Summary:

- We start with the overarching matter of “The Metaverse.” What is it?

- Why does it take multiple tens of billions of dollars in R&D and when will those multiple tens of billions of R&D dollars begin to generate revenues?

- Has META stock become just an open-ended bet on founder CEO (and controlling shareholder) Mark Zuckerberg’s avarice to prove his vision of the metaverse?

tolgart

The following segment was excerpted from this fund letter.

“Our hope is that within the next decade, the metaverse will reach a billion people, host hundreds of billions of dollars of digital commerce.”

Mark Zuckerberg, CEO Meta Platforms. October 2021.

With apologies to W.P. Kinsella, Mark Zuckerberg has built it. And they did come. And they have stayed. By the billions. The Metaverse will be the next evolutionary chapter by Meta Platforms.

Speaking of billions. Meta Platforms’ (NASDAQ:META) Family of Apps (FoA: Facebook, Instagram, WhatsApp and Messenger) currently has over 3.7 billion monthly active users – this includes almost 3.0 billion daily active users. If baseball is sports national pastime, Family of Apps is the social national pastime. The International Telecommunications Network (ITU) estimates that of the 8 billion in world population, nearly 3 billion are without an internet connection. If you exclude China’s population of +400 million (where U.S. social media companies are largely banned), Meta Platforms Family of Apps are used monthly by a staggering 90% of the world’s connected population and by 70% on a daily basis. This level of user engagement and density across the Company’s FoAs would seem to be an impenetrable fortress. It surely has been in the continued growth and stickiness in terms of users. In terms of an economic fortress, as in the case back in 2018 (Cambridge Analytica), 2022 brutally challenged that assumption.

Annus Horribilis.

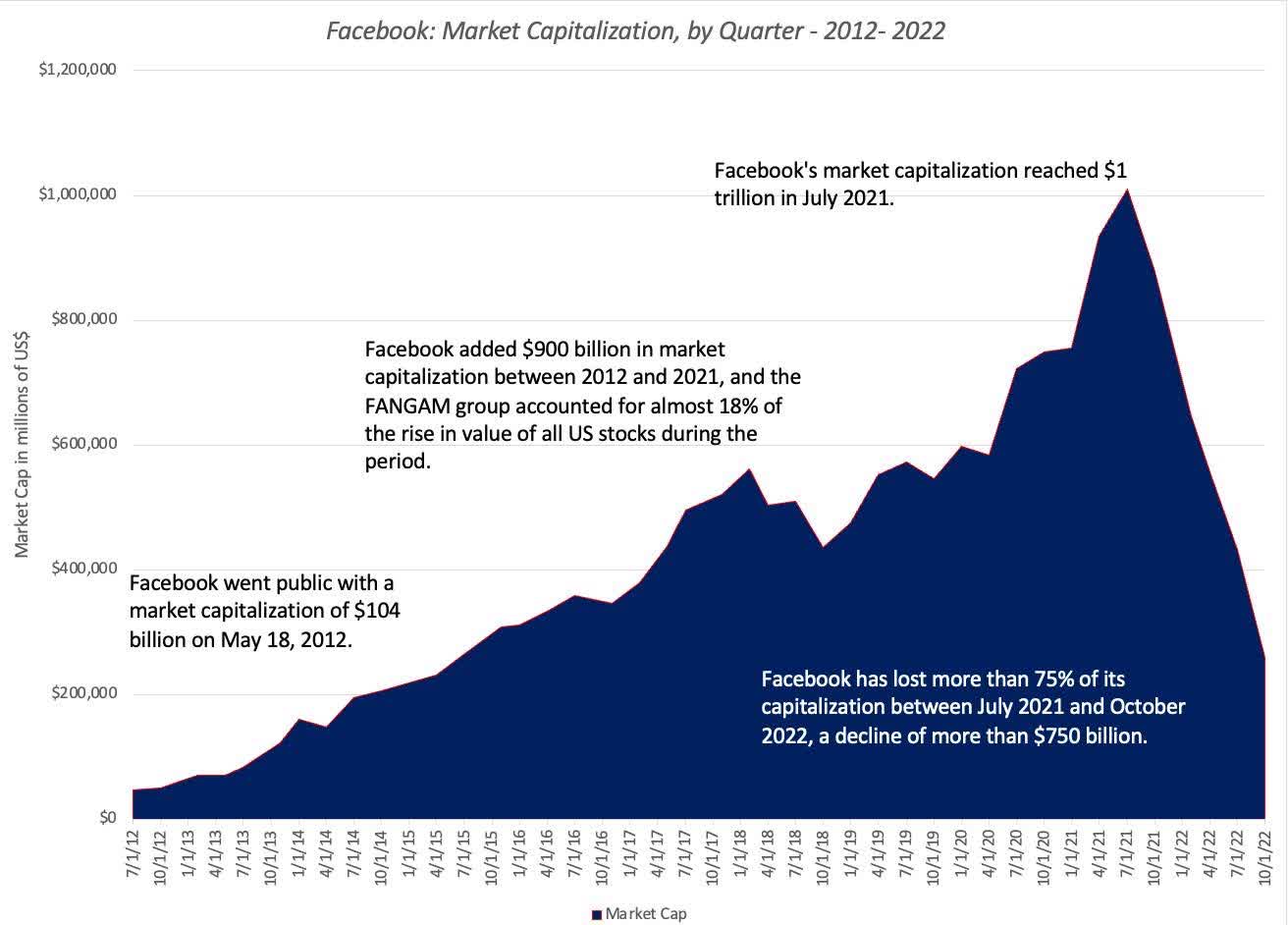

We’ve chronicled the difficulties Meta Platforms has endured in 2022 in recent Letters. With this Letter we expand our commentary on the Company and why we still remain quite bullish on the future of Meta Platforms. But first, we need to report some brutal numbers. The stock collapsed in 2022, declining -64%. Worse still, the stock had declined -70% from its all-time high of $384 in early September in 2021.

It seemed that everything that could go wrong for the Company in 2022 – did go wrong: A post-Pandemic growth hangover, the multibillion revenue hit from Apple’s (AAPL) infamous iOS 14.5 update that introduced the Company’s App Tracking Transparency (ATT), a cyclical slowdown in online advertising spending, poor capital allocation timing of stock buybacks, CEO Zuckerberg’s unchecked spending of billions on both new hirings and massive billions to be spent on Artificial Intelligence and the “Metaverse.” Even the renaming the Company from Facebook to Meta Platforms seems premature. In short (from that long list), CEO Zuckerberg has lost the confidence of shareholders. In the coin of the realm circa-2022, Meta Platforms had lost “the narrative” – despite its still intact Family of Apps profit and cash generation machinery.

Let’s start with the overarching matter of “The Metaverse.” What is it? When will it arrive? Why does it take multiple tens of billions of dollars in R&D? When will those multiple tens of billions of R&D dollars begin to generate revenues? What will be the return on those multiple tens of billions of R&D dollars? Is it possible that there may never be a return on those multiple billions of R&D dollars? Has META stock become just an open-ended bet on founder CEO (and controlling shareholder) Mark Zuckerberg’s avarice to prove his vision of the metaverse? Such questions, along with a collapsing stock price, have become a vicious circle that demand answers. We hope to offer answers in this commentary.

What is the “Metaverse?” These are hard questions to answer in 2022. Would the “3D version of the internet” simplistically suffice for now? We think so. Like so many other computer related technologies, “new” technologies are rarely “big-bang” revolutionary, but most often evolutionary. The metaverse will be no different.

Source: American Online

KATHLEEN (Meg Ryan): I don’t actually know him.

JOE (Tom Hanks): Really?!

KATHLEEN: We only know each other — oh God, you’re not going to believe this —

JOE: Let me guess. From the Internet?

KATHLEEN: Yes.

JOE: You’ve Got Mail.

KATHLEEN: Yes.

JOE: Very powerful words.

KATHLEEN: Yes…

– You’ve Got Mail. 1998.

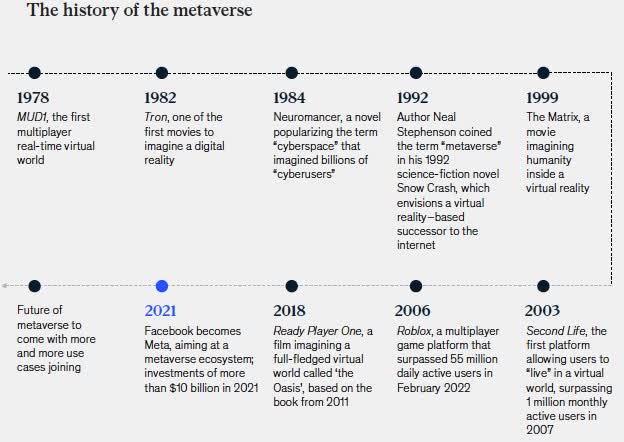

Think back to the first time you heard of this thing called the “Internet.” If you were a government researcher, you likely heard of it back in the 1960’s. If you were employed in the technology sector you may have heard about it in early 1983 when the TCP/IP became the standard protocol. Or maybe in 1994 when Mosaic Communications launched its Netscape Navigator web browser. Maybe 1989 when Quantum Computer launched its first instant messaging service. Quantum would rename itself America Online in 1991. More still heard of the potential internet in May 1995 when Bill Gates penned his famous memo entitled “The Internet Tidal Wave.”

Consider too the evolution of Cloud Computing. According to Keith D. Foote from Dataversity, the origins of two people using a single computer simultaneously was an idea funded by DARPA (the Defense Advanced Research Projects Agency) with a $2 million grant to MIT in 1963. In 1969, J.C.R. Licklider, who helped develop an early version of the internet called ARPANET promoted his idea of everyone on the planet would one day be interconnected by computers with access to an endless amount of information. Licklider called his computer vision with the zest of a sci-fi writer the Intergalatic Computer Network. “Virtual” private networks advancements in the 1990’s would bear the offspring we now call cloud computing. In 1999, Salesforce was a pioneer commercializing the internet to deliver software programs to their end users. In 2006, Amazon (AMZN) introduced Amazon Web Services. That same year Google (GOOG, GOOGL) launched Google Docs. A year later IBM and Google teamed with a few universities to develop huge server farms. That same year Netflix (NFLX) launched their streaming video service. The list goes on. 2011: Hybrid Clouds, IBM SmartCloud, Apple iCloud and Adobe (ADBE) Creative Cloud. 2012: Oracle (ORCL) Cloud. Today, cloud computing is ubiquitous – even the smallest Mom & Pop shop utilizes cloud computing.

So goes it with the metaverse. Meta Platforms addressed its vision of the metaverse in an internal memo entitled “The Metaverse” in June 2018, with the notable line early on in the memo that read, “The Metaverse is ours to lose…” Fast forward to 2022; we’ll let noted metaverse author and commentator Matthew Bell describe his informed view of the metaverse.

Source: Wall Street. 1987.

“Think of the metaverse as a fourth era of computing and networking—succeeding mainframes, which ran from the 1950s to 1970s; personal computers and the Internet of the 1980s to mid-2000s; and the mobile and cloud era we experience today. We are in the mobile era today, but the first cellular network call was in 1973, the first wireless data network was in 1991, smartphone in 1992, and so on until the iPhone in 2007. While it’s impossible to say when the development of the metaverse began, it’s clearly underway.

“Each era changed who accessed computing and networking resources, when, where, why, and how. The results of these changes were profound. But they were also hard to specifically predict. Think of the metaverse as a parallel virtual plane of existence that spans all digital technologies and will even come to control much of the physical world.

“The metaverse is often misdescribed as immersive virtual reality headsets, such as the Meta Quest (née Oculus VR), or augmented reality glasses, the most famous example of which to date is Google’s infamous Glass. VR and AR devices may become a preferred way to access the metaverse, but they are not it. Consider that smartphones are not the same thing as the mobile internet. The metaverse is also not Roblox, Minecraft, Fortnite, or any other game; these are virtual worlds or platforms that are likely to be part of the metaverse, just as Facebook and Google are part of the internet. For similar reasons, think of the metaverse as singular, just as we say “the internet” not “an internet. The next evolution to this trend seems likely to be a persistent and “living” virtual world that is not a window into our life (such as Instagram) nor a place where we communicate it (such as Gmail) but one in which we also exist—and in 3D (hence the focus on immersive VR headsets and avatars).”

-Matthew Ball, The Metaverse

Source: McKinsey & Company

The challenges of what the metaverse will be for Meta Platforms, notwithstanding, when asked when the metaverse will arrive as a commercial product, as well as when Meta expects to recoup its enormous R&D/Capex investment in the metaverse, CEO Zuckerberg’s answers are fleeting at best, and unanswerable circa-2022, at worst. Shareholders have thrown in the towel waiting for cogent answers.

Lest we kid ourselves, the idea that Zuckerberg has “lost Meta’s narrative” and share price appreciation (and depreciation) are not mutually exclusive. Zuckerberg has admitted that he greatly overestimated the longevity of the post-Pandemic business tailwinds – which in turn led him to budget enormous spending on AI ((FoA)) and Reality Labs (Metaverse). (Note: we made the same mistake on Meta and PayPal, PYPL.) Such booming tailwinds pulled forward so much growth, that that future comparison would begin to seem bust-like by late 2021 – and well into 2022.

Consider where Zuckerberg’s thinking was in the summer of 2021. The Company reported second quarter results on July 28. Revenues were up over 2020 by +56%. Operating margin expanded to 43% from 32%. Net income rose +101%! Shareholders rejoiced too. The stock would peak about a month later at $384 – a peak gain for the year of +40%. Recall too that the stock was up +108% in the preceding two years of 2019 and 2020. In late October that year, Zuckerberg changed the name of the Company from Facebook to Meta Platforms. Zuckerberg explained the name change and his vision of the metaverse in his Founder’s Letter, 2021 excerpted below:

“We are at the beginning of the next chapter for the internet, and it’s the next chapter for our company too. In recent decades, technology has given people the power to connect and express ourselves more naturally. When I started Facebook, we mostly typed text on websites. When we got phones with cameras, the internet became more visual and mobile. As connections got faster, video became a richer way to share experiences. We’ve gone from desktop to web to mobile; from text to photos to video. But this isn’t the end of the line.

“The next platform will be even more immersive — an embodied internet where you’re in the experience, not just looking at it. We call this the metaverse, and it will touch every product we build. The defining quality of the metaverse will be a feeling of presence — like you are right there with another person or in another place. Feeling truly present with another person is the ultimate dream of social technology. That is why we are focused on building this.

“As I wrote in our original founder’s letter: ‘we don’t build services to make money; we make money to build better services.’ This approach has served us well. We’ve built our business to support very large and long term investments to build better services, and that’s what we plan to do here.

“Right now our brand is so tightly linked to one product that it can’t possibly represent everything we’re doing today, let alone in the future. Over time, I hope we are seen as a metaverse company, and I want to anchor our work and our identity on what we’re building towards. We just announced that we’re making a fundamental change to our company. We’re now looking at and reporting on our business as two different segments: one for our family of apps and one for our work on future platforms. Our work on the metaverse is not just one of these segments. The metaverse encompasses both the social experiences and future technology. As we broaden our vision, it’s time for us to adopt a new brand.

“To reflect who we are and the future we hope to build, I’m proud to share that our company is now Meta. Our mission remains the same — it’s still about bringing people together. Our apps and their brands aren’t changing either. We’re still the company that designs technology around people.

“But all of our products, including our apps, now share a new vision: to help bring the metaverse to life.

And now we have a name that reflects the breadth of what we do. From now on, we will be metaverse first, not Facebook-first. That means that over time you won’t need a Facebook account to use our other services. As our new brand starts showing up in our products, I hope people around the world come to know the Meta brand and the future we stand for.”

We have long applauded companies that invest for the long-term. Companies, regardless of their particular industry, must adapt, or evolve, or they will slowly die. That’s why for years we have emphasized in our research the importance of capital allocation. This is critical to our investment process. We endeavor to hold our investments for many years, not just for a few quarters – which is the typical fare on Wall Street. Our portfolio of best of breed businesses generates substantial retained earnings. The deployment of this largesse into a myriad of capital allocation decisions (R&D, capex, M&A, stock buybacks) is arguably the most critical function of the C-suite.

We’ve owned Apple since 2005. Apple is a very different company than it was 15 years ago – much different still from the Company’s founding in Steve Jobs parents’ garage in 1975. At the time of our first purchase, the iPhone was little more than a twinkle in Steve Jobs eyes. In fact, early on in those years, the iPad was slated to be launched before the iPhone.

“An iPod. A phone. An internet communicator. Are you getting it?! This is ONE device.”

-Steve Jobs introducing the iPhone in 2007

Think of the evolution of Apple since Time magazine named the iPhone its Invention of the Year. Faster, smaller, more energy efficient semiconductors continue to change the technological and commercial landscape in ways unimagined just a few short years (Tesla, TSLA?). If you enjoyed binge-watching Breaking Bad on your iPad, you can thank advancements in cellular, fiber optics, WiFi, CPUs, GPUs and Retina 6K video. The App Store has allowed our super-computer mobile phones to become the most powerful, most personalized devices in human history. In short, the technological evolution at Apple (along with countless other integrated technologies) has created mobile devices to allow any human without fortune or political power to instantaneously connect to another human on the other side of the globe – all for the everyday low price of $20 per month.

“Humans love video, there’s five and half billion people that watch 2.6 hours of video per day of video content. In the United States it’s 300 million Americans watching five and a half hours per day”

– Matthew Ball. The Metaverse.

Now consider how different Meta Platforms is from its founding in Mark Zuckerberg’s college dorm room in 2004 as a Harvard-only social network. The lineage would first be text, and then photos, and then videos. The next (metaverse) will be full immersive, virtual reality.

In 2006, Facebook launched algorithmically generated updates user friends News Feed on desktops. Messenger was launched in 2011, plus launched for both Google Android and Apple iOS. Recall that mobile ad revenue was so slow to grow that the consensus view then was the Company missed “mobile.” Indeed, mobile app advertising revenues were just 11% of the Company’s revenue base early on. Yet, by just 2018, mobile app revenues were 93% of the base. In 2012, Zuckerberg bought Instagram for the then preposterous sum of $1 billion. Zuckerberg was just getting warmed up on the spending front. Oculus VR was acquired in 2014 for $2 billion. In 2014, Zuckerberg bought WhatsApp for the then astronomical price tag of $22 billion. In the fall of 2015, Facebook announces it had 1 billion users on a single day – 2 billion by the next summer. In 2017, Facebook rolled out Stories – which took time to ramp. In September 2021, the Company rolled out Reels – which also took time to ramp. Yet, according to the Company, just one year later, 140 billion video Reels are played across Facebook and Instagram – a gain of 50% in just six months. In addition, the Company reports they are gaining time spent share versus their dreaded rival TikTok. Even in the difficult year of 2022, the Company reports that users continue to spend more time on FoA.

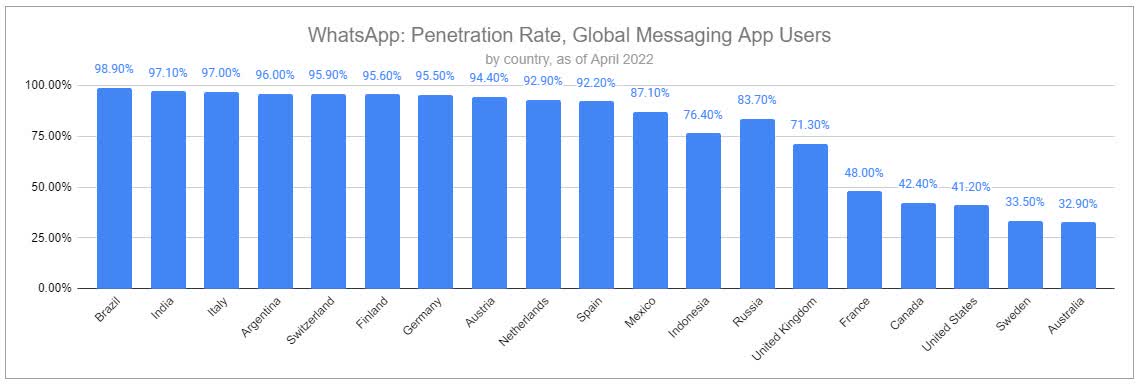

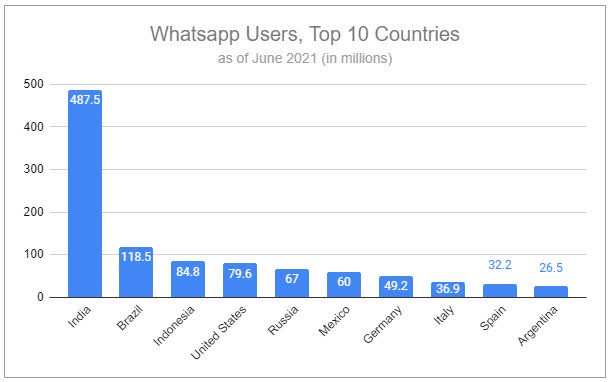

And WhatsUp with WhatsApp? WhatsApp has been flying under the radar for years. We suspect that’s about to notably change – in fact, it has. WhatsApp is actually the Company’s largest user platform. As mentioned above, Zuckerberg paid a king’s ransom for WhatsApp eight years ago – and we’ve only heard tidbits about the platform during earnings conference calls over the ensuing years. Even though WhatsApp is the Company’s fastest growing platform in the U.S., where WhatsApp has really shined is in underdeveloped markets and in Europe. Today, after enormous sunk costs, WhatsApp is the largest messaging app in the world.

Sources: Statista and Invariant Sources: Statista and Invariant

The free app has become ubiquitous as a basic messaging app. The last user update from the Company was back in 2020. At the time, monthly user growth reached 2 billion. However, during the Company’s last earnings conference call, the Company noted that WhatsApp daily average users now exceeds 2 billion – which has just surpassed Facebook’s DAUs.

According to Devin LaSarre of Invariant:

“In India, the country with the greatest number of WhatsApp users, for example, people rely on WhatsApp to communicate with friends, family, and colleagues, buy and sell items, send money, read news, and even access personal medical information. In other countries, like Brazil and Indonesia, total usage and use cases indicate the app may be more important than any other, including Facebook, Instagram, TikTok. Even in Russia, when Facebook and Instagram were banned following Russia’s invasion of Ukraine earlier in the year, WhatsApp was untouched. Popular throughout the country, it is clear that the Kremlin worried that blocking WhatsApp could generate significant blowback and loss of public support.”

The Company launched WhatsApp Business in 2018 for very small businesses and single entrepreneurs. Since then, the Company has offered the following updates on WhatsApp during recent earnings conference calls (thanks to LaSarre for chronicling these calls):

3Q 2018: 3 million business accounts on WhatsApp.

2Q 2019: Building WhatsApp Business ecosystem.

1Q 2020: Tens of millions business accounts on WhatsApp.

2Q 2020: 50 million businesses on WhatsApp.

2Q 2020: Zuckerberg introduces the term “messaging commerce.” 3Q 2020: Integrating WhatsApp Business with Facebook Shops.

3Q 2020: Per Zuckerberg. “But I think it should simplify things and make it so that these 3 different networks that we’ve had, between Messenger, Instagram and WhatsApp, can start to

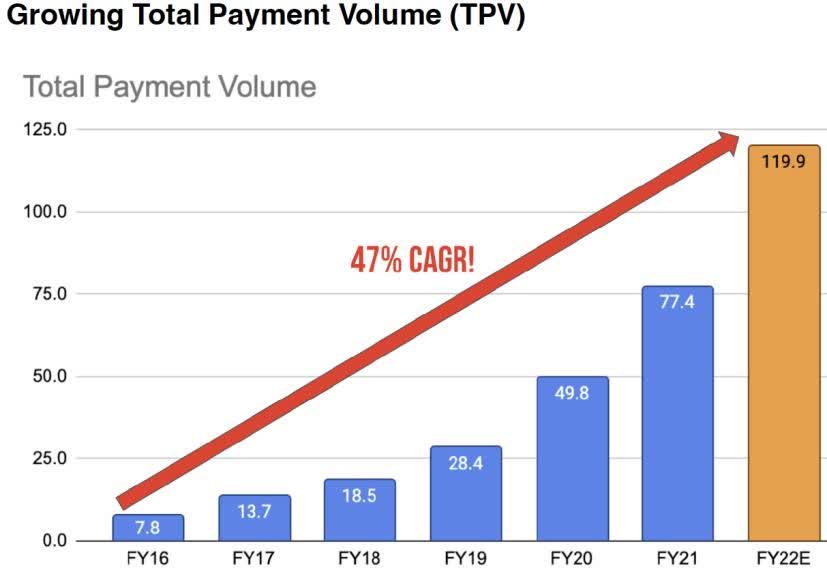

function a little bit more like one connected interoperable system.” 1Q 2021: WhatsApp Payments live in India and Brazil.

1Q 2021: WhatsApp Business API sending +100 million messages per day.

1Q 2021: During COVID conversations between people and businesses on Messenger and Instagram grew by more than 40%.

1Q 2021: More than 3 million advertisers use click-to-message ads to direct people to Messenger.

4Q 2021: More than 150 million users globally now view a business catalog in WhatsApp each month.

Q2 2022: Per Sandberg. “So that means the click-to-messaging ads become the perfect opportunity. They help us move people from discovery to a direct relationship with a business. In a world where we’re trying to do more with less data, they give businesses and consumers a direct connection, so it’s much easier to measure ROI. And so we’re investing heavily. You can message a business from Facebook and Instagram feed from Facebook, Instagram, Messenger Stories to WhatsApp, Messenger, Instagram Direct.”

Q3 2022: Per Zuckerberg. “Beyond Reels, messaging is another major monetization opportunity. Billions of people and millions of businesses use WhatsApp and Messenger every day, and we’re confident that we can connect them in ways that create valuable experiences. We started with click-to-messaging ads, which lets businesses run ads on Facebook and Instagram that start a thread on Messenger, WhatsApp or Instagram Direct, so they can communicate with customers directly. And this is one of our fastest-growing ads products with a $9 billion annual run rate. And this revenue is mostly on click to Messenger today since we started there first. But click to WhatsApp just passed a $1.5 billion run rate and growing more than 80% year-over-year.”

Lastly, in early December the Company announced a WhatsApp payments partnership with Latin America e-commerce giant MercadoLibre (MELI) for in-app payments. MercadoLibre is at the forefront of the huge unbanked/underbanked Latin American population.

Source: MELI 10-Q, 10-K and Jun Hao

Admittedly, these revenues won’t make or break any quarter in the near future, but at a minimum, they could well cover the Apple ATT revenue losses in the years ahead. In addition, the WhatsApp journey demonstrates that few, if any of the tech behemoths can challenge Meta Platforms in social media – particularly as they curate first-order, global content across FoA – and then next into the metaverse.

In our view, Zuckerberg has built and navigated the Company quite well as technology and user behavior has changed. He has built it. They have come. He continues to build. His “vision thing” has be good too considering his early critics on mobile, Stories and Reels. The jury is still out on his mega spending on metaverse – no, check that – the jury is out on this score. By Wall Street’s reaction, Zuckerberg’s metaverse vision and spending is a near unanimous flop. We don’t share this view. We remain bulls on Zuckerberg and Meta Platforms.

Actually, we’d be less bullish on the long-term prospects of Meta if Zuckerberg wasn’t building out a key element of the metaverse. To be clear, Zuckerberg isn’t building the metaverse, just a piece of it. Further, given the Company’s massive 3.5 billion monthly user, plus the fact that many millions of these users use their Facebook login credentials to access other websites throughout the internet, no other company has the combined billions in users and billions in capital to build a metaverse platform. Such a platform (think Microsoft, MSFT) would allow the Company to be more independent from the Apple iOS/Alphabet Android mobile duopoly. Apple’s ATT blocking of +$10 billion every year in Meta’s revenues has no doubt focused Zuckerberg’s mind – and will to spend – on this score. Speaking of Microsoft, Zuckerberg is no doubt well-versed too in the drama of how one of the wealthiest corporations ever to exist missed the mobile revolution. When it comes to technology platforms, one platform is a monopoly. Two platforms are a duopoly party. Three’s a crowd. Once Apple iOS and Google’s Android captured the smartphone market, despite Microsoft’s multi-billions in party favors, Gates, Ballmer & Co. were never invited to the trillion-dollar mobile party.

In fact, the general internet economy, which is to say any enterprise or institution whereby the internet today is in any way relevant, expect future “digital disruption.” These countless entities are already planning for the next evolution of the internet (call it what you will). And they collectively are already planning for it in size – whether Zuckerberg builds his vision of a metaverse platform or not.

McKinsey & Company published an exhaustive study last summer entitled, “Value Creation in the Metaverse: The Real Business of the Virtual World. Here are their key findings:

- The metaverse has the potential to impact everything from employee engagement to the customer experience, omnichannel sales and marketing, product innovation, and community building.

- We believe the metaverse has the potential to be the next iteration of the internet. It may seamlessly combine our digital and physical lives by featuring a sense of immersion, real-time interactivity, user agency, interoperability across platforms and devices, the ability for thousands of people to interact simultaneously, and use cases spanning activities well beyond gaming.

- Beneath the hype, the metaverse’s development continues. Roblox, launched in 2006, has attracted companies including Nike and Gucci as advertisers and partners. Fortnite has more than 20 million daily active users (DAUs), has hosted concerts (more than 27 million unique players attended a Travis Scott performance last April), and generated more than $14 billion in transactions between 2018 and 2020. Naver Z’s Zepeto—Asia’s largest metaverse platform—has over 300 million global subscribers, and in April partnered with Samsung for its Galaxy S Treasure Hunt campaign.

- We estimate it may have a market impact of between $2 trillion and $2.6 trillion on e-commerce by 2030, depending on whether a base or upside case is realized. Similarly, we estimate it to have an impact of $180 billion to $270 billion on the academic virtual learning market, a $144 billion to $206 billion impact on the advertising market, and a $108 billion to $125 billion impact on the gaming market.

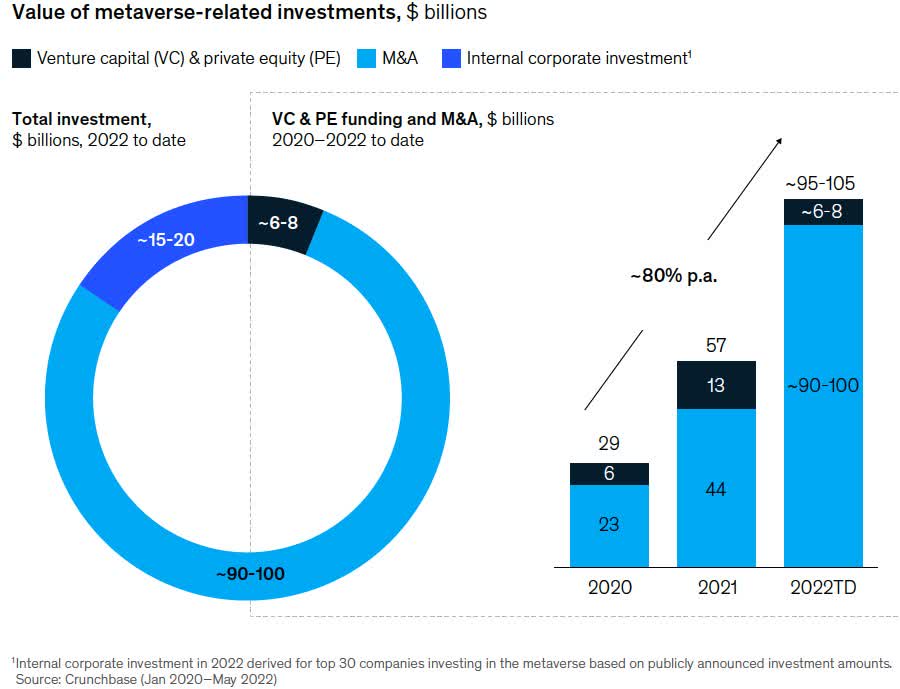

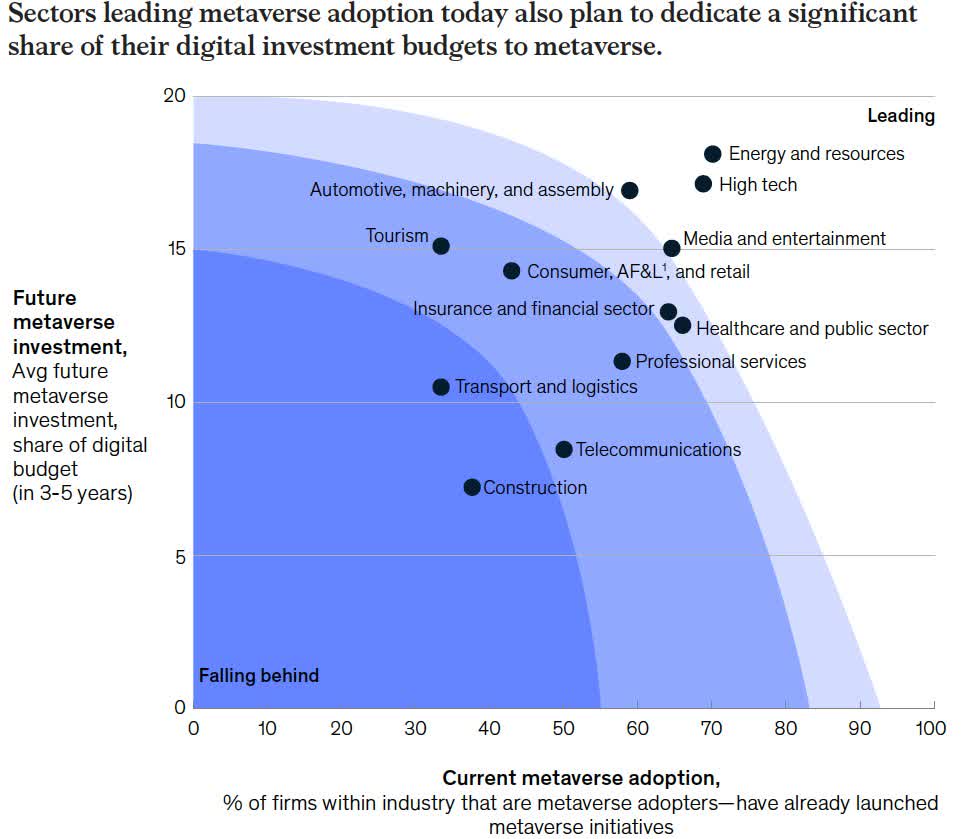

- Large technology companies, venture capital (VC), private equity (PE), start-ups, and established brands are seeking to capitalize on the metaverse opportunity. Corporations, VC, and PE have already invested more than $120 billion in the metaverse in the first five months of 2022, more than double the $57 billion invested in all of 2021, a large part of it is driven by Microsoft’s planned acquisition of Activision for $69 billion. Large technology companies are the biggest investors — and to a much greater extent than they were for artificial intelligence (AI) at a similar stage in its evolution, for example. Industries currently leading metaverse adoption also plan to dedicate a significant share of their digital investment budgets to it.

- Our survey of more than 3,400 consumers and executives found significant excitement about the potential of the metaverse. Almost 60 percent of consumers using today’s early version of the metaverse are excited about transitioning everyday activities to it, with connectivity among people the biggest driver, followed by the potential to explore digital worlds. Some 95 percent of business leaders expect the metaverse to have a positive impact on their industry within five to ten years, and 61 percent expect it to moderately change the way their industry operates. Industries most likely to be impacted by the metaverse include consumer and retail, media and telecommunications, and healthcare, and those industries are also among those already undertaking metaverse initiatives.

We may look back in time and chuckle at the enormity of McKinsey’s forecasts. On the other, history is rife with outrageously low forecasts of how big computers, the internet and smartphones would ultimately become.

Here are a few more metaverse forecasts to mark for posterity:

- KPMG forecasts a $13 trillion market opportunity and 5 billion users for the metaverse by 2030.

- Morgan Stanley (MS) forecasts an $8.3 trillion opportunity for advertising and e-commerce on the metaverse.

- Citi estimated the total addressable market (TAM) for the metaverse between $8 trillion to $13 trillion.

- Goldman Sachs’ (GS) global metaverse projection between $2.5 trillion and $12.5 trillion.

OK, all that future metaverse bounty aside, let’s get back to the present. We have no doubt been on the wrong side of the stock in 2022. A review of the good, the bad and the ugly – mostly ugly – in 2022 is in order.

Source: aswathdamodaran.blogspot.com

The first crack in the bull “narrative” came early in 2022 when on February 2 the Company reported weaker than expected fourth quarter net income. Even though revenues were in line at +20% growth, net income came in at -5%. The Company gave weak guidance, reported that user growth had slowed, but even worse, expenses skyrocketed up +38%. The Company quantified Apple’s ATT hit at an annual run rate of $10 billion. Zuckerberg was adamant that spending would remain at elevated levels. The stock tanked -20% the next day. The stock would suffer more than the general market over the course of the bear market. The coup de grâce for Zuckerberg & Co. would come on October 26 when the Company reported third quarter results.

The results were truly awful. Year-over-year revenue -4% – the second consecutive quarterly revenue decline. Expenses were +19%. Operating margin collapsed to 20% from 36%. Net income collapsed -52%! Losses at Reality Labs skyrocketed too. Losses in this segment rose to -$3.7 billion during the quarter and -$9.4 billion in the first three fiscal quarters. As bad as these backward-looking numbers were, forecasts for 2023, were in a word, shocking. For the full year in 2022 total expenses were likely to come in at around $86 billion – a gigantic number. 2023 forecasted expenses were expected to increase to $96-$101 billion. Reality Lab losses in 2023 were forecasted to “grow significantly.” Even the most patient of investors had seen – and heard enough. No valuation was too low enough to negate selling. The stock fell -25% the next day to $98 – and drifted to $90 over the next week. The low was $88. From its high of $384, the stock collapsed -77% in little more than 14 months.

Meta Platforms (Zuckerberg’s) ensuing consensus epitaph was swift and brutal. Zuckerberg broke Facebook. In his zeal and quest to build the next-generation internet platform he – and he alone – would not only bet (and lose) the Company’s treasury of multiple billions. These billions were gone, never to be recouped. Metaverse spending was a sinkhole. But he would also risk in the process neglecting the Company’s cash-generating machine (FoAs). The stock? Well. Wall Street’s swift verdict – dead and buried money.

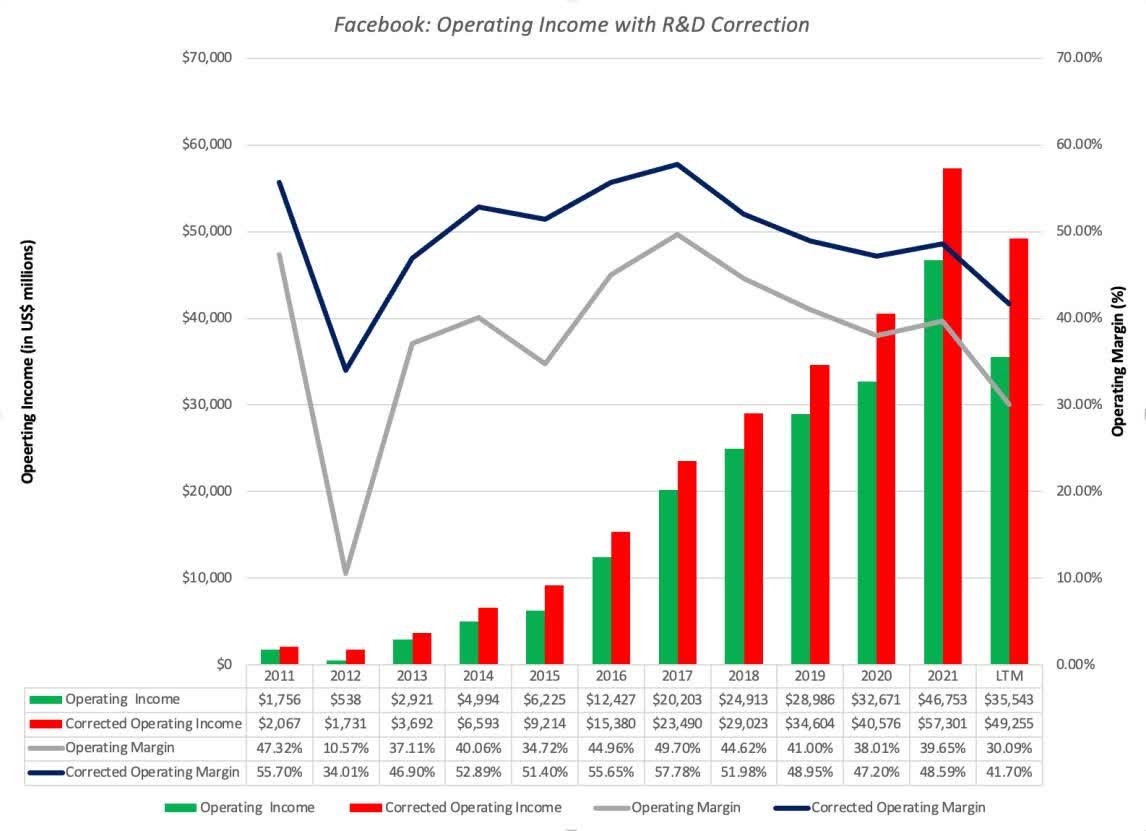

As disappointing as the recent reported financials have been – and no doubt they are, we would like to offer a second, perhaps more judicious look at the Company’s reported financials. Aswath Damodaran is a Professor of Finance at the Stern School of Business at NYU. His blog, Musings on Markets is a must read for both finance students and investment professionals. In a November post he detailed on the Company’s conservative accounting treatment of its R&D expenditures. The Company passes these huge R&D expenses through their income statement as operating expenses.

Source: aswathdamodaran.blogspot.com

Damodaran makes the case (and we agree) that the Company’s R&D expenses should be capitalized assets on the balance sheet, and then prudently amortized over a three-year period. Such treatment offers a more accurate economic reality for the Company compared to the misplaced accounting treatment. In the graph below, please note the significantly higher corrected operating income and corrected operating margin. Wall Street’s knee-jerk obits on Meta Platforms look to be quite a bit more fiction, than nonfiction.

So how did we fare in our evolving analysis and portfolio management during these repeated disappointments in 2022. In a word, poor. Very poor. Grade F.

We first bought the stock in February 2018 during the Cambridge Analytic scandal. Recall then the bearish pileup on Facebook throughout 2018: Huge government fines, huge new spending on employees and R&D on new privacy initiatives, missed analysts’ expectations, slowing user growth and revenue growth, European Union’s General Data Protection Regulation (GDPR) was launched, plus the recent launch of Stories was monetizing at poor rates. (Kind of has a familiar ring to 2022.)

We first bought Facebook stock in February around $179. We slowly added to our position throughout 2018 and into March of 2019. The prices we added were around $153 and $170. By the last add in March 2020, the position became our largest at a 9.0% weight. The stock would find a bottom (as well as the overall stock market – Powell Pivot) in late December that year around $125. The stock would then boom (with a very short Pandemic-related decline in March of 2020) to nearly $385 at its peak in early September 2022. We made small trims in mid-2020 at $228 and $294. So far, so good.

As mentioned, we made the mistake thinking that Pandemic-related growth rates in 2021 for the Company, while likely to moderate in growth rates, yet still grow, would not decline – and heretofore online ad spending less cyclical than tradition mediums. Wrong on both. As such, after to stock retreated from its 2021 high, we added to our position at… $328. Ugh. We added again this past March at $194. As the stock collapsed in 2022, so did our grade point.

The saying, “When you’re in a hole, stop digging” applies to portfolio management too. We’ve stopped digging – for now. Although our weighting in the stock currently stands at +4%, the client capital we’ve cumulatively invested in the stock is considerably more. The stock at year-end is back to $120 – a sharp climb from $88 at the depths in early November.

The stock at current valuations has priced in zero growth in FoA users and little rebound in profitability. This is fat-pitch territory. Valuations at current levels need to assume a long secular decline in the Company’s Family of Apps business and continued billions dumped into the assumed metaverse landfill. Both extremes in the negative, in our view. If the combination of favorable 2023 catalysts emerge, along with unduly cheap valuations we may well swing again at the shares.

2023 Catalysts

- Macro: Cadence of improvement in digital ad spending. Verticals like healthcare and travel remain healthy, but larger verticals such as e-commerce and gaming have been struggling.

- Capex: 82% of spend is on FoA. Zuckerberg is not betting the Company treasure on Reality Labs (metaverse). This outsized focus will be on Artificial Intelligence (AI) and Machine Learning (ML) probabilistic models – key to Reels growth too. 15% of the content users viewed on Facebook and Instagram has been generated by AI. Per the Company, “…our level of Capex investment will depend on the returns that we generate through these investments in AI…and if we don’t, we’ll pace back our spend accordingly.” Capex spending of billions on FoA continues to be a key competitive advantage for the Company.

- FoA: North America user base is largely saturated. Will users stay? Stickier users engage more.

- Reels: Continued user engagement growth across FoA and improved monetization. Comparisons of Stories monetization are instructive: Stories took four years to monetize at the rate of News Feed. Per Zuckerberg on Q2 2022 earnings call, “Reels is actually making faster progress than we expected. We’ve now crossed $1 billion annual run rate for Reels ads, Reels also has a higher revenue run rate than Stories did at the identical times post launch.”

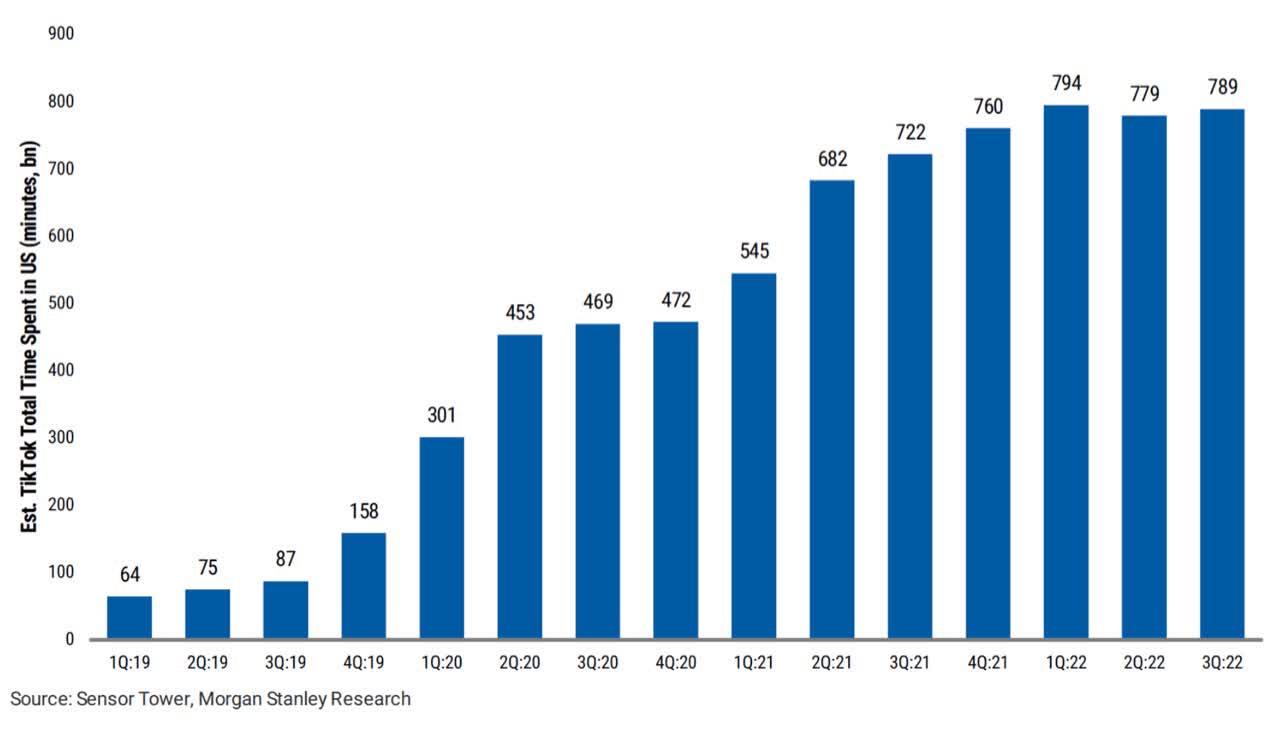

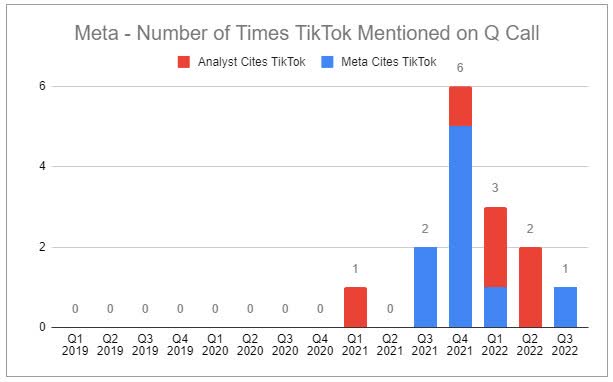

- TikTok: Does TikTok continued to impede Instagram’s growth? Peak TikTok may be at hand. Growing awareness of national security risks at state level issued phones, federal level politicians, CFIUS and the FBI. Even if calls for bans in the U.S. don’t materialize, national advertisers may move away from TikTok, to Reels benefit.

Source: Invariant

- Twitter: According to Media Matters for America, Twitter has lost half of its largest 100 brand advertisers due to Elon Musk’s political leanings. If this continues, advertisers may spend some of these ad dollars with Meta Platforms.

- WhatsApp and Messenger: Continued monetization on both platforms. WhatsApp daily average users (DAU) in North America (their fastest growing market) continues apace. WhatsApp growing significantly internationally. Key commercialization on both platforms helps to offset Apple’s ATT/IDFA.

- Advantage+: New machine learning tools such as Advantage+ continue to grow beyond early verticals of e-commerce and retail.

- Apple: ATT/IDFA impact post-2023 one-year anniversary. ATT hurts Apple ads revenues as well. Apple’s next gen ad attribution (SKAdNetwork 4.0) will offer more signal linkages between advertiser and click-through attribution.

- AI: Artificial Intelligence (plus Machine Learning) continues to power better ad rankings and scale engagement.

- Privacy: An unremarked competitive advantage for the Company. Privacy spending on social networks is gigantic. Privacy is multi-billion annual table stakes in global social media platforms. Meta Platforms is without peer. Ironically, ever more stringent privacy regulations will actually protect the Company’s outsized competitive privacy advantage, and thus profitability.

- Currency: At its worst in 2022 forex was a -700 basis point headwind to revenue. The U.S. dollar has fallen since then. Note, on a forex-neutral basis, 3Q revenues actually rose by +2%.

- Management: If the macro digital ad environment worsens will Zuckerberg reign in spending at a concomitant rate? Zuckerberg’s most recent comments speak to a newfound balance on spending. In early November, Zuckerberg announced layoffs of more than 11,000 workers (13% of headcount). In December, at a New York Times hosted event, Zuckerberg stated he will operate the Company with “discipline and rigor.”

| The information and statistical data contained herein have been obtained from sources, which we believe to be reliable, but in no way are warranted by us to accuracy or completeness. We do not undertake to advise you as to any change in figures or our views. This is not a solicitation of any order to buy or sell. We, our affiliates and any officer, director or stockholder or any member of their families, may have a position in and may from time to time purchase or sell any of the above mentioned or related securities. Past results are no guarantee of future results. This report includes candid statements and observations regarding investment strategies, individual securities, and economic and market conditions; however, there is no guarantee that these statements, opinions or forecasts will prove to be correct. These comments may also include the expression of opinions that are speculative in nature and should not be relied on as statements of fact. Wedgewood Partners is committed to communicating with our investment partners as candidly as possible because we believe our investors benefit from understanding our investment philosophy, investment process, stock selection methodology and investor temperament. Our views and opinions include “forward-looking statements” which may or may not be accurate over the long term. Forward-looking statements can be identified by words like “believe,” “think,” “expect,” “anticipate,” or similar expressions. You should not place undue reliance on forward-looking statements, which are current as of the date of this report. We disclaim any obligation to update or alter any forward-looking statements, whether as a result of new information, future events or otherwise. While we believe we have a reasonable basis for our appraisals and we have confidence in our opinions, actual results may differ materially from those we anticipate. The information provided in this material should not be considered a recommendation to buy, sell or hold any particular security. i Returns are presented net of fees and include the reinvestment of all income. “Net (Actual)” returns are calculated using actual management fees and are reduced by all fees and transaction costs incurred. |

Editor’s Note: The summary bullets for this article were chosen by Seeking Alpha editors.