Summary:

- Adobe’s strong financials and efficient operations position it for continued growth, despite recent share sell-offs.

- Fiscal year 2024 Q4 results exceeded expectations, but shares declined due to lowered guidance and concerns about AI investments paying off.

- Adobe’s valuation is attractive, trading below historical averages, and potential returns could be double digits if growth targets are met.

- Technical indicators show bearish momentum and short-term volatility could be expected, but strong fundamentals suggest long-term value.

Richard Drury

Adobe (NASDAQ:ADBE) is the parent company behind many well known products including Photoshop, Illustrator, Acrobat, and many more.

It is one of the largest software companies in the world and caters to creative professionals including photographers, video editors, graphic designers, marketers, and many more.

They operate three major businesses:

-

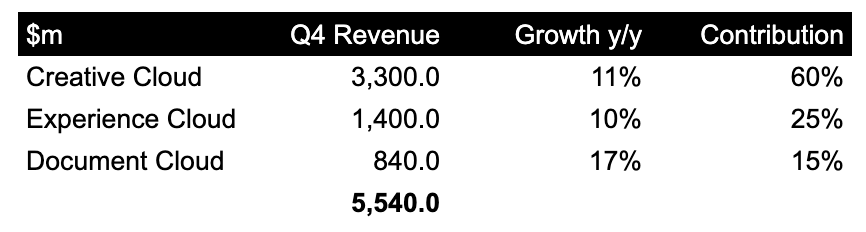

Creative cloud – software-as-a-service model for many of the well known creator applications including Photoshop for photo editing, Illustrator for vector graphics, InDesign for layout design, After Effects for motion graphics, and Premiere Pro for video editing, Express for quick edits, and many more

-

Experience cloud – customer journey tracking, analytics, marketing workflows, content, commerce, and insights to help enterprises understand their customers and optimize the experience

-

Document cloud – Acrobat for creating, editing, and modifying PDFs, as well as e-signature solutions

All three areas are growing double digits year-over-year and very promising.

Adobe revenue by cloud (Adobe & author’s work)

Adobe has established themselves as a leader in AI, pushing forward with Adobe Firefly as the embedded solution for their creative suite of tools and Adobe Sensei for intelligence in documents and their experience platform.

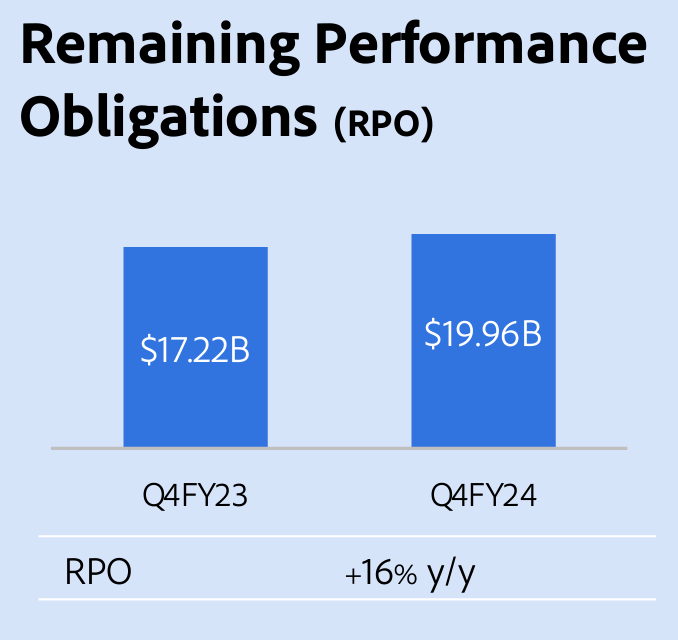

Fiscal year 2024 Q4 results were very solid. Revenue and EBITDA came in ahead of expectations. Remaining performance obligations, a leading indicator of revenue (basically commitments that are not yet booked), grew 16% y/y, outpacing the company’s revenue growth for the quarter.

RPO (Adobe)

While the company beat on revenue and earnings, shares sold off due to lowered guidance.

They continue to focus and execute on their plan – specifically driving AI and customer acquisition.

Adobe has been investing heavily in AI. Given the lowered guidance, investors are concerned about the timing of those investments paying off. Adobe hasn’t been optimizing monetization. On the earnings call, CEO Shantanu Narayen, emphasized their current focus being adoption and high usage.

“The deep integration of Firefly across our flagship applications in Creative Cloud, Document Cloud, and Experience Cloud is driving record customer adoption and usage. Firefly-powered generations across our tools surpassed 16 billion, with every month this past quarter setting a new record”

Adobe is also investing heavily in new customer acquisition on the individual and SMB side of the market. This strategy may have arisen following the failed Figma acquisition. Adobe must stay relevant beyond the enterprise, to avoid a newcomer slowly entering their space.

“Creative Cloud growth drivers included: strong demand for new subscriptions for Creative Cloud All Apps across individuals, Teams, Enterprise and Education; strength in Creative Cloud single apps for Acrobat Pro, Lightroom and Photoshop; momentum with new subscriptions in emerging markets; demand for Adobe Express across education, SMB, and enterprises and adoption of Firefly Services in the enterprise.”

“We reimagined creativity and productivity for a broader set of customers with Adobe Express, the quick and easy create-anything app.”

While monetization is not the current focus, Adobe is performing very well and has a very strong financial profile. Adobe’s financials are solid. The company doesn’t require a lot of capital to operate, it is highly profitable, and very efficient.

They are executing on their stated plan. They’re focusing on embedding AI throughout their suite of solutions. These tools are critical for the professionals that use them every day.

Emerging competitors such as Figma and Canva can pose potential threats. They’ve gained rapid traction amongst consumers and amateurs. They have solid offerings and are no doubt interested in making their way up to larger businesses and enterprises, knowing that those are the bigger accounts.

To build a successful company, however, takes more than a solid product. Although Figma received $1 billion as a breakup fee, the acquisition process was a huge drain and time sink. The illusion of a significant payday was a distraction and has left many of the talented Figma team looking for new experiences. New York Times wrote up a detailed article: After Its $20 Billion Windfall Evaporated, a Start-Up Picks Up the Pieces.

Adobe has a significant advantage with its time-tested ecosystem, that saves professionals significant time via the tight integration across tools. This seamless integration and propagation of changes across applications allows professionals to move between tasks without breaking their workflow.

Diving into the financials:

Financial summary (Adobe)

-

TTM revenue grew 11%, holding relatively steady over the last few years

-

Guidance calls for revenue growth to slow slightly to 10%, yet companies are known for providing conservative outlooks & RPO growth shows the possibility of even acceleration

-

TTM gross margin held steady at 89%. This is very impressive and shows how efficient the company is at the unit level.

-

TTM EBITDA margin came in at 40%, showing a steady uptrend

-

TTM FCF margin jumped up to 37%, as the company works past the $1b breakup fee they paid Figma. Historical margins were 40%+, so more room to improve there.

-

Balance sheet is strong, with a net cash position of $2.2 billion

-

Shares outstanding declined 2.4% y/y. Their share buybacks are more than offsetting stock based compensation.

-

The company is very efficient, with ROIC of 36% FCF ROIC at 38.6%. ROIC gives context on the performance of prior decisions.

-

ROIC ex goodwill is significantly higher at 97%. ROIC ex goodwill gives an indication of ongoing capital requirements. Most of Adobe’s capital outlay has been due to acquisitions. The company’s operations do not require much capital at all.

As for valuation:

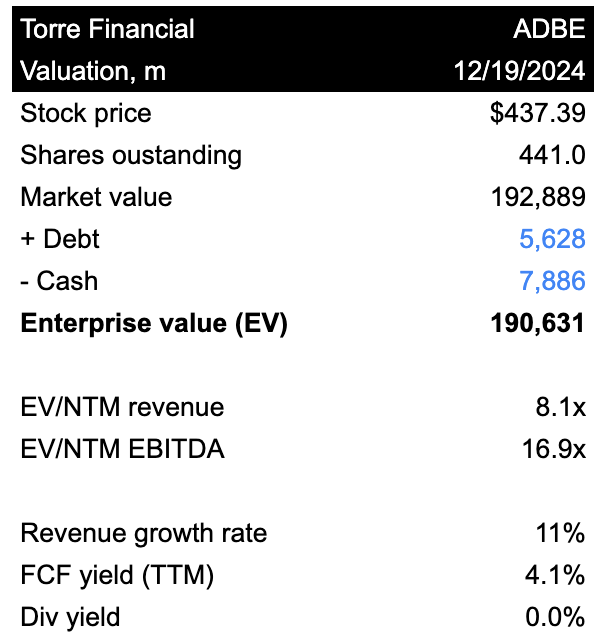

Valuation (Koyfin)

Adobe trades for an EV/NTM EBITDA multiple of 16.9x. This is not very expensive at all for such a profitable and capital efficient company with ongoing growth.

For context, Adobe’s 10 year average multiple is 23.5x with a standard deviation of 5.1x. The current multiple is more than 1 standard deviation cheaper than the historical average.

The FCF yield of 4.1% is very attractive as well, in absolute terms as well as in historical terms compared to the 10 year average of 3.06%.

(Note in the LTM FCF in the chart below has not yet been updated with the latest earnings report.)

Valuation metrics (Koyfin)

Looking at the next few years, revenue is expected to grow ~9-10% and EBITDA is expected to grow ~9%.

Estimates (Koyfin)

The following table shows possible annualized returns over the next 5 years across various scenarios. The model assumes share count declines by 1.5% each year due to continued buybacks.

Sensitivity graph of future returns (Author’s work)

An investment in ADBE can very reasonably yield double digit returns.

-

If EBITDA grows at 8% CAGR and multiple trades at 18x, shares could return 11% per year

-

If EBITDA grows at 10% CAGR and multiple trades at 20x, shares could return 15% per year

-

If EBITDA grows at 10% CAGR and multiple trades at 22x, shares could return 18% per year

FastGraphs provides another look.

FastGraphs (FastGraphs)

Looking a few years out, if shares were to trade at a P/E of 25x, shares could return 13% per year.

If shares were to trade at their historical normal P/E of 38.6x, shares could return 30%+ per year.

Taking a look at the price action:

Technical chart (Koyfin)

After the interest-rate induced sell off in 2022, Adobe shares recovered significantly throughout all of 2023.

The beginning of 2024 brought some volatility, with shares drawing down nearly 30%.

The most recent sell off dropped below the June 2024 low, forming a series of lower highs and lower lows & indicating bearish momentum.

The 50-day simple moving average (SMA) is below the 200-day SMA, which is a bearish signal. The price is also trading below both moving averages, further supporting the downtrend.

The relative strength indicator (RSI), currently below 30, indicates that the stock may be oversold. This could suggest a potential reversal in the near term.

The volume profile shows low activity around the current price levels. If the stock were to bounce back, there would likely be some resistance at ~$470. On the downside risk, the next level of strong support would be ~$380.

All said, the current technical picture doesn’t look too great. Over time, the company’s strong fundamentals are likely to become reflected in the stock price. It may, however, be a choppy ride in the short term.

Analyst’s Disclosure: I/we have a beneficial long position in the shares of ADBE either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.