Summary:

- Quantum computing is still pre-mature and cannot live up to its hype, with unresolved errors and challenges in scalability.

- IonQ acknowledges the weaknesses of quantum computing, particularly in error mitigation, indicating a lack of commercialization.

- IONQ’s financial performance reveals net losses and a caution to investors, with a target price suggesting over 20% downside, making it a sell.

Just_Super/E+ via Getty Images

Introduction

Quantum computing is ideal for high-level tasks such as running simulations and data analysis. Quantum computing has attracted interest because of its rapid evolution of complex problem solutions. However, the technology has sparked mixed reactions to investors wondering whether quantum computing is as lucrative as its hype with its unsolved errors. IonQ (NYSE:IONQ), a leading developer of trapped ion quantum computers, has entered the dawn of the quantum age. IonQ develops quantum computers charged with ions as qubits that lasers manipulate to solve complex problems.

For a disruptive technology like this, an investor has to determine that whether the company is effectively developing the technology with maturity, and if the commercialization and profitability is in sight. Based on our analysis, IONQ’s development on both aspects are a “no”. Therefore, it is a sell to us.

Quantum computing is still pre-mature and cannot live up to its hype

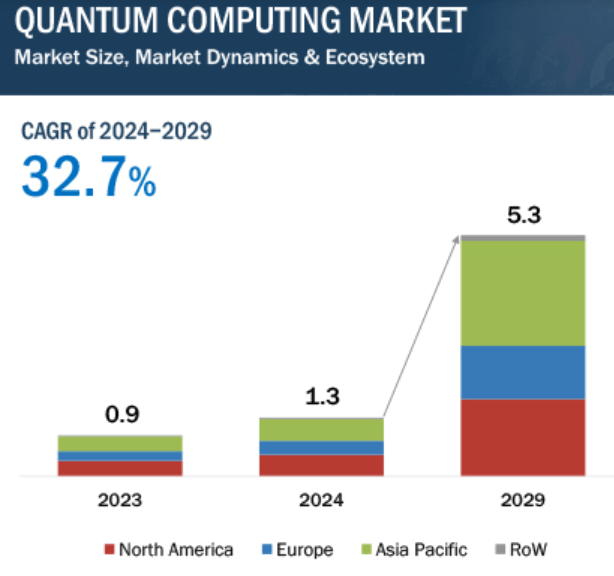

In my opinion, the forecasted growth of the quantum computing market from 1.4 billion in 2024 to 5.3 billion by 2029 is exaggeratedly optimistic because of the technical and commercial hurdles that it has not overcome.

Quantum Computing Market

According to McKinsey, quantum technology could create value to trillions of dollars in the next 10 years. Still, it is not certain when the underlying challenges are yet to be solved. There are several reasons why 32.7% growth is an overhype:

Unresolved errors of quantum computing

The companies in the quantum computing business are still figuring out how to solve the pressing challenge of quantum errors. As engineers promise impressive performance, quantum computers are still in the research and development stage. You can now relate when Meta’s head of AI research, Mr. Yann LeCun, states that there is a possibility that quantum computers’ usefulness is fabricated.

Currently, there is tremendous hype in the industry, making it difficult to filter an opportunity from unrealistic projections. With this hype, quantum computers are still prone to errors, sending caution to technology investors.

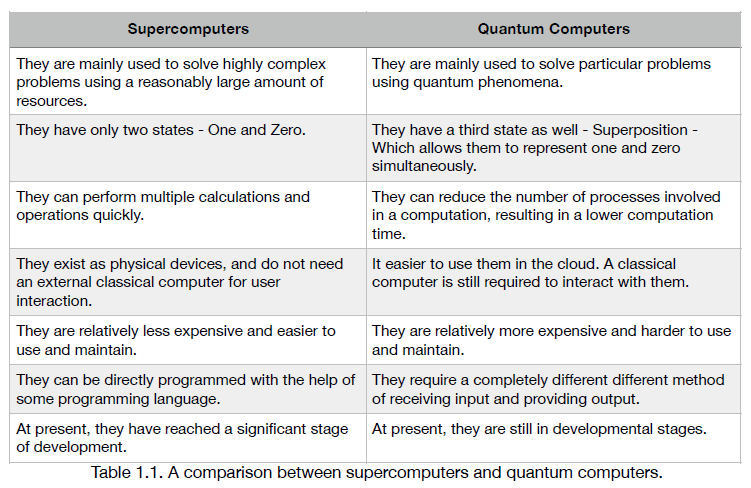

Still not better than supercomputers

Here are the differences on why supercomputers are currently much better than quantum computers, hence the hype.

-

Supercomputers are better at calculating exact and deterministic solutions than quantum computers.

-

Supercomputers can transact more operations in seconds, while quantum computers are slower, with the unrealistic hype.

-

Supercomputers are more versatile and solve multiple problems simultaneously, while quantum computers are applied for challenges that supercomputers fail to solve.

-

The scalability of supercomputers is limited by budget constraints, while quantum computers’ scalability is still under research, leading to a concern on ‘why the hype?’.

The Data Analytics Report

For example, IonQ’s main challenge is scaling up its quantum computers. As a result, quantum computing lags in competitive advantage over supercomputers. As a technology investor, you should be concerned about why the hype is more than a response to challenges on existing quantum computers. The hype promises more research to accelerate computing speed, but the quantum computing innovation is still under primary research.

IonQ acknowledges the weaknesses of quantum computer

IonQ news details in the recent announcement acknowledged their commitment to continuous quantum computer research. In the announcement, researchers are aware of the fact that quantum computers’ cutting edge is in the correction of errors. The closest IonQ researchers have come up with in error mitigation is a noise reduction innovation called Clifford gates.

The Clifford Noise Reduction (CLINR) uses 3.1 qubit overhead, which is an improvement compared to other quantum applications that require hundreds and even thousands of qubits to correct an error.

You can now relate to how IonQ recognizes that quantum computing has not yet achieved error mitigation, contrary to the hype. It is evident that the forecasted results are unrealistic.

John Preskill states that quantum computers are under the noisy intermediate-scale quantum (NISQ). It means they are still in development, pending perfection for meaningful usefulness. Recall that since error correction is still an underlying challenge until error-correction codes are developed, quantum computers will not yield as forecasted.

Quantum advantages are not yet satisfactory, but the developments make quantum computing lucrative. However, the hype loses meaning considering the existing technical questions concerning the hardware. For example, there is still a technical need for more qubits for better hardware control.

IonQ President and CEO Peter Chapman states that achieving an error correction code innovation will be an edge in quantum computing delivery of scale, performance, and solution of most complex problems. As a leader in quantum computing error mitigation, IonQ is in recognition of quantum computer drawbacks. The computer requires many data samples to be implemented, increasing the time to develop a solution.

These underlying fundamental issues make quantum computing more overhyped than it is in reality.

The company is remote from commercialization

IonQ commercialisation is far from near. Scaling and developing quantum computers is the first determining factor in their commercialization. The research stage involves the addition of more qubits for better control of the hardware, which is not easy.

IonQ has attempted to solve the error challenge using its next-generation barium qubits to increase the accuracy of the quantum system when solving complex problems.

IONQ

The IonQ quantum computers are still in the initial research and development stage. The company commercial highlights indicate that IonQ was funded by Congress $40 million under the key achievement of US national security to design first-of-kind quantum computers. Government funding indicates companies struggle to commercialize.

According to Dean Kassmann, SVP of Engineering & Technology at IonQ, the market demand for commercial quantum computing is huge. The company is actively accelerating its quantum computing strategy. For instance, IonQ combines photonic interconnects, multicore parallelism, novel technology, and systems engineering to deliver scalable, high-performance, and enterprise-grade quantum computers.

IonQ has not achieved an impressive commercial advantage, but it is working on an expansion strategy for infrastructure through collaborations with other industry leaders. For example, IonQ has contracted with AWS to offer its commercialized world-class quantum computers under the Amazon Bracket.

Valuation

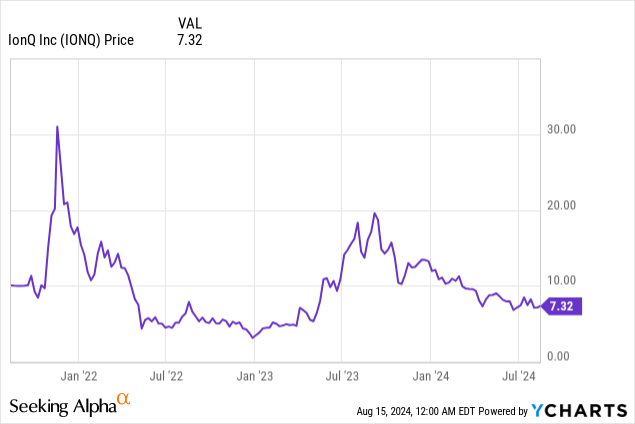

The company has recorded a significant plunge from its peak near the $20 level in 2023. This has proven that investors know that IonQ’s ion traps are slower to react than superconducting circuits, especially after the departure of its founder in Feb 2024. Ion traps also scale badly due to their dimension geometry. These uncertainties have scared away investors, leading to the stock price decline. Research and development in quantum computing will inevitably revolutionize the computer world as we know it, but only until the underlying issues are resolved as discussed. Therefore, shares price-wise, it will be depressed.

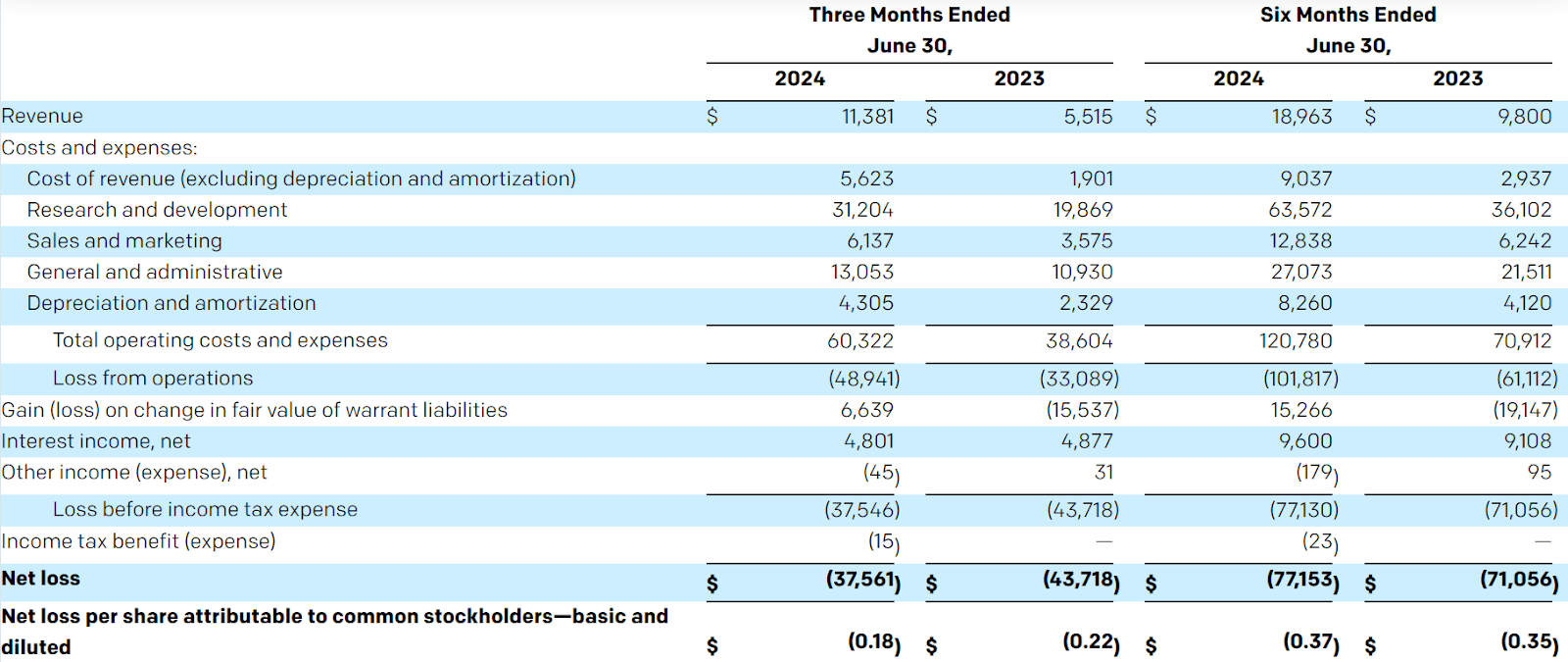

From the recent financial highlights of the second quarter, IonQ’ financial performance reveals the unrealistic hype with the record net losses. The company has recorded net losses since 2023, within the recent Q2 net loss at $37.6 million.

IONQ

With the EBITDA loss of $23.7 million in the second quarter just released, it provided a caution to investors who are ready to invest in the IonQ company. The latest announcement shows that the company’s existing shareholders will lose $0.18 per share. The estimated EPS was -$0.11 versus the actual EPS of -$0.209. Q3 EPS of -$0.12 could be more ranging between -$0.140 and -$0.209, as indicated by the management

The revenues are performing better than expected, with the second quarter recording $11.4 million above the forecasted $7.6 – $9.2 million. This is a 105% growth compared to the previous year’s $5.5 million last year following the recent quantum algorithm upgrade.

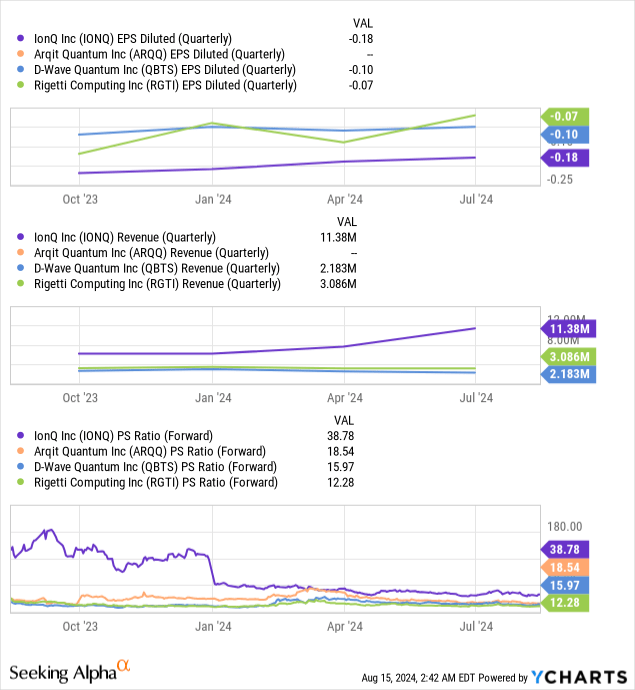

To do an educated assessment of the company’s target price, revenue and Price-to-Sales ratio are going to be the most relevant metrics given the remote profitability expectation. In terms of revenue expectation, the consensus estimate of revenue ranges from $38 – 42 million. On multiple perspective, since IONQ has the highest commercial revenue compared to its peers, and with its closer to commercialization, it has a relatively high P/S ratio. In the short-term, we expect that the valuation multiple will remain suppressed because of interest rate level and the slower-than-expected rate cut, as well as the calling off of AI frenzy as exemplified by the revaluation of Nvidia recently. Therefore, the company could be valued anywhere near the 25 – 30x range.

As such, the target price will be at around $5 – $5.4, which represents an over 20% downside. Therefore, it is a Sell to us.

Investment Risk

-

High Market volatility: IonQ stock price has decreased by 61% in the last 52 weeks. The company has a steady rise in revenues and valuation. This could form a buying point for an investor if the algorithmic IonQ quantum computing technology works. However, currently, it is risky to invest in IonQ shares with the existing uncertainties.

-

Uncertain Profitability: IonQ reported a net loss of $37.6 million in the recent Q2 announcement. The company relies on the sale of assets as the investment portfolio to fund its operations. Operations recorded a loss of $48.941 million in the recent Q2, showing it is indeed a risky strategy.

-

Technology still Infant: Quantum computing is still under research and development. IonQ computer systems are noisy, generate simple results, and are prone to errors. The company is also struggling to commercialize its technology.

Analyst’s Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.