Summary:

- Some investors have ignored the merits of holding banks such as Bank of America Corporation in their portfolio in favor of large tech stocks, like Apple.

- Since the banking crisis began, both regional and big banks have been under intense pressure, creating HUGE opportunities.

- Bank of America has a five year DGR of 15% and they have increased their dividend for 9 consecutive years.

blackdovfx/iStock via Getty Images

When it comes to investing, it is all about opportunity. Far too often, investors try and time the market, and more often than not, they miss opportunities. Opportunities come and go.

Obviously, over the past 12 months, we have seen a lot more opportunities in stocks than the 12 months prior when we were in the midst of a bull market, one that happened to be the longest bull market in history. But now, things are different.

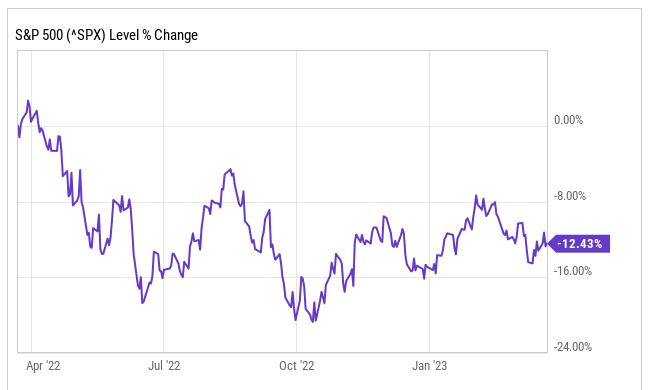

Now, we are stuck in the midst of a bear market, again, one that seems to continue to chug along now for more than a year. Over the past 12 months, the S&P 500 (SP500) has fallen by 12%.

ycharts

However, with the majority of the market in the red, there are some very different valuations among the leaders. For years, many have run to leadership names like Apple Inc. (AAPL), and for good reason, as they have displayed strength from a balance sheet perspective and demand as well as innovation in terms of products.

However, many believe we are headed towards a recession, and analysts believe Apple’s growth is likely to slow or decline in 2023, but the current valuation does not reflect that.

In addition, we just went through a mini banking crisis with Silicon Valley Bank of SVB Financial Group (SIVB), among others, which has uncovered huge opportunities in SPECIFIC financial leaders, one of which I believe is trading at a sizable discount in Bank of America Corporation (NYSE:BAC).

Bank of America has strengthened over the years under the leadership of CEO Brian Moynihan, who some believe to have surpassed Jamie Dimon of JPMorgan Chase (JPM) in terms of leadership and running a large financial institution. Bank of America has prioritized returning money to shareholders, as evidenced by their five-year dividend growth rate of 15% and nine consecutive years of dividend growth.

Bank of America Is Trading At Multi-Year Lows

Bank of America, as you may know, is one of the two largest U.S. banks, in terms of assets, trailing only JPMorgan Chase.

As many of you are aware right now, unless you have been off the grid for a few weeks, the financial markets have been going through a bit of what I call a mini financial crisis. Nothing to the magnitude of 2008, but the sector has seen intense selling, especially within the regional sector, but the big four banking institutions have also felt the selling pressure.

What happened at Silicon Valley Bank was that the bank was overextended in US treasury bonds that they bought towards the early part of the rate hike cycle. Their strategy was that the Fed would slowly roll out its policy, but in reality, we saw one of the fastest rate hike cycles in modern history.

Given the pace of the rate hikes, these bonds fell in value, and SVB was sitting on huge losses. Now, if they held those to maturity, they would have been fine, but SVB announced a capital raise which brought into question the safety of depositor funds. Once this became known, depositors rushed to request their money all at once, what is called a “run on the bank.” SVB did not have enough liquidity to cover, and thus the bank failed and regulators were forced to step in.

That is a quick synopsis. However, this sent shockwaves through the banking sector as a whole, regardless of the size of the bank.

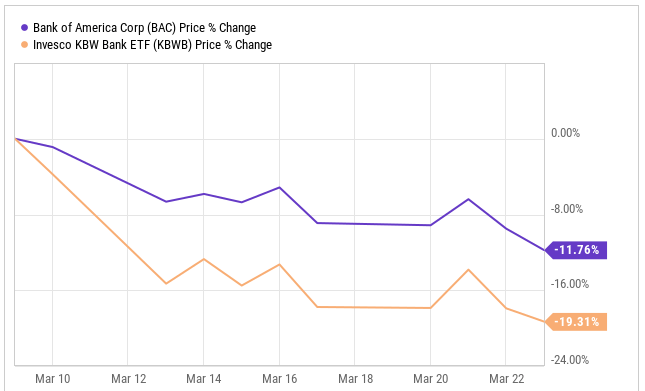

SVB shares were sent tumbling on March 9th, and since that date, shares of the Invesco KBW Bank ETF (KBWB) are down nearly 20%, while shares of BAC are down 12%.

ycharts

We also saw Credit Suisse Group AG (CS) come under pressure in recent weeks, and it was just announced that their rival UBS Group AG (UBS) would be acquiring them as soon as April.

So, a lot of Bank news, but what this has done is put INTENSE pressure on the sector as a whole, creating opportunities.

One of those opportunities as I briefly mentioned was in shares of Bank of America. BAC has a market cap of $222 Billion.

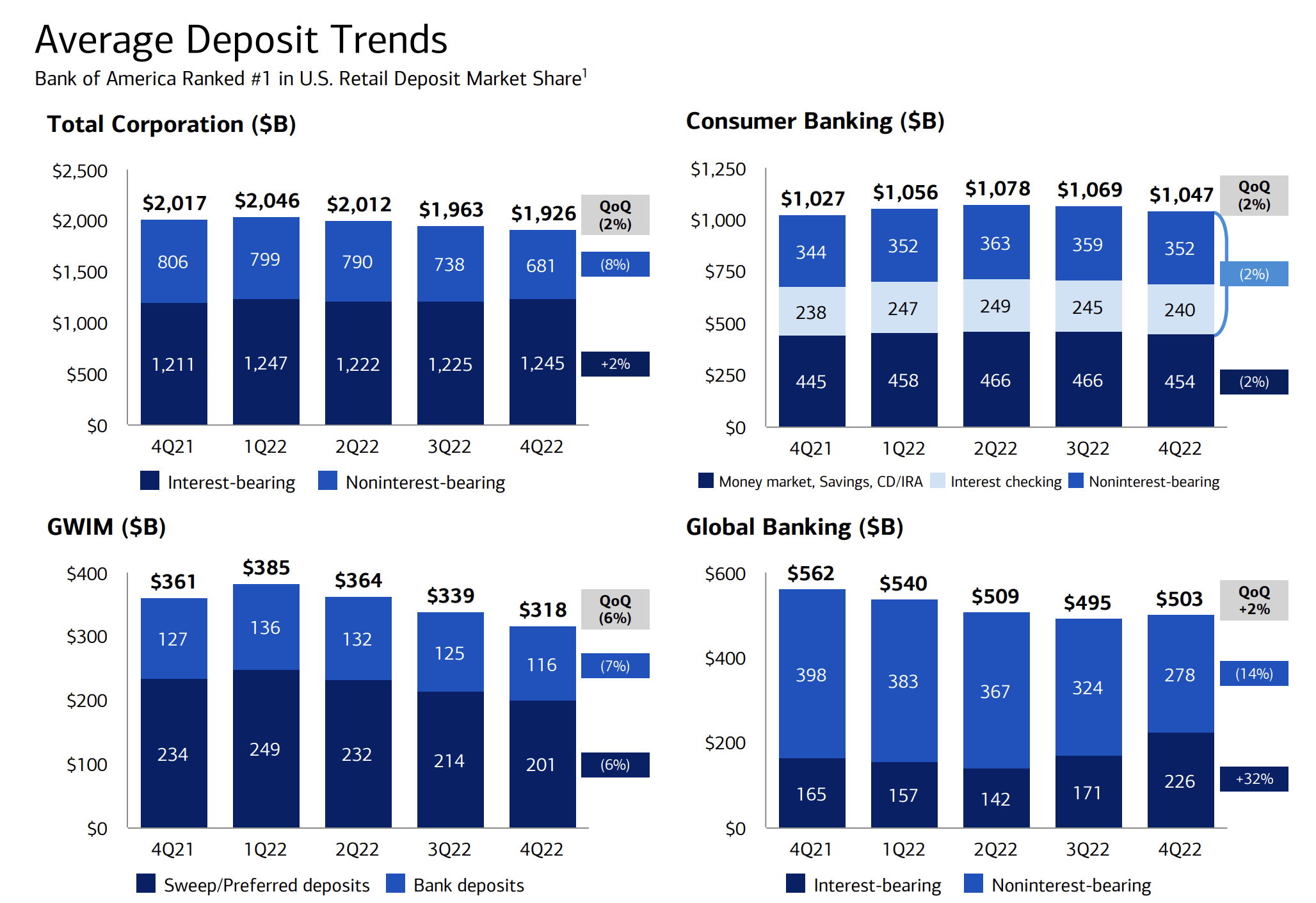

The thing is, Bank of America also has Held to Maturity securities just like Silicon Valley Bank did, except BAC has the proper amount of additional capital, meaning they do not need to sell any of those assets at a loss like SVB was forced to do. As of the company’s latest filing, BofA has $1.93 trillion in customer deposits

BAC Q4 Investor Presentation

In fact, Bloomberg reported that this mini crisis actually helped BofA – the business, not the stock – as all financials fell, but the company saw $15 billion in new deposits come in after the SVB failure. Consumers are clearly looking for more stability, which a big bank like BAC offers.

As such, given the drop in shares of BAC, we are seeing shares trading at multi-year lows and trading at an extremely low valuation, making this a potential great opportunity for long-term minded investors.

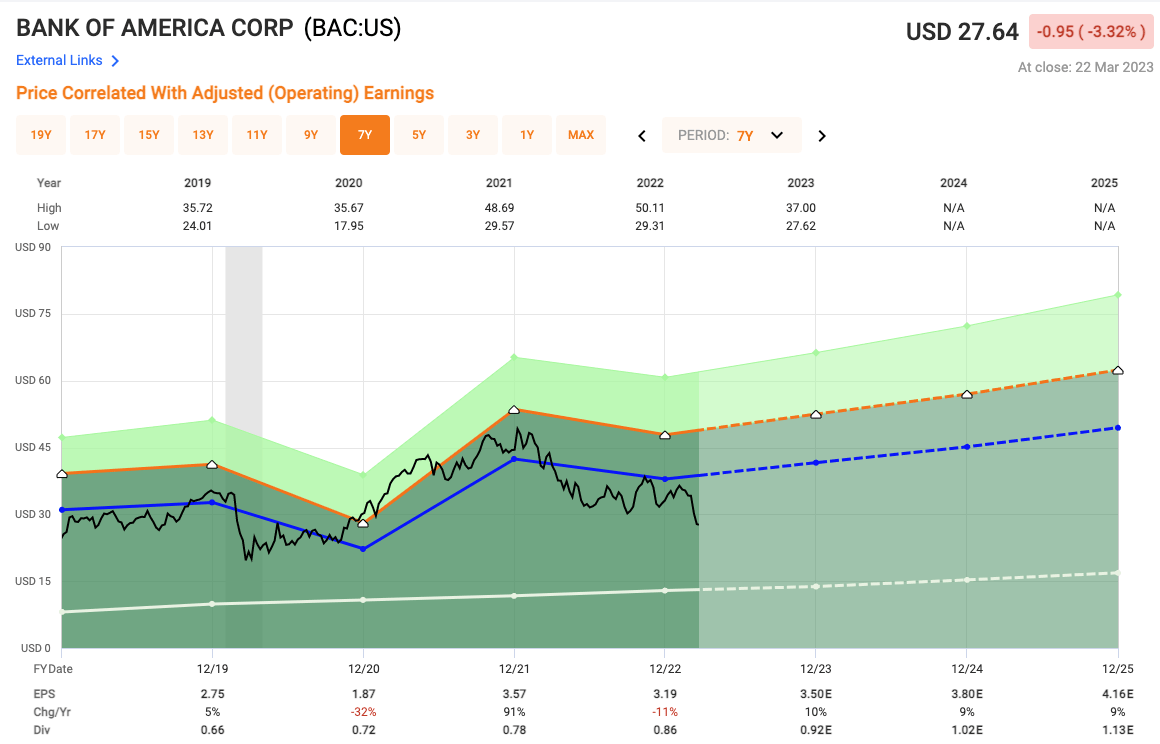

Analysts expect Bank of America to produce EPS of $3.50 in 2023 and $3.80 in 2024, and the stock is currently trading around $27. As such, investors can now buy the large bank stock at similar valuations to what we saw during the start of the global pandemic.

BAC shares are trading at a forward earnings multiple of just 7.7x, which is incredibly low. We are talking about one of the two largest banks in the U.S., and the world for that matter, trading at less than 8x, more than HALF the multiple of the S&P 500. Talk about value.

Bank of America Corporation stock could absolutely face more downside, but you know right here, you are buying at multi-year lows and getting great long-term value.

For comparable purposes, BAC shares over the past five years have traded with an average earnings multiple of 11.9x, so we are a good 30% PLUS from that AVERAGE level.

Fast Graphs

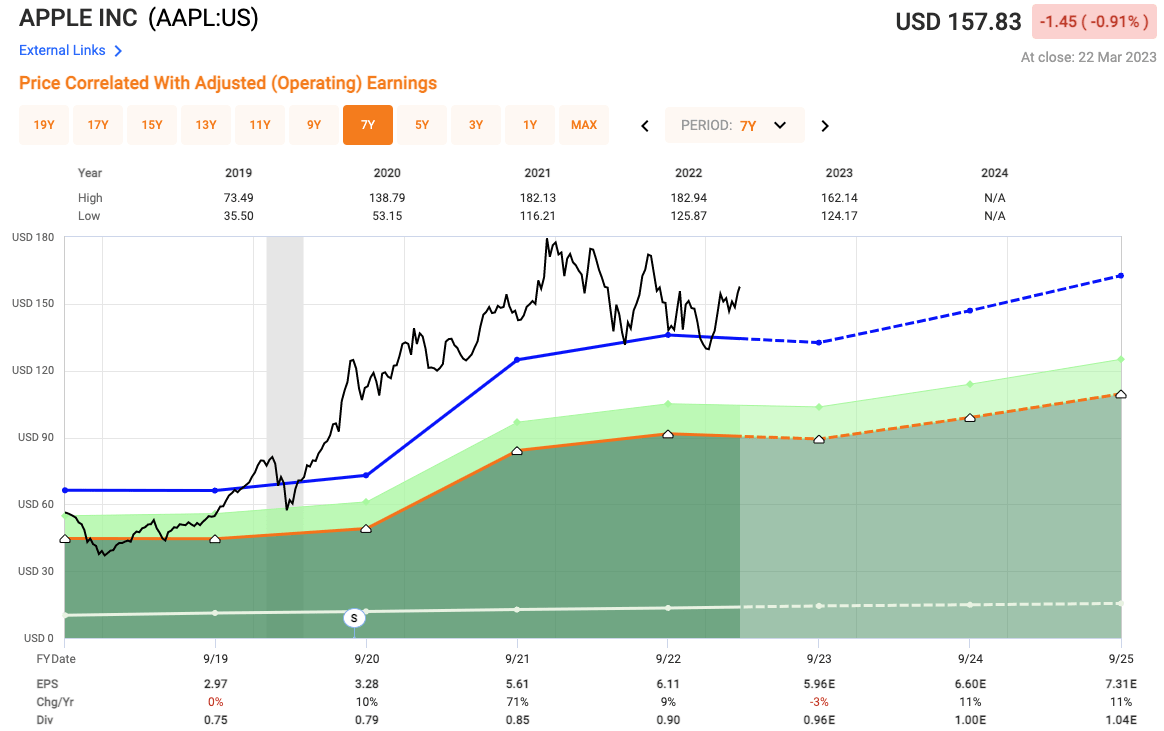

Now let’s take a closer look at Apple, a stock that tends to always grab the headlines. Apple shares have traded at an average multiple of 22.3x over the past five years, which makes sense because a higher multiple usually comes with higher growth and growth potential.

However, when looking at the Fast Graphs chart below, analysts are actually looking for EPS decline by 3% in 2023 to $5.96, which equates to a forward earnings multiple of 26.4x.

Fast Graphs

Now, I understand Apple is very different from Bank of America, but either way, you are paying a 26x multiple of -3% EPS growth? On the flip side, you can pay less than 8x for EPS growth of 10%. Obviously these are estimates, so anything can happen.

Investor Takeaway

Investing in the stock market is about opportunities, and right now, the opportunity we are seeing with Bank of America Corporation looks very intriguing.

Even after a rough year in 2022, some big tech stocks still look expensive. Meanwhile, especially after this mini banking crisis, we are seeing a great opportunity in shares of Bank of America. The crisis has actually helped the company in terms of deposit inflows.

I think we can all agree that at this very moment, shares of Bank of America Corporation look far more compelling from a valuation perspective than some of the larger technology names.

Let me know your thoughts down in the comments below.

Disclosure: I/we have a beneficial long position in the shares of AAPL, BAC either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Additional disclosure: Disclosure: This article is intended to provide information to interested parties. I have no knowledge of your individual goals as an investor, and I ask that you complete your own due diligence before purchasing any stocks mentioned or recommended.