Summary:

- Airbnb’s stock price slid after a short report was issued last week.

- ABNB stock is now flirting with my target price for buying shares.

- Does the short report change the investment thesis? Let’s take a look.

Viktoriya Telminova/iStock via Getty Images

What happened to Airbnb stock last week?

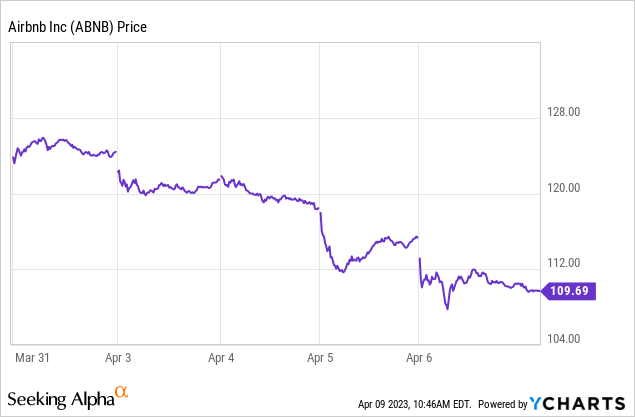

Popular short stock publication The Bear Cave released a report last week detailing what it deems serious issues at Airbnb (NASDAQ:ABNB) that make the stock a poor investment. Airbnb stock was already having a bit of a down week, and this caused an additional 5% slide, as shown below.

The stock was down 10% overall last week. Incidentally, it is approaching the target price I laid out in this recent article.

Excerpt below:

Still, patience could be rewarded in this shaky market. Buying below $102 per share puts the forward P/E ratio under 30, based on consensus estimates. Although I have picked up a few shares recently, this is the level I will more aggressively average into a long-term position.

Should we pay attention to short reports?

Writing negative (“short”) articles on stocks is no fun. Many investors get rightfully nervous when presented with the other side, which often leads to blaming the messenger. So don’t dismiss them out of hand.

Here are two personal examples.

I focus on writing positive articles but have sprinkled in bear cases. The second article I ever published on Seeking Alpha was a sell article on The RealReal (REAL). There was a lot of pushback, but the stock is down 95% since.

Carnival Corporation (CCL) is another company that I am notoriously bearish on. It is down 31% (compared to the S&P 500, down just 2%) since my initial article. The share price will continue to fall as long-term as investors see that higher revenue is not translating to significant positive free cash flow, and more debt or equity financing will be needed.

What’s the point? Being the bearer of bad news isn’t pleasant. When someone makes the bear case, it pays to examine it on its merits.

Does the short report on Airbnb make it a sell?

The Bear Cave’s report boils down to this:

- Profession hosts make up a significant portion of revenues and are going to develop competing platforms; and

- horror stories and Twitter sentiment are turning against the company.

Let’s start with #2.

Horror stories will always be an issue for Airbnb. The math alone says so. The company reported 393 million nights and experiences last year alone. One-hundredth of one percent is more than 39,000 dissatisfied experiences last year alone. This is unavoidable.

I covered this risk in my previous Airbnb article linked above. Airbnb’s introduction and marketing campaign for its AirCover initiative is tremendous. It provides additional liability protection for hosts and security for guests. The initiative shows that Airbnb’s management recognizes this risk and is proactive in coverage and public relations.

Horror stories are true for all large consumer-facing companies, from Amazon (AMZN) to Walmart (WMT), and definitely hotels and other platforms that Airbnb competes with directly.

In terms of pulling sensational posts from Twitter to judge a stock, I will give this all the attention it merits. Let’s move on.

Moving on to #1.

The Bear Cave points out that a few professional property managers make up 23% of available listings in the short-term rental market. This stat is taken from another blog and is not confirmed by Airbnb. However, it is almost certainly true that a significant portion of revenue comes through a small percentage of hosts.

This is true of many businesses, as many analysts have pointed out already. Amazon and Shopify (SHOP) have high-volume sellers, for instance. Many sellers use multiple platforms, including their own, but these companies still dominate the market.

Airbnb’s large hosts compete with the company, and new competing platforms are risky. However, not as significant as the report would have us believe.

The competition may find that operating these platforms is more costly and challenging than it seems. Airbnb has the infrastructure, the means ($9.5 billion in cash and marketable securities), and the reputation to continue dominating the industry.

The short report points to a side-by-side listing where the property manager undercuts Airbnb’s pricing by ~5%. But the competing listing does not offer AirCover protection. For many travelers, including myself, knowing that there is a reputable name behind a booking is definitely worth a small premium.

What’s the bottom line?

Competition is one of the most significant risks to Airbnb. This is true of almost every business – certainly in this industry. Investors should keep a close eye on its effects over time.

However, there is no evidence that Airbnb’s sales are suffering greatly thus far or that hosts or customers are leaving en masse. Revenue was up 40% last year and 75% over 2019. It produced its first GAAP profitable year with an impressive 23% margin, and free cash flow skyrocketed to $2.9 billion on a 35% margin.

Airbnb stock is most appropriate for investors with a multi-year timeline who don’t mind moderate risk and volatility and accumulate shares over time.

Airbnb is in a tremendous position because of its streamlining during the dark days of the pandemic. While other tech companies are seeing shrinking margins and rushing to reduce workforces, Airbnb’s headcount is already 5% below 2019 levels – and business is booming. This means profits, free cash flow, and an enticing opportunity for long-term investors.

Analyst’s Disclosure: I/we have a beneficial long position in the shares of ABNB, AMZN either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.