Summary:

- While the hype has faded, Unity remains an investment on the growth of digital modeling and the meta verse.

- The company is moving beyond its operational issues and is integrating its ironSource acquisition.

- The company has repurchased $1.5 billion of stock.

- I discuss why the forward growth rate is not all that it seems.

We Are

After a protracted period trading at “crashed” prices, Unity Software (NYSE:U) management finally believes that they are moving past the ad monetization headwinds that had plagued the company in the past several quarters. The company has completed $1.5 billion in share repurchases and is positioned to benefit from its now-closed acquisition of ironSource. A slowdown in online advertising due to macro headwinds will undoubtedly hold back U in the near term, but the company has been diversifying outside of the gaming sectors and may benefit from the long term secular tailwinds of 3-D modeling. I continue to find U highly buyable as one awaits further recovery in tech sector valuations.

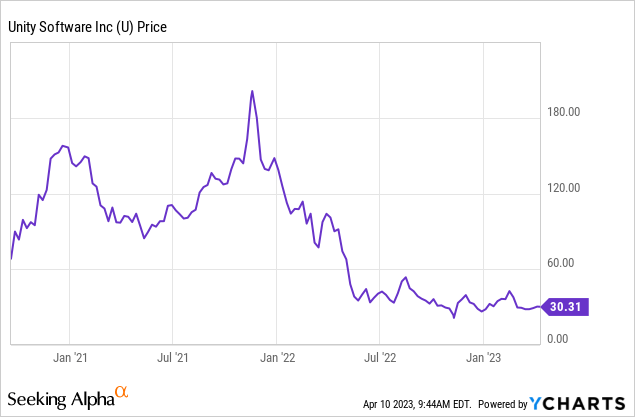

U Stock Price

U was undoubtedly one of the tech bubble poster children as retail investors bid the stock up due to its exposure to the metaverse. The stock has since imploded and has not quite recovered.

I last covered U in February where I rated the stock a buy based on the long term opportunity in the metaverse. The stock has since fallen 16% as turmoil in the banking sector created further flight-to-safety headwinds for the stock price.

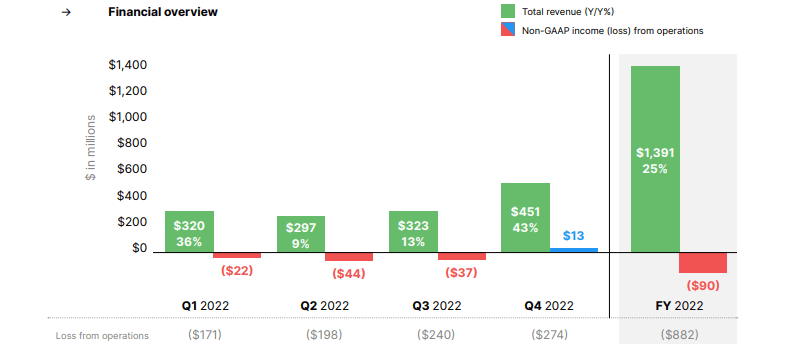

Unity Stock Key Metrics

In the most recent quarter, U delivered 43% YOY revenue growth to $451 million, surpassing guidance of $425 million to $445 million in revenue. The non-GAAP operating margin came in at 3%, at the high end of guidance. That 43% growth rate was a huge acceleration from the 13% posted a quarter prior, but was mostly influenced by the company’s acquisition of ironSource.

2022 Q4 Shareholder Letter

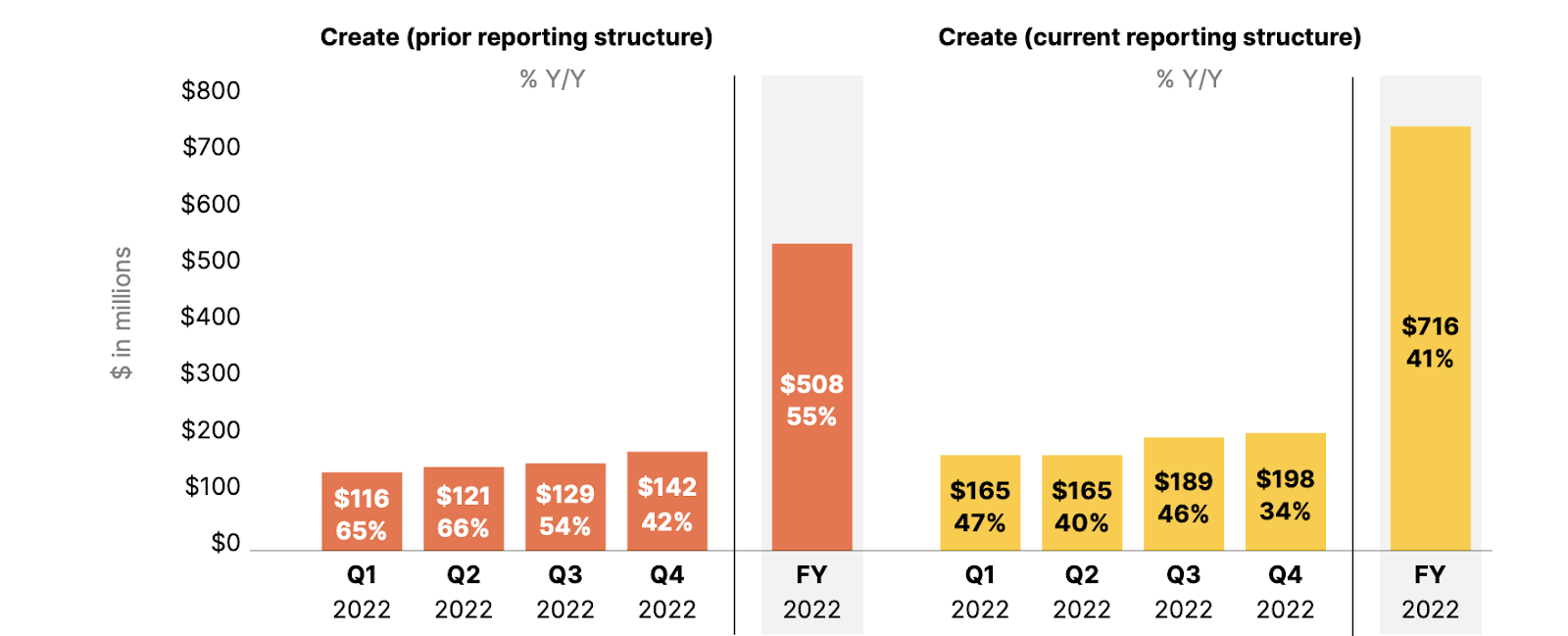

In this quarter, U announced a change to future financial reporting as its Create Solutions segment will now include Unity Gaming Services (previously reported under Operate) and Strategic Partnerships (previously its own segment).

2022 Q4 Shareholder Letter

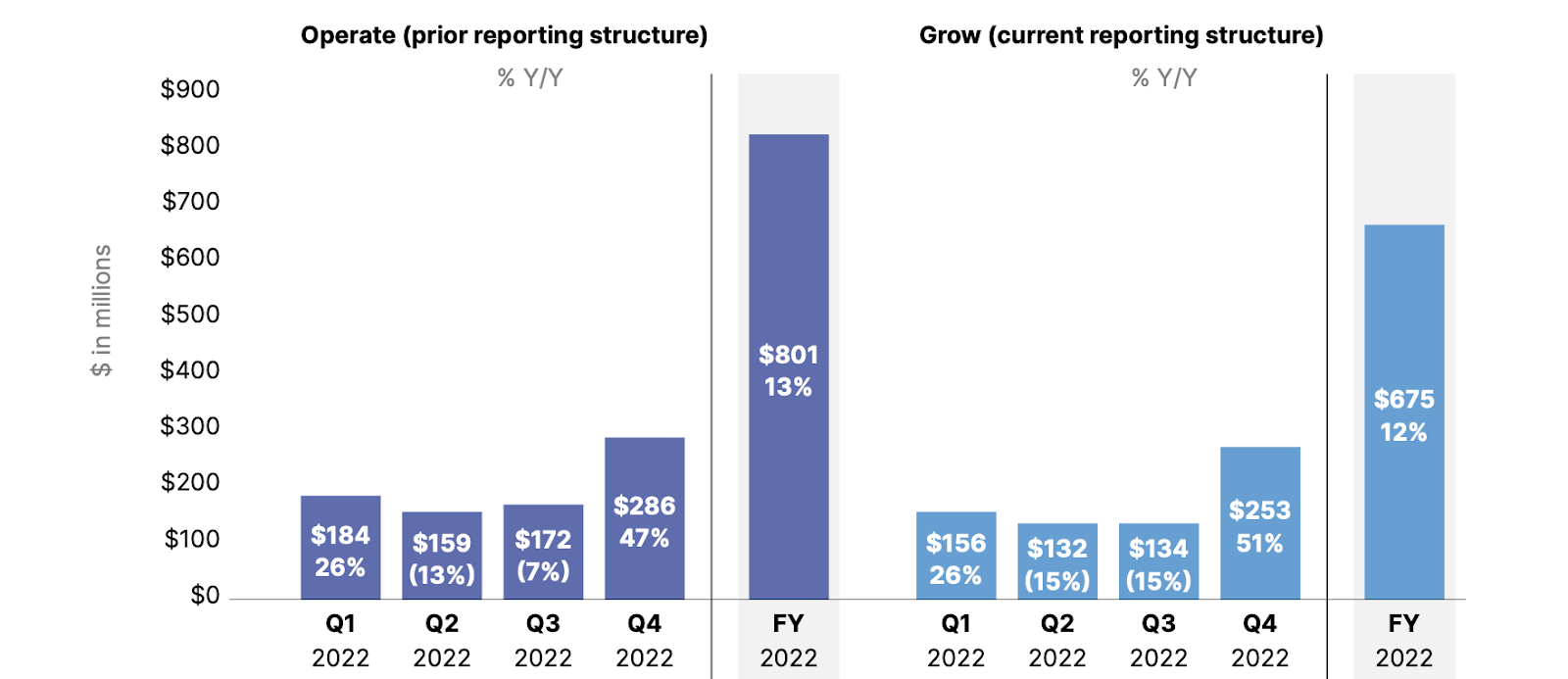

The Operate segment will be renamed “Grow” and will include their advertising products, Supersonic, Aura, and Luna.

2022 Q4 Shareholder Letter

In the fourth quarter, U repurchased 42.7 million shares at an average price of $35.10 per share, totaling $1.5 billion of its $2.5 billion share buyback program. While buybacks are typically bullish for the stock, I question this use of capital considering that the company has a $1.2 billion net debt position, the company is only barely profitable on an adjusted EBITDA basis, and the stock is not obviously cheap relative to tech peers. That said, the stock may prove to be deeply undervalued if management can deliver on long term guidance for sustainable 30% growth.

Looking ahead, management has guided for up to $480 million in revenue in the first quarter, representing 50% YOY growth. But that growth rate may be misleading. The aforementioned ironSource generated $190 million in the 2022 comparable quarter once again implying the bulk of the growth will come from that acquisition. Management has guided for $2.2 billion in revenue and $300 million in adjusted EBITDA, representing a 14% adjusted EBITDA margin. IronSource had previously been guiding for $780 million in 2022 revenue. Combine this with the $1.425 billion in original 2022 revenue guidance for stand-alone-Unity, and 2023 guidance is implying essentially no organic growth.

2022 Q4 Shareholder Letter

On the conference call, management reiterated guidance for “$1 billion in adjusted EBITDA run-rate by the end of 2024.” Management detailed some of its cost-cutting actions as including its near-300 layoff announced in January, as well as paying greater attention to stock-based compensation. Management expects costs to remain “relatively flat during the year.” That is expected to lead to the projected operating leverage and management expects to be profitable (on an adjusted EBITDA basis) every quarter in the year.

Management notes that their guidance is not assuming a quick recovery in the ad market, despite their internal signs showing that there should be one by the end of this year. Management noted that this upcoming quarter will be their toughest comparable because the overall advertising market was up in the “mid-20s” last year, and subsequent quarters will provide easier comps. One thing worth pointing out is that management did not discuss their previous assertions of this being a business which can sustain 30% growth over the long term – but they also did not explicitly retract that guidance.

Is U Stock A Buy, Sell, or Hold?

Consensus estimates seem to have made up their mind regarding that last point, as analysts do not even expect U to sustain 20% growth in the years following 2023. As yet another reminder, 2023 growth rates will be heavily boosted by their acquisition of ironSource.

Seeking Alpha

Based on 493 million fully diluted shares, U is trading at around 6.5x forward sales. If U can sustain 30+% growth rates following 2023, then that multiple would look like a bargain. Based on 30% growth, 30% long term net margins, and a 1.5x price to earnings growth ratio (‘PEG ratio’), fair value might hover at around 13.5x sales, implying well over 100% potential upside over the next 12 months.

But what if growth rates are closer to consensus estimates at around 15%. Based on 15% growth, 30% long term net margins, and a 1.5x PEG ratio, fair value would hover at around 6.8x sales, implying some but far less upside over the next 12 months. The upside here heavily rests on the company’s ability to sustain rapid growth over the long term but investors may need to be patient as there are no shortage of obstacles in the near term.

What are the key risks? Valuation remains the most important risk. During a period in which U is guiding for minimal organic growth in 2023 and consensus estimates are calling for mid-teens growth thereafter, I can see U trading down as much as 50% just to trade in-line with peers of a similar growth cohort. It appears that Wall Street still retains some hope for an acceleration in growth and that explains the current valuation. U has a significant net debt position which has been exacerbated by the $1.5 billion spent on the share repurchase program. If U sees unexpected margin deterioration (perhaps due to a disappointment in top-line numbers), then the company might need to raise cash through dilutive equity offerings or expensive debt financing. It is unclear how much confidence investors should have in management’s long term guidance considering the great uncertainty of the current macro environment and the potential that the company’s growth rates may also be impaired even after the economy improves. I continue to view a basket of undervalued growth stocks as being a top strategy to position ahead of a recovery in the tech sector. U is highly buyable as part of such a basket as the company may benefit from long term secular tailwinds – I reiterate my buy rating.

Analyst’s Disclosure: I/we have a beneficial long position in the shares of U either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

I am long all positions in the Best of Breed Growth Stocks Portfolio.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.

Sign Up For My Premium Service “Best of Breed Growth Stocks”

After a historic valuation reset, the growth investing landscape has changed. Get my best research at your fingertips today.

Get access to Best of Breed Growth Stocks:

- My portfolio of the highest quality growth stocks.

- My best 6-8 investment reports monthly.

- My top picks in the beaten down tech sector.

- My investing strategy for the current market.

- and much more

Subscribe to Best of Breed Growth Stocks Today!