Summary:

- Algonquin Power & Utilities owns and operates various regulated and non-regulated power assets, including utilities for generation, distribution, and transmission.

- The company plans to improve its business by reducing costs, maintaining its credit rating, minimizing the need for new equity financing, and focusing on organic growth.

- AQN will reduce its dividend by 40% and suspend its DRIP program, sell assets worth $1 billion, and pursue the acquisition of Kentucky Power.

- My target value is $8 per share, based on a DCF model using a cost of capital of 6.4%. I would stay away till more news on Kentucky Power and the divestitures.

SimonSkafar

Algonquin Power & Utilities Corp. (NYSE:AQN) (TSX:AQN:CA) owns and operates a range of regulated and non-regulated power assets, including generation, distribution, and transmission utilities. On January 12, AQN provided an investor update where they presented their plans to improve their business by reducing costs, maintaining their credit rating, and minimizing the need for new equity financing. One of the key actions they will take is a 40% reduction in dividends and suspending their DRIP program. They also plan to sell assets worth $1 billion and continue to pursue the acquisition of Kentucky Power (‘KP’).

In this article, I will summarize the key points from the investor update and update my valuation. In a nutshell, I believe the fair value is $8 per share.

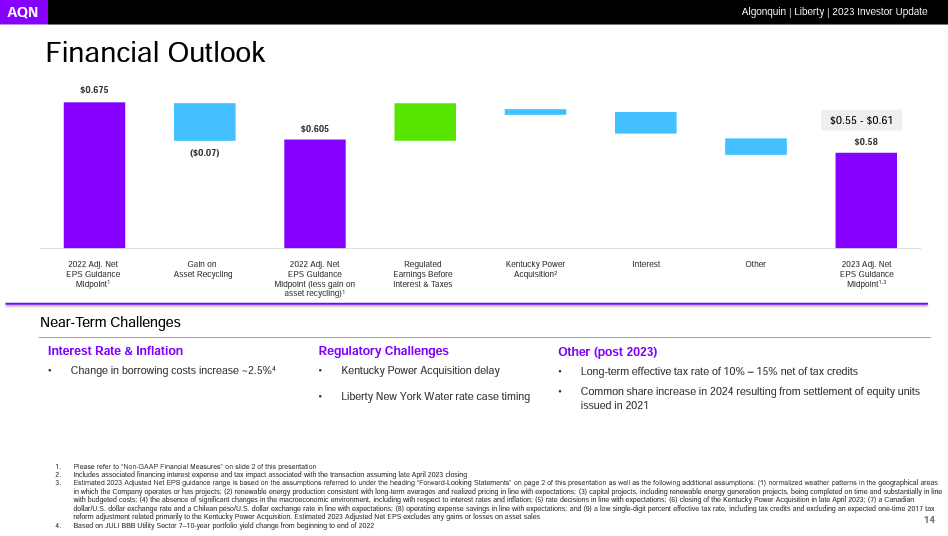

Regarding EPS, AQN forecasts a range of $0.55 to $0.61 per share for 2023. The reduction is due to delays in the KP acquisition, pressure from interest rates, and one-time gains from asset recycling in 2022.

Company presentation

AQN aims to achieve a normalized annual EPS growth of 5% to 8% by focusing on organic growth. However, there are challenges, such as higher tax rates and increased interest rates. Despite this, AQN has secured about $400 million in floating-rate debt at 4.5%. There could also be a potential impact on earnings due to the expiration of Production Tax Credits for some of their older wind farms, resulting in lower income from the sale of their renewable energy. On the positive side, AQN expects to benefit from rate-case adjustments in some of its regulated operations and further organic growth in its renewable energy portfolio. The success of AQN’s plan to sell off $1 billion of assets will depend on which assets are sold and the price they are sold for.

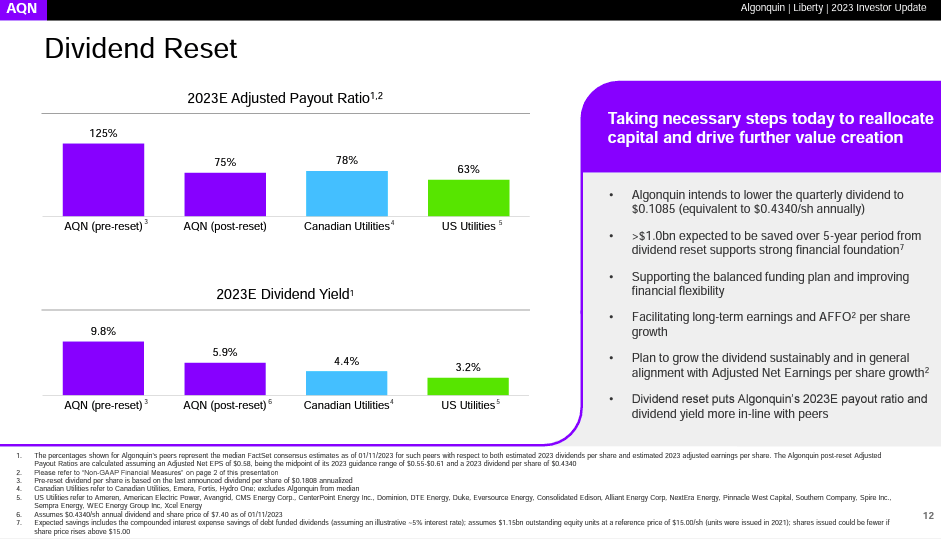

AQN intends to decrease the quarterly dividend to $0.1085 per share ($0.4340 per share annually) from $0.1808 per share starting in Q1 2023. Management expects to save over one billion in a 5-year period through its dividend reset plan. This plan aims to strengthen the company’s financial foundation, improve its financial flexibility, and support its balanced funding plan. The dividend reset is also expected to facilitate long-term earnings and AFFO per share growth. Management plans to grow its dividend sustainably and align with its EPS growth. The dividend reset will bring the 2023 payout ratio and dividend yield more in line with its peers.

Company presentation

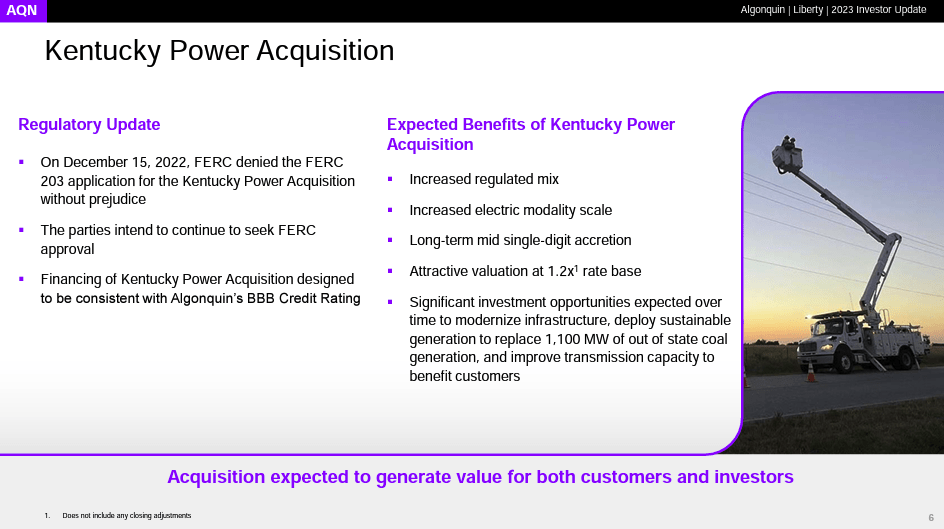

Despite being rejected by the FERC in December 2022, AQN and American Electric Power Company Inc. (AEP) plan to continue working to close the Kentucky Power acquisition. In my opinion, AQN will be unsuccessful in the appeal. This could be viewed as positive news as it could alleviate the balance sheet.

Company presentation

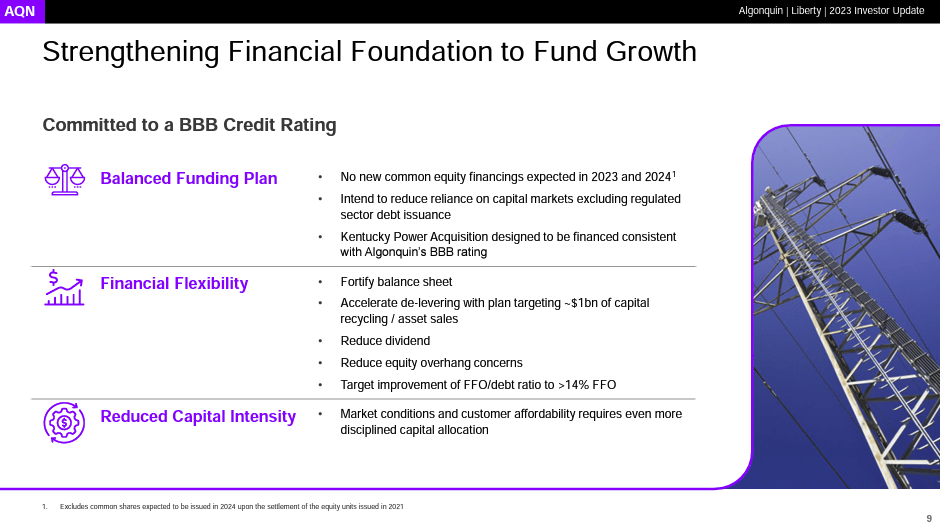

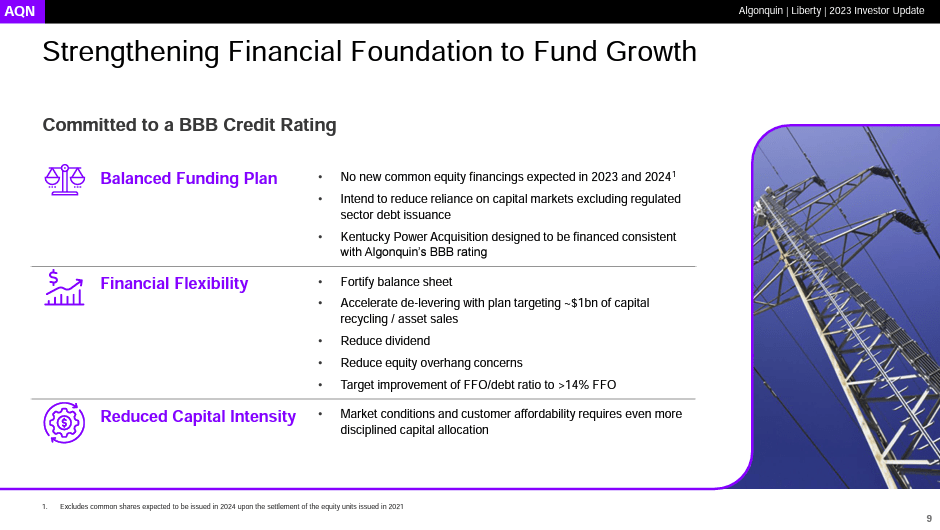

AQN plans to maintain its BBB credit rating by implementing a balanced funding plan, which includes no new equity financing until the end of 2024 and reducing capital spending. The company aims to raise one billion through renewable asset recycling transactions and additional asset sales to pay down debt and remain compliant with its credit metrics after the KP acquisition. To achieve this, AQN has committed not to engage in new equity financings and suspended its DRIP as of the Q1 2023 dividend payment. AQN had approximately $2.3 billion of available liquidity on credit facilities at the end of 2022.

Company presentation

The one billion asset recycling plan involves selling renewable assets with proceeds expected in 2023 and 2024. AQN completed its inaugural asset recycling transaction by selling operating U.S. wind assets in December 2022. While AQN has not provided specific details on which other assets may be sold, I believe its stake in Atlantica Yield (AQN owns 44%) could be a potential candidate for sale.

Company presentation

AQN has provided guidance for 2023 and expects adjusted EPS of $0.55-$0.61 per share, down year-over-year from $0.675 in 2022. The elimination of one-time gains is the main factor contributing to this decrease in earnings. The drop in adjusted EPS is also largely driven by higher interest rates on existing debt and the higher cost of servicing incremental debt needed to fund the Kentucky Power transaction.

Valuation

My target value is $8 per share. This is based on a DCF model using a cost of capital of 6.4%. The assumed unlevered beta corrected for cash is 0.41 (source). I expect revenues to increase by 7% in 2023, in line with management’s guidance. I expect a headwind due to interest rates (15% of debt is variable rate) and inflation impacting the medium-term. As a result, I expect 2023 EPS slightly lower than guidance at 50 cents per share.

Company filings

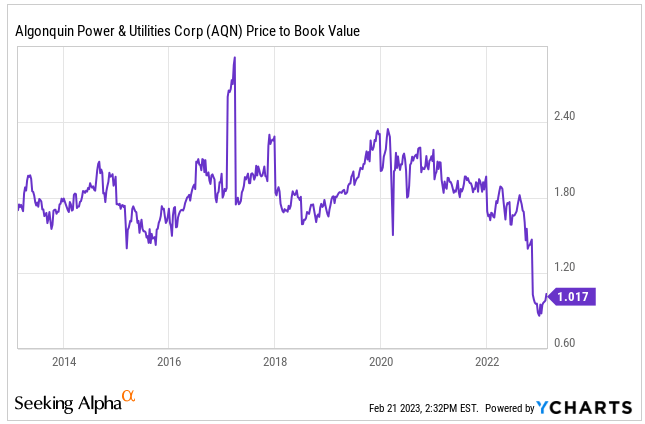

This valuation implies 1.06x book value, which is in line with the forecasted ROE that is 100-150 bps above the cost of capital in the medium term.

Ycharts

Conclusion

AQN is taking strategic actions to improve its financial position and achieve long-term growth. The company is implementing a balanced funding plan, reducing costs, and suspending its DRIP program. AQN is also focusing on organic growth and expanding its renewable energy portfolio while pursuing the acquisition of Kentucky Power. The dividend reset plan will strengthen the company’s financial foundation, improve its financial flexibility, and support its balanced funding plan.

However, challenges such as higher tax rates, increased interest rates, and potential impact on earnings from the expiration of Production Tax Credits for some of their older wind farms are expected.

I expect AQN to have a lower return on equity than its past around its cost of capital. Thus, by the valuation of $8 per share seems justifies as it is close to the book value per share. I would stay on the sidelines till we have more clarity on KP and more news on the asset divestitures.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.