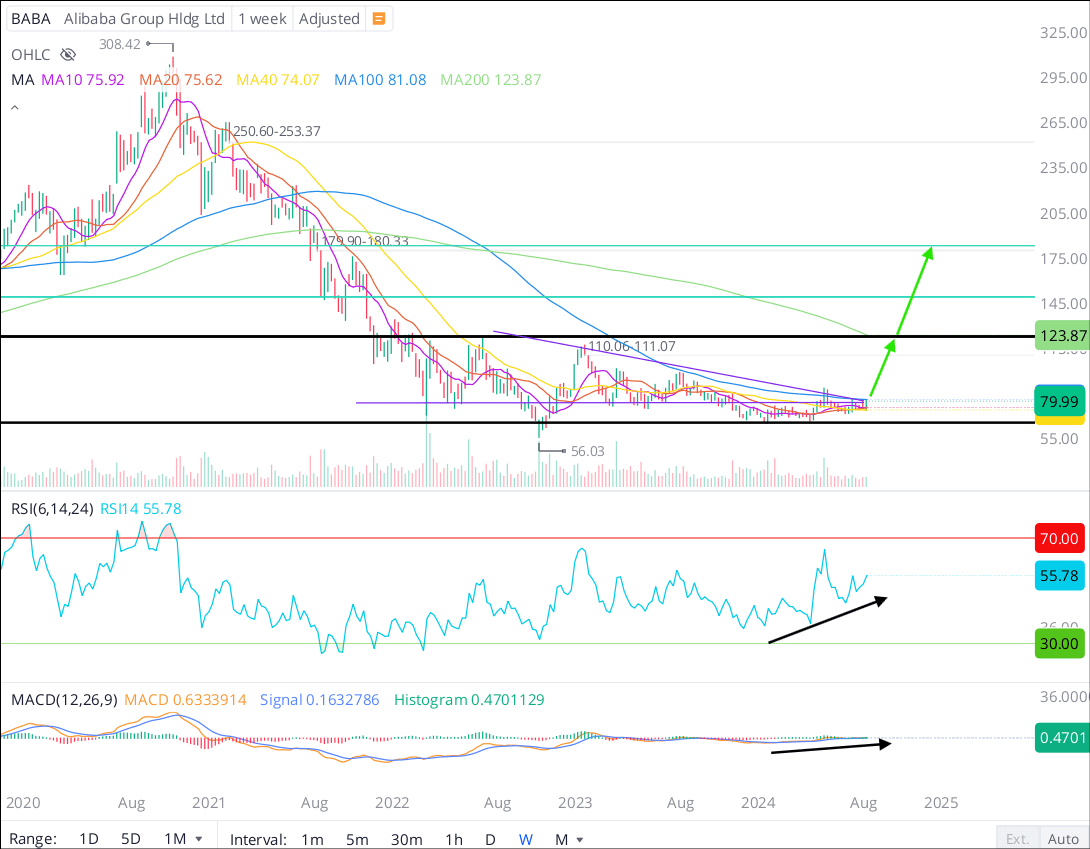

Back in August, I called for a rally in Alibaba Group Holding Limited (NYSE:BABA) stock to $120 per share based on improving business performance, cheap valuation, shareholder-friendly capital allocation policy, and technicals:

Technically, BABA stock remains stuck in a “Stage-I” accumulation base. However, with Alibaba successfully holding the lower end of this base, I think a breakout above the descending wedge (marked in purple) and the 100-week moving average at ~$82 could trigger a sharp upside rally towards the upper end of Alibaba’s Stage-I base at ~$120. The idea of such a rally is supported by rising RSI and MACD indicators.

Alibaba Stock Chart 08/21/2024 (WeBull Desktop)

While Alibaba broke out above the 100-week MA last Friday, the rally has fizzled out, and BABA stock is currently trading at ~$80 per share. As I see it, BABA holding this confluence of weekly moving averages and re-claiming the 100-week MA at ~$82 in upcoming sessions would be quite bullish. An upside breakout could see BABA move to $120 in a jiffy.

Predicting where a stock will trade in the near term is impossible; however, given its resilient business performance in the face of a challenging operating environment in China, Alibaba Group Holding Limited remains a no-brainer buy for long-term investors at a depressed valuation of ~9x P/FCF and ~6x EV/FCF. A recovery in business growth and the continuation of a shareholder-friendly capital allocation policy are set to power Alibaba’s redemption arc over the next 12-24 months.

Key Takeaway: I continue to rate Alibaba a “Strong Buy” in the $80s.

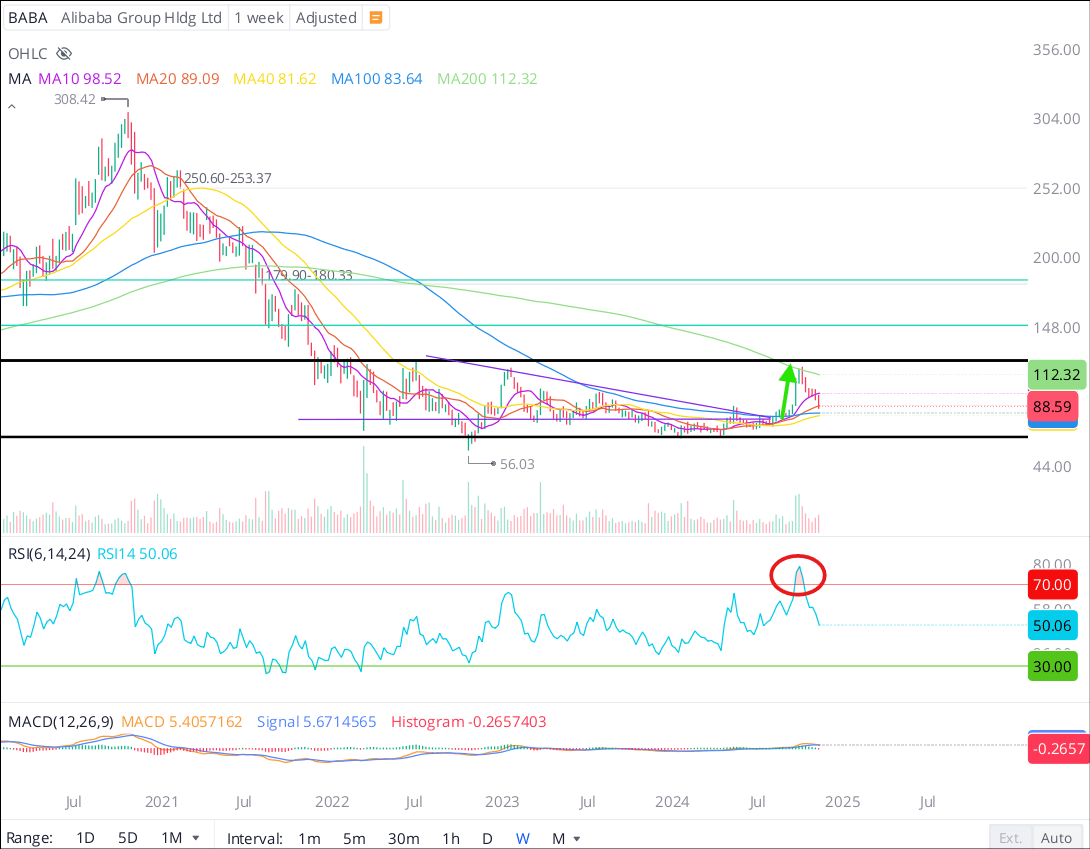

Now, with China unveiling a flurry of monetary and fiscal stimulus, Chinese equities came to life in late September. For its part, Alibaba soared to the upper end of its Stage-I accumulation base at $120 in a vertical run-up:

Alibaba Stock Chart 11/15/2024 (WeBull Desktop)

However, the stimulus-based frenzy in the Chinese stock market proved to be ephemeral. Alibaba stock reversed almost all of its gains in recent sessions — retreating to BABA’s technical breakout level, i.e., the 100-week moving average, which now stands at ~$84 per share.

In today’s note, we shall check up on Alibaba’s business by assessing its Q2 FY2025 report. Furthermore, we will re-evaluate BABA’s long-term risk/reward to reach an informed investment decision.

Analyzing Alibaba’s Q2 FY2025 Report

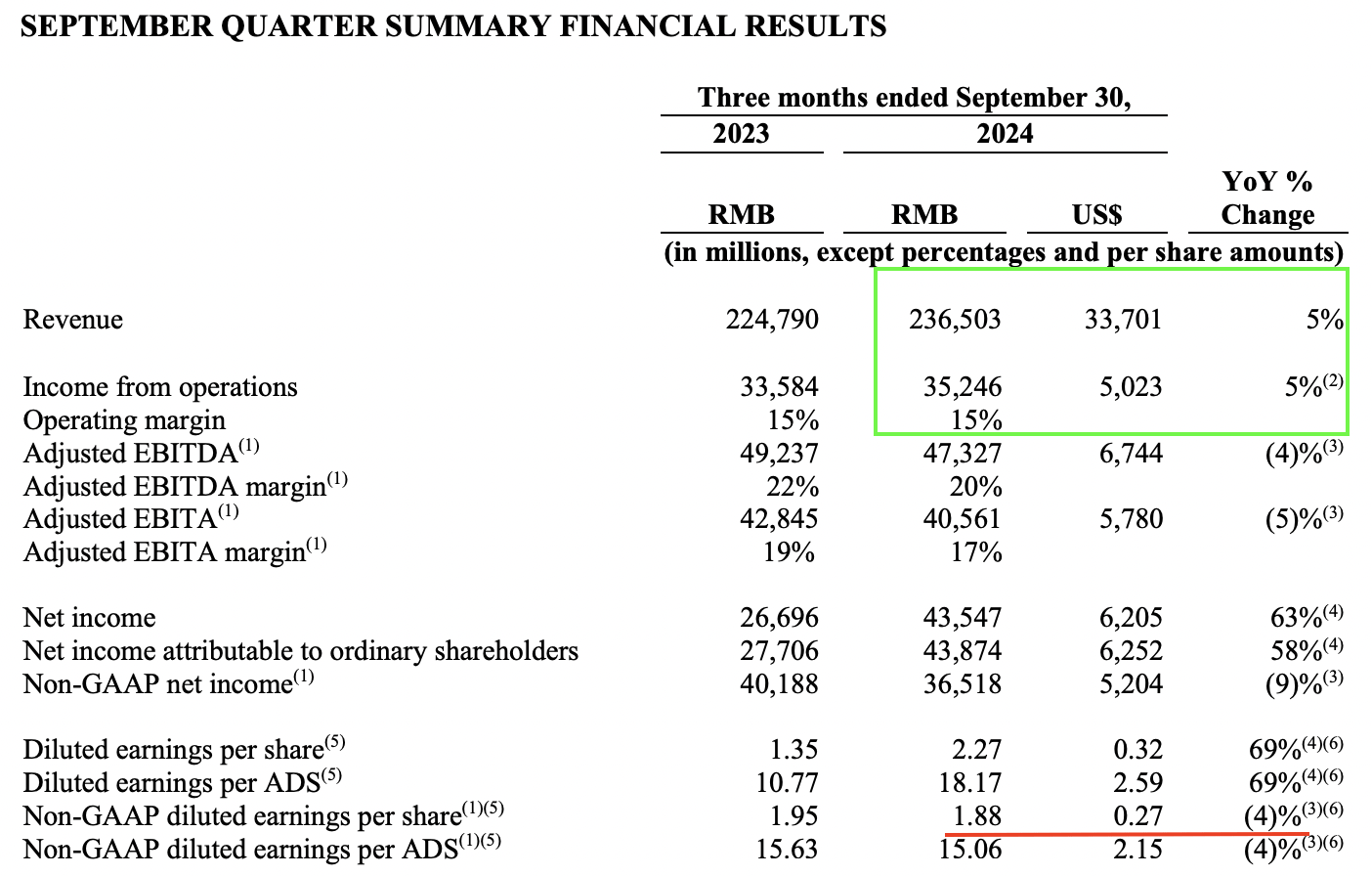

For Q2 FY2025, Alibaba reported revenues of $33.7B (+5% y/y), marking an acceleration in top-line growth and beating consensus estimates of $33.2B. While Alibaba’s operating income rose in line with revenues, normalized earnings fell -4% y/y as the Chinese tech giant’s aggressive stock buybacks failed to offset increased investments across TTG, Cloud, and AIDC segments.

Alibaba Investor Relations

Alibaba Investor Relations

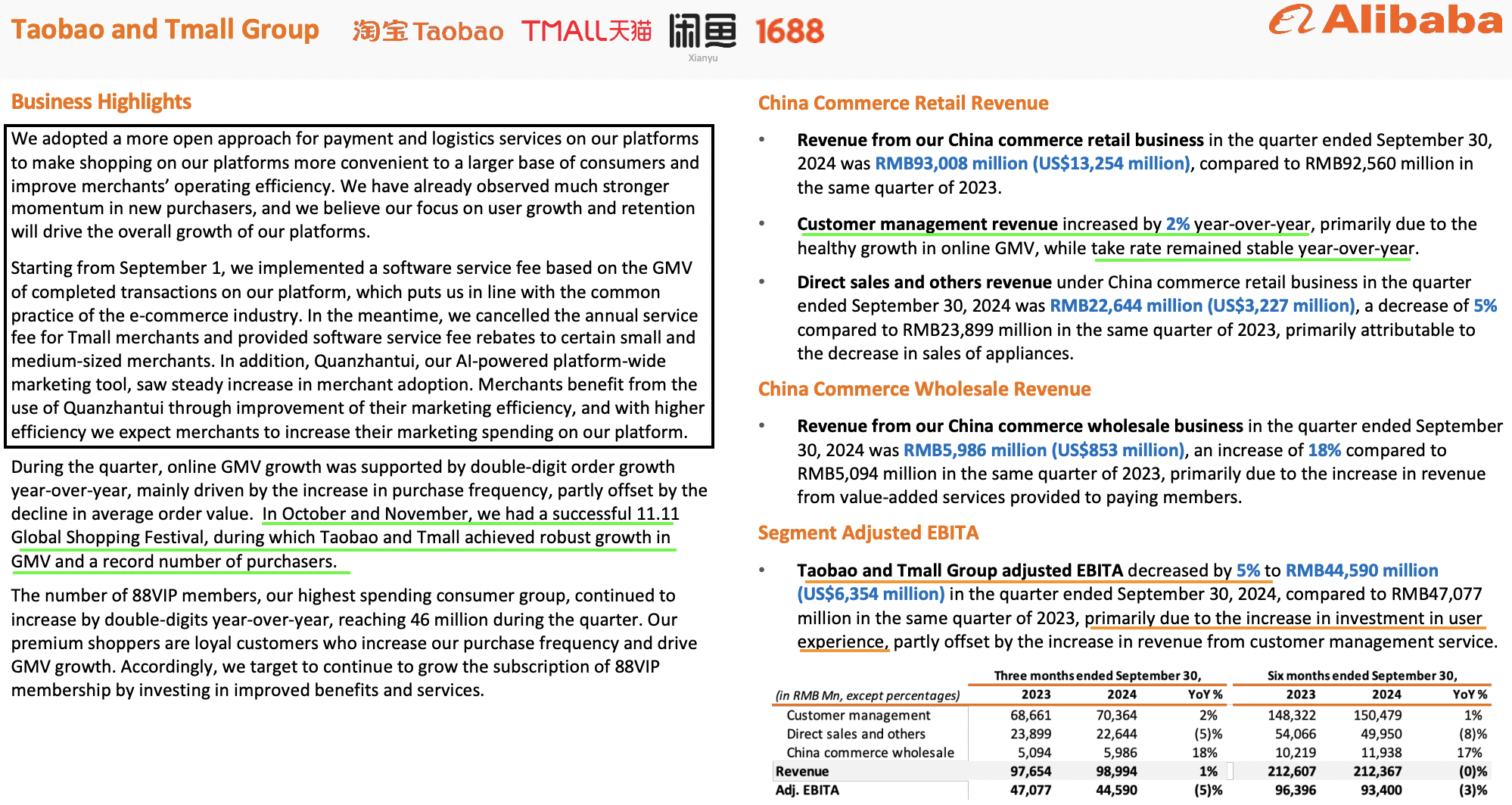

Within Alibaba’s core Taobao & Tmall Group [TTG] business, positive growth in customer management revenue fully offset the ongoing contraction in direct sales revenue — with BABA’s management providing a positive outlook for GMV growth and marketing spend on their platforms:

Alibaba Investor Relations

As per Alibaba’s CFO during the call, Toby Xu, recent strategic investments into TTG are starting to pay off in the form of improved monetization (emphasis added):

Our revenue growth this quarter was driven by improving monetization of Taobao and Tmall Group, which included GMV-based service fees and merchant adoption of our marketing tool Quanzhantui. Consistent with our strategy, we continue to invest in our core businesses while enhancing operational efficiency.

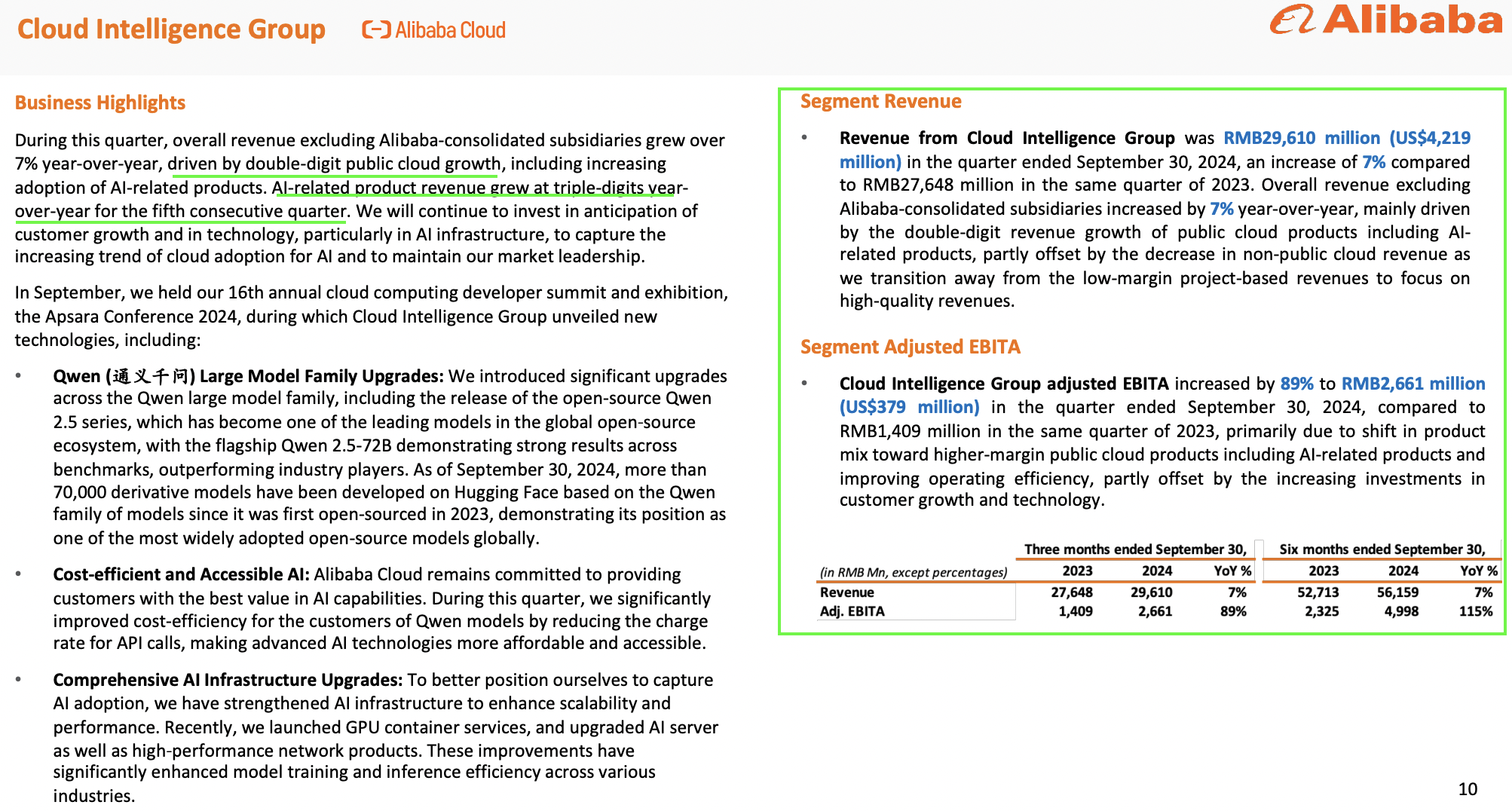

Furthermore, Alibaba’s CEO, Eddie Wu expressed optimism about further acceleration in TTG growth, whilst also waxing lyrical about improving momentum in Alibaba’s Cloud business (emphasis added):

This quarter we continued to invest in the user experience and strengthen product offerings to serve our consumers. We entered into long-term collaborations with industry peers to broaden payment and logistics services on Taobao and Tmall platforms, which we expect will accelerate our overall growth. Growth in our Cloud business accelerated from prior quarters, with revenues from public cloud products growing in double digits and AI-related product revenue delivering triple-digit growth. We are more confident in our core businesses than ever and will continue to invest in supporting long-term growth. Our other businesses continued to improve their operating efficiency, with most of them continuing to increase their profitability or reduce losses.

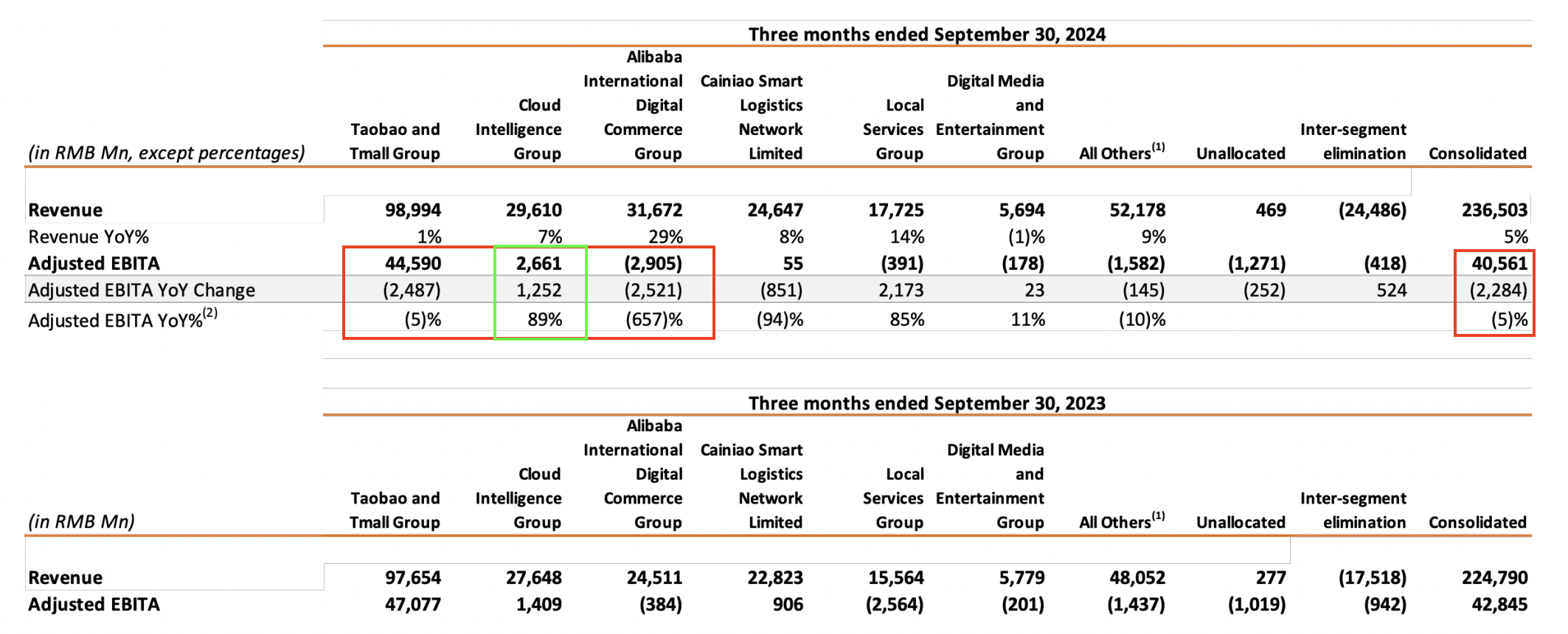

Turning to Alibaba Cloud, rapid adoption of AI and the strategic pivot away from low-margin project-based contracts are driven sales and earnings momentum. In Q2, Cloud Intelligence Group revenues accelerated to +7% y/y, with AI-related product revenues up triple digits y/y for the fifth consecutive quarter. Furthermore, Cloud EBITA jumped +89% y/y to $379M, which is further proof that CIG is an emerging cash cow within Alibaba’s empire.

Alibaba Investor Relations

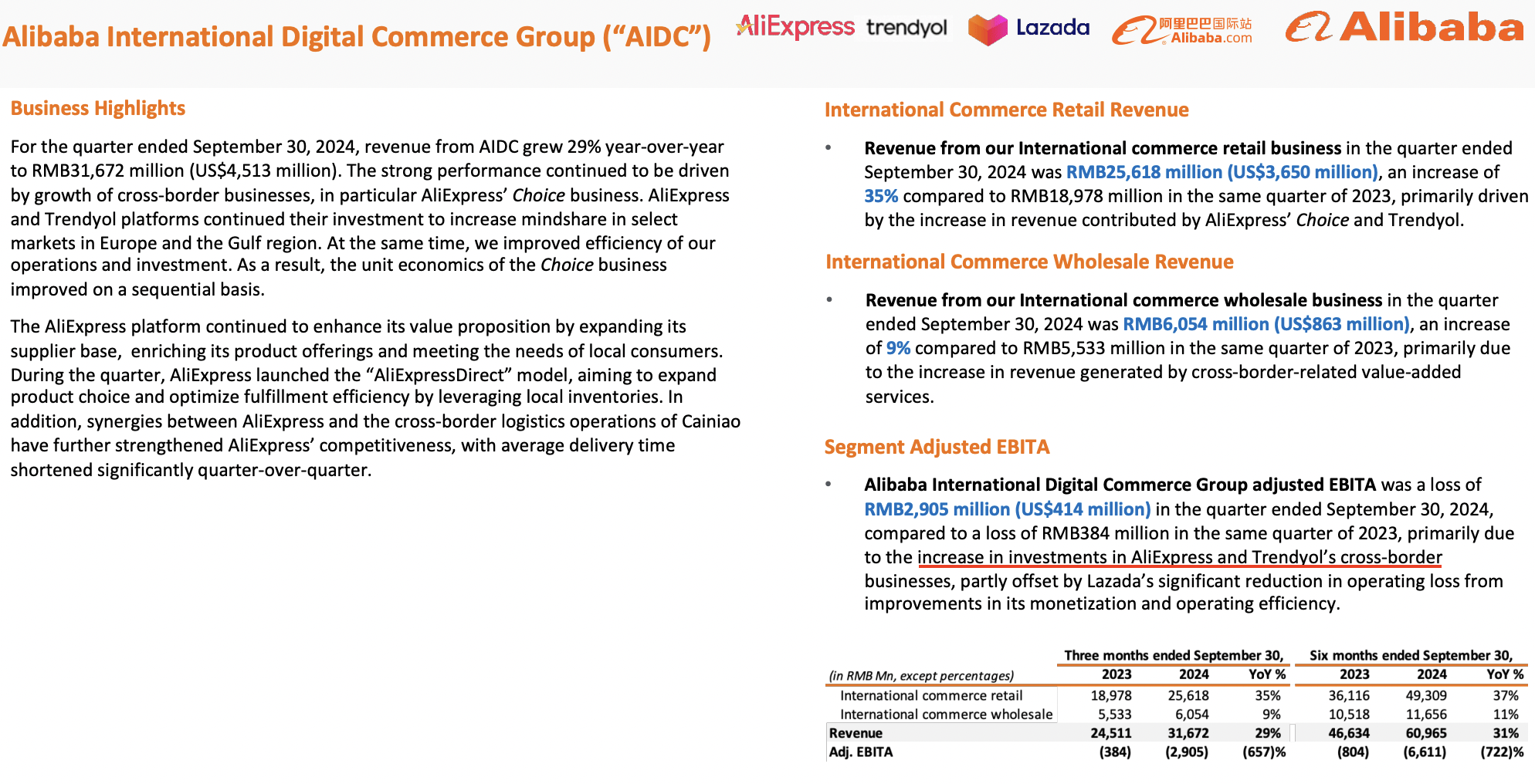

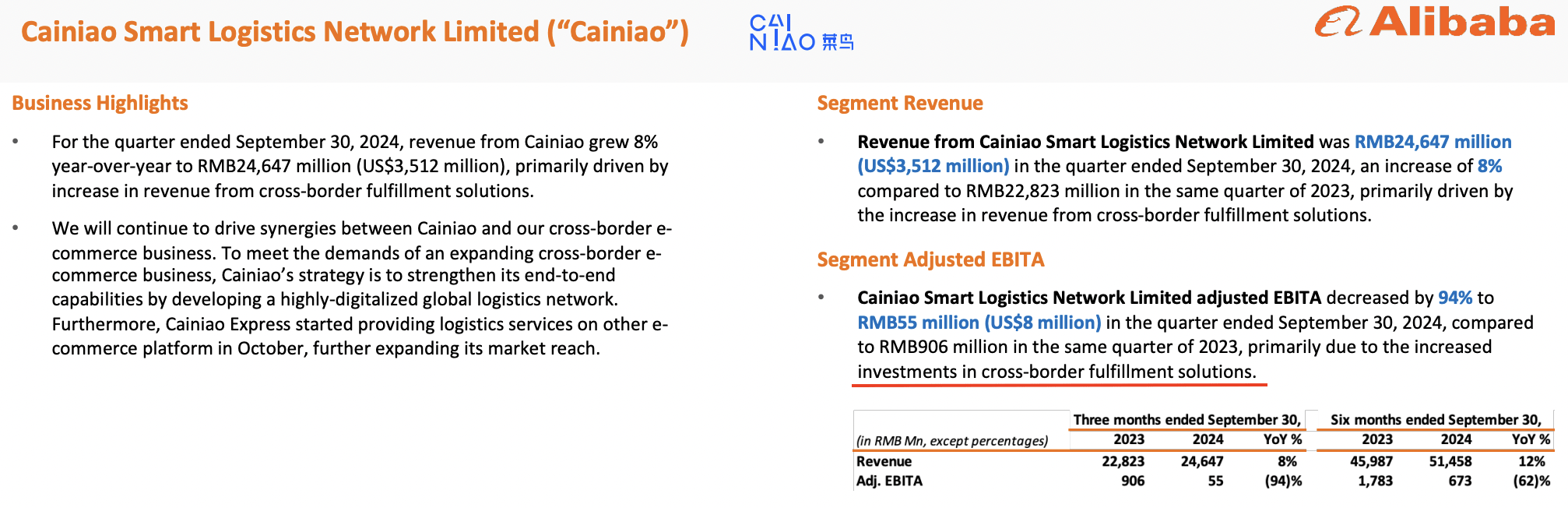

Beyond the core, Alibaba’s AIDC Group and Cainiao [logistics] businesses are still exhibiting solid top-line momentum; however, increased investments in cross-border commerce platforms [AliExpress and Trendyol in particular] and fulfilment solutions are hurting the bottom-line performance of both AIDC Group and Cainiao:

Alibaba Investor Relations

Alibaba Investor Relations

Given the weak consumption environment in China, Alibaba’s growth push in international markets such as Europe and the Gulf region makes complete sense to me, and as such, I continue to view the diversification beyond China as a big positive.

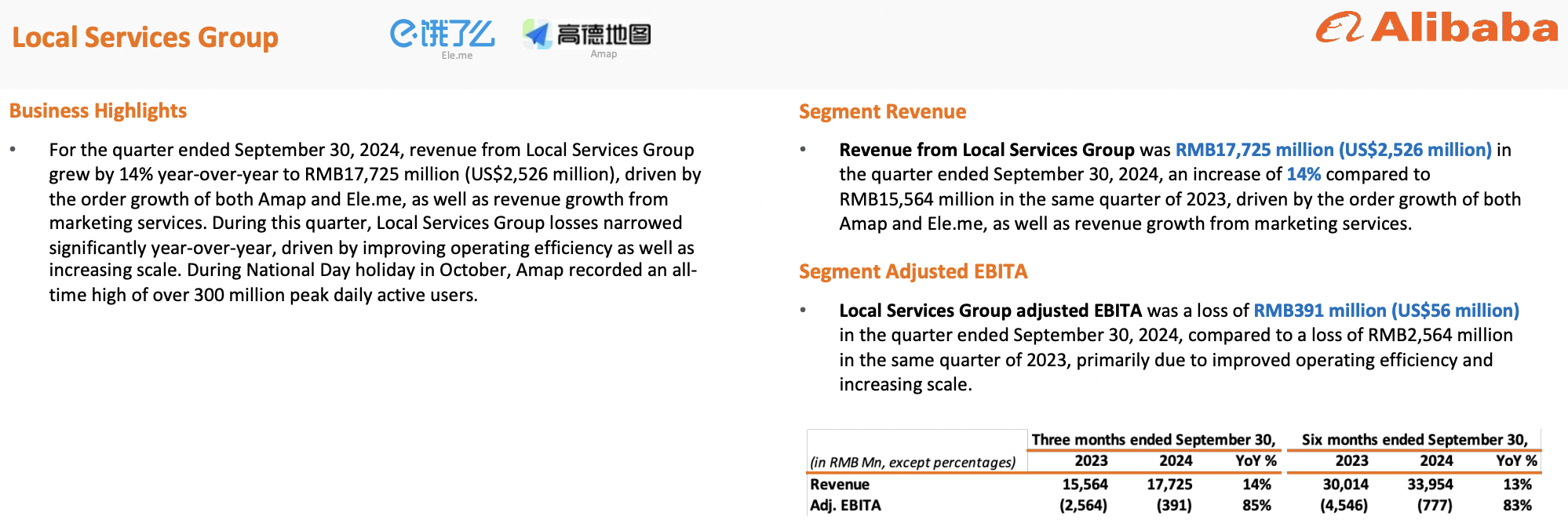

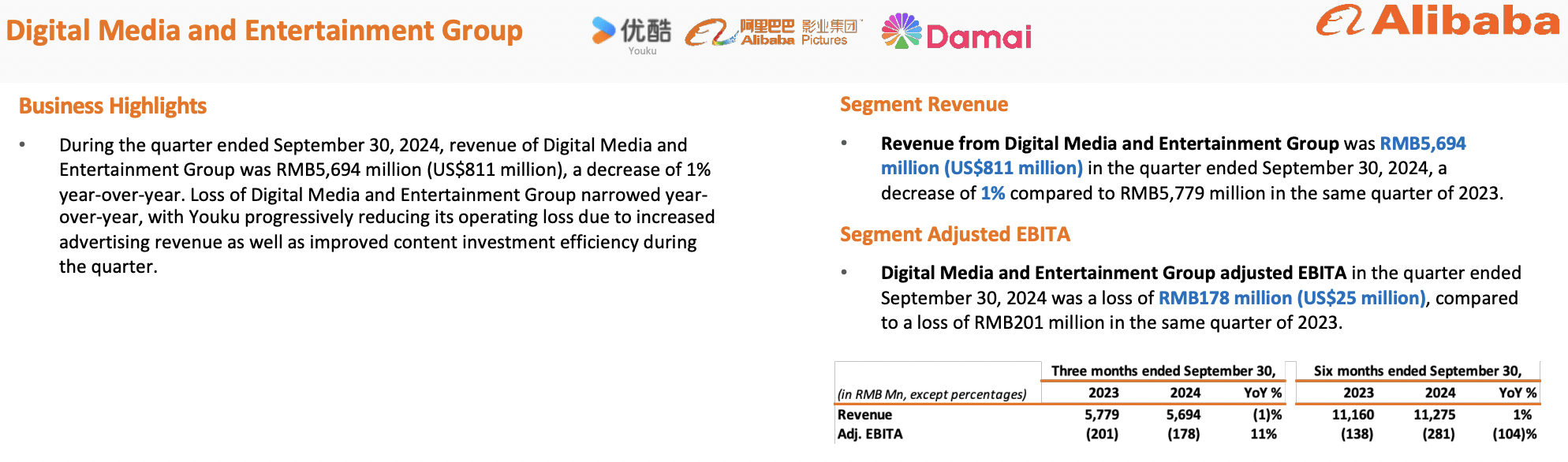

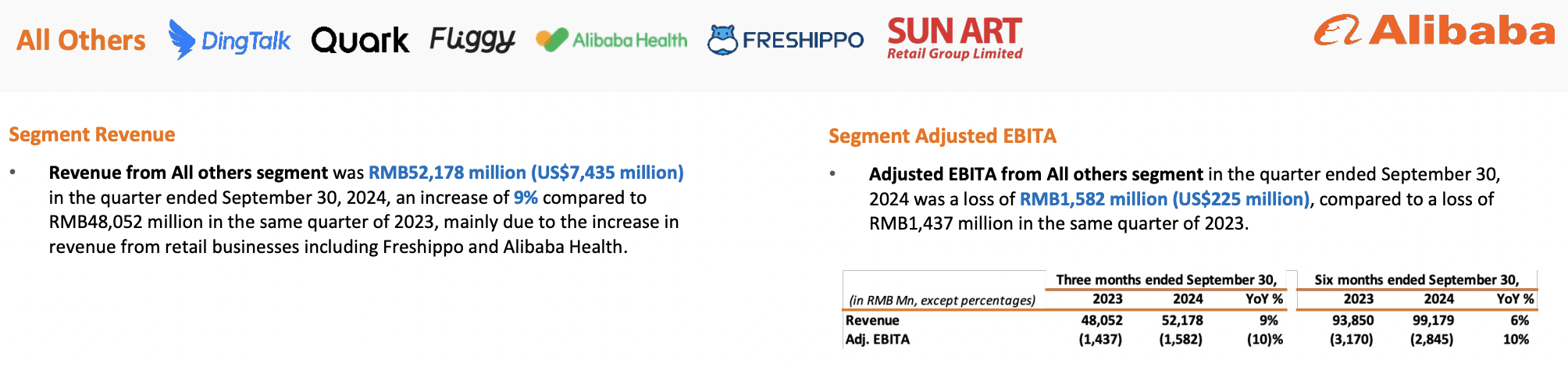

Last, but not the least, Alibaba’s Local Services, Digital Media & Entertainment, and All Other [Ding Talk, Quark, Fliggy, Alibaba Health, Freshippo, Sun Art] segments are recording positive y/y top-line growth and reducing losses through operational efficiencies in most of these non-core businesses.

Alibaba Investor Relations

Alibaba Investor Relations

Alibaba Investor Relations

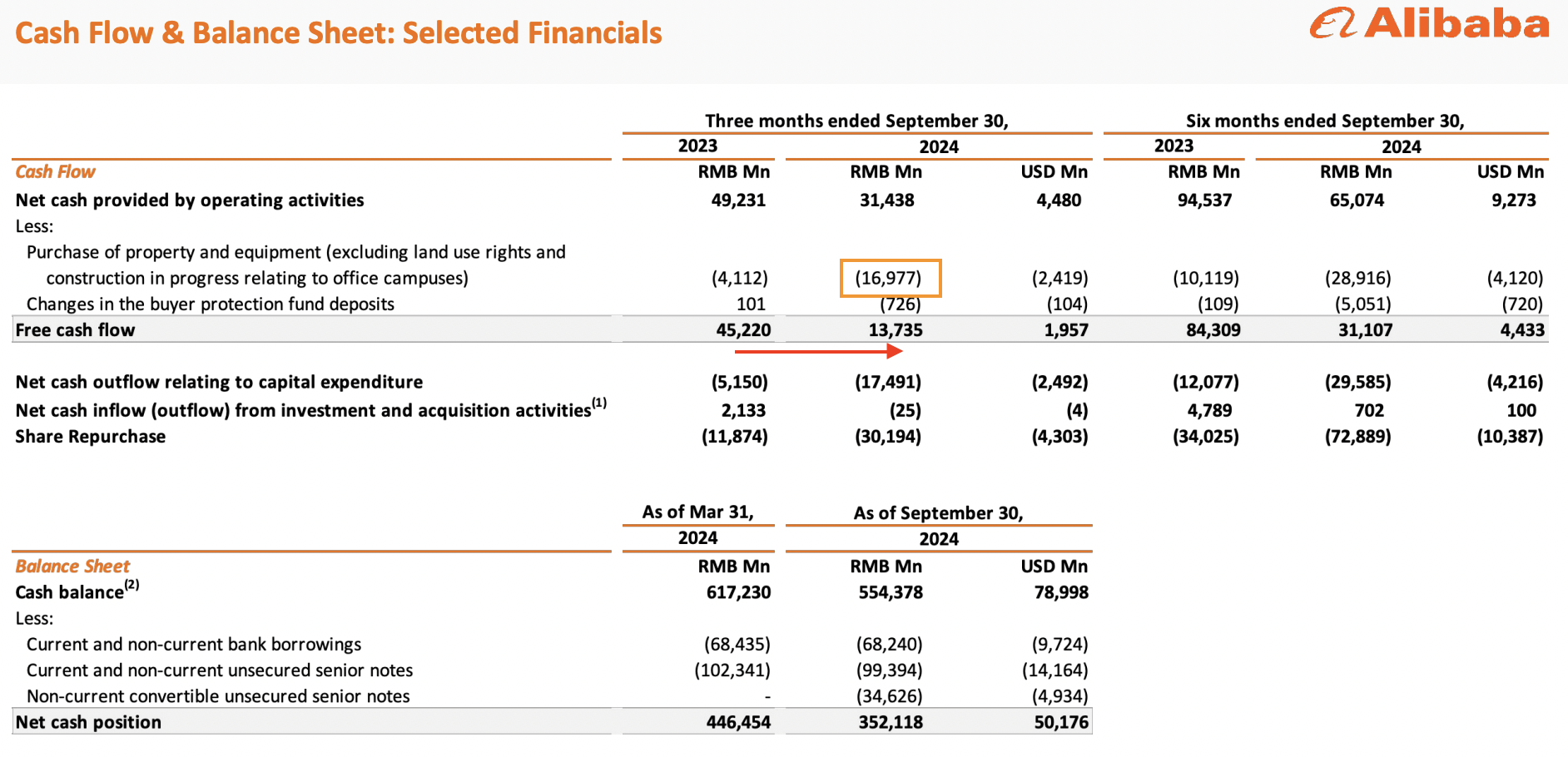

Now, with management increasing investments across Alibaba’s core businesses in the hunt for long-term top-line growth, Alibaba’s free cash flow generation has been wobbly in recent quarters, and this trend continued in Q2 FY2025 as quarterly FCF shrunk to $1.96B [-70% y/y, and down from $2.4B in Q1 FY2025].

Alibaba Investor Relations

As an Alibaba shareholder, I find the continuing cash flow wobbles to be disappointing; however, I have gone through multiple investment cycles with the likes of Amazon (AMZN), and view these spending sprees as necessary short-term pain for long-term gain.

Based on management’s commentary, Alibaba’s cloud infrastructure spending is likely to continue at breakneck pace in upcoming quarters as the company invests in AI infrastructure anticipating demand:

Free cash flow this quarter was RMB13.7 billion, a decrease of 70% compared to RMB45.2 billion in the same quarter last year. This was mainly attributed to our investments in Alibaba cloud infrastructure.

In addition, there is a refund to Tmall merchants after we cancelled the annual service fee and some other working capital changes related to factors, including the scale-down of certain direct sales businesses. Given the sustained and strong demand for AI, we will continue to invest in AI infrastructure as we anticipate future demand for AI-driven cloud services.

– Alibaba Q2 FY2025 Earnings Transcript.

In my view, the triple digit y/y growth in AI-related product revenues within Alibaba Cloud Intelligence group warrant the ongoing CAPEX spending. Furthermore, Alibaba’s TTG investments are paying off in the form of GMV and order growth. Based on underlying data trends, I expect TTG revenue growth to accelerate to mid-to-high single digits — bridging the gap to GMV growth!

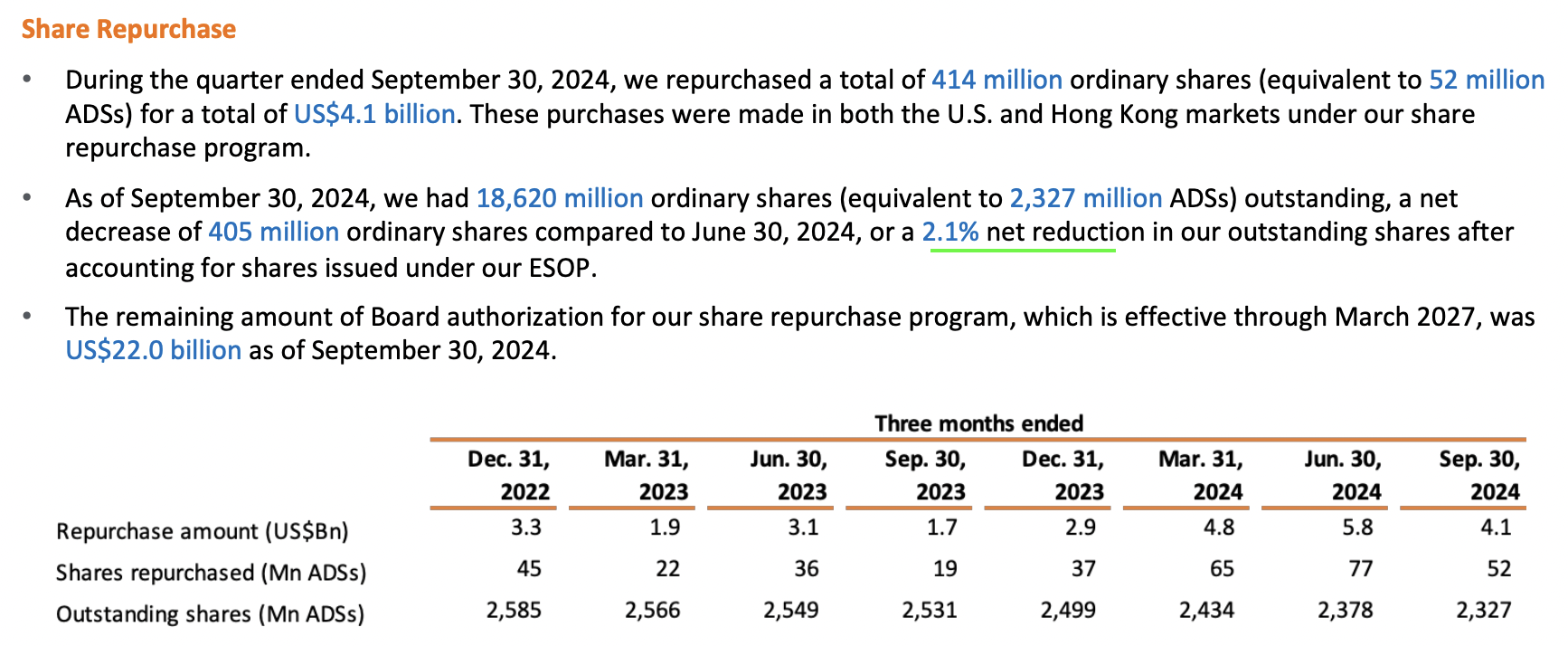

In Q2 FY2025, Alibaba returned $4.1B to shareholders via stock buybacks — reducing outstanding share count by -2.1% from June 2024:

Alibaba Investor Relations

While Alibaba returned more cash to shareholders than it generated in Q2 FY2025, Alibaba continues to boast a robust financial foundation to support its aggressive investment cycle and shareholder-friendly capital return policies, with a net cash balance of $50B+.

In my view, Alibaba building a digital advertising business on top of its e-commerce platform [akin to Amazon] promises to be a fantastic long-term revenue and profit growth opportunity. And, with monetization expected to improve in the back half of FY2025, Alibaba’s management remains confident about its future cash flow generation prospects. Hence, if BABA stock valuation remains depressed, I would expect Alibaba’s management to keep executing on stock buybacks, given that the buyback program still has ~$22B in authorized capital. As such, I see a bulk of Alibaba’s proposed $5B debt raise going towards aggressive stock buybacks in H2-FY2025.

In the past, we have discussed management’s shareholder-friendly approach at length. Given Alibaba’s recent buybacks and dividends, I am happy with its shareholder return program, especially because Alibaba’s management is executing these aggressive buybacks at a dirt-cheap valuation.

Alibaba Fair Value And Expected Return

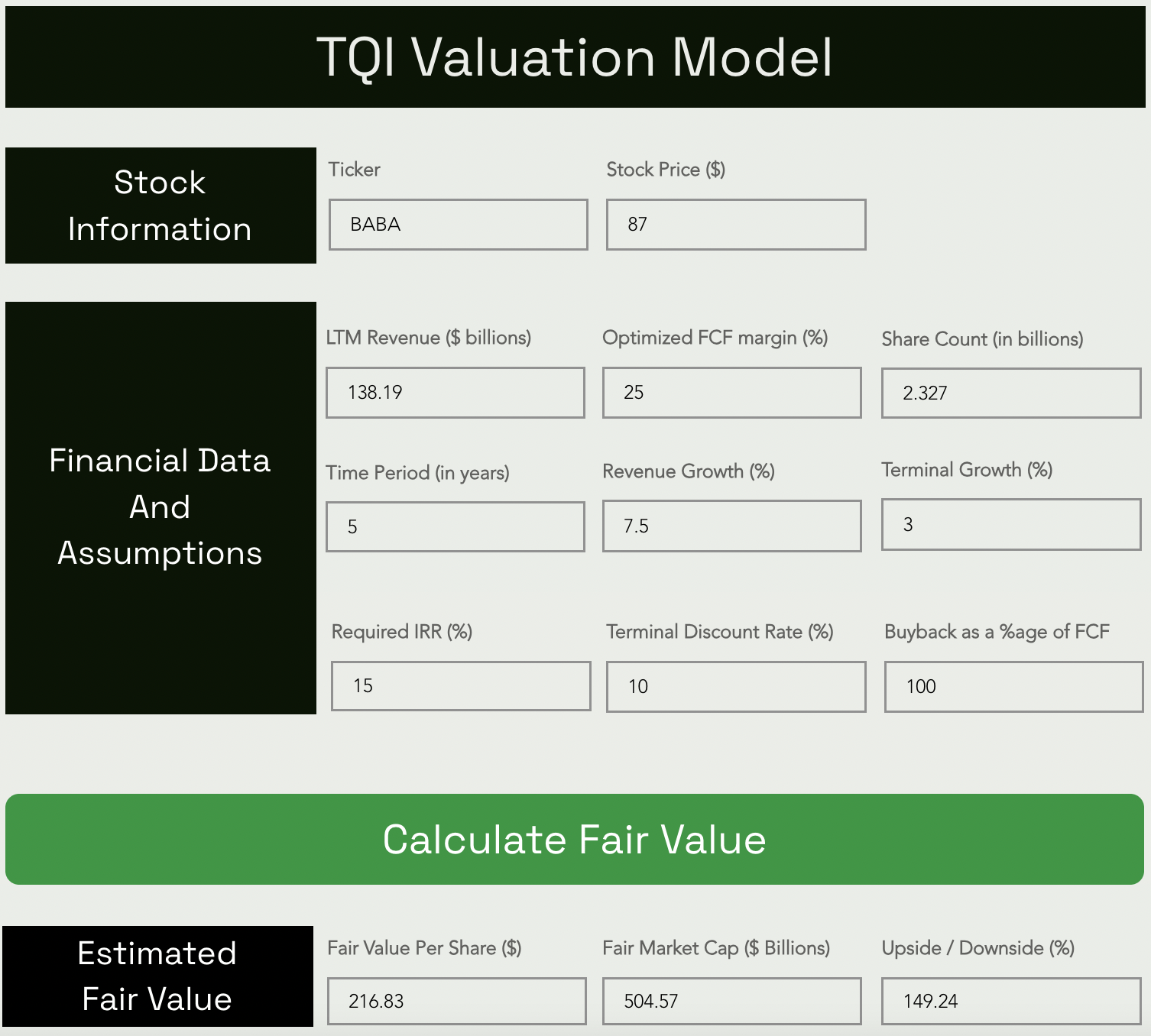

Based on reasonable assumptions for future sales growth and optimized FCF margins, TQI’s fair value estimate for BABA stock has increased from ~$200 per share to ~$217 per share. Given Alibaba is trading in the high ~$80s, I see a +150% upside to fair value for BABA stock.

TQI Valuation Model (Free to use at TQIG.org)

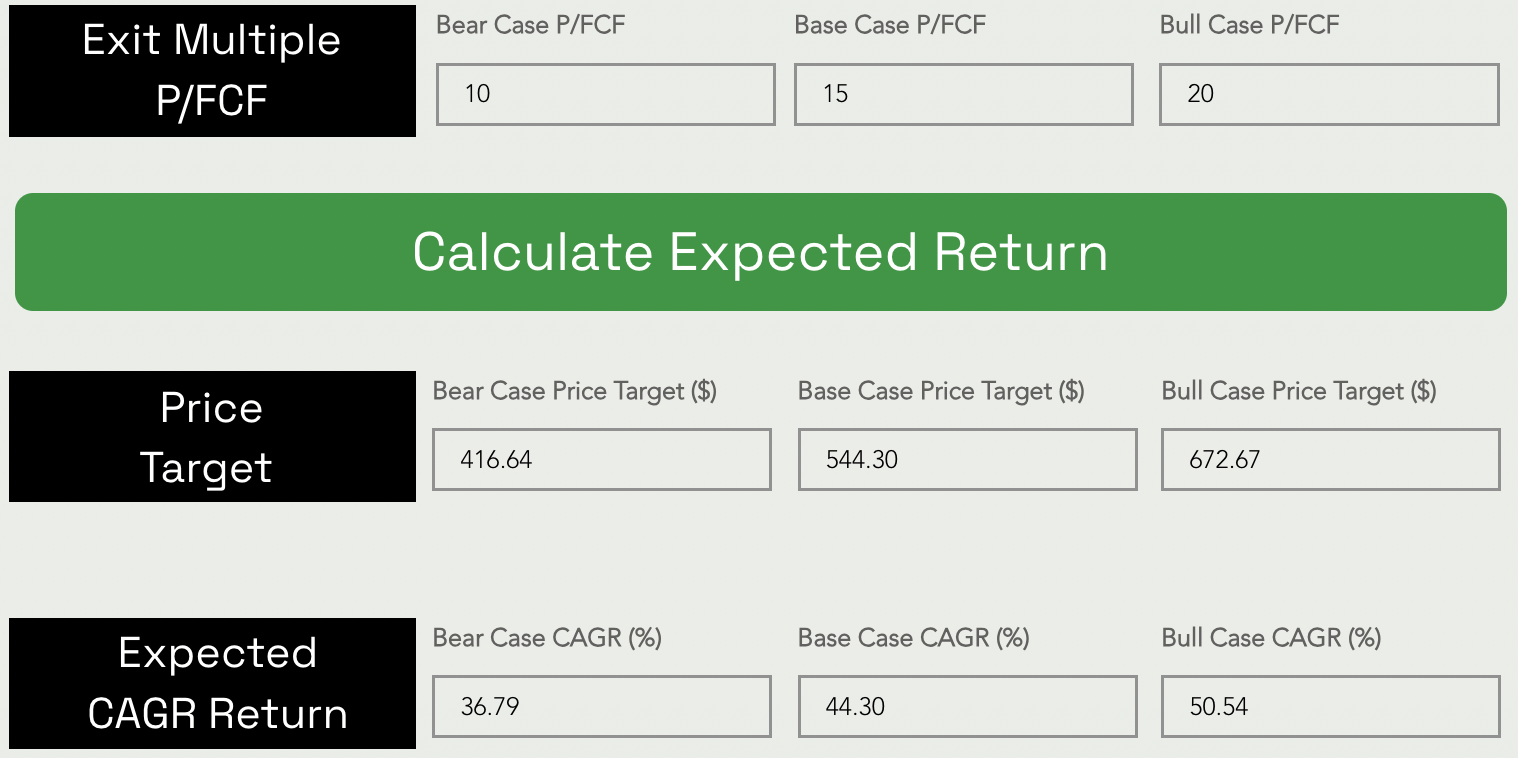

Assuming a conservative exit multiple of ~15x P/FCF (a “China” discount is embedded into this assumption), I think Alibaba’s stock could be trading at ~$503 per share five years from now. This price target implies a 5-year CAGR return of ~44.4%, and handily exceeds our investment hurdle rate of 15%.

TQI Valuation Model (Free to use at TQIG.org)

Considering the asymmetric risk/reward on offer (44%+ CAGR return for the next five years), I continue to view Alibaba as an incredible investment opportunity!

Concluding Thoughts

Although Alibaba is currently undergoing a period of heavy investment, underlying business performance is improving. While geopolitical factors, regulatory pressures, and economic conditions in China have significantly dampened investor and consumer sentiment, I believe the market is handsomely rewarding long-term investors willing to allocate capital to Alibaba stock, with BABA’s 5-year expected CAGR sitting at approximately 44%.

Key Takeaway: I continue to rate Alibaba Group Holding Limited stock a “Strong Buy” in the $80s.

Thanks for reading, and happy investing! Please share your thoughts, questions, and/or concerns in the comments section below.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Analyst’s Disclosure:I/we have a beneficial long position in the shares of BABA either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.

Want More Asymmetric Investment Ideas?

To help supercharge our members’ journey to financial freedom, we publish TQI’s Asymmetric Ideas Series within our investing group – “The Quantamental Investor“. Since launch in April 2023, TQI’s Asymmetric Ideas Series has grown to 18 Picks, with the average return for these ideas standing at +62%.

While past performance is no guarantee of future returns, nailing three 3-bagger [200%+ return] stocks in 18 months is a solid validation of our proprietary investing methodology. If you’d like for TQI’s Asymmetric Ideas Series to be delivered right to your inbox every month, join TQI Basic or Full Access now.